Office Market Overview Mid Year 2017 Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brickell Retail/Restaurant Spaces Available Contact Us

Brickell Retail/Restaurant Spaces Available Contact us: BRICKELL ARCH | 1395 BRICKELL AVENUE | MIAMI, FL 33131 Jonathan Carter Executive Managing Director Colliers International is pleased to offer the opportunity to lease retail/ +1 786 517 4971 restaurant spaces on the ground floor of Brickell Arch, a 36-story [email protected] mixed-use project that features over 268,000 SF of class “A” office space and the 203-room Conrad Hotel. Jenny Gefen Director +1 786 517 4974 FEATURES [email protected] • Adjacent to JW Marriott Hotels and The Four Seasons Kirk Fetter • 980 car attached parking garage with on-site valet +1 786 999 8003 • Large outdoor seating area and lobby courtyard access [email protected] AVAILABILITY SPACE 1 SPACE 2 SPACE 3 Colliers International ± ± ± South Florida, LLC 4,538 SF 758 SF 2,594 SF 801 Brickell Avenue, Suite 850 Miami, FL 33131 GROUND FLOOR SPACE 1 ±4,538 SF SW 14TH STREET Jonathan Carter Jenny Gefen Kirk Fetter Executive Managing Director Director +1 786 999 8003 +1 786 517 4971 +1 786 517 4974 [email protected] [email protected] [email protected] Outdoor Patio Small Brickell Retail/Restaurant Spaces Available GROUND FLOOR VALET Space 1: ± 758 SF Space 2: ± 2,594 SF Lobby Total: 3,352 SF Brickell Avenue ± BRICKELL AVENUE BRICKELL Situated on the ground floor of Brickell Arch and supported by the Conrad Hotel, a 36 story mixed-use tower with over 268,000 SF of class “A” office space and 203 hotel rooms SPACE 3 SPACE 2 ±2,594 SF 980 car attached parking garage with on- ±±758 -

Macy's Redevelopment Site Investment Opportunity

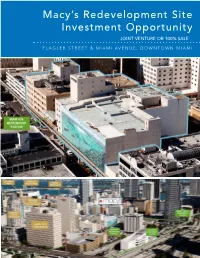

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

Luxury Homebuyers Pay a Premium for Residences with Livable Outdoor Spaces, So Architects and Builders Have Become Creative in Accommodating Those Preferences

T H E G RE AT OUTDOORS Luxury homebuyers pay a premium for residences with livable outdoor spaces, so architects and builders have become creative in accommodating those preferences. By Roger Grody “I think a lot of developers are doing a great job in transforming tight spaces into little paradises.” Brickell City Centre’s luxurious penthouses spill onto expansive terraces accommodating outdoor kitchens, plunge pools and spas. ivable outdoor space has long been an in Greater Miami, reports that properties with There are few places in the country Market (SoMa) district, architect Jeffrey Heller A three-bedroom penthouse at 181 architect Renzo Piano, is slated for completion essential element of luxury residential outdoor spaces sell at a premium. “I think a lot of that are as exciting from both a real estate and has capitalized on the neighborhood’s newest Fremont sold for $15 million last summer, setting later this year. Not only will it offer sprawling L architecture, so even in areas where land developers are doing a great job in transforming lifestyle perspective as San Francisco, but the SWIRE PROPERTIES COURTESY PHOTO recreational asset. Although there are no private a new price-per-square-foot record (more than common areas fully integrated with an adjoining is increasingly scarce, such as revitalized city tight spaces into little paradises,” Rein says. “If compact city with extraordinarily high land costs balconies, 181 Fremont is loaded with communal $4,500) for condos in San Francisco, and a full- 35-acre park, but generous recreational spaces centers or overdeveloped coastlines, that coveted you have a spacious balcony, the indoor-outdoor has always forced designers of luxury residences recreation space and enjoys direct access to an floor, 6,941-square-foot penthouse was originally within each of the 70 high-end residences. -

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna Businesses searching for space in Miami's urban core have more options than they might think. While vacancy rates are down across the board, significant chunks of space are available in several Class A buildings in downtown and the Brickell Avenue financial district. "There are more alternatives available for those companies that take the time to appropriately investigate the market," said Chris Lovell, a senior managing director with Savills Studley in Miami. Leasing space on an upper floor with a view may be difficult since only six buildings on Brickell have a full floor above the 20th story available for lease. For tenants that can live without the view, there is plenty of open space to choose from. Four downtown Class A buildings have at least 75,000 square feet of contiguous space available, one Class A building on Brickell has a 65,000- square-foot block — "and we don't have tenants of that size standing in line to the claim the space," Lovell said. Savills Studley has found many of the large available blocks are in older downtown buildings. "You're always going to have buildings that are going to have certain pockets available," said Tere Blanca, founder of Miami-based Blanca Commercial Real Estate Inc. She said the market is responding well to the new Miami Central project, which is under construction with 60 percent of its office component pre- leased. The mixed-use development will serve as Brightline's downtown train station and will add 286,000 square feet of office space in two buildings. -

OFFERING MEMORANDUM Miami, FL 33131 235 SE 1St Street Themiamiplaza.Com

THE P LA ZA themiamiplaza.com MEMORANDUM 235 SE 1st Street Miami, FL 33131 OFFERING THE P LA ZA THE P LA ZA 235 SE 1st Street THE OFFERING Miami, FL 33131 he Plaza is a 81,000 SF office building Ton a 20,000 SF corner lot located in the heart of Downtown Miami and its most prominent corner. The site benefits from the most liberal mixed-use zoning in all of South Florida, T6-80-O, allowing up to 489,600 SF of development and 470 residential units. The Plaza is an amazing add value office building with tremendous future uses for development. Developers will benefit from the ability to receive temporary cash flow while waiting on the next cycle or plan approval. THE CORNER OF DOWNTOWN MIAMI THE P LA ZA PROPERTY SUMMARY + + Address: Lot Size: Building Size: Zoning: FLR Allowable FLR Allowable +Bonus Building Height: Building Height +Bonus: Allowable Units: Folio: 235 SE 1st St. 20,400/ 81,382 SF T6-80-O 489,600 SF Unlimited 80 Unlimited 470 01-0112-000-1020 Miami, FL 33131 0.47 Acres 6 7 FOUR SEASONS BRICKELL CITY INVESTMENT CENTRE ICON BRICKELL HIGHLIGHTS SOUTHEAST FINANCIAL CENTER WELLS FARGO CENTER MIAMI TOWER ASTON MARTIN JAMES L. KNIGHT RESIDENCES CENTER MET SQUARE CINEPLEX WHOLE FOODS CENTRO Covered Land with In-Place Income he Plaza is a prime opportunity to repurpose or add value to an existing Tclass C office building located in Downtown’s most highly trafficked corridor. The property is positioned to capture an already active-large tenant base with over 175,000 employees existing within Downtown’s LA EPOCA Central Business District. -

Miami Cbd Large Blocks of Office Space

RESEARCH MIAMI CBD AUGUST 2019 LARGE BLOCKS OF OFFICE SPACE 836 MACARTHUR CAUSEWAY 100,000+ SF Blocks 395 Southeast Financial Center Four Seasons Tower 200 S Biscayne Boulevard 1441 Brickell Avenue Ponte Gadea USA 9 Millennium Partners Management 1 1,225,000 RBA – 67.8% Leased 258,767 RBA – 98.1% Leased 133,120 SF Max Contig. 28,763 SF Max Contig. $53.25/RSF FS $60.00/RSF FS Citigroup Center 1221 Brickell 201 S Biscayne Boulevard 1221 Brickell Avenue Crocker Partners Rockpoint Group 2 809,594 RBA – 74.0% Leased 10 408,649 RBA – 86.1% Leased 95 127,634 SF Max Contig. 26,761 SF Max Contig. $48.00-$52.00/RSF FS $52.50/RSF FS Freedom PORT BLVD A1A Tower Wells Fargo Center 50,000 - 99,999 SF Blocks 333 SE 2nd Avenue AVE MetLife Real Estate Investments AVE 11 ND 752,845 RBA – 85.9% Leased ND SunTrust International Center 26,000 SF Max Contig. 1 SE 3rd Avenue BISCAYNE BLVD BISCAYNE $48.00/RSF FS N MIAMI AVE MIAMI N 2 NE NW 2 NW MiaMarina Pacific Coast Capital Partners MIAMI RIVER 3 440,299 RBA – 66.4% Leased 90,255 SF Max Contig. $38.00-$40.00/RSF FS 15,000 - 24,999 SF Blocks Brickell Office Plaza Brickell World Plaza Downtown 777 Brickell Avenue 600 Brickell Avenue 8 Padua Realty Company Elm Spring, Inc. 4 288,457 RBA – 74.8% Leased 12 631,866 RBA – 92.5% Leased 3 6 68,386 SF Max Contig. CLASS 24,138 SF Max Contig. -

Echo Brickell

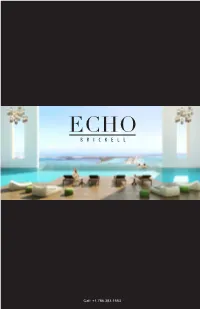

ECHO BRICKELL ECHO BRICKELL Call: +1.786.383.1553 Call: +1.786.383.1553 ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. OBTAIN THE PROPERTY REPORT REQUIRED BY FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE , IF ANY, OF THIS PROPERTY . EAST/SOUTHEAST VIEW VIEWS ACTUAL VIEWS MAY VARY AND CANNOT BE GUARANTEED. VIEWS SHOWN CANNOT BE RELIED UPON AS THE ACTUAL VIEW FROM ANY PARTICULAR UNIT WITHIN THE CONDOMINIUM. ORAL REPRESENTATIONS CAN- NOT BE RELIED UPON AS CORRECTLY STATING REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. OBTAIN THE PROPERTY REPORT REQUIRED BY FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE, IF ANY, OF THIS PROPERTY. OVERVIEW ECHO Brickell is a boutique residential high-rise in the epicenter of Miami’s fastest growing metropolitan neighborhood, located on the coveted East side of Brickell Avenue. Echo Brickell’s 157 state-of-the-art residences redefine opulent living in Miami’s most exciting locale. With conceptual design from mastermind Carlos Ott, ECHO Brickell is a host of privilege at every turn. Echo Brickell’s interiors introduce an exciting new concept to the world - fusing world renowned architect, Carlos Ott and yoo design studio, in a first time collaboration to create a limited edition collection: Carlos Ott + yoo . -

Academic Catalog 2016-2017

ACADEMIC CATALOG 2016-2017 Brown Mackie College – Miami Main Campus 3700 Lakeside Drive Miramar, FL 33027 Brown Mackie College – Miami Bayfront Plaza –Learning Site 100 South Biscayne Boulevard, 5th Floor Miami, FL 33131 Phone: 305-341-6600 Fax: 954-624-9712 Toll free: 866-505-0335 www.brownmackie.edu Volume #1 Effective: January 2016 In order to continually provide current information, this catalog may be amended by any inserts identified as Bulletins to the 2016-2017 Academic Catalog. Such bulletins are intended as, and are to be regarded as, an integral part of this catalog. See bmcprograms.info for program duration, tuition, fees, and other costs, median debt, salary data, alumni success, and other important info. TABLE OF CONTENTS CONSUMER INFORMATION ............................................................................................................................................. 1 ABOUT THE COLLEGE ...................................................................................................................................................... 1 COLLEGE MISSION AND PURPOSE ................................................................................................................................ 2 Mission Statement ............................................................................................................................................................. 2 General Education Philosophy .......................................................................................................................................... -

Welcome to Kaplan Medical

Welcome to Kaplan Medical 4425 Ponce De Leon, #1612 Coral Gables, FL 33146 Miami Kaplan Center 4425 Ponce De Leon Boulevard Suite 1612 Coral Gables, FL 33146 Hours of Operation Monday-Thursday 9am - 9pm Friday-Sunday 10am - 5pm (305) 441-5323, Ext. 5000 or 5002 2 Our Neighborhood Coral Gables: Coral Gables’ founders imagined both a “City Beautiful” and a “Garden City,” with lush green avenues winding through a residential city, punctuated by civic landmarks and embellished with detailed and playful architectural features. Known as The City Beautiful, Coral Gables stands out as a planned community that blends color, details, and the Mediterranean Revival architectural style. International: From its inception, Coral Gables was designed to be an international City, and is now home to more than 20 consulates and foreign government offices and more than 140 multinational corporations. As early as 1925, City Founder George Merrick predicted Coral Gables would serve as "a gateway to Latin America." To further establish international ties, the City has forged relationships with six Sister Cities: Aix-en Provence, France; Cartagena, Colombia; Granada, Spain; La Antigua, Guatemala; Province of Pisa, Italy; and Quito, Ecuador (emeritus). 3 Our Neighborhood University of Miami: The University of Miami is located in Coral Gables Shopping: Coral Gables attracts national and regional retailers along with an abundance of boutiques and retail shops. Miracle Mile is the center of a true downtown district. Located across the street from the Kaplan Medical Center in Coral Gables is “The Village of Merrick Park”, a 780,000 square foot retail, residential and office project anchored by Neiman Marcus and Nordstrom, and has more than 100 other select retailers including Tiffany & Co., Burberry, Coach and Gucci. -

Swire Properties Inc, Receives Temporary Certificate of Occupancy for RISE Luxury Condominium Tower at Brickell City Centre

Swire Properties Inc, Receives Temporary Certificate of Occupancy for RISE Luxury Condominium Tower at Brickell City Centre Media Selects- https://w e.tl/Pw ZOlO66rq MIAMI (Se ptember 13, 2016) – The City of Miami has granted Swire Properties Inc, one of South Florida’s leading international developers of urban real estate, a temporary certificate of occupancy (TCO) for Brickell City Centre’s second residential tower, RISE. The grant will officially allow residents to move into their new homes. Receiving this certification marks a final stage of completion for REACH and RISE, finalizing the TCO process for both luxury residential towers. Located in the heart of Brickell, the landmark $1.05 billion Brickell City Centre offers residents a unique work, live, play lifestyle with over nine acres of meticulous urban planning and award-winning inspirational design. The project continues to remain popular amongst U.S and international buyers, with prices starting from $595,000 to $2.7 million and penthouse prices provided upon request. “Receiving the TCO for RISE marks a significant milestone for Brickell City Centre and brings us one step closer to unveiling the full experience of living within Miami’s largest single mixed-us e development,” says Maile Aguila, Senior Vic e President of Residential Sales for the project. “Swire Properties represents something unique, special and high-end, and we are proud to share our vision and creation with our fellow neighbors,” adds Aguila. To promote wellness and sustainability as well as a commitment to their vibrant community, Brickell City Centre has incorporated programming such as the weekly ‘Farmers Market’ featuring conventional and organically grown produce. -

BRICKELL 801 Brickell Avenue Miami, FL 33131

801 BRICKELL 801 Brickell Avenue Miami, FL 33131 SUBLEASE IMMEDIATELY AVAILABLE 9,742 SF | 6TH FLOOR | SUITE 600 NEGOTIABLE ASKING RATE TERM THROUGH JULY 21ST, 2020 AVAILABLE CLASS A BRICKELL FOR IMMEDIATE OFFICE SPACE MIAMI, FL OCCUPANCY SUBLEASE IMMEDIATELY AVAILABLE 801 BRICKELL AVENUE MIAMI, FL 33131 Strategic Location In the Heart of Brickell Plug and Play Condition Efficient Layout Furniture Available 9,742 SF NEGOTIABLE ASKING RATE 6TH FLOOR SUBLEASE THROUGH SUITE 600 JULY 21 ST, 2020 46" AFF D-G 46" AFF D-G 46" AFF D-G 46" AFF D-G 2" 2" D- 46" AFF 6 3/4" LV D.S. D D D-20 D-20 D-20 44" D A.F.F. 44" A.F.F. 44" A.F.F. 44" A.F.F. 44" 44" 44" 44" 44" A.F.F. A.F.F. A.F.F. A.F.F. A.F.F. D 2 D-20 D-20 D-20 D-20 D-20 D-20 D-20 D-20 D-20 D-20 D-20 D Aventura Miami Lakes SUBLEASE IMMEDIATELY AVAILABLE 801 BRICKELL AVENUE MIAMI, FL 33131 LOCATION HIGHLIGHTS • Minutes from Downtown Miami Doral and PortMiami • Immediate access to I-395, I-95 Downtown and 836 EXPY Brickell • Conveniently located within Coral Gables walking distance of Brickell restaurants and other retail South Coconut Miami Grove establishments • Plug & Play condition Kendall Adjacent to Brickell City Centre & Mary Brickell Village Brickell Avenue Views PROPERTY HIGHLIGHTS BUILDING FEATURES • Plug and play condition • On-site security • Available immediately • Secured floors accessed by key only • Efficient layout • Parking 1.4/1,000 SF • Furniture available • Restaurant • Private office spaces • LEED Certified Gold • Collaborative lounges • Property management on site • Easy access to Miami’s Metromover 801 BRICKELL 801 Brickell Avenue Miami, FL 33131 For more information, please contact: TONY JONES Executive Director Tenant Advisory Group D: +1 305 351 2453 M: +1 305 710 1425 [email protected] CUSHMAN & WAKEFIELD OF FLORIDA, LLC JAKE WEISS 333 SE 2nd Avenue, Suite 3900 Tenant Advisor Tenant Advisory Group Miami, Florida 33131 D: +1 305 533 2844 M: +1 305 733 3509 cushwakesouthfl.com [email protected] @CushWakeSouthFL ©2019 Cushman & Wakefield. -

East, Miami Serves As Anchor Hotel for Brickell City Centre – Swire Properties’ $1.05 Billion Mixed-Use Development, and First-Ever Swire Hotels Hotel in the U.S

EAST, MIAMI SERVES AS ANCHOR HOTEL FOR BRICKELL CITY CENTRE – SWIRE PROPERTIES’ $1.05 BILLION MIXED-USE DEVELOPMENT, AND FIRST-EVER SWIRE HOTELS HOTEL IN THE U.S. The hotel features destination dining, Quinto La Huella and Sugar, a locally and internationally curated fashion, music, design, culinary, wellness, and arts program, exclusive partnership with the National YoungArts Foundation, and purveyors like Panther Coffee and JoJo Tea Miami, Florida (May 10, 2016) - After nearly three years of planning and development, highly-anticipated lifestyle hotel EAST, Miami, has opened in the heart of Miami’s Brickell district. The anchor hotel for Swire Properties’ $1.05 Billion, 5.4 million square foot mixed-used development, and the first of its kind for the Hong Kong-based brand in the United States, features destination dining, state-of-the-art fitness facilities, cutting edge technology, and quality amenities available to both local residents and visitors to Miami. The hotel offers a distinctive and unconventional experience for individuals who seek innovation, style and personalized service, building upon the success of the EAST brand, which includes EAST, Hong Kong and EAST, Beijing. EAST, Miami offers 352 guest rooms to include eight suites and 89 residence suites all owned and operated by Swire Hotels. Ranging in size from 300 to 1,800 square feet, the contemporary rooms, suites, and residence suites feature balconies with views of the Miami skyline and Biscayne Bay, floor-to-ceiling windows, walk-in rain shower, and complimentary WiFi. The one-, two- and three-bedroom residence suite options also offer fully equipped kitchen and laundry facilities along with access to all amenities and services of the hotel.