Chapter 2: Comments from the Supplementary Reports Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Committee on Government Vernment Vernment Assurances Assurances

COMMITTEE ON GOGOGOVERNMENT ASSURANCES 85 (20(20(20181818-20-20-20191919))) SIXTEENTH LOK SABHA EIGHTYEIGHTYEIGHTY-FIFTH-FIFTH REPORREPORREPORTTT REQUESTS FOR DROPPING OF ASSURANCES (ACCEDED TO) (Presented to Lok Sabha on 08 January, 2019) LOK SABHA SECRETARIAT NEW DELHI January, 2019/Pausha, 1940 (Saka) EIGHTY-FIFTH REPORT COMMITTEE ON GOVERNMENT ASSURANCES (2018-2019) (SIXTEENTH LOK SABHA) REQUESTS FOR DROPPING OF ASSURANCES (ACCEDED TO) (Presented to Lok Sabha on 08 January, 2019) LOK SABHA SECRETARIAT NEW DELHI January, 2019/Pausha, 1940 (Saka) CGA No. 335 Price: ` 40.00 © 2019 BY LOK SABHA SECRETARIAT Published under Rule 382 of the Rules of Procedure and Conduct of Business in Lok Sabha (Fifteenth Edition) and Printed by the Manager, Government of India Press, Minto Road, New Delhi-110 002. CONTENTS PAGE COMPOSITION OF THE COMMITTEE (2018-2019) ............................................ (iii) COMPOSITION OF THE COMMITTEE (2017-2018) ............................................ (V) INTRODUCTION ........................................................................................... (vii) REPORT ..................................................................................................... 1 APPENDICES-I-IV REQUESTS FOR DROPPING OF ASSURANCES (ACCEDED TO) I. Statement showing summary of requests received from various Ministries/Departments regarding Dropping of Assurances ....... 2 II. SQ No. 321 (Supplementary by Smt. Anupriya Patel, M.P.) dated 16.12.2014 regarding ‘Loss-making PSUs’ .................................. 3 III. Minutes of the sitting of the Committee held on 11 July, 2018 ..... 16 IV. Minutes of the sitting of the Committee held on 04 January, 2019 .... 19 COMPOSITION OF THE COMMITTEE ON GOVERNMENT ASSURANCES* (2018-2019) Dr. Ramesh Pokhriyal “Nishank” — Chairperson MEMBERS 2. Shri Rajendra Agrawal 3. Shri Anto Antony 4. Shri Tariq Anwar 5. Shri E.T. Mohammed Basheer 6. Prof. (Dr.) Sugata Bose 7. Shri Naranbhai Bhikhabhai Kachhadiya 8. -

Medium and Light Engineering

MEDIUM AND LIGHT ENGINEERING Public Enterprises Survey 2013-2014 : Vol-II 189 10. Medium and Light ngineering 11 HMT BEARINGS LTD. 16.33 12.55 As on 31.03.2014, there were 22 Central Public Sector Enterprises 12 HMT CHINAR WATCHES LTD. 0.36 0.36 in the Medium and Light Engineering group. The names of these 13 HMT LTD. 79.71 100.95 enterprises along with their year of incorporation in chronological 14 HMT MACHINE TOOLS LTD. 175.25 239.44 order are given below: - 15 HMT WATCHES LTD. 11.06 11.06 Year of S. No. Enterprise Incorporation 16 I T I LTD. 773.16 922 1 BIECCO LAWRIE LTD. 1919 17 IDPL (TAMILNADU) LTD. 13.44 13.44 2 BALMER LAWRIE & CO. LTD. 1924 18 INSTRUMENTATION LTD. 158.49 172.06 3 I T I LTD. 1950 RAJASTHAN ELECTRONICS AND 19 215.97 239.62 4 HMT LTD. 1953 INSTRUMENTS LTD. RICHARDSON & CRUDDAS(1972) 5 BHARAT ELECTRONICS LTD. 1954 20 66.99 74.16 LTD. 6 INSTRUMENTATION LTD. 1964 21 SCOOTERS INDIA LTD. 194.35 209.82 7 ELECTRONICS CORPN. OF INDIA LTD. 1967 22 VIGNYAN INDUSTRIES LTD. 36.75 27.47 8 BHARAT DYNAMICS LTD. 1970 TOTAL : 14982 14496.11 9 BHARAT PUMPS & COMPRESSORS LTD. 1970 10 HINDUSTAN CABLES LTD. 1972 5. 1HW 3UR¿W /RVV The details of enterprises, which earned 11 RICHARDSON & CRUDDAS(1972) LTD. 1972 QHW SUR¿W RU VXVWDLQHG QHW ORVV DUH JLYHQ EHORZ 12 SCOOTERS INDIA LTD. 1972 (` in Crore) 13 CENTRAL ELECTRONICS LTD. 1974 1HW 3UR¿W /RVV 14 ANDREW YULE & COMPANY LTD. -

Annual Report 2019-2020

ANNUAL REPORT 2019-2020 Administrative Staff College of India Bella Vista : Hyderabad July 22, 2019: Inauguration of the Post Graduate Diploma in Management (PGDM) byShri Jayesh Ranjan , IAS, Principal Secretary, Government of Telangana, considered as a red letter day in the history of ASCI January 31, 2020: Shri K.Taraka Ramarao, a dynamic July 11, 2019: The two-year Post Graduate Diploma in Minister in Telangana government, and Shri K.Padmanabhaiah, Management (PGDHM) students with military background ASCI Chairman, during INK@WASH conference in Hyderabad exchanging pleasantries with the ASCI Chairman Shri K.Padmanabhaiah and the Healthcare Management Centre Director Dr Subodh Kandhamuthan April 29, 2019:World renowned Radiologist Shri Kakarla Subba Rao April 5, 2019: The British Deputy High Commissioner interacting with doctors after delivering a lecture on HE Andrew Fleming at a programme organized in Bella Vista to importance of Public Relations in hospitals in Bella Vista mark the International Day of Sport for Development and Peace Leadership through Learning ANNUAL REPORT 2019–2020 Administrative Staff College of India Bella Vista : Hyderabad Contents Chairman's Statement 5 Governance of the College 9 Academic Activities 10 Activities of the Centres 19 Statement of Accounts 27 Statement of Accounts (CIPS) 41 Annexures 1. Members of the College Society 57 2. Court of Governors 59 3. Personnel 61 4. Management Development Programmes 66 5. Research and Management Studies (A, B & C) 75 6. Endowed and Public Lectures 89 63rd ANNUAL REPORT 2019–2020 Chairman’s Statement On behalf of the Court of customized training programmes were conducted for the Governors, I have pleasure in benefit of more than 2500 participants. -

Top Public Sector Companies

Top Public Sector Companies Air India Bharat Coking Coal Limited Bharat Dynamics Limited Bharat Earth Movers Limited Bharat Electronics Limited Bharat Heavy Electricals Ltd. Bharat Petroleum Corporation Bharat Refractories Limited Bharat Sanchar Nigam Ltd. Bongaigaon Refinery & Petrochemicals Ltd. Broadcast Engineering Consultants India Ltd Cement Corporation of India Limited Central Warehousing Corporation Chennai Petroleum Corporation Limited Coal India Limited Cochin Shipyard Ltd. Container Corporation Of India Ltd. Cotton Corporation of India Ltd. Dredging Corporation of India Limited Engineers India Limited Ferro Scrap Nigam Limited Food Corporation of India GAIL (India) Limited Garden Reach Shipbuilders & Engineers Limited Goa Shipyard Ltd. Gujarat Narmada Valley Fertilizers Company Limited Haldia Petrochemicals Ltd Handicrafts & Handloom Exports Corporation of India Ltd. Heavy Engineering Corp. Ltd Heavy Water Board Hindustan Aeronautics Limited Hindustan Antibiotics Limited Hindustan Copper Limited Hindustan Insecticides Ltd Hindustan Latex Ltd. Hindustan Petroleum Corporation Ltd. Hindustan Prefab Limited HMT Limited Housing and Urban Development Corporation Ltd. (HUDCO) IBP Co. Limited India Trade Promotion Organisation Indian Airlines Indian Oil Corporation Ltd Indian Rare Earths Limited Indian Renewable Energy Development Agency Ltd. Instrumentation Limited, Kota Ircon Internationl Ltd. ITI Limited Kochi Refineries Ltd. Konkan Railway Corporation Ltd. Krishna Bhagya Jala Nigam Ltd Kudremukh Iron Ore Company Limited Mahanadi -

List of Government Companies in Tamilnadu List of Central

List of Government companies in Tamilnadu Central Govt Public Sector Units in TN: * Neyveli Lignite Corporation Limited (NLC), Chennai * Bharat Heavy Electrical Limited (BHEL), Trichy * Chennai Metro Rail Limited (CMRL), Gopalapuram, Chennai * Chennai Petroleum Corporation Ltd. (CPCL), Chennai * Nuclear Power Corporation of India Limited (NPCIL), Kancheepuram * National Textile Corporation Limited (NTCL), Coimbatore * Bharatiya Nabhikiya Vidyut Nigam Ltd., Chennai * Ennore Port Ltd., Chennai * Hindustan Photo Films Manufacturing Co. Ltd., Ootacamund * Madras Fertilizers Limited, Chennai * Sethusamudram Corpn. Ltd., Chennai * Tamil Nadu Trade Promotion Organisation, Chennai * United India Insurance Company, Chennai * RailTel Corporation of India Limited, Chennai Tamil Nadu Government Organizing Industries: * Tamil Nadu Newsprint and Papers Limited (TNPL) * Tamil Nadu Cement Corporation Limited (TANCEM) * Tamil Nadu Magnesite Limited (TANMAG) * Tamil Nadu Industrial Explosives Limited (TEL) * Tamil Nadu Minerals Limited (TAMIN) * Tamil Nadu Small Industries Corporation Limited (TANSI) * Tamil Nadu Co-operative Sugar Federation (TNCSF) * Tamil Nadu Salt Corporation Limited (TNSC) * Southern Structurals Limited (SSL) * Tamil Nadu Paints And Allied Products Limited (TAPAP List of Central Government Companies DEPARTMENT OF ATOMIC ENERGY 1. Electronics Corporation of India Limited (R&S) 2. Indian Rare Earths Limited (R&S) 3. Nuclear Power Corporation of India Limited (R&S) 4. Uranium Corporation of India Limited (R&S) MINISTRY OF CHEMICALS & -

APPENDIX –XII (Referred to in Para No

APPENDIX –XII (Referred to in Para No. 4.11) SALES, PROFIT PER EMPLOYEE Sector and Name of the Company Sales per Profit per Ratio of Employee employee Labour cost to Total Cost (Rs. in lakh) Agro based Industries 1. Andaman & Nicobar Islands Forest and Plantation 0.41 -0.39 0.92 Development Corporation Limited 2. National Seeds Corporation Limited 8.38 0.87 0.28 3. The State Farms Corporation of India Limited 2.91 -0.35 0.74 Chemicals & Petrochemicals 4. Hindustan Organic Chemicals Limited 25.00 -2.63 0.12 5. Karnataka Antibiotics and Pharmaceuticals 14.03 0.83 0.16 Limited 6. Rajasthan Drugs and Pharmaceuticals Limited 11.59 0.80 0.19 7. Hindustan Insecticides Limited 8.40 -1.31 0.24 8. Bengal Chemicals and Pharmaceuticals Limited 3.85 0.95 0.27 9. Hindustan Fluorocarbons Limited 7.45 -4.63 0.16 10. Smith Stanistreet Pharmaceuticals Limited 0.01 -7.61 0.97 11. Indian Medicines and Pharmaceuticals Corporation 3.04 0.48 0.37 Limited 12. Bengal Immunity Limited 0.06 -7.03 0.95 13. Bharat Immunologicals and Biologicals 17.13 -4.28 0.10 Corporation Limited 14. Hindustan Antibiotics Limited 6.13 -0.45 0.13 15. UP Drugs and Pharmaceuticals Company Limited 7.28 5.08 0.20 Coal & Lignite 16. Eastern Coalfields Limited 2.55 -0.29 0.65 17. Central Coalfields Limited 4.23 0.48 0.54 18. Neyveli Lignite Corporation Limited 14.63 7.32 0.30 19. Coal India Limited 2.58 28.09 0.41 20. -

Review of Aob Rules, 2010

Review of AoB Rules, 2010. NAME OF MINISTRY/DEPTT. : MINISTRY OF AGRICULTURE D/O AGRICULTURE AND COOPERATION S. EXISTING ENTRIES PROPOSED CHANGES Reasons for change if any, No. provided by the Ministry/Department. 1. Part-I 1. Liaison with international Agri-organisations like Food & 1. CARE is now defunct as far as 1. Liaison with International Agri- Agriculture Organisation of the United Nations, India is concerned. Organisations like Food and Agriculture “International Plant Protection Convention (IPPC), World 2. International Plant Protection Organisation of the United Nations, handling of Food Programme and facilitating operations associated Convention is a new entry. CARE goods concerning agriculture, etc. with it”. 2. Part-I 2. Participation in international conferences, associations and Deptt. of Agri. & Coopn. in 2. Participation in international conferences, other bodies concerning agriculture and coordination of Ministry of Agriculture is the associations and other bodies concerning matters relating to bilateral and multilateral cooperation nodal Department for coordination agriculture and implementation of decisions in Ministry of Agriculture and promoting national in bilateral and multilateral made thereat. profiles/interests abroad through agriculture in cooperation. Achievements in the consultation with Ministry of External Affairs and field of agriculture are well implementation of decisions made thereat . recognized and many Afro-Asian countries look up to India for guidance/ assistance. 3. Part-I 5(a). Development of -

![[ 19 DEC. 1985 ] on the Table 146 Report on the Accounts And](https://docslib.b-cdn.net/cover/1863/19-dec-1985-on-the-table-146-report-on-the-accounts-and-3281863.webp)

[ 19 DEC. 1985 ] on the Table 146 Report on the Accounts And

145 Papers Laid [ 19 DEC. 1985 ] on the Table 146 Report on the Accounts and comments of II (a) Annual Report and Accounts of the Comptroller and Auditor General of the Indian National Science Academy, India thereon. New Delhi, for the year 1984 o5, together with the Auditors Report on the (b) Statement by Government Accounts. accepting the above Report. [Placed in Library. See No. LT— Ob) Statement by Government 1686/35 for (a) and (b)]. accepting the abovs Report. [Placed in Library. See No. LT— IV. (a) Thirty-first Annual Report . and 1692/85 for (a) and (b)]. Accounts of the National Research Development Corporation of India, New III. (a) Annual Repoit and Delhi, for the year 1984-S5, together with the Accounts of the Tata Memorial Auditors' Report on the Accounts and Centre, Bombay, for the year comments of the Comptroller and Auditor 1984-85, together with the Audi General of India thereon. tors' Report or. the Accounts. (b) Statement by Government (b) Statement by Government accepting the above Report. accepting the above Report. [Placed in Library. See No. LT— [Placed in Library. See No. LT— 1916/85 for (a) and (b)]. 1691/85 for (a) and (b)]. V. (a) . Thirty-fifth Annual Report IV. (a) Annual Report and and Accounts of the Indian Rare Earths Accounts of the Raman Research Limited. Bombay, for the year 1984-85, Institute, Bangalore, for the pear together with the Auditors' Report on the 1984-85, together with the Audit Accounts and comments of the Report on the Accounts. Comptroller and Auditor General of (b) Statement by Government India thereon. -

SL No. Folio NO./ DPID and Client ID No. Name of the Member Address of the Member Number of Shares 1 0000002 H C ASTHANA 17

BALLARPUR INDUSTRIES LIMITED DETAILS OF THE MEMBERS AND SHARE FOR TRANSFER TO THE INVESTOR EDUCATION AND PROTECTION FUND SL Folio NO./ DPID Name of the Member Address of the Member Number of No. and Client ID No. Shares 1 0000002 H C ASTHANA 17, SAIFABAD, HYDERABAD-DN. 30 2 0000003 RAFIQ BEG THE PRAGA TOOLS CORPN. LTD., ALEXANDRA 30 ROAD, SECUNDARABAD. 3 0000006 K M HAMEEDA C/O. K.B. MAQSOOD HUSSAIN, BADAUN, 30 4 0000007 V K DHAGE PODAR CHAMBERS, PARESEE BAZAR STREET, 30 FORT, BOMBAY 5 0000020 PUTHENCHERI GOPALAN NAIR SUPERINTENDENT, P.W.D. M.P. RETD P.O. 75 TIRUVEGAPPURA, KERALA STATE 6 0000029 S ABDUL WAHIB 5, OLD TRANQUEBAR STREET, KARIKAL, SOUTH 63 7 0000051 HALIMABAI C/O. IQBAL STORES, IQBAL MANZIL, RESIDENCY 975 ROAD, NAGPUR. 8 0000066 GOBIND RAM THAKURDAS WADHWANI 48, HAZRAT GANJ LUCKNOW. 3 9 0000067 RAMBHAU BANGDE C/O BHARATI SAW & RICE MILLS, EKORI WARD, 72 BINBA ROAD, CHANDRAPUR, M.S. 10 0000083 S J KHARAS NO.5,JEERA COMPOUND, KINGSWAY, 9 11 0000091 VATSALABAI MANDPE C/O. SHRI D.W. MANDPE, HINDUSTHAN OIL MILLS, 657 GHAT ROAD, NAGPUR. 12 0000098 SAMUEL JOHN NETURIA COAL CO./P/ LTD., P.O. NETURIA, DIST. 192 13 0000102 JAGJIT SINGH PAUL C/O.M/S. BANWARILAL AND CO LTD QUEENS 1,566 MANSIONS, BASTION ROAD FORT BOMBAY 14 0000122 GOTETI RADHA KRISHNA MURTY KUCHMANCHIVANI AGRAHARAM, AMALAPURAM, 30 DT. EAST GODAVARI. 15 0000124 K ANASUYA C/O P PATHU RAJU KEAVEKALKURGUMME 3 GUDDE,CIRCAR THOTA MACHLIPATTAM,KRISHNA 16 0000127 VENGARA RADHAKRISHNA MURTY 4-61/10 DILSHUKHNAGAR HYDERABAD 78 17 0000129 BALWANT SINGH AGRICULTURAL ASSISTANT, 85, MODEL TOWN, 192 18 0000131 GANGABAI MAHADEORAO JOGLEKAR JOGLEKAR WADA, GANJIPURA, JABALPUR. -

Indian Geography

INDIAN GEOGRAPHY PHYSIOGRAPHY “Fastest Continent” India is the largest country in the Indian subcontinent lying India is entirely contained on the Indian Plate, a major tectonic entirely in the Northern Hemi- plate that was formed when it split off from the ancient continent Gondwanaland. About 50 to 55 million years ago, in the Eocene sphere. epoch of the Cenozoic Era, the plate collided with Asia after The mainland extends from lati- covering a distance of 2,000 to 3,000 km (1,243 to 1,864 miles), tude 8°4’ north to 37°6’ north having moved faster than any other known” This plate. is causing India is thethus and from longitude 68° 7’ east “fastest continent. referred to as the to 97°25’ east. Eurasian Plate to deform, and the India Plate to compress at a The southernmost point in In- rate of 4 mm/yr (0.15 in/yr). dian territory, the Indira Point is situated at 6°30’ north in the The Indian mainland can be divided into Nicobar Islands. five physiographic units namely India stretches 3,214 km from i. The Great Mountains of the North north to south and 2,933 km ii. The North Indian Plains from east to west. The total length of the main- iii. The Peninsular Plateau land coastline is nearly 6,100 iv. The Coastal Plains km and that of the land frontier v. The Islands is about 15,200km. The total length of the coastline includ- dence, the country was divided bicameral legislatures. Legis- ing that of the islands, is about into hundreds of small states lative power is distributed be- 7,500 km. -

Surging Ahead After the 'Golden Journey'

Surging ahead after the ‘Golden Journey’ 50th Annual Report 2013-14 The now 50 years strong Institute of Public Enterprise has had a promising academic year 2013-14, witnessing the Golden jubilee celebrations on one side and the spurt of research and academic activities on the other. IPE is proud in presenting its 50th Annual Report to all its stake holders. Highlights of the year ..............................................................................14 Research & Consultancy projects ...........................................................18 Completed projects Ongoing projects Centers of research .................................................................................23 Research publications during the year ...................................................29 Doctoral Programme ...............................................................................33 National and International Conferences .................................................36 Contents Training programmes ..............................................................................41 Golden Jubilee Distinguished lectures ....................................................47 Distinguished Visitors to IPE ...................................................................51 Management Education Programs ..........................................................55 Student Activities for the year 2013-14 ...................................................58 Financial Statements 2013-14 .................................................................65 -

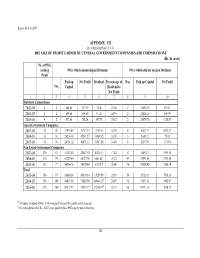

Appendix Vii Details of Profit Earned by Central

Report No.9 of 2007 APPENDIX VII (As referred in Para 1.3.3.1 ) DETAILS OF PROFIT EARNED BY CENTRAL GOVERNMENT COMPANIES AND CORPORATIONS (Rs. in crore) No. of PSUs earning PSUs which declared/paid Dividend PSUs which did not declare Dividend Profit Paid up Net Profit Dividend Percent-age of Nos. Paid up Capital Net Profit Nos. Capital Dividend to Net Profit 1 2 3 4 5 6 7 8 9 10 Statutory Corporations 2003-04 4 2 484.65 337.39 74.08 21.96 2 12625.29 963.81 2004-05 4 2 499.65 366.69 91.48 24.95 2 21014.15 658.90 2005-06 4 2 517.65 788.24 157.78 20.02 2 25874.78 1128.07 Listed Government Companies 2003-04 32 28 17939.49 33713.83 11109.35 32.95 4 6002.71 2612.33 2004-05 36 30 24264.63 45341.37 14969.35 33.01 6 1648.12 79.93 2005-06 36 30 24331.12 42891.13 14945.28 34.84 6 2267.96 373.94 Non Listed Government Companies 2003-04 120 67 51382.55 22587.92 4024.51 17.82 53 16492.13 3959.16 2004-05 118 74 61255.40 26117.98 5543.40⊕ 21.22 44 12991.04 2753.84 2005-06 135 77 64364.16 28658.40 8155.93£ 28.46 58 19628.40 5586.74 Total 2003-04 156 97 69806.69 56639.14 15207.94 26.85 59 35120.13 7535.30 2004-05 158 106 86019.68 71826.04 20604.23⊕ 28.69 52 35653.31 3492.67 2005-06 175 109 89212.93 72337.77 23258.99£ 32.15 66 47771.14 7088.75 ⊕ Excludes dividend of Rs.11.74 crore paid by one PSU partly out of reserves.