FCIC\Tempintern

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

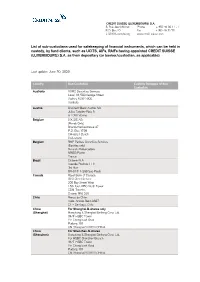

List of Sub-Custodians Used for Safekeeping of Financial Instruments

CREDIT SUISSE (LUXEMBOURG) S.A. 5, Rue Jean Monnet Phone + 352 46 00 11 - 1 P.O. Box 40 Fax + 352 46 32 70 L-2010 Luxembourg www.credit-suisse.com List of sub-custodians used for safekeeping of financial instruments, which can be held in custody, by fund clients, such as UCITS, AIFs, RAIFs having appointed CREDIT SUISSE (LUXEMBOURG) S.A. as their depositary (or banker/custodian, as applicable) Last update: June 30, 2020 Country Sub-Custodian Custody Delegate of Sub- Custodian Australia HSBC Securities Services Level 13, 580 George Street Sydney NSW 2000 Australia Austria UniCredit Bank Austria AG Julius Tandler-Platz 3 A-1090 Vienna Belgium SIX SIS AG (Bonds Only) Brandschenkestrasse 47 P.O. Box 1758 CH-8021 Zurich Switzerland Belgium BNP Paribas Securities Services (Equities only) 9 rue du Débarcadère 93500 Pantin France Brazil Citibank N.A. Avenida Paulista 1111 3rd floor BR-01311-290 Sao Paulo Canada Royal Bank of Canada GSS Client Service 200 Bay Street West 15th floor, RBC North Tower CDN-Toronto, Ontario M5J 2J5 Chile Banco de Chile Avda. Andrés Bello 2687 CL – Santiago, Chile China For Shanghai-B-shares only (Shanghai) Hongkong & Shanghai Banking Corp. Ltd. 34/F HSBC Tower Yin Cheng East Road Pudong 101 CN-Shanghai 200120 CHINA China For Shenzhen-B-shares (Shenzhen) Hongkong & Shanghai Banking Corp. Ltd. For HSBC Shenzhen Branch 34/F HSBC Tower Yin Cheng East Road Pudong 101 CN-Shanghai 200120 CHINA Colombia Cititrust Colombia S.A. Sociedad Fiduciaria Carrera 9A No. 99-02 First Floor Santa Fé de Bogotá D.C. -

Safety Glass–Restoring Glass Steagall

June 2013 www.citizen.org Safety Glass Why It’s Time to Restore the 1930s Law Separating Banking and Gambling Acknowledgments This report was written by Bartlett Naylor, financial policy advocate for Public Citizen’s Congress Watch division. Significant research assistance was provided by Jack Berghel and Nicholas Kitchel. Wallace Turbeville, senior fellow at Demos, provided invaluable advice. Congress Watch Research Director Taylor Lincoln edited the report. About Public Citizen Public Citizen is a national non-profit organization with more than 300,000 members and supporters. We represent consumer interests through lobbying, litigation, administrative advocacy, research, and public education on a broad range of issues including consumer rights in the marketplace, product safety, financial regulation, worker safety, safe and affordable health care, campaign finance reform and government ethics, fair trade, climate change, and corporate and government accountability. Public Citizen’s Congress Watch 215 Pennsylvania Ave. S.E Washington, D.C. 20003 P: 202-546-4996 F: 202-547-7392 http://www.citizen.org © 2013 Public Citizen. Public Citizen Safety Glass ighty years ago, on June 16, 1933, President Franklin Roosevelt signed the Banking Act, E also known as “Glass-Steagall,” in reference to Sen. Carter Glass (D-Va.) and Rep. Henry Steagall (D-Ala.). The law created deposit insurance, with the creation of the Federal Deposit Insurance Corp. In exchange for guaranteeing the deposits of bank customers, Glass-Steagall steered FDIC banks into engaging in socially useful activity, notably making loans to businesses and consumers. In effect, Glass-Steagall forced the mega-banks of the day to sell off their investment divisions. -

Confidential-Sample Chapters Full Text On

CONFIDENTIAL-SAMPLE CHAPTERS FULL TEXT ON REQUEST Praise for $uperHubs “In $uperHubs, Ms. Navidi skillfully applies network science to the global finan- cial system and the human networks that underpin it. $uperHubs is a topical and relevant book that should be read by anyone seeking a fresh perspective on the human endeavor that is our financial system.” CONFIDENTIAL-SAMPLE—PROFESSOR LAWRENCE H. SUMMERS, CHAPTERS Harvard; former US Secretary of the Treasury, former Director of the US National Economic Council, former president of Harvard University, and author “Sandra Navidi’s book $uperHubs is beautifully and effectively done. Not only is it a fascinating description of the power wielded by elite networks over the financial sector, it is also a meditation on the consequences of this system for FULLthe economy TEXT and the society. ON In recentREQUEST times, we have seen extraordinary rup- tures—notably Britain’s vote to break away from the European Union and the intensified sense of exclusion felt by much of America’s working class. The last chapter of $uperHubs proposes that this ruling system›s “monoculture,” its iso- lation from the rest of society, and its seeming unawareness of the fragility of what it has built are largely responsible for these ruptures, and that the system may lead to a major crisis in the future.” —PROFESSOR EDMUND S. PHELPS, Columbia University, 2006 Nobel Prize in Economics; Director, Center on Capitalism and Society, and author “$uperHubs” is a book written with great style but also containing a lot of impor- tant substance. The style is so engaging, a real page turner, that I finished it in one non-stop session. -

The Weekly Globaliser

Citi Research The Weekly Globaliser US Election Special: Global Economic Implications Economics & Currencies | Strategy | Global Sector Highlights 10 Nov 2016 22:35:19 ET In this week’s special edition, we assess potential implications of the Trump Presidency across the markets in the US and around the world. Citi Global Research +44-20-7500-1400 Trump Wins – The Republican candidate Donald Trump won the 2016 US Presidential Election; Republicans retained their majority in the House of Editors Representatives and the Senate. US presidents have the greatest authority over Tatiana Voytekhovich foreign and security policy and trade. But with a single-political party government and a President-elect that ran his campaign mainly as an ‘outsider’, the scope for +61-2-8225-4118 potential policy changes under the next administration is unusually large. Multi-Asset US Implications – The new administration will likely pursue some fiscal Global loosening, deregulation in certain industries and, at a minimum, reassess the costs and benefits of further liberalization of international trade and investment. But the scale & nature of any fiscal boost or of changes to external trade and investment policy are uncertain at this stage and will depend in part on intra-party agreements about the size of (corporate) tax cuts and infrastructure spending. The combination of fiscal loosening, trade restrictions & anti-immigration policies could raise US inflation, increase the pace of Fed rate hikes and boost the dollar. Global Implications – US growth, US financial conditions and US-related uncertainties matter greatly for global growth: the US economy accounts for 24.7% of global GDP (at market exchange rates) and an eighth of world goods imports. -

Media Release

Australian High Commission, Kuala Lumpur MEDIA RELEASE 15 DECEMBER 2017 Deepening Australia’s engagement with the Muslim world – visit to Malaysia by Australia’s Special Envoy to the OIC, Mr Ahmed Fahour AO Australia’s Special Envoy to the Organisation of Islamic Cooperation (OIC), Mr Ahmed Fahour AO, visited Malaysia for a one-day official visit yesterday. Mr Fahour called on Deputy Minister in the Prime Minister’s Department, Dato’ Dr Asyraf Wajdi Dusuki, to discuss Australia’s engagement with the OIC, Islamic banking and finance, as well as key challenges facing the Muslim world. They also shared experiences on countering violent extremism. Mr Fahour was treated to a tour and prayers at Masjid Negara with the Grand Imam, Tan Sri Syaikh Ismail Muhammad. He also had lunch with local experts and commentators, to exchange views on trends in Islam in Australia and Malaysia. A highlight for Mr Fahour was a visit to the “Faith, Fashion, Fusion: Muslim Women’s Style in Australia” exhibition at the Islamic Arts Museum Malaysia, which is being displayed for the first time internationally with the support of the Australian Government and Lendlease Malaysia. Developed by the Museum of Applied Arts and Sciences in Sydney, “Faith, Fashion Fusion” explores the experiences and achievements of Australian Muslim women and how they express their faith through fashion. It also displays Australia’s growing modest fashion market and the work of a new generation of Muslim designers and entrepreneurs. Mr Fahour, who is also the Patron of the Islamic Museum of Australia said, “The exhibition showcases the diversity of Australia’s Muslim communities and the significant contribution they make to Australia’s contemporary, multicultural society.” Mr Fahour welcomed these efforts that help to build understanding and respect between the Islamic community and other faiths and cultures. -

Annual Report 2014 (PDF)

Impact 2014 Together we are working toward our vision of a community where every woman and girl has the opportunity to reach her full potential. Dear Supporter, The Women’s Fund of Omaha dedicated 2014 to building our capacity to improve the lives of women and girls through research, grants, and advocacy. Here are the highlights of what we accomplished in 2014 because of you: Identifying Issues The Women’s Fund of The cornerstone of our mission is to seek relevant, credible information Omaha is a trusted expert concerning the status of women and girls in our community. Through surveys in the community, we identify and in-depth research we are able to identify major issues that impact their critical issues, fund innovative lives. In 2014, we completed the following research: solutions and influence dynamic change. Since our beginning in 1990, the ► Adolescent Health Project (AHP) –This project seeks to create Women’s Fund has supported sustainable community-wide changes through a research-based, results local agencies with more focused, comprehensive approach that will: (1) increase the sexual than $4.5 million in grants for knowledge and health of youth and, thereby, (2) decrease the number programs that address the most of youth engaging in risky sexual behavior and the rates of STDs and pressing issues as identified teen pregnancy. Learn more about AHP at http://goo.gl/lG2rlN by our research, and we have established our own programs to meet ► Women’s Voices & the U-VISA - A qualitative study designed to assess unaddressed needs. the impact of the U-VISA program from the Latina women that have used the program to escape intimate partner violence. -

Rebuilding Bank Governance After the Financial Crisis: Best Practices Thomson Reuters CONTENTS

REBUILDING BANK GOVERNANCE AFTER THE FINANCIAL CRISIS: BEST PRACTICES THOMSON REUTERS CONTENTS WHY BANKS ARE DIFFERENT . 3 ESTABLISHING A FRAMEWORK FOR ASSESSING RISK . 4 FOCUSING ON THE RIGHT DATA REMAINS A CORE CHALLENGE . 5 FINDING THE RIGHT PEOPle – EXPERIENCE IS KEY, BUT NOT THE ONLY ANSWER . 5 A SPOTLIGHT ON EXECUTIVE PAY . 6 CONCLUSION . 7 2 REBUILDING BANK GOVERNANCE AFTER THE FINANCIAL CRISIS: BEST PRACTICES OCTOBER 2012 Demands on bank directors have rarely been There is also a wider array of risks bank higher . Following the financial crisis of 2008, managements and boards must assess in board members in the U .s . and Europe contrast to other industries . These include have confronted dozens of new rules from a credit; market; liquidity; operational; legal and multitude of regulators, while striving to regain reputational risks . At any time, one of these the confidence of customers and shareholders . risks has the potential to jeopardize the bank’s Amidst this newfound scrutiny, bank boards business—making it critical for board members are increasingly being held accountable, with to have timely access to information . regulators as well as private plaintiffs pursuing The regulatory scrutiny to which banks are claims when performance falters . In the first subject, as well as the rising risk of litigation, nine months of 2012, the FDIC authorized suits makes it particularly important for banks to against 274 defendants—although many of be able to point to an effective governance these will ultimately be settled . structure . For example, banks should give The scrutiny shows no sign of abating . Just in careful thought to what percentage of directors the last few months, there has been the Libor are ‘inside’ directors versus independent rate-setting scandal that led to the resignation directors; what the appropriate board of Barclays chief executive, and the unexpected committees are to establish and of course, who trading loss of more than $5 .8 billion at is best equipped to run those committees . -

Comunicado De Prensa 78-2016.Pdf

– – – – Evaluación Calificación Estatus Final De 80% a 100% Calidad Buena De 51% a 79% Calidad Regular Menor o igual a 50% Calidad Deficiente Instrumento No. de emisoras Verde Amarillo Rojo Acciones 137 124 5 8 Deuda a largo plazo 66 66 - - FIBRAs* 11 11 - - CKDs 55 55 - - Total 269 256 5 8 * Incluye un fideicomiso hipotecario. Nota: La calificación que obtuvo cada una de las emisoras evaluadas se detalla en el Anexo 1 de este comunicado. , Clave de Razón Social de la emisora (ACCIONES) Calificación Pizarra Accel, S.A.B. de C.V. ACCELSA 100 Alfa, S.A.B. de C.V. ALFA 100 Alpek, S.A.B. de C.V. ALPEK 100 América Móvil, S.A.B. de C.V. AMX 100 Arca Continental, S.A.B. de C.V. AC 100 Axtel, S.A.B. de C.V. AXTEL 100 Banregio Grupo Financiero, S.A.B. de C.V. GFREGIO 100 Bio Pappel, S.A.B. de CV PAPPEL 100 Bolsa Mexicana de Valores, S.A.B. de C.V. BOLSA 100 Casa de Bolsa Finamex, S.A.B. de C.V. (3) FINAMEX 100 Cemex, S.A.B. de C.V. CEMEX 100 CMR, S.A.B. de C.V. CMR 100 Coca-Cola FEMSA, S.A.B. de C.V. KOF 100 Compañia Minera Autlan, S.A.B. de C.V. AUTLAN 100 Consorcio Ara, S.A.B. de C.V. ARA 100 Consorcio Aristos, S.A.B. de C.V. ARISTOS 100 Controladora Vuela Compañía de Aviación, S.A.B. de C.V. VOLAR 100 Convertidora Industrial, S.A.B. -

Mos Episode Transcript: Sallie Krawcheck REID HOFFMAN

MoS Episode Transcript: Sallie Krawcheck REID HOFFMAN: When you think of the first computer, maybe you imagine a huge mainframe in a college lab in the 1950s; serious-looking people in white coats feeding in punch cards as the machinery whirs. But the story of computing started much earlier. And it probably looked a bit different than you imagine. STEVEN JOHNSON: In the 1830s Charles Babbage, the British inventor, invented basically a programmable computer that was a hundred years ahead of its time. HOFFMAN: That’s Steven Johnson, host of the podcast “American Innovations”, and author of many books about technology and progress that you should read. Steven’s latest book is called Farsighted: How We Make the Decisions That Matter the Most. As he wrote it, he kept thinking about Babbage and this first computer. JOHNSON: These machines had almost all the key elements of modern computing. They were programmable, they had the sense of a CPU, they had the sense of RAM, the sense of a hard drive-like storage. HOFFMAN: There was just one small problem: this was the 1830s. Scientists hadn’t yet mastered electricity. Babbage’s designs were too complex to be built. But this didn’t stop them from sparking people’s imaginations. And one person they sparked was a mathematician named Ada Lovelace. JOHNSON: Lovelace was a young woman who was a math prodigy at a time when this is very unusual. And she is now widely considered to be the first software programmer. HOFFMAN: Lovelace wrote the first example of what we’d now call “computer code”. -

Printmgr File

Citigroup Inc. 399 Park Avenue New York, NY 10043 March 13, 2007 Dear Stockholder: We cordially invite you to attend Citigroup’s annual stockholders’ meeting. The meeting will be held on Tuesday, April 17, 2007, at 9AM at Carnegie Hall, 154 West 57th Street in New York City. The entrance to Carnegie Hall is on West 57th Street just east of Seventh Avenue. At the meeting, stockholders will vote on a number of important matters. Please take the time to carefully read each of the proposals described in the attached proxy statement. Thank you for your support of Citigroup. Sincerely, Charles Prince Chairman of the Board and Chief Executive Officer This proxy statement and the accompanying proxy card are being mailed to Citigroup stockholders beginning about March 13, 2007. Citigroup Inc. 399 Park Avenue New York, NY 10043 Notice of Annual Meeting of Stockholders Dear Stockholder: Citigroup’s annual stockholders’ meeting will be held on Tuesday, April 17, 2007, at 9AM at Carnegie Hall, 154 West 57th Street in New York City. The entrance to Carnegie Hall is on West 57th Street just east of Seventh Avenue. You will need an admission ticket or proof of ownership of Citigroup stock to enter the meeting. At the meeting, stockholders will be asked to ➢ elect directors, ➢ ratify the selection of Citigroup’s independent registered public accounting firm for 2007, ➢ act on certain stockholder proposals, and ➢ consider any other business properly brought before the meeting. The close of business on February 21, 2007 is the record date for determining stockholders entitled to vote at the annual meeting. -

A Century of Ideas

COLUMBIA BUSINESS SCHOOL A CENTURY OF IDEAS EDITED BY BRIAN THOMAS COLUMBIA BUSINESS SCHOOL Columbia University Press Publishers Since 1893 New York Chichester, West Sussex cup.columbia.edu Copyright © 2016 Columbia Business School All rights reserved Library of Congress Cataloging-in-Publication Data Names: Thomas, Brian, editor. | Columbia University. Graduate School of Business. Title: Columbia Business School : a century of ideas / edited by Brian Thomas. Description: New York City : Columbia University Press, 2016. | Includes bibliographical references and index. Identifiers: LCCN 2016014665| ISBN 9780231174022 (cloth : alk. paper) | ISBN 9780231540841 (ebook) Subjects: LCSH: Columbia University. Graduate School of Business—History. Classification: LCC HF1134.C759 C65 2016 | DDC 658.0071/17471—dc23 LC record available at https://lccn.loc.gov/2016014665 Columbia University Press books are printed on permanent and durable acid-free paper. Printed in the United States of America c 10 9 8 7 6 5 4 3 2 1 contents Foreword vii 1 Finance and Economics 1 2 Value Investing 29 3 Management 55 4 Marketing 81 5 Decision, Risk, and Operations 107 6 Accounting 143 7 Entrepreneurship 175 vi CONTENTS 8 International Business 197 9 Social Enterprise 224 Current Full-Time Faculty at Columbia Business School 243 Index 247 foreword Ideas with Impact Glenn Hubbard, Dean and Russell L. Carson Professor of Finance and Economics Columbia Business School’s first Centennial offers a chance for reflection about past success, current challenges, and future opportunities. Our hundred years in business education have been in a time of enormous growth in interest in university-based business education. Sixty-one students enrolled in 1916. -

Group Corporate Affairs

Group Corporate Affairs 500 Bourke Street Melbourne Victoria 3000 AUSTRALIA www.nabgroup.com National Australia Bank Limited ABN 12 004 044 937 ASX Announcement Monday 17 November 2008 NAB Australian Region market update National Australia Bank Executive Director and CEO Australia, Ahmed Fahour, is conducting a series of market briefings following the release of the NAB full year results on Tuesday 21 October. The briefing materials are attached and are largely based on the information disclosed during the full year results announcement. “NAB’s Australian Region continues to deliver excellent results in a challenging market, demonstrating increased revenue growth and a tight focus on cost control,” Mr Fahour said. “This is an outstanding achievement when viewed in the context of the external environment over the course of the year. “Throughout this difficult time NAB has continued to invest in our business by developing new brands such as UBank, extending our microfinance initiatives, delivering new products such as the Clear home loan, and commencing new infrastructure initiatives such as our Next Generation platform. “NAB has remained strong through these challenging conditions, and continues to focus on providing excellent support and service to our customers,” Mr Fahour said. Australian Region Financial Performance The Australia Region delivered cash earnings growth (before IoRE) of 15.8% and underlying profit growth of 19.3% over the prior comparative period. Revenue growth of 10.1% was an excellent result achieved in a very challenging environment. The strong performance of cash earnings growth of 18.5% by the Australia Banking business reflects continued momentum in business lending and consumer deposit gathering.