Code Security Description ABC ADELAIDE BRIGHTON ALL

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2017 Annual Report 1 I Sirtex 2017 Highlights

2017 ANNUAL REPORT 1 I SIRTEX 2017 HIGHLIGHTS DOSES SOLD 2017 12,578 14,000 12,000 10,000 8,000 6,000 4,000 2,000 0 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 CONTENTS ABOUT SIRTEX 03 2017 FINANCIAL SUMMARY Sirtex Medical Limited is an Australian- 05 CHAIRMAN’S REPORT based global healthcare business working to 09 CHIEF EXECUTIVE OFFICER’S REPORT improve outcomes for people with cancer. 18 ENVIRONMENTAL, SOCIAL AND Our lead product is a targeted radiation GOVERNANCE therapy known as SIR-Spheres® Y-90 resin 22 BOARD OF DIRECTORS microspheres. It is available in more than 23 KEY MANAGEMENT PERSONNEL 40 countries, within over 1,090 certified hospitals to treat patients with 24 FINANCIAL REPORT inoperable liver cancer. Our business revolves around helping medical professionals understand and use our product to improve clinical outcomes and the quality of life for people with liver cancer. While at the same time, we work closely with government and private payers to ensure our patients receive the appropriate reimbursement for our product. We are challenging established practices and developing innovative new therapies that promise to improve the health and lives of many people suffering from cancer or other diseases. Our ongoing success is based on a commitment to serving our customers, professionalism, continuous improvement and innovation. ANNUAL REPORT 2017 I 2 DOSE SALES 12,578 +5.4% REVENUE $234.3m +0.8% NET LOSS AFTER TAX $26.3m -149.0% THE AMERICAS EUROPE, MIDDLE ASIA PACIFIC EAST, AFRICA Boston, United States Frankfurt, -

Australian Listed Equities: Weekly Share Market Wrap

Australian Listed Equities: Weekly Share Market Wrap Total Shareholder Returns as at 15 April 2016 Price 1 week 1 month 6 months 1 year 2 years 3 years 5 years 10 years 10 years Ticker Stock Name $ % % % % % p.a. % p.a. % p.a. % p.a. ranking A2M The A2 Milk Company 1.665 -4.31 2.78 134.51 208.33 - - - - - ABC Adelaide Brighton 5.10 -1.16 6.03 26.15 17.04 19.09 19.37 12.82 10.84 34 ABP Abacus Property Group 3.10 2.99 5.08 -0.47 12.76 20.70 17.15 11.90 -1.96 105 AFI Australian Foundat. 5.53 0.18 -1.60 -4.25 -7.23 0.42 5.09 6.71 5.22 58 AGL AGL Energy Limited. 18.24 -0.65 0.55 15.71 25.25 14.52 10.63 9.90 6.32 53 AHG Automotive Holdings. 3.85 -0.52 -3.78 -1.13 -2.98 4.35 4.94 12.70 14.45 22 AIA Auckland Internation 5.75 -1.88 0.45 25.03 28.95 28.14 37.37 30.93 14.31 23 AIO Asciano Limited 8.84 1.14 -1.67 13.83 38.00 31.68 21.04 13.79 - - AIZ Air New Zealand 2.70 -0.37 9.76 4.19 3.16 27.56 39.16 31.16 13.06 24 ALL Aristocrat Leisure 10.12 4.01 1.50 14.85 23.98 45.00 42.39 29.35 -1.72 102 ALQ ALS Limited 4.38 15.57 1.15 -16.29 -1.83 -16.66 -16.64 -6.48 10.25 37 AMC Amcor Limited 14.76 1.17 4.53 15.59 5.97 25.73 23.23 20.98 11.71 29 AMP AMP Limited 5.79 5.46 2.84 3.13 -8.72 11.19 8.68 4.71 1.17 88 ANN Ansell Limited 19.68 13.30 14.42 3.31 -32.90 7.34 12.16 9.27 7.39 47 ANZ ANZ Banking Grp Ltd 23.85 7.05 -6.07 -13.17 -28.60 -9.52 0.33 6.22 3.50 72 AOG Aveo Group 3.30 0.30 4.10 16.20 24.07 30.19 38.74 -1.59 -9.34 119 APA APA Group 8.71 0.46 5.83 1.14 -1.03 22.97 17.57 21.10 11.78 28 APE AP Eagers Limited 10.00 4.06 -0.58 0.99 24.34 45.68 30.49 -

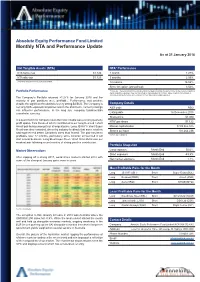

Monthly NTA and Performance Update

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

Realindex Australian Share Fund

Realindex Australian Share Fund Fact sheet - 31 Aug 2015 Fund strategy Fund facts The Realindex Australian Share Fund uses the RAFI® methodology in the Benchmark S&P / ASX 200 Accumulation Index construction of its portfolios which selects and weights companies Funds under management $2800.1 million according to their economic footprint defined by fundamental measures of Inception Date 17 November 2008 company size (sales, cash flow, book value and dividends). The portfolio is further enhanced by applying additional factors such as quality of earnings and debt coverage. Commentary The Realindex Australian Shares Fund returned -7.39% (gross of fees) during August 2015 outperforming the S&P/ASX 200 Accumulation Index which returned -7.79% (its worst monthly performance since October 2008). Value (-7.3%) slightly outperformed Growth (-8.0%) during the month, extending the longer-term outperformance trend (-2.4% vs. -6.1%, 12 months to 31 August 2015). This outcome is typically favourable for portfolio performance, given the Value tilt inherent in the Fundamental Indexation methodology. The Materials sector (-5.2%) was the top contributor to relative performance during the month, driven by overweight holdings in steel companies Sims Metal Management (+21.4%) and BlueScope Steel (+18.7%). Sims reported a better-than-expected FY15 result, while BlueScope committed to $200m cost out by FY17, which was well received by investors. An overweight holding in Spark New Zealand (+13.0%) led the portfolio’s outperformance in the Telecommunications sector (-8.3%). Spark rallied after announcing positive earnings growth and an annual dividend increase at its FY15 results. Spark was the top contributor to relative performance across the portfolio at a company level. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Sep Tem B Er

4 201 Quarterly Newsletter September FML S In this quarterly edition we review performance and attribution. We profile GBST Holdings and IProperty Group. Offshore we take a look at QE and US Energy. We also consider how Technology for the Ages changes with each generation. Photo: School holidays - no worries, surfing for a 9 year old maybe as good as it gets and no technology needed. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 3, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au selector About Selector We are a boutique fund manager and we have a combined experience of over 150 years. We believe in long term wealth creation and building lasting relationships with our investors. Our focus is stock selection. Our funds are high conviction, concentrated and index unaware. As a result we have low turnover and produce tax effective returns. First we identify the best business franchises with the best management teams. Then we focus on valuations. Please forward to us contact details if you would like future newsletters to be emailed to family, friends or business colleagues. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 3, 10 Bridge Street Sydney NSW 2000, Australia Telephone 612 8090 3612 Web www.selectorfund.com.au selector September 2014 Selector High Conviction Equity Fund Quarterly Newsletter #45 Dear Investor, With the company reporting season over for another year, investor attention has quickly shifted to the road ahead. Here the simple message, proceed with caution, has been top of mind and for good reason. -

SIR-Spheres® Y-90 Resin Microspheres

Manufacturer: US Sales Office: Sirtex Medical Limited Sirtex Medical Inc Level 33, 101 Miller Street, 300 Unicorn Park Drive, North Sydney NSW 2060, Australia Woburn MA 01801, USA Tel: +61 2 9964 8400 Tel: 1 888 474 7839 www.sirtex.com 4 Warnings • Some patients may experience gastric problems following treatment but H-2 blocking agents may 4.1 Non-Target Delivery of SIR-Spheres be used the day before implantation of SIR- microspheres Spheres microspheres and continued as needed to reduce gastric complications. Inadvertent delivery of SIR-Spheres microspheres to extra-hepatic structures such as the esophagus, • Many patients may experience abdominal pain SIR-Spheres® Y-90 resin stomach, duodenum, gallbladder or pancreas may immediately after administration of SIR-Spheres result in radiation injury to these structures. microspheres and pain relief may be required. microspheres Meticulous angiographic technique must be • SIR-Spheres microspheres demonstrated a mild (Yttrium-90 microspheres) employed to prevent the non-target delivery of SIR- sensitization potential when tested dermally in an Spheres microspheres to any extra-hepatic animal model. structures. 1 Description 4.2 Radioembolization Induced Liver 6 Clinical Trial Results SIR-Spheres microspheres consist of biocompatible microspheres containing yttrium-90 with a size Disease (REILD) In a randomized, controlled clinical trial, a total of 70 patients were studied in two arms, 34 patients with between 20 and 60 microns in diameter. Yttrium-90 Delivery of excessive radiation to the normal liver FUDR chemotherapy (control group), and 36 is a high-energy pure beta-emitting isotope with no parenchyma may result in REILD – see description patients with FUDR plus SIR-Spheres microspheres. -

Smallco Investment Fund

Smallco Investment Fund Quarterly Update 30 September 2014 SIF Portfolio Commentary SIF Performance Smallco Investment Fund (SIF) delivered 6.8% during the Return to 30 September 2014 September quarter and for the 12 months was up a solid 12.3%. During the quarter Iress, Isentia Group and Sirtex 3 months 6.8% Medical performed positively, while Carsales.com, Ozforex 1 year 12.3% Group and Macquarie Atlas Roads were negative 3 year p.a. 36.4% contributors. 5 year p.a. 22.5% For the September quarter the Small Ordinaries index was 10 year p.a. 13.6% modestly positive at 1.5% while for the year to 30 Since inception (31.10.00) p.a. 14.2% September it was down -0.1%. Value of $100,000 invested at inception $631,173 In general the Australian market had a solid reporting Fund returns calculated after all fees and expenses and based season and that was reflected in share prices during upon exit price and reinvestment of distributions. August, particularly for Industrial companies. However, towards the end of the quarter, the Australian and international markets became concerned about global political tensions – Ukraine, Iraq and Hong Kong – with a falling iron ore price having a significant negative impact on the Australian resources index. SIF Structure: by sector (look through) One of our major holdings is IRESS (IRE). SIF originally invested in IRE in 2002 when it had a market capitalisation of $260m. At the time we invested it was already the dominant provider of information systems to the professional equity market in Australia and New Zealand (ANZ). -

2020 Mid-Year Report

NON-U.S. LITIGATION UPDATE / 2020 MID-YEAR REPORT The LIAISON NEW YORK | WASHINGTON, D.C. | DELAWARE LABATON.COM Contents and EXECUTIVE SUMMARY EXECUTIVE SUMMARY CONTENTS Labaton Sucharow is pleased to present The Liaison: 2020 Mid-Year Report. P 1 EXECUTIVE SUMMARY The Firm has been a pioneer in protecting clients’ interests in non- U.S. litigation. With its nearly 20 years of experience abroad, and deep P 2 TRENDS IN NON-U.S. SECURITIES CLASS relationships with law firms around the world, Labaton Sucharow ACTION LITIGATION has a unique perspective on investment-related issues and recovery opportunities outside the United States. Featured in this edition are: P 4 NOTEWORTHY DEVELOPMENTS P 4 Changes to the Landscape for • Recent settlements in non-U.S. securities matters; Securities Class Action in Australia • Noteworthy developments regarding securities litigation in Australia; P 7 A New Opportunity for U.S. Investors • Ramifications of the recent U.S. decision in the Toshiba class action; to Seek Recovery in the United States • Summary of the newly-proposed Westpac action in Australia; or Losses on Shares Abroad? • Updates on select pending non-U.S. securities actions; and • Deadlines for participation in non-U.S. actions and for the submission P 10 NEWLY ANNOUNCED MATTER: of settlement claims. WESTPAC BANKING CORPORATION We would be happy to provide more comprehensive assessments and P 11 ONGOING CASE STUDIES recommendations with regard to any of the topics discussed or highlighted P 12 Germany in The Liaison. P 12 The Netherlands P 13 United Kingdom With best regards, P 14 Denmark P 14 New Zealand Labaton Sucharow LLP P 15 Australia P 17 Japan P 18 Brazil P 19 CONTACT US The LIAISONPAGE 1 THE LIAISON Trends in Non-U.S. -

(ASX100) Women on Boards Analysis

Australia/NZ | Australia Thematic Investing (Citi) Equities 18 August 2011 │ 32 pages ESG: ASX100 Women on Board Analysis Increasing Focus on Board Diversity Women on Boards of ASX100 Companies — The ASX Corporate Governance Council’s new principles and recommendations on diversity commenced on 1 January Elaine Prior 2011. This is likely to lead to increasing focus on companies’ approaches to diversity +61-2-8225-4891 issues, including female representation on company boards. This report looks at data [email protected] on women directors on ASX100 company boards. The number of women directors has Felipe Faria increased, particularly in recent months (Figure 5 to Figure 8). Board diversity may [email protected] enhance effectiveness, by providing a wider range of perspectives and knowledge. Women on Boards Data — We collected and analysed data on female board directors of S&P/ASX100 companies from FY08 to 8 August 2011 (Figure 5 to Figure 9). At 8 August 2011 there were 134 women on ASX100 boards, a 46% increase from FY08. ASX100 companies with no female board directors were AQP, CQO, EGP, FMG, IPL, JHX, LEI, LYC, OSH, PDN, PRY, RHC, RMD, SGM and SWM. Companies with three female directors (the highest number identified) are AMP, BEN, CBA, MQG, QAN, QBE and WBC. Seven female directors each currently hold three ASX100 directorships. Business Case for Gender Diversity — Reibey Institute research found that those ASX500 companies with women directors on 30 June 2010 had a 3-year return on equity (ROE) 10.7% higher than those without any women directors. The 5-year ROE was 11.1% higher. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied.