The French Automotive Industry 2014 Analysis and Statistics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PRESS RELEASE Groupe PSA and FCA Plan to Join Forces to Build A

PRESS RELEASE IMPORTANT NOTICE By reading the following release, you further agree to be bound by the following limitations and qualifications: This communication is for informational purposes only and is not intended to and does not constitute an offer or invitation to exchange or sell or solicitation of an offer to subscribe for or buy, or an invitation to exchange, purchase or subscribe for, any securities, any part of the business or assets described herein, or any other interests or the solicitation of any vote or approval in any jurisdiction in connection with the proposed transaction or otherwise, nor shall there be any sale, issuance or transfer of securities in any jurisdiction in contravention of applicable law. This communication should not be construed in any manner as a recommendation to any reader of this communication. This communication is not a prospectus, product disclosure statement or other offering document for the purposes of Regulation (EU) 2017/1129 of the European Parliament and of the Council of June 14th 2017, as amended from time to time and as implemented in each member State of the European Economic Area and under French and Dutch law and regulation. An offer of securities in the United States pursuant to a business combination transaction will only be made, as may be required, through a prospectus which is part of an effective registration statement filed with the US Securities and Exchange Commission (“SEC”). Shareholders of Fiat Chrysler Automobiles N.V. (“FCA”) and Peugeot S.A. who are US persons or are located in the United States are advised to read the registration statement when and if it is declared effective by the US Securities and Exchange Commission because it will contain important information relating to the proposed transaction. -

Shareholders

LETTER TO OUR SHAREHOLDERS SEPTEMBER 2016 P.3 P.4 P.6 P.8 PERFORMANCE HIGHLIGHTS DECIPHERING SHAREHOLDER THE DATA INFORMATION P.4 P. 5 In the first half of 2016, our revenue of €3.2 billion was up by 11%, and our profitability was growing even faster, with an operating margin up by nearly 13%. LAURENT BURELLE CHAIRMAN AND CHIEF EXECUTIVE OFFICER P. 2 P. 6 MESSAGE from the Chairman and Chief Executive Officer You can find the presentation of the 2016 half-year results at www.plasticomnium.com €3.2 billion revenue +8% €267 million operating margin +12.7% TO OUR SHAREHOLDERS, During the first half of 2016, Plastic Omnium once again Such performance is €155 million achieved a record level of proof of the continuous net profit, revenue and results. Our revenue commitment of of €3.2 billion was up by 11%, Group share and our profitability was growing our employees to even faster, with an operating margin operational excellence. up by nearly 13%. For the first time, +9.5% our operating margin exceeded the historic level of 10%. LAURENT BURELLE At the same time, our net debt Chairman and has been even further reduced. Chief Executive Officer €383 million Such performance is proof of EBITDA the continued commitment of our employees to operational It is this extremely healthy financial excellence – total quality position which has made it possible +10.5% in development and production, for us to seize an opportunity and perfect logistics. for sizeable external growth, with This operational excellence, the acquisition of Faurecia’s Exterior together with a policy of sustained Systems, carried out on July 29. -

P 01.Qxd 6/30/2005 2:00 PM Page 1

p 01.qxd 6/30/2005 2:00 PM Page 1 June 27, 2005 © 2005 Crain Communications GmbH. All rights reserved. €14.95; or equivalent 20052005 GlobalGlobal MarketMarket DataData BookBook Global Vehicle Production and Sales Regional Vehicle Production and Sales History and Forecast Regional Vehicle Production and Sales by Model Regional Assembly Plant Maps Top 100 Global Suppliers Contents Global vehicle production and sales...............................................4-8 2005 Western Europe production and sales..........................................10-18 North America production and sales..........................................19-29 Global Japan production and sales .............30-37 India production and sales ..............39-40 Korea production and sales .............39-40 China production and sales..............39-40 Market Australia production and sales..........................................39-40 Argentina production and sales.............45 Brazil production and sales ....................45 Data Book Top 100 global suppliers...................46-50 Mary Raetz Anne Wright Curtis Dorota Kowalski, Debi Domby Senior Statistician Global Market Data Book Editor Researchers [email protected] [email protected] [email protected], [email protected] Paul McVeigh, News Editor e-mail: [email protected] Irina Heiligensetzer, Production/Sales Support Tel: (49) 8153 907503 CZECH REPUBLIC: Lyle Frink, Tel: (49) 8153 907521 Fax: (49) 8153 907425 e-mail: [email protected] Tel: (420) 606-486729 e-mail: [email protected] Georgia Bootiman, Production Editor e-mail: [email protected] USA: 1155 Gratiot Avenue, Detroit, MI 48207 Tel: (49) 8153 907511 SPAIN, PORTUGAL: Paulo Soares de Oliveira, Tony Merpi, Group Advertising Director e-mail: [email protected] Tel: (35) 1919-767-459 Larry Schlagheck, US Advertising Director www.automotivenewseurope.com Douglas A. Bolduc, Reporter e-mail: [email protected] Tel: (1) 313 446-6030 Fax: (1) 313 446-8030 Tel: (49) 8153 907504 Keith E. -

Registration Document

20 REGISTRATION DOCUMENT Including the annual financial report 17 GROUPE PSA - 2017 REGISTRATION DOCUMENT -1 ANALYSIS OF THE BUSINESS AND GROUP OPERATING RESULTS IN 2017 AND OUTLOOK Capital Expenditure in Research & Development 4.4.2. Banque PSA Finance, signature of a framework agreement with the BNP Paribas Group to form a car financing Partnership for Opel Vauxhall vehicles On 6 March 2017, when the Master Agreement was concluded with BNP Paribas Personal Finance, will from an accounting point of view General Motors, the Company simultaneously signed a Framework retain the current European platform and staff of GM Financial. The Agreement with BNP Paribas and BNP Paribas Personal Finance, to Opel Vauxhall finance companies will distribute financial and organise the joint purchase of Opel Vauxhall’s finance companies insurance products over a territory initially including the following and the setting up of a car financing partnership for Opel Vauxhall countries: Germany, United Kingdom, France, Italy, Sweden, Austria, vehicles. Ireland, Netherlands, Belgium, Greece and Switzerland. The The acquisition of Opel Vauxhall’s finance companies will be cooperation may potentially be extended thereafter to other completed through a holding company. This joint venture, owned in countries where Opel Vauxhall has a presence. equal shares and on the same terms by Banque PSA Finance and 4.5. CAPITAL EXPENDITURE IN RESEARCH & DEVELOPMENT Automotive Expertise to deliver useful technologies Innovation, research and development are powerful levers for Every year, Groupe PSA invests in research and development to developing competitive advantages by addressing the major stay ahead, technologically, of environmental and market changes. challenges faced in the automotive industry (environmental, safety, emerging mobility and networking needs, etc.). -

Who's Who at Europe's Supplier Parks

AN_070319_23.qxd 15.03.2007 11:19 Uhr Page 23 March 19, 2007 www.autonewseurope.com · PAGE 23 2007 Guide to purchasing Who’s who at Europe’s supplier parks AUDI VOLKSWAGEN 1. Ingolstadt 23. Autoeuropa Supplier Park opened in 1995 Supplier Park opened in 1995 Ingolstadt Logistics Center (GVZ) Palmela, Quinta da Marquesa, 85057 Ingolstadt, Germany Quinta do Anjo, Portugal Tel :(49) 841-890 Tel: (351) 1-321-2541/2601 Carcoustics: door sound proofing; Delphi: interior ArvinMeritor, Benteler, Edscha, Faurecia, Tenneco; wiring harness; Dräxlmaier: wiring, instrument panels; Hayes Lemmerz: wheels; Kautex; Magna Donnelly; Pal- Faurecia: front-end modules; Montes: air filters and metal: Logistics; PPG; Vanpro (joint venture JCI-Faurecia) filtration equipment; Preymesser: consolidation tasks Rehau: bumpers; Scherm: logistics; Röchling Auto- 24. Brussels 30 motive: door trim; Siemens VDO: fuel tanks; Tenneco: Supplier Park opened in 2001 emission control systems; Venture/Peguform: door trim Blvd. De la 2eme Armee, Britannique 201, 201, Britse Tweedelegerlaan, 2a. Neckarsulm 1190 Brussels, Belgium Supplier Park opened in 1996 15 Tel: (32) 2-348-2111 Bad Friedrichshall Industry and Commerce Park ArvinMeritor: door mechanisms, fittings; Expert: 28 NSU Str. 24-32 13 4 bumpers; Inergy: fuel tanks; Hayes Lemmerz: wheels; 74172 Neckarsulm, Germany Siemens VDO: fuel tanks; Sumitomo Electric Indus- 26 Tel: (49) 7132-310 12 24 11 tries: electrical cables AFL Michels: wiring; Plastal: bumpers; Faurecia: floor- 19 29 8 ing; Fritz Logistik: logistics; Grammer: central consoles; 2a 3 25. Pamplona 5 2b HP Pelzer: roofs; Johnson Controls: instrument panels, 18 1 16 Supplier Park opened in 1999 6 27 pillars; Rhenus: logistics; Siemens VDO: fuel tanks; 9 Pol. -

Air Dryer Cartridge 5001004902 New

AIR DRYER CARTRIDGE 5001004902 NEW Product Images PARTS THAT ARE NOT INCLUDED, CAN BE OFFERED ON REQUEST This is general information. Depending on the engine model, deviations are possible WWW.HAMOFA.COM PARTS THAT ARE NOT INCLUDED, CAN BE OFFERED ON REQUEST This is general information. Depending on the engine model, deviations are possible WWW.HAMOFA.COM Additional Information MARKE RENAULT Replaces Ref. No. Agrale 6008099011006 Askam 25242T Astra 0010 7163 Astra 0017 4767 Astra 0819 0948 Astra 5 0313 7484 Astra 5 0313 7742 Bluebird 5008414 BMC 9P917828 DAF 1504900 DAF 1505970 DAF 1518683 DAF 1527756 DAF 6993878 DAF BBU8146 DAF BBU9424 Demag 76117673 Dennis 4324102227 Dennis 4324102227WHITE Dennis 6528852 ERF 1368731 Faun 99707305720 Fendt F 931 882 140 010 Fiat 0017 4767 Fiat 0190 0812 Fiat 0190 7612 Fiat 0299 2261 Fiat 0812 3564 Fiat 0819 0948 Fiat 1990 7612 Fiat 21 3091 2136 Fiat 5 0313 7484 Fiat 5 0313 7742 Fiat 58 0138 2289 Fiat 80 1011 2016 Fiat 8512 7004 Fiat 9844 6957 Fruehauf CF352490 Heuliez 0299 2261 Heuliez 5 0344 6090 Iveco 0017 4767 Iveco 0190 0812 Iveco 0190 7612 Iveco 0299 2261 Iveco 0812 3564 Iveco 0819 0948 Iveco 0819 0984 Iveco 17 4767 Iveco 190 7612 Iveco 1990 7612 Iveco 21 3091 2136 Iveco 299 2261 Iveco 5 0005 0616 Iveco 5 0313 5256 Iveco 5 0313 7484 Iveco 5 0313 7742 Iveco 50 0183 0112 Iveco 50 0186 5037 Iveco 50 0601 6342 Iveco 80 1000 2016 Iveco 80 1011 2016 Iveco 812 3564 Iveco 819 0948 JCB 15/920105 John Deere AL204884 Kamaz 00100000 King Long 35G4211501 Kögel 326549 Liebherr 571352308 Mack 950011 MAN 04.32410.2227 MAN 08.15210.2008 MAN 79.20036.1087 MAN 79.20036.1090 MAN 81.52102.0008 MAN 81.52102.0009 MAN 81.52102.0010 MAN 81.52102.0013 Ersetzt Ref. -

Who Supplies Whom in Europe

20080317-GTP_who_supplies.qxd 3/14/08 5:58 PM Page 2 2008 Guide to purchasing Who supplies whom in Europe Audi BMW Fiat Ford GM Europe Jaguar-Land RoverMercedes/Smart Air conditioning Behr, Denso, Valeo Behr, Denso, Valeo Denso, Valeo Behr, Visteon Behr, Delphi, Valeo Behr, Denso, Visteon Behr, Denso, Eberspächer, Valeo Airbags Autoliv, Key Safety Systems, Alcoa, Autoliv, Takata Petri, Autoliv, Key Safety Systems, Autoliv, Takata-Petri, Autoliv, Key Safety Systems, Autoliv Alcoa , Autoliv, Takata-Petri, Takata-Petri, TRW TRW Automotive TRW Automotive TRW Automotive Takata-Petri, TRW Automotive TRW Automotive Antilock brakes Bosch, Continental Bosch, Continental Bosch, TRW Automotive Continental, TRW Automotive Bosch, Continental, Bosch, Continental Bosch TRW Automotive Automatic Aisin AW, Magneti Marelli, ZF Friedrichshafen Aisin AW, Magneti Marelli Jatco, Magneti Marelli Aisin AW, Magneti Marelli ZF Friedrichshafen Getrag, Magneti Marelli, ZF Friedrichshafen transmissions ZF Friedrichshafen, ZF Sachs Axles Volkswagen Braunschweig Alcoa, ThyssenKrupp, Johnson Controls, Magneti Marelli, Benteler Delphi, Magneti Marelli Dana, Visteon Benteler, ThyssenKrupp, TMD Friction ZF Friedrichshafen TRW Automotive, Varta Batteries Johnson Controls, Moll, Varta Johnson Controls, Seeber, Varta, n/a Johnson Controls, Benteler Delphi, Johnson Controls, Delphi, Johnson Controls, Varta Johnson Controls, Varta, Voestalpine Vb Autobatterie Varta, Vb Autobatterie Brake lines/ Continental, Cooper-Standard, Continental, Freudenburg, FTE, Bosch, CF Gomma, Continental, -

Press Release

Press release Nanterre (France), October 23, 2020 THIRD-QUARTER 2020 SALES Q3 SALES SIGNIFICANTLY BETTER THAN PREVIOUSLY EXPECTED H2 GUIDANCE UPGRADED In €m Q3 2019 Q3 2020 Change 9m 2019 9m 2020 Change Group sales 4,185 3,874 -7.4% 13,157 10,043 -23.7% At constant scope and currencies -7.0% -26.4% Q3 SALES SIGNIFICANTLY BETTER THAN PREVIOUSLY EXPECTED ▪ Strong sequential improvement at constant scope and currencies: -7.0% in Q3, after -19.7% in Q1 and -50.0% in Q2 ▪ Month-after-month improvement throughout the quarter, with September up 1.2% year-on- year ▪ Strong sales in China, up 15.4% at constant scope and currencies ▪ Outperformance of Seating and Clean Mobility (representing combined 65% of Group sales), while Interiors and Clarion Electronics underperformed the market H2 GUIDANCE UPGRADED With the revised assumption that worldwide automotive production in H2 should drop in the mid- single digits vs. H2 2019 (vs. “down around 15%” as announced on July 27), Faurecia is upgrading its financial targets for the second half of the year: ▪ Sales of at least €8 billion (vs. “around €7.6 billion” as announced on July 27) ▪ Operating income of at least 5.5% of sales (vs. “around 4.5% of sales” as announced on July 27) ▪ Net cash flow of at least €700m (vs. “around €600 million” as announced on July 27) Patrick KOLLER, CEO of Faurecia, declared: “Our sales in Q3 were better than previously expected. Despite ongoing uncertainty related to the Covid-19, we are now more confident about worldwide automotive production in the second half of the year that should drop only in the mid- single digits vs. -

Final Frm Map.Qxd

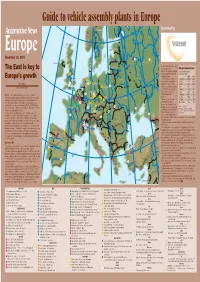

Guide to vehicle assembly plants in Europe NORWAY SWEDEN Sponsored by 33 16 ESTONIA 12 9 November 29, 2004 11 9 LATVIA 18 1 RUSSIA IRELAND DENMARK 21 greater worker flexibility and local U. K. LITHUANIA The East is key to sales growth, says Europe’s top producers 4 35 Felix Kuhnert, an auto consultant Vehicle assembly capacity, 12 for PricewaterhouseCoopers in 7 10 in thousands of units 12 14 7 29 southern Germany. 2004 2009 Europe’s growth “But being present in these 1. Germany 6,190 6,398 9 16 12 1 BELARUS 8 1 markets and the possibility to 2. France 4,356 4,500 7 6 2 7 JESSE SNYDER 5 10 4 export from there is another 3. Spain 3,329 3,318 14 4 NETH. 15 1 14 5 driver,” he said. “However, if you 4. UK 2,632 2,613 AUTOMOTIVE NEWS EUROPE 3 POLAND 6 19 look at the EU capacity trends 5. Russia 1,874 2,113 9 13 13 4 GERMANY through 2007 you also see 6. Italy 1,803 1,802 5 1 11 2 25 significant expansion in 7. Belgium 1,133 1,222 MUNICH – The manufacturing movement to the East continues. 2 5 BELGIUM 5 3 18 8 Germany.” 8. Turkey 1,003 1,105 New and expanded plants in eastern Europe have driven total vehicle 6 3 3 3 17 8 UKRAINE assembly capacity in greater Europe above 26 million units a year. 2 5 LUX. 19 Helped by the 2005 opening of 9. Poland 847 654 6 4 In central and eastern Europe, manufacturers are rapidly adding 31 1 7 CZECH a BMW plant in Leipzig, 10.Czech Rep. -

Stellantis Announces Conditional Distribution of Faurecia Shares and Cash

PRESS RELEASE Stellantis announces conditional distribution of Faurecia shares and cash Amsterdam, March 4, 2021 – Stellantis N.V. (NYSE / MTA / Euronext Paris: STLA) (“Stellantis”) announced today a conditional distribution by Stellantis to the holders of its common shares of up to 54,297,006 ordinary shares of Faurecia S.E. (“Faurecia”) and up to €308 million in cash, being the proceeds received by Peugeot S.A. from the sale of ordinary shares of Faurecia in October 2020, payable to holders of Stellantis common shares of record as of Tuesday, March 16, 2021, pursuant to a capital reduction (the “Distribution”). Payment of the Distribution is conditional upon the further announcement that the Distribution has been approved by the Extraordinary General Meeting of Shareholders of Stellantis to be held on March 8, 2021 and that certain Dutch law formalities have been satisfied. Absent such announcement that the Distribution has become unconditional, no Distribution will be payable. If the Distribution becomes unconditional as described above, the expected calendar for the Distribution will be as follows: (i) ex-date on Monday, March 15, 2021; and (ii) record date on Tuesday, March 16, 2021. Holders of Stellantis common shares will be entitled to: (i) 0.017029 ordinary shares of Faurecia; and (ii) Euro 0.096677 for each common share of Stellantis they hold on the record date for the Distribution. The cash portion of the Distribution is expected to be paid on or about Monday, March 22, 2021. Generally, the ordinary shares of Faurecia are expected to be delivered to holders of Stellantis common shares entitled thereto on or about Monday, March 22, 2021. -

France Axa Private Equity Cède Sa Participation

BRÈVES DE 10H30 2013/04/12 FRANCE AXA PRIVATE EQUITY CÈDE SA PARTICIPATION MAJORITAIRE DANS AIXAM MEGA Axa Private Equity a cédé sa participation majoritaire dans Aixam Mega, groupe français spécialisé dans la production de voitures sans permis, à l’américain Polaris Industries. Aixam Mega gère deux usines de production en France et a généré en 2012 un chiffre d’affaires de 90 millions d’euros (5 000 voitures écoulées dans l’Hexagone). (Echos) Par Alexandra Frutos HEULIEZ A SIX MOIS POUR SURMONTER SES DIFFICULTÉS Heuliez a été placé en redressement judiciaire le 11 avril par le tribunal de commerce de Niort, qui lui a laissé six mois pour surmonter ses difficultés. Dans son jugement, le tribunal décrète le redressement judiciaire et accorde une période d’observation de six mois, laissant à l’administrateur du temps pour trouver un éventuel repreneur, alors que le carrossier de Cerizay (Deux-Sèvres) est en lice pour gagner un important contrat avec Volkswagen.(Figaro) Par Alexandra Frutos LA MORTALITÉ ROUTIÈRE A DIMINUÉ DE 26,8 % EN MARS ET DE 11,1 % AU PREMIER TRIMESTRE Le nombre de personnes décédées dans des accidents de la route a diminué de 26,8 % en mars (203 victimes) et de 11,1 % au premier trimestre (692 victimes). (Largus.fr) Par Alexandra Frutos LANCEMENT DES NOUVELLES SÉRIES SPÉCIALES PEUGEOT ROLAND GARROS Comme chaque année depuis 29 ans, le Tournoi de tennis de Roland Garros s’accompagne de la commercialisation de la série spéciale éponyme chez Peugeot. Trois modèles richement dotés sont concernés : la 207 CC, la 308 CC et le 3008. -

Transports ; Direction Des Transports Terrestres (1923-1989)

Transports ; Direction des transports terrestres (1923-1989) Répertoire (19920581/1-19920581/69) Archives nationales (France) Pierrefitte-sur-Seine 1992 1 https://www.siv.archives-nationales.culture.gouv.fr/siv/IR/FRAN_IR_018269 Cet instrument de recherche a été encodé en 2011 par l'entreprise diadeis dans le cadre du chantier de dématérialisation des instruments de recherche des Archives Nationales sur la base d'une DTD conforme à la DTD EAD (encoded archival description) et créée par le service de dématérialisation des instruments de recherche des Archives Nationales 2 Archives nationales (France) INTRODUCTION Référence 19920581/1-19920581/69 Niveau de description fonds Intitulé Transports ; Direction des transports terrestres Date(s) extrême(s) 1923-1989 Nom du producteur • Direction des transports terrestres Localisation physique Pierrefitte DESCRIPTION Présentation du contenu Sommaire Art 1-14 : Rapports d’inspection générale des directions départementales et régionales de l’équipement, fonctionnement de l’association des inspecteurs des transports, 1961-1984. Art 15-32 : Coopération internationale et accords en matière de transports :. PV de réunions des conseils des ministres de la CEE, 1961-1975. Travaux de la CEE consacrée à la mise en place de la Tarification d’Usage des Infrastructures (TUI), 1961-1981. PV de réunions de la Conférence Européenne des Ministres des Transports (CEMT), 1953-1988. Accords multilatéraux et bilatéraux, 1960-1989. Art 33-39 : Tutelle de la Caisse Autonome Mutuelle de Retraite (CAMR) et la Caisse Autonome de Retraites Complémentaires et de Prévoyance des Transports (CARCEPT) : Législation, réglementation, législation de la sécurité sociale, 1923-1986. Art 40-42 : Participation du Fonds de Développement Economique et Social (FDES) concernant la RATP et la SNCF : Projets d’investissements, compte rendus de réunions, 1981-1986.