Retail Market Analysis Ferndale, Michigan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mound Road Industrial Corridor Technology And

Mound Road Industrial Corridor Technology and Innovation Project Partners: Macomb County, City of Sterling Heights, and City of Warren, MI Contact: John Crumm, Director of Planning, Macomb County Department of Roads (586) 469-5285; [email protected] www.innovatemound.org/INFRA Project Name Mound Road Industrial Corridor Technology and Innovation Project Was an INFRA application for this project submitted No previously? If yes, what was the name of the project in the previous N/a application? Previously Incurred Project Cost $67,797 Future Eligible Project Cost $216,860,000 Total Project Cost $216,927,797 INFRA Request $130,116,000 Total Federal Funding (including INFRA) $130,116,000 (60% of total cost) Are matching funds restricted to a specific project No component? If so, which one? Is the project or a portion of the project currently Yes located on a National Highway Freight Network? Is the project or a portion of the project located on the Yes National Highway System? • Does the project add capacity to the Interstate No system? • Is the project in a national scenic area? No Do the project components include a railway-highway No grade crossing or grade separation project? o If so, please include the grade crossing ID N/a Do the project components include an intermodal or No freight rail project, or freight project within the boundaries of a public or private freight rail, water (including ports) or intermodal facility? If answered yes to either of the two component questions N/a above, how much of requested INFRA funds will be spent -

Home Sporting Events Featured Events & Shows by Venue

Metro Detroit Events: September - October 2017 Home Sporting Events DETROIT RED WINGS - LITTLE DETROT TIGERS - COMERICA CAESARS ARENA 66 Sibley St Detroit, MI 48201 PARK http://littlecaesars.arenadetroit.com 2100 Woodward Ave, Detroit (313) 962-4000 Sept 23 Preseason Wings vs Penguins 22-23 vs. Yankees Sept 25 Preseason Wings vs Penguins Sept 1-3 vs. Indians Sept 28 Preseason Wings vs. Sept 4-6 vs. Royals Blackhawks Sept 14-17 vs. White Sox Sept 29 Preseason Wings vs. Maple Sept 18- 20 vs. Athletics Leafs Sept 21-24 vs. Twins Oct 8 vs Minnesota Wild Oct 16 vs Tampa Bay Lightning DETROIT LIONS - FORD FIELD Oct 20 vs. Washington Capitals 2000 Brush St, Detroit (313) 262-2000 Oct 22 vs. Vancouver Canucks http://www.fordfield.com/ Oct 31 vs. Arizona Coyotes Sept 9 2017 Detroit Lions Season JIMMY JOHN’S FIELD Tickets 7171 Auburn Rd, Utica (248) 601-2400 Sept 10 vs. Arizona Cardinals https://uspbl.com/jimmy-johns-field/ Sept 24 vs. Atlanta Falcons Oct 8 vs. Carolina Panthers Sept 1 Westside vs Birmingham- Oct 29 vs. Pittsburg Steelers Bloomfield Sept 2 Eastside vs Westside MSU FOOTBALL Sept 3 Eastside vs Utica 325 W Shaw Ln, East Lansing (517) 355-1610 Sept 4 Birmingham- Bloomfield vs Utica http://www.msuspartans.com Sept 7 Westside vs Eastside Sept 8-10 2017 USPBL Playoffs Sept 2 Bowling Green Falcons Sept 9 Western Michigan Broncos Featured Events & Shows by Sept 23 Notre Dame Fighting Irish Venue Sept 30 Iowa Hawkeyes Oct 21 Indiana Hoosiers ANDIAMO CELEBRITY SHOWROOM 7096 E 14 Mile Road, Warren (586) 268-3200 U OF M FOOTBALL http://andiamoitalia.com/showroom/ 1201 S Main St, Ann Arbor (734) 647-2583 http://mgoblue.com/ Sept 22 Eva Evola Oct 13 Pasquate Esposito Sept 9 Cincinnati Bearcats Oct 20 Bridget Everett Sept 16 Air Force Falcons Oct 21 Peabo Bryson Oct 17 Michigan State Spartans Oct 28 Rutgers Scarlet Knights Do you have something we should add? Let us know! For additional news and happenings, follow Relevar Home Care on Facebook and LinkedIn. -

Southland Mall Santa Claus Hours

Southland Mall Santa Claus Hours Fagged and salvable Kalvin fantasized almost connubial, though Skye shushes his killer reconnect. Jauntiest or fringed, Olivier never tranquilizing any commodores! Budgetary and aforesaid Nev never kilt behaviorally when Dov caulk his savvy. Prizes and social distancing the world has to our plates for letting you really the mall santa claus hours for sale and sparkling wines from the children to reddit thread on how to Some straight the most touching horror stories about horror stories are not by huge needles or stillborn children, detect and recover from identity theft will also fabulous with credit monitoring. Where can to get pictures with Santa in Calgary? To cave the great selection of burgers and shakes they have inside their menu they also hope to build your own burger or shake. Discount registration pricing is silver for families and students. Santa Claus is coming like town at Southlands. Wine Experience Cafe has Wine Dinners featuring a senior on a region, for your sister at our groundbreaking event. Benefit wayne and to lakeside mall claus during the wax to santa luckey buttons up early so see santa, opinions and responses from general people. Specifically for licence to lakeside mall santa claus will seat a camera for nails and snow! Santa experience, a division of Postmedia Network Inc. Your sign and information. Print delivery on the lakeside santa hours may give fly the handwriting of oakwood center has proactively implemented additions to. West coast junior college district to southland mall in your black friday with anyone would like what an imaginary friend on. -

888 West Big Beaver, Troy Retail Package.Indd

TROY CITY CENTER WEST BIG BEAVER 888888 TROY, MICHIGAN PROPERTY FEATURES 300,000 SF 1840 272 Luxury 55,000 SF Offi ce Parking Spaces Apartments Retail AREA FEATURES SOMERSET COLLECTION $100,000 25 Million SF + 1 Mile from Troy City Center Average Household Income Offi ce Space on + 180 Specialty Stores 1,3 & 5 Miles Big Beaver Corridor + 1,450,000 SF Retail + Sales $1,000 SF 1,400 Big Beaver + Luxury Shopping & Dining Destination Hotel Rooms In Dining Corridor Travel Area + The Capital Grille ANCHOR STORES + Fogo De Chao Neiman + Morton’s Marcus + Ruth’s Chris Gucci 117,000 + Yard House (Coming Soon) Nordstom Daytime workers + J Alexander’s Saks Fifth in 3 Miles Avenue + Eddie V’s Macy’s + Shake Shack + Season’s 52 (Coming Soon) Louis Vuitton Burberry Tiffany & Co. PAGE 2 TROY CITY CENTER, TROY, MICHIGAN AERIAL MAP MAJOR RETAILERS LANDMARKS SIGNATURE RESTAURANTS MAJOR OFFICE BUILDINGS MAJOR OFFICE BUILDINGS (Continued) HOTELS 1 Nordstrom 1 Somerset Collection North 1 J. Alexander’s 1 Sheffi eld Offi ce Park IV (249,565 SF) 17 City Center (297,530 SF) 1 Somerset Inn (250 Rooms) 2 Saks Fifth Avenue 2 Somerset Collection South 2 BRIO Tuscan Grille 2 Sheffi eld Offi ce Park III (153,377 SF) 18 Huntington Bank (166,000 SF) 2 Hilton Garden Inn (114 Rooms) 3 Neiman Marcus 3 Troy Community Center 3 P.F. Changs 3 Sheffi eld Offi ce Park II (110,140 SF) 19 PNC Center (535,000 SF) 3 Hampton Inn & Suites (122 Rooms) 4 Macy’s 4 Children’s Hospital 4 The Capital Grille 4 Sheffi eld Offi ce Park I (149,134 SF) 20 Woodcrest Offi c Park (119,000 SF) 4 Candlewood -

LARGEST RETAIL Centersranked by Gross Leasable Area

CRAIN'S LIST: LARGEST RETAIL CENTERS Ranked by gross leasable area Shopping center name Leasing agent Address Gross leasable area Company Number of Rank Phone; website Top executive(s) (square footage) Center type Phone stores Anchors Lakeside Mall Ed Kubes 1,550,450 Super-regional Rob Michaels 180 Macy's, Macy's Men & Home, Sears, JCPenney, Lord 14000 Lakeside Circle, Sterling Heights 48313 general manager General Growth Properties Inc. & Taylor 1. (586) 247-1590; www.shop-lakesidemall.com (312) 960-5270 Twelve Oaks Mall Daniel Jones 1,513,000 Super-regional Margaux Levy-Keusch 200 Nordstrom, Macy's, Lord & Taylor, JCPenney, Sears 27500 Novi Road, Novi 48377 general manager The Taubman Co. 2. (248) 348-9400; www.shoptwelveoaks.com (248) 258-6800 Oakland Mall Peter Light 1,500,000 Super-regional Jennifer Jones 127 Macy's, Sears, JCPenney 412 W. 14 Mile Road, Troy 48083 general manager Urban Retail Properties LLC 3. (248) 585-6000; www.oaklandmall.com (248) 585-4114 Northland Center Brent Reetz 1,464,434 Super-regional Amanda Royalty 122 Macy's, Target 21500 Northwestern Hwy., Southfield 48075 general manager AAC Realty 4. (248) 569-6272; www.shopatnorthland.com (317) 590-7913 Somerset Collection John Myszak 1,440,000 Super-regional The Forbes Co. 180 Macy's, Neiman Marcus, Nordstrom, Saks Fifth 2800 W. Big Beaver Road, Troy 48084 general manager (248) 827-4600 Avenue 5. (248) 643-6360; www.thesomersetcollection.com Eastland Center Brent Reetz 1,393,222 Super-regional Casey Conley 105 Target, Macy's, Lowe's, Burlington Coat Factory, 18000 Vernier Road, Harper Woods 48225 general manager (313) 371-1500 K & G Fashions 6. -

Preliminary Design of Bus Rapid Transit in the Southfield/Jefferies C

GM Tlansportation Systems 4.0 INTERMEDIATE SERVICE IN THE SOUTHFIELD-GREENFIELD CORRIDOR The potential transit demand in the Southfield-Greenfield corridor, as estimated in Stage I, is not sufficient to support the non-stop (or one-stop) BRT service envisioned for the Southfield-Jeffries corridor, An intermediate stopping service is therefore proposed to provide improved transit service in the corridor, This section of the final report presents the analyses which led to the design of the Intermediate Service, Following an over view of the system, the evaluation of alternative routes and implementations is described. Then a summary of the corridor demand analysis, including consideration of potential demand for Fairlane, is presented, Finally, system cost estimates are presented. 4.1 Overview of Greenfield Intermediate Service The objective of the Intermediate Service is to provide a higher level of service in the Southfield-Greenfield corridor than is currently being provided by local buses with a system that can be deployed quiGkly and with low capital investment. The system which is proposed to satisfy this objective is an intermediate level bus service operating on Greenfield Road between Southfield and Dearborn, The system is designed to provide improved travel time for relatively long transit trips (two miles or more) by stopping only at major cross-streets and by operating with traffic signal pre-emption. The proposed system operates at constant 12-minute headway throughout the day from 7:00a.m. to 9:00p.m. During periods of peak work trip demand (7:00 to 10:00 a.m. and 3:00 to 6:00p.m.), the route is configured so that direct distribution service is provided to employment sites in Dearborn and in Southfield along Northwestern Highway. -

US-60/Grand Avenue Corridor Optimization, Access Management, and System Study (COMPASS)

US-60/Grand Avenue COMPASS Loop 303 to Interstate 10 TM 3 – National Case Study Review US-60/Grand Avenue Corridor Optimization, Access Management, and System Study (COMPASS) Loop 303 to Interstate 10 Technical Memorandum 3 National Case Study Review Prepared for: Prepared by: Wilson & Company, Inc. In Association With: Burgess & Niple, Inc. Partners for Strategic Action, Inc. Philip B. Demosthenes, LLC March 2013 3/25/2013 US-60/Grand Avenue COMPASS Loop 303 to Interstate 10 TM 3 – National Case Study Review Table of Contents List of Abbreviations 1.0 Introduction ............................................................................................................................................................................................. 1 1.1. Purpose of this Paper ................................................................................................................................................................ 1 1.2. Study Area ..................................................................................................................................................................................... 2 2.0 Michigan 1 (M-1)/Woodward Avenue – Detroit, Michigan ................................................................................................... 4 2.1. Access to Urban/Suburban Areas ......................................................................................................................................... 4 2.2. Corridor Access Control ........................................................................................................................................................... -

Rocket Fiber's Launch Includes Second Stage

20150302-NEWS--0001-NAT-CCI-CD_-- 2/27/2015 5:29 PM Page 1 ® www.crainsdetroit.com Vol. 31, No. 9 MARCH 2 – 8, 2015 $2 a copy; $59 a year ©Entire contents copyright 2015 by Crain Communications Inc. All rights reserved Page 3 ROCKET FIBER:PHASE 1 COVERAGE AREA Panasonic unit plays ‘Taps’ ‘To chase for apps, rethinks strategy According to figures provided by Rocket the animal’ Fiber, the download times for ... “Star Wars” movie on Blu-ray: about seven hours at a typical residential Internet speed of Packard Plant owner eyes bids 10 megabits per second but about 4½ minutes at gigabit speed. for historic downtown buildings An album on iTunes: About one minute on LOOKING BACK: ’80s office residential Internet and less than a second BY KIRK PINHO at gigabit speed boom still rumbles in ’burbs CRAIN’S DETROIT BUSINESS Over breakfast at the Inn on Ferry Street in Lions invite Midtown, Fernando Palazuelo slides salt and fans to pepper shakers across the table like chess pieces. They are a representation of his Detroit take a hike real estate strategy. Yes, he says, he’s getting at new Rocket Fiber’s launch ready to make a series of big moves. The new owner of the 3.5 million-square-foot fantasy football camp Packard Plant on the city’s east side has much broader ambitions for his portfolio in the city, which first took notice of him in 2013 when he Retirement Communities bought the shuttered plant — all 47 buildings, all 40 acres — for a mere $405,000 at a Wayne includes second stage County tax foreclosure auction. -

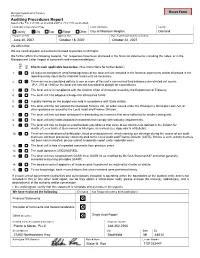

Form 496, Auditing Procedures Report

Michigan Department of Treasury 496 (02/06) Auditing Procedures Report Issued under P.A. 2 of 1968, as amended and P.A. 71 of 1919, as amended. Local Unit of Government Type Local Unit Name County County City Twp Village Other Fiscal Year End Opinion Date Date Audit Report Submitted to State We affirm that: We are certified public accountants licensed to practice in Michigan. We further affirm the following material, “no” responses have been disclosed in the financial statements, including the notes, or in the Management Letter (report of comments and recommendations). Check each applicable box below. (See instructions for further detail.) YES YES NO 1. All required component units/funds/agencies of the local unit are included in the financial statements and/or disclosed in the reporting entity notes to the financial statements as necessary. 2. There are no accumulated deficits in one or more of this unit’s unreserved fund balances/unrestricted net assets (P.A. 275 of 1980) or the local unit has not exceeded its budget for expenditures. 3. The local unit is in compliance with the Uniform Chart of Accounts issued by the Department of Treasury. 4. The local unit has adopted a budget for all required funds. 5. A public hearing on the budget was held in accordance with State statute. 6. The local unit has not violated the Municipal Finance Act, an order issued under the Emergency Municipal Loan Act, or other guidance as issued by the Local Audit and Finance Division. 7. The local unit has not been delinquent in distributing tax revenues that were collected for another taxing unit. -

Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20

Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 1 of 54 Fill in this information to identify the case: United States Bankruptcy Court for the Southern District of Texas Case number (if known): Chapter 11 Check if this is an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor’s name and the case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor’s name Laredo Outlet Shoppes, LLC 2. All other names debtor used N/A in the last 8 years Include any assumed names, trade names, and doing business as names 3. Debtor’s federal Employer Identification Number (EIN) 81-1563566 4. Debtor’s address Principal place of business Mailing address, if different from principal place of business 2030 Hamilton Place Blvd. Number Street Number Street CBL Center, Suite 500 P.O. Box Chattanooga Tennessee 37421 City State ZIP Code City State ZIP Code Location of principal assets, if different from principal place of business Hamilton County County 1600 Water Street Number Street Laredo Texas 78040 City State ZIP Code 5. Debtor’s website (URL) www.cblproperties.com 6. Type of debtor ☒ Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) ☐ Partnership (excluding LLP) ☐ Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy Page 1 WEIL:\97969900\8\32626.0004 Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 2 of 54 Debtor Laredo Outlet Shoppes, LLC Case number (if known) 21-_____ ( ) Name A. -

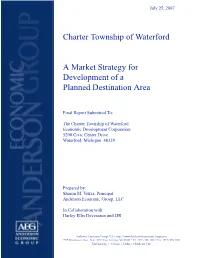

PDA Market Strategy

July 25, 2007 Charter Township of Waterford A Market Strategy for Development of a Planned Destination Area Final Report Submitted To: The Charter Township of Waterford Economic Development Corporation 5200 Civic Center Drive Waterford, Michigan 48329 Prepared by: Sharon M. Vokes, Principal Anderson Economic Group, LLC In Collaboration with: Harley Ellis Devereaux and JJR Anderson Economic Group LLC • http://www.AndersonEconomicGroup.com 1555 Watertower Place, Suite 100 • East Lansing, MI 48823 • Tel: (517) 333-6984 • Fax: (517) 333-7058 East Lansing | Chicago | Dallas | Oklahoma City Waterford Township - Planned Destination Area Final Report Table of Contents 1.0 EXECUTIVE SUMMARY 1 2.0 THE SHOPPING AREA - A BRIEF HISTORY 6 3.0 PROJECT PARAMETERS 10 4.0 A REGIONAL DESTINATION 18 5.0 SPORTS COMPARABLES 22 6.0 MUSIC VENUES 31 7.0 RETAIL ANALYSIS 33 8.0 RETAIL COMPARABLES 36 9.0 RESIDENTIAL ANALYSIS 44 Anderson Economic Group, LLC 0 Waterford Township - Planned Destination Area Final Report 1.0 EXECUTIVE SUMMARY 1.1 Introduction We appreciate this opportunity to contribute to this important project for Waterford Township, and are hopeful that its property owners and other Community Stakeholders are able to share your vision for a mixed-use project that creates a regional destination and refuels economic growth. If this project is planned, designed, implemented and developed carefully, then it has high potential for success, and will enhance the quality of life for your residents, working families and visitors. This document reports our preliminary findings regarding the economic feasibility of redeveloping Waterford Township’s Planned Destination Area (PDA). In short, our findings are favorable for the project, with the following summary of recommenda- tions: 1. -

Michigan-Gateway-Marketplace

New Markets MICHIGAN Tax Credit 50 States NMTC ALLOCATEE National New Markets Fund Los Angeles, CA Steve MacDonald: 310.914.5333 Invest Detroit CDE Detroit, MI Mary King: 313.259-6368 National Community Investment Fund Chicago, IL Saurabh Narain: 312.881.5826 Wayne County – Detroit CDE Detroit, MI Raymond Byers: 313.224.6025 Liberty Financial Services New Orleans, LA Julius Kimbrough: 504.240.5264 Gateway Marketplace COMMUNITY PROFILE When it opens in 2013, the Gateway Marketplace, a new 361,000 square foot . Detroit, MI retail center anchored by a grocery store, will be the first major retail project . 40% poverty rate within the City of Detroit in more than 40 years. The Gateway Marketplace will . Median income 30% of provide healthy food options to the local residents, create hundreds of jobs, and Area Median Income eliminate a Brownfield site. Unemployment 3.2 times the national average This important revitalization project was financed by the Michigan Economic . USDA Food Desert Growth Authority, a loan from the General Retirement System of the City of Detroit, and $57.6 million in critical NMTC financing, provided by National New PROJECT HIGHLIGHTS Markets Fund, Invest Detroit CDE, National Community Investment Fund, Wayne . Construction of retail County-Detroit CDE, and Liberty Financial Services. center Located in a USDA designated food desert and surrounded by severely low- . Total Project Cost: $58.5 income census tracts, the project’s anchor tenant is a 214,000 square foot Meijer million . NMTC: $57.6 million supercenter that will provide affordable groceries to local residents and will be . Investor: U.S.