Discover Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pdf/Rosen Eng.Pdf Rice fields) Connnecting Otsuki to Mt.Fuji and Kawaguchiko

Iizaka Onsen Yonesaka Line Yonesaka Yamagata Shinkansen TOKYO & AROUND TOKYO Ōu Line Iizakaonsen Local area sightseeing recommendations 1 Awashima Port Sado Gold Mine Iyoboya Salmon Fukushima Ryotsu Port Museum Transportation Welcome to Fukushima Niigata Tochigi Akadomari Port Abukuma Express ❶ ❷ ❸ Murakami Takayu Onsen JAPAN Tarai-bune (tub boat) Experience Fukushima Ogi Port Iwafune Port Mt.Azumakofuji Hanamiyama Sakamachi Tuchiyu Onsen Fukushima City Fruit picking Gran Deco Snow Resort Bandai-Azuma TTOOKKYYOO information Niigata Port Skyline Itoigawa UNESCO Global Geopark Oiran Dochu Courtesan Procession Urabandai Teradomari Port Goshiki-numa Ponds Dake Onsen Marine Dream Nou Yahiko Niigata & Kitakata ramen Kasumigajo & Furumachi Geigi Airport Urabandai Highland Ibaraki Gunma ❹ ❺ Airport Limousine Bus Kitakata Park Naoetsu Port Echigo Line Hakushin Line Bandai Bunsui Yoshida Shibata Aizu-Wakamatsu Inawashiro Yahiko Line Niigata Atami Ban-etsu- Onsen Nishi-Wakamatsu West Line Nagaoka Railway Aizu Nō Naoetsu Saigata Kashiwazaki Tsukioka Lake Itoigawa Sanjo Firework Show Uetsu Line Onsen Inawashiro AARROOUUNNDD Shoun Sanso Garden Tsubamesanjō Blacksmith Niitsu Takada Takada Park Nishikigoi no sato Jōetsu Higashiyama Kamou Terraced Rice Paddies Shinkansen Dojo Ashinomaki-Onsen Takashiba Ouchi-juku Onsen Tōhoku Line Myoko Kogen Hokuhoku Line Shin-etsu Line Nagaoka Higashi- Sanjō Ban-etsu-West Line Deko Residence Tsuruga-jo Jōetsumyōkō Onsen Village Shin-etsu Yunokami-Onsen Railway Echigo TOKImeki Line Hokkaid T Kōriyama Funehiki Hokuriku -

Summary of Family Membership and Gender by Club MBR0018 As of June, 2009

Summary of Family Membership and Gender by Club MBR0018 as of June, 2009 Club Fam. Unit Fam. Unit Club Ttl. Club Ttl. District Number Club Name HH's 1/2 Dues Females Male TOTAL District 333 C 25243 ABIKO 5 5 6 7 13 District 333 C 25249 ASAHI 0 0 2 75 77 District 333 C 25254 BOSHUASAI L C 0 0 3 11 14 District 333 C 25257 CHIBA 9 8 9 51 60 District 333 C 25258 CHIBA CHUO 3 3 4 21 25 District 333 C 25259 CHIBA ECHO 0 0 2 24 26 District 333 C 25260 CHIBA KEIYO 0 0 1 19 20 District 333 C 25261 CHOSHI 2 2 1 45 46 District 333 C 25266 FUNABASHI 4 4 5 27 32 District 333 C 25267 FUNABASHI CHUO 5 5 8 56 64 District 333 C 25268 FUNABASHI HIGASHI 0 0 0 23 23 District 333 C 25269 FUTTSU 1 0 1 21 22 District 333 C 25276 ICHIKAWA 0 0 2 36 38 District 333 C 25277 ICHIHARA MINAMI 1 1 0 33 33 District 333 C 25278 ICHIKAWA HIGASHI 0 0 2 14 16 District 333 C 25279 IIOKA 0 0 0 36 36 District 333 C 25282 ICHIHARA 9 9 7 26 33 District 333 C 25292 KAMAGAYA 12 12 13 31 44 District 333 C 25297 KAMOGAWA 0 0 0 37 37 District 333 C 25299 KASHIWA 0 0 4 41 45 District 333 C 25302 BOSO KATSUURA L C 0 0 3 54 57 District 333 C 25303 KOZAKI 0 0 2 25 27 District 333 C 25307 KAZUSA 0 0 1 45 46 District 333 C 25308 KAZUSA ICHINOMIYA L C 0 0 1 26 27 District 333 C 25309 KIMITSU CHUO 0 0 1 18 19 District 333 C 25310 KIMITSU 5 5 14 42 56 District 333 C 25311 KISARAZU CHUO 1 1 5 14 19 District 333 C 25314 KISARAZU 0 0 1 14 15 District 333 C 25316 KISARAZU KINREI 3 3 5 11 16 District 333 C 25330 MATSUDO 0 0 0 27 27 District 333 C 25331 SOBU CHUO L C 0 0 0 39 39 District 333 C -

Family Gender by Club MBR0018

Summary of Membership Types and Gender by Club as of June, 2015 Club Fam. Unit Fam. Unit Club Ttl. Club Ttl. Student Leo Lion Young Adult District Number Club Name HH's 1/2 Dues Females Male Total Total Total Total District 333 C 25243 ABIKO 5 8 8 12 0 0 0 20 District 333 C 25249 ASAHI 0 0 4 70 0 0 0 74 District 333 C 25254 BOSHUASAI L C 0 0 1 9 0 0 0 10 District 333 C 25257 CHIBA 15 24 12 44 0 0 0 56 District 333 C 25258 CHIBA CHUO 6 14 11 18 0 0 0 29 District 333 C 25259 CHIBA ECHO 6 7 8 25 0 0 0 33 District 333 C 25260 CHIBA KEIYO 0 0 1 15 0 0 0 16 District 333 C 25261 CHOSHI 3 3 0 34 0 0 0 34 District 333 C 25266 FUNABASHI 7 10 10 34 0 0 0 44 District 333 C 25267 FUNABASHI CHUO 7 13 14 45 0 0 0 59 District 333 C 25268 FUNABASHI HIGASHI 2 2 1 25 0 0 0 26 District 333 C 25269 FUTTSU 9 21 15 28 0 0 0 43 District 333 C 25276 ICHIKAWA 4 5 7 35 0 0 0 42 District 333 C 25277 ICHIHARA MINAMI 6 6 5 22 0 0 0 27 District 333 C 25278 ICHIKAWA HIGASHI 1 4 6 16 0 0 0 22 District 333 C 25279 IIOKA 0 0 1 31 0 0 0 32 District 333 C 25282 ICHIHARA 10 10 8 31 0 0 0 39 District 333 C 25292 KAMAGAYA 3 3 4 9 0 0 0 13 District 333 C 25297 KAMOGAWA 0 0 3 51 0 0 0 54 District 333 C 25299 KASHIWA 0 0 4 31 0 0 0 35 District 333 C 25302 BOSO KATSUURA L C 6 6 11 72 0 0 0 83 District 333 C 25303 KOZAKI 0 0 2 27 0 0 0 29 District 333 C 25307 KAZUSA 18 24 22 43 0 0 0 65 District 333 C 25308 KAZUSA ICHINOMIYA L C 0 0 0 24 0 0 0 24 District 333 C 25309 KIMITSU CHUO 7 13 5 18 0 0 0 23 District 333 C 25310 KIMITSU 20 48 38 58 0 0 0 96 District 333 C 25311 KISARAZU CHUO -

Around Tokyo from Narita Airport Model Course Depart Narita Airport ➡ Nikko ➡ Chichibu ➡ Narita ➡ Arrive Narita Airport (A Model Course)

Nikko Area Nikko Area *Please be aware that transport and the time required for a model course may vary depending on the weather and/or traffic conditions *Please note that Chichibu 2-Day Pass does not cover the Red Arrow Limited Express fare Around Tokyo from Narita Airport Model course Depart Narita Airport ➡ Nikko ➡ Chichibu ➡ Narita ➡ Arrive Narita Airport (A model course) Keisei Skyliner & Tokyo Subway Ticket NIKKO ALL AREA PASS Keisei Skyliner & Tokyo Subway Ticket Chichibu 2-Day Pass Keisei Skyliner & Tokyo Subway Ticket Narita-Kaiun Pass Keisei Tokyo Metro Tobu Limited Express Tobu Limited Express Tokyo Metro Ginza Line / Tozai Line / Red Arrow Red Arrow Tokyo Metro Marunouchi Line / Tozai Line / Keisei Skyliner Ginza Line SPACIA, Revaty SPACIA, Revaty Marunouchi Line Limited Express Limited Express Ginza Line Skyliner Keisei Main Line Keisei Main Line Narita Airport Ueno Sta. Asakusa Sta. Tobu Nikko Sta. Asakusa Sta. Ikebukuro Sta. Seibu Chichibu Sta. Ikebukuro Sta. Ueno Sta. Narita Airport Keisei Narita Sta. Narita Airport About 44 minutes About 5 minutes About 110 minutes About 110 minutes About 29 minutes About 78 minutes About 78 minutes About 16 minutes About 44 minutes About 10 minutes About 10 minutes Nikko Area Narita Area Chichibu Area Narita Area Chichibu Area Use the Use the Use the Chichibu 2-Day pass Narita-Kaiun pass Experience the mysterious charm of Nikko NIKKO ALL AREA PASS Try Sanja Meguri (visiting three shrines) to feel nature and history for sightseeing in Chichibu! Multifarious places well worth visiting near the airport! for sightseeing in Narita! for sightseeing in Nikko! Please refer to the back of the brochure for details. -

Chiba Art Festival 2020 Painting/Photograph Exhibition Application Form (For Personal Use)

■Chiba Art Festival 2020 Painting/Photograph Exhibition Application Form (For personal use) The items marked with ★ will be displayed with your work.(Name or pen name, age category, title of № the work, a story associated with the work) ※Will be filled in at the secretariat Name★ Telephone Pen name★ ― ― number Small child (first to third grade) Age Age category★ Fourth to sixth grade or middle school ※As of submission ※As of submission High school student or adult (〒 - ) Address E-mail Title of the work★ A story associated with the work★ How to return the If you would like for us to return your work, If you don't want us to return your work,we work ※Check appropriate box please pay the return fee. will dispose of it after the exhibition. Please check the theme which you celected from Chiba Cultural Assets Sengen Shrine and Pine Forest Lake Tega Fireworks Display Inubosaki Lighthouse Katsuura Morning Market Otomi Kagura in Inage Home of the Shirakaba-school Choshi Electric Railway and Inohana Castle Site Katsuura Tantanmen Kujukutani View Park and its Writers Scenery Along the Line Edo Cultural Heritage of Fusa Katsuura Big Hina Matsuri Mishima Bojutsu (Stick Kasori Shell Mounds Choshi Soy Sauce Breweries District (Doll’s Festival) Fighting) and Kakkomai Kamagaya Great Buddha and Views of Ohara Hadaka Matsuri (Naked Senyo-ji Temple and Chiba-warai Choshi Hane Taiko Drumming Takeoka-Style Ramen Nearby Shopping Festival) Street Kazusa-bori Well-Boring Chiba City Museum of Art Ino Kabuki Byobugaura Cliff and Geopark Scenery of Isumi Railway -

History of the Chiba Bank Group

Summary History of the Chiba Bank Group Since its establishment in 1943, we have continued to grow in step with the region by actively March 2019 responding to financial needs generated by the development of Chiba Prefecture. Capital stock: ¥145 billion 6.26 Number of employees: 4,224 million people Number of branches: 185 Deposits: ¥12,333.4 billion Former Head Office Current Head Office Loans and Bills Discounted: 2014.3 (millions of people) (¥ trillion) Balance of loans ¥10,136.8 billion Total deposits 7 12 Balance of deposits reached ¥10 trillion Population of Chiba Prefecture 6 10 March 1943 (at the time of establishment) 5 Capital stock: ¥10 million 1988.9 Number of employees: 725 Total deposits 8 Number of branches: 70 reached Deposits: 4 ¥247.02 million ¥5 trillion Loans and Bills Discounted: 1.62 ¥51.59 million 6 million people 3 1983.3 Total deposits reached ¥3 trillion 4 2 1975.9 Total deposits reached ¥1 trillion 2 1 1963.9 Total deposits reached ¥100 billion 0 0 1943.3 1953.3 1963.3 1973.3 1983.3 1993.3 2003.3 2013.3 2019.3 Our Transition 1943.3 1960- 1970.10 Founded as a result of the merger of Chiba Deposits and loans grew in Listed on the 2nd section of the Tokyo Stock Godo Bank, Omigawa Agricultural and response to high economic growth Exchange (changed to 1st section in August 1971) Commercial Bank, and the Kujuhachi Bank 1964.2 1971.10 Started the first online system Set a sunflower as the bank flower 1973.3 Built the new Head Office building and relocated the Head Office from Chuo to Chiba-minato Flow of Society 1941-1945 -

TOD Practice in Japan Tokyo, a Global City Created by Railways

TOD Practice in Japan Tokyo, A Global City Created by Railways This is a partial English translation of a book titled as “TOD Practice in Japan; Tokyo, A Global City Created by Railways”. (Edited and written by Takashi Yajima and Hitoshi Ieda. Published by The Institute of Behavioral Sciences) The copyright for the original text is held by the authors noted above, the publisher, and the sources noted in the diagrams and figures in the book. The copyright for the translation is held by JICA (Chapter 1), and the Ministry of Land, Infrastructure, Transport and Tourism (Chapters 2 - 4). The book was proofread by Takashi Yajima, Takashi Yamazaki, Masafumi Ota and Mizuo Kishita. (1st Edition, published in Mar. 2019) Edited and written by Takashi Yajima and Hitoshi Ieda [Study Group on TOD] Takashi Yajima, Hitoshi Ieda, Takayuki Kishii, Tsuneaki Nakano, Takashi Yamazaki, Masafumi Ota, Hisao Okuma, Hiroyuki Suzuki, Shinichi Hirata and Hajime Daimon Table of contents The contents of the original are as below. The sections considered necessary in order for persons from overseas to gain an understanding of Japan’s practice on TOD were selected for translation. Specifically, those are the sections that give an overview of Japan’s urban development and transportation, and sections relating to the former Japanese National Railways/current East Japan Railway Company as well as Tokyu Corporation as typical examples clearly illustrating TOD practice in Japan. Translated sections are indicated in the contents with an asterisk (*). Introduction Tokyo: The -

Chiba Travel

ChibaMeguri_sideB Leisure Shopping Nature History&Festival Tobu Noda Line Travel All Around Chiba ChibaExpressway Joban Travel Map MAP-H MAP-H Noda City Tateyama Family Park Narita Dream Farm MITSUI OUTLET PARK KISARAZU SHISUI PREMIUM OUTLET® MAP-15 MAP-24 Express Tsukuba Isumi Railway Naritasan Shinshoji Temple Noda-shi 18 MAP-1 MAP-2 Kashiwa IC 7 M22 Just within a stone’s throw from Tokyo by the Aqua Line, Nagareyama City Kozaki IC M24 Sawara Nagareyama IC Narita Line 25 Abiko Kozaki Town why don’t you visit and enjoy Chiba. Kashiwa 26 Sawara-katori IC Nagareyama M1 Abiko City Shimosa IC Whether it is for having fun, soak in our rich hot springs, RyutetsuNagareyamaline H 13 Kashiwa City Sakae Town Tobu Noda Line Minami Nagareyama Joban Line satiate your taste bud with superior products from the seas 6 F Narita City Taiei IC Tobu Toll Road Katori City Narita Line Shin-Matsudo Inzai City Taiei JCT Shiroi City Tonosho Town and mountains, Chiba New Town M20 Shin-Yahashira Tokyo Outer Ring Road Higashikanto Expressway Hokuso Line Shibayama Railway Matsudo City Inba-Nichi-idai Narita Sky Access Shin-Kamagaya 24 you can enjoy all in Chiba. Narita Narita Airport Tako Town Tone Kamome Ohashi Toll Road 28 34 Narita IC Musashino Line I Shibayama-Chiyoda Activities such as milking cows or making KamagayaShin Keisei City Line M2 All these conveniences can only be found in Chiba. Naritasan Shinshoji Temple is the main temple Narita International Airport Asahi City butter can be experienced on a daily basis. Narita Line Tomisato IC Ichikawa City Yachiyo City of the Shingon Sect of Chizan-ha Buddhism, Funabashi City Keisei-Sakura Shisui IC You can enjoy gathering poppy , gerbera, Additionally, there are various amusement DATA 398, Nakajima, Kisarazu-City DATA 689 Iizumi, Shisui-Town Sobu LineKeisei-Yawata Shibayama Town M21 Choshi City Isumi and Kominato railroad lines consecutively run across Boso Peninsula, through a historical Choshi 32 and antirrhinum all the year round in the TEL:0438-38-6100 TEL:043-481-6160 which was established in 940. -

Blood Types in Japan 1

Yap. or. Human Genet. 23, 197-209, 1978 THE DISTRIBUTION OF THE RH(D) BLOOD TYPES IN JAPAN 1 Yoshiko FUJITA, Katumi TANAKA,and Masako TANIMURA Department of Human Genetics, Tokyo Medical and Dental University, Tokyo Summary Data on the Rh(D) types of 2,745,618 individuals were collected from prefectural health departments, health centers, and Red Cross blood centers in 35 of 47 prefectures in the whole country. Phenotypic and gene frequencies for each subpopulations were calculated and tabulated. The frequency of Rh(D) negatives in the whole sample is 0.5428~ and the frequency of the Rh(D) negative gene is estimated to be 7.37__+0.03~. An insignificant cline of the frequencies is suggested, i.e. the Rh(D) negative gene is increased from the northeast to the southwest of Japan. INTRODUCTION Frequencies of Rh blood types in different localities in Japan were summarized by Akaishi and Kudo (1975) who compiled available data on 10 prefectures from literature and through their own surveys. A majority of the studied prefectures cluster in the northmost part of the country and, therefore, distribution of the Rh system in the whole of Japan was still uncertain. Recently, examination of the Rh(D) type is extensively carrying out at health centers and blood centers in the whole country. The present authors collected such data and report here the results of the analyses. MATERIALS AND METHODS The data on the numbers of Rh(D) positives and negatives were obtained from health centers, prefectural health departments and Red Cross blood centers by mail. -

The Chiba Bank, Ltd. Integrated Report 1-2, Chiba-Minato, Chuo-Ku, Chiba-Shi, Chiba 260-8720, Japan Phone: 81-43-245-1111 2019

The Chiba Bank Integrated Report 2019 The Chiba Bank, Ltd. Integrated Report 1-2, Chiba-minato, Chuo-ku, Chiba-shi, Chiba 260-8720, Japan Phone: 81-43-245-1111 https://www.chibabank.co.jp/ 2019 005_9326487911909.indd 1-3 2019/09/26 11:52:20 Introduction Our Philosophy Corporate Data The Chiba Bank, Ltd. As of March 31, 2019 Aiming to be Principal Shareholders Introduction the “best retail” banking group The ten largest shareholders of the Bank and their respective shareholdings as of March 31, 2019 were as follows: Number of Shares Percentage of Total (in thousands)*1 Shares Issued*2 (%) The Master Trust Bank of Japan, Ltd. (Trust Account) 52,123 6.84 that provides top-class satisfaction Japan Trustee Services Bank, Ltd. (Trust Account) 36,583 4.80 Nippon Life Insurance Company 26,870 3.52 and is highly regarded by The Dai-ichi Life Insurance Company, Limited 26,230 3.44 Sompo Japan Nipponkoa Insurance Inc. 18,537 2.43 Meiji Yasuda Life Insurance Company 18,291 2.40 Summary customers of the region SUMITOMO LIFE INSURANCE COMPANY 17,842 2.34 MUFG Bank, Ltd. 17,707 2.32 STATE STREET BANK AND TRUST COMPANY 505223 15,001 1.97 Japan Trustee Services Bank, Ltd. (Trust Account 5) 13,702 1.79 Excluded from the figures above are 79,121 thousand treasury shares in the name of the Chiba Bank, Ltd. (Excludes one thousand shares which, although registered in the name of the Chiba Bank, Ltd. on the shareholder list, are not actually owned by the Bank.) *1 Rounded down to the nearest thousand Management Policy *2 Rounded down to two decimal places “Sustainable -

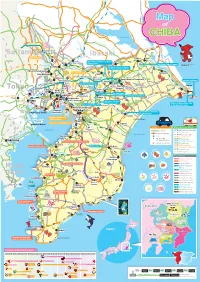

Guide Map of Chiba2020

Map of Tsukuba JCT Lake Kasumigaura CHIBA Ken-O ExpressWay Tobu Noda Line 24 Joban ExpressWay Tsukuba Express JR Kashima Line Shimizu-koen Nodashi Itako Saitama Ibaraki 124 Shimizu Park Sawara Katori JR Joban Line Tone River Toride Chiba Prefectural Boso-no-Mura / Namegawa JR Musashino Line Abiko 6 Ryutetsu Cosplay Annex Kozaki 3 The Historic Town of Sawara Chiba Prefecture mascot Nagareyama CHI-BA+KUN 356 51 Sawara-Katori Railway Kashiwa JR Narita Line Naritasan Shinsho-ji Temple / 356 Teganuma Pond 16 Naritasan Omotesando Street Minami-Nagareyama H.C. Andersen Park 408 Taiei Toso Toll Road Sasagawa Shin Matsudo Ajiki 2 Higashi-Kanto ExpressWay Chiba-New-Town Inba- Taiei JCT Yabashira JR Narita Line Nihonidai Narita Airport Terminal 2, 3 Otogari Shin Kamagaya Hokuso Line 1 Inubosaki Lighthouse Shin Narita Narita Shinkuko Narita Yahashira Nishi- 464 464 Sakura Furusato Square Keisei Airport Shiroi 23 Yachiyo Inbanuma Narita Narita Shibayama- ShinKeisei Furusato Station Pond Choshi Misaki 7 Tomisato Airport Chiyoda Electric Ichikawa Line Keisei Rose Keisei Shisui Michi-no-Eki Railway Tokyo Nishi- 296 Tako Ajisaikan Garden Sakura Shisui Funabashi Toyo Kosoku Line296 4 6 Ueno 14 5 The Hotta House 126 Choshi Ichikawa Funabashi Keisei Main Line 10 9 JR Sobu Line Katsutadai Old Samurai Residences Inubo Shinjuku Sakura Motoyawata Tsudanuma Fuwari Keisei Tsudanuma Sakura Shibayama JR Sobu Main Line Tokyo JR Keiyo Line Kawamura Memorial Yokoshiba Hikari Makuhari Keiyo Road Chiba Kita 8 Miyanogi JCT DIC Museum of Art Matsuo Yokoshiba Chikyu no -

Appointed Areas by Group(PDF 52.1KB)

Tuesday, March 22nd : Group 1 (Original Schedule: 9:20 ~ 13:00) -Blackout Period: Approximately 3 hours between ( 9:20 ~ 13:00 ) -Expected Number of Customers: Approximately 2,500,000 -Applicable Region: Chiba pref., Tochigi pref., Saitama pref., Gunma pref., Kanagawa pref., Shizuoka pref. No.(※) Areas A Kyonan Town, Kamogawa City, Tateyama City, Kimitsu City, Ichihara City, Sodegaura City, Chonan Town, Nagara Town, Minamiboso City, Futtsu City, Mobara City, Kisarazu City B Sakura City, Otawara City, Nasukarasuyama City, Nasushiobara City, Nakagawa Town, Nasu Town, Yaita City C Saitama City (Nishi ward), Fujimino City, Sayama City, Sakado City, Shiki City, Tokorozawa City, Niiza City, Kawagoe City, Asaka City, Miyoshi Town, Iruma City, Fujimi City, Wako City Yotsukaido City, Isumi City, Sakura City, Oamishirasato Town, Ichihara City, Chiba City (Inage Ward, Hanamigawa Ward, Wakaba Ward, Chuo Ward, Mihama Ward, Midori Ward), Funabashi City, Ichinomiya Town, Chosei Village, Chonan Town, Nagara Town, Shirako D Town, Mutsuzawa Town, Togane City, Yachimata City, Yachiyo City, Mobara City E Minano Town, Ogano Town, Chichibu City, Yorii Town, Nagatoro Town, Higashichichibu Village, Yokoze Town, Hanno City, Ogawa Town, Tokigawa Town, Ranzan Town F Yokosuka City, Yokohama City (Isogo Ward, Sakae Ward, Kanazawa Ward, Konan Ward), Kamakura City, Chigasaki City, Hayama Town, Zushi City, Fujisawa City G Kamagaya City, Funabashi City, Shiroi City H Kawasaki City (Kawasaki Ward) I Midori City, Isesaki City, Kiryu City, Tamamura Town, Maebashi City J