2017 Forecast

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2012 FINALISTS ICSC Is Proud to Announce the Finalists of the 2012 U.S

2012 FINALISTS ICSC is proud to announce the finalists of the 2012 U.S. MAXI Awards. The U.S. MAXI Awards honor outstanding marketing campaigns from all over the United States. Chosen by a panel of industry professionals, these finalists represent excellence throughout the industry. The 2012 U.S. Maxi Awards will be presented at ICSC’s first-ever NOI + Conference in Orlando, Florida, September 5, 2012. TRADITIONAL MARKETING - ADVERTISING Single Center Pooches Pose at The Brickyard’s PUParazzi! The Brickyard Shopping Center Chicago, Illinois Owner: Retail Properties of America, Inc. Management Company: RPAI US Management, LLC The Gateway provides Daily Dish The Gateway Salt Lake City, Utah Owner: Retail Properties of America, Inc. Management Company: RPAI, Southwest Management Favorite Label Consumer Campaign Natick Mall Natick, Massachusetts Owner/Management Company: General Growth Properties Home for the Holidays Promotional Campaign Southlake Town Square Southlake, Texas Owner: Retail Properties of America Inc Management Company: RPAI Southwest Management LLC Company 2011 Hillsdale’s South End Renovation Bohannon Development Company San Mateo, California MORE Holiday Advertising CBL & Associates Properties, Inc. Chattanooga, Tennessee Joint Center Club Estrellas E-Magazine The Shops at La Cantera and North Star Mall San Antonio, Texas Management Company: General Growth Properties TRADITIONAL MARKETING - BUSINESS-TO-BUSINESS (B2B) Single Center The Writing’s on the Wall West Acres Shopping Center Fargo, North Dakota Owner/Management Company: West Acres Development, LLP Company Think Retail. Create Value. DDR Corp. Beachwood, Ohio Keep The Dollars In Dallas United Commercial Realty Dallas, Texas TRADITIONAL MARKETING - CAUSE RELATED MARKETING Single Center Queen for a Day Aspen Grove Littleton, Colorado Owner/Management Company: DDR Corp. -

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

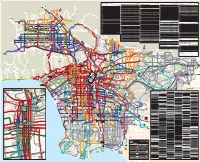

Metro Bus and Metro Rail System

Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Metro Bus Lines East/West Local Service in other areas Weekdays Saturdays Sundays North/South Local Service in other areas Weekdays Saturdays Sundays Limited Stop Service Weekdays Saturdays Sundays Special Service Weekdays Saturdays Sundays Approximate frequency in minutes Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Weekdays Saturdays Sundays 102 Walnut Park-Florence-East Jefferson Bl- 200 Alvarado St 5-8 11 12-30 10 12-30 12 12-30 302 Sunset Bl Limited 6-20—————— 603 Rampart Bl-Hoover St-Allesandro St- Local Service To/From Downtown LA 29-4038-4531-4545454545 10-12123020-303020-3030 Exposition Bl-Coliseum St 201 Silverlake Bl-Atwater-Glendale 40 40 40 60 60a 60 60a 305 Crosstown Bus:UCLA/Westwood- Colorado St Line Route Name Peaks Day Eve Day Eve Day Eve 3045-60————— NEWHALL 105 202 Imperial/Wilmington Station Limited 605 SANTA CLARITA 2 Sunset Bl 3-8 9-10 15-30 12-14 15-30 15-25 20-30 Vernon Av-La Cienega Bl 15-18 18-20 20-60 15 20-60 20 40-60 Willowbrook-Compton-Wilmington 30-60 — 60* — 60* — —60* Grande Vista Av-Boyle Heights- 5 10 15-20 30a 30 30a 30 30a PRINCESSA 4 Santa Monica Bl 7-14 8-14 15-18 12-18 12-15 15-30 15 108 Marina del Rey-Slauson Av-Pico Rivera 4-8 15 18-60 14-17 18-60 15-20 25-60 204 Vermont Av 6-10 10-15 20-30 15-20 15-30 12-15 15-30 312 La Brea -

ORLANDO Vacation Guide & Planning Kit

ORLANDO Vacation Guide & Planning Kit Orlando, Florida Overview Table of Contents Orlando, the undisputed “Vacation Capital of the World,” boasts Orlando, Florida Overview 1 beautiful weather year round, world-class theme parks, thrilling water Getting To And Around Orlando 2 parks, unique attractions, lively dinner theaters, outdoor recreation, Orlando Theme Parks 3 luxurious health spas, fine dining, trendy nightclubs, great shopping Walt Disney World Resort 3 opportunities, championship golf courses and much more. The seat of Universal Orlando® Resort 4 Orange County, Florida, Orlando boasts a population of approximately SeaWorld® Orlando 4 228,000 – making it the sixth largest city in Florida. Easily accessible Orlando Attractions 5 via Interstate 4 and the Florida Turnpike, Orlando is also home to the Orlando Dining 8 Orlando International Airport – the 10th busiest airport in the United Orlando Live Entertainment 8 States and the 20th busiest in the world. Orlando Shopping 9 Orlando Golf 10 Experience the magic of Walt Disney World® Resort – Discover the Orlando Annual Events 11 enchanted lands of Disney’s Magic Kingdom® Park, blast off into the Orlando Travel Tips 13 future at Epcot®, journey through the fascinating history of Hollywood movies at Disney’s Hollywood Studios™ and take a fun-filled safari expedition at Disney’s Animal Kingdom® Theme Park. Don’t miss the thrilling rides at the two amazing theme parks of Universal Orlando® Resort – Universal Studios® Florida and Universal’s Islands of Adventure®, as well as the up-close animal encounters of SeaWorld® Orlando. Cool off at one of Orlando’s state-of-the-art water parks such as Aquatica, Wet ‘n Wild® Water Park, Disney’s Blizzard Beach or Disney’s Typhoon Lagoon. -

2018 EARLY DECEMBER 2018 Text & Photos by Mike Ritto [email protected] Fullerton Photo Quiz NEW in TOWN

OBSERVER 40 TH B-D AY page 20 COMMUNITY Fullerton bsCeALErNDAvR Peage 1r 3-15 O EAR FULLERTON’S ONLY INDEPENDENT NEWS • Est.1978 (printed on 20% recycled paper) • Y 40 #20 • EARLY DECEMBER 2018 Submissions: [email protected] • Contact: (714) 525-6402 • Read Online at : www.fullertonobserver.com Vinny De La Torre Honored by Fullerton and France by Ed Paul The City of Fullerton proudly recognized long-time resident, Ventura “Vinny” De La Torre, for his heroic service to his country over 70 years ago. The presentation was made at the November 19 Council meeting and Vinny was given a standing ovation by all present. Vinny De La Torre was also recognized by receiving France’s Legion of Honor, the coun - try’s highest honor, on November 11, 2018, in recognition for his service with Gen. George Patton’s Third Army during WWII. Vinny was in more than 200 days of contin - uous combat, liberating many French cities and in 1945, was part of the division that fought at the Battle of the Bulge and liberated two concentration camps, Buchenwald and Ebensee. He was almost 21 years old at that time. Like many of the WW II generation, Vinny kept much of this story to himself. But in recent years his family, mostly his grandchil - dren, slowly obtained bits and pieces of his service. They conducted some research and provided it to the French Consulate General who, after reviewing it for over a year, made the presentation to Vinny on November 11 at the National Cemetery in West Los Angeles. -

Chapter 11 Case No. 21-10632 (MBK)

Case 21-10632-MBK Doc 249 Filed 04/06/21 Entered 04/06/21 16:21:35 Desc Main Document Page 1 of 92 UNITED STATES BANKRUPTCY COURT DISTRICT OF NEW JERSEY In re: Chapter 11 L’OCCITANE, INC., Case No. 21-10632 (MBK) Debtor. Judge: Hon. Michael B. Kaplan CERTIFICATE OF SERVICE I, Ana M. Galvan, depose and say that I am employed by Stretto, the claims and noticing agent for the Debtors in the above-captioned case. On April 2, 2021, at my direction and under my supervision, employees of Stretto caused the following documents to be served via first-class mail on the service list attached hereto as Exhibit A, and via electronic mail on the service list attached hereto as Exhibit B: Notice of Deadline for Filing Proofs of Claim Against the Debtor L’Occitane, Inc. (attached hereto as Exhibit C) [Customized] Official Form 410 Proof of Claim (attached hereto as Exhibit D) Official Form 410 Instructions for Proof of Claim (attached hereto as Exhibit E) Dated: April 6, 2021 /s/ Ana M. Galvan Ana M. Galvan STRETTO 410 Exchange, Suite 100 Irvine, CA 92602 Telephone: 855-434-5886 Email: [email protected] Case 21-10632-MBK Doc 249 Filed 04/06/21 Entered 04/06/21 16:21:35 Desc Main Document Page 2 of 92 Exhibit A Case 21-10632-MBK Doc 249 Filed 04/06/21 Entered 04/06/21 16:21:35 Desc Main Document Page 3 of 92 Exhibit A Served via First-Class Mail Name Attention Address 1 Address 2 Address 3 City State Zip Country 1046 Madison Ave LLC c/o HMH Realty Co., Inc., Rexton Realty Co. -

State Storeno Mall Name Store Type 2015 Sales 2014 Sales Variance

Variance State StoreNo Mall Name Store Type 2015 Sales 2014 Sales Inc/(Dec) % Inc/(Dec) TX 83 NorthPark Center In-Line 1,472,766.00 1,363,984.00 108,782.00 7.98% SC 135 Coastal Grand Mall In-Line 1,151,631.67 1,113,877.31 37,754.36 3.39% TX 20 Barton Creek Square Shopping Center In-Line 1,096,658.41 1,083,499.33 13,159.08 1.21% CA 8 Westfield Valencia Town Center In-Line 1,071,022.26 1,087,795.83 (16,773.57) -1.54% TX 19 Baybrook Mall In-Line 1,025,120.43 1,055,953.79 (30,833.36) -2.92% AZ 125 Park Place Mall In-Line 950,664.23 946,527.12 4,137.11 0.44% TN 48 Wolfchase Galleria In-Line 923,588.32 867,012.22 56,576.10 6.53% TX 55 Stonebriar Centre In-Line 876,800.55 815,558.37 61,242.18 7.51% CA 126 Westfield Galleria at Roseville In-Line 869,168.30 754,757.11 114,411.19 15.16% CO 167 Cherry Creek Shopping Center In-Line 868,959.85 835,887.13 33,072.72 3.96% CO 61 Park Meadows Center In-Line 831,157.07 800,397.91 30,759.16 3.84% AZ 28 Arrowhead Towne Center In-Line 771,406.64 656,746.72 114,659.92 17.46% CA 39 Westfield University Towne Center In-Line 738,949.33 573,464.00 165,485.33 28.86% CA 35 The Promenade at Temecula In-Line 733,268.27 666,557.65 66,710.62 10.01% KY 78 Mall St. -

Desert Fashion Plaza Property Condition Report and Phase I Environmental Assessment

.,.,. .r.-· ~ Building Diagnostics, Ltd. DESERT FASHION PLAZA PROPERTY CONDITION REPORT AND PHASE I ENVIRONMENTAL ASSESSMENT t'7;38 Elton Road Sbite 318 Silver Spring, MD 20903 The Property Condition Report & BDL Phase I Environmental Site Assessment for: . I Property Name DESERT FASHION PLAZA~ Property Address 123 North Canyon Drive Palm Springs, California 92262 Report Number 8-o1-o1o 11 Prepared for EXCEL LEGACY CORPORATION, its successors and/or assigns Gateway Tower, 563 West 500 South Suite 440 Woods Cross, Utah 84087 Prepared by BUILDING DIAGNOSTICS, L TO 1738 Elton Road, Suite 318 Silver Spring, Maryland 20903 301 408 2552 Evaluation Date · . January 19, 1998\\ Report Date January 23, 1998\\ .. Table of Contents Section Page Topic .I EXECUTIVE SUMMARY 1 #3 • Rapid Review .....I I .. I 2 #9 • Scope of Work I SITE OVERVIEW I 3 #16 • Subject Property Description I j PROPERTY CONDITION REPORT I 4 #19 • Site and Common Elements I I 5 #24 • Architectural I 6 #28 • Mechanical and Electrical Systems 7 #34 • Photographs I 8 #40 • Americans with Disabilities Act I I PHASE I ENVIRONMENTAL SITE ASSESSMENT I 9 #41 • Site Reconnaissance I 10 #54 • Records and Database Review I 11 #79 • Information Sources 12 #80 • Appendixes I © 1998 Building Diagnostics, Ltd. 2 Desert Fashion Plaza Executive Summary ' 8-01,D10. 1/19198 Rapid Review I SECTION 1 RAPID REVIEW~ SUMMARY II These charts present a summary only. Please refer to the I pages listed for comprehensive information about each _ item listed. b=================~ CONDmON The designations "good", "fair", and "poor'' are defined as DESIGNA110N follows: "Good" means that the item is in average or better condition for its age, use and location of the property. -

Marge Me.” Her Father Ran a Grocery Store and Her Mother Taught Piano Lessons

LOS CERRITOS Serving Artesia, Bellflower, Cerritos, Commerce, Downey, Hawaiian Gardens, Lakewood, Norwalk, and Pico Rivera • 86,000 Homes Every Friday •See July 8, 2016 page • Vol 31, No. 1614 A Hews Media Group-Community News Investigation Commerce Councilman Argumedo's 2010 Conviction Was Missing Crucial Evidence By Brian Hews HMG-CN. But in reality the contents of the entered a “Minute Order” stating, “the Argumedo was charged with a felony Declaration were public record. case is settled.” On the same day, Judge Hews Media Group-Community News and subsequently plead guilty to one On September 7, 2005, Leal filed a Richey recorded, “it appears that the case has obtained information that strongly misdemeanor count of obstruction of civil action against the City of Commerce has settled pending Council approval on indicates the 2010 perjury case against justice, was forced to resign his council to recover legal fees for March, April and September 22, 2006.” current Commerce Councilman Hugo seat, and was prohibited from running for May of 2005 in the amount of $125,626. Court records indicate that then- Argumedo, prosecuted by the Los Angeles office for three years. On January 6, 2006, the City of Commerce Commerce Mayor Nancy Ramos, current District Attorney’s office under Steve The case against Argumedo, who signed filed a cross-complaint. Commerce City Attorney Eduardo Olivo, Cooley, was missing critical evidence that a Declaration letter in favor of Francisco The case languished for over a year and Leal attended the meeting. likely would have resulted in a dismissal in Leal’s lawsuit against Commerce in 2005, when, on September 19, 2006, judge Leal, Olivo, and Ramos all agreed on favor of Argumedo. -

350-420 Palm Canyon

FOR SALE | PRIME DOWNTOWN PALM SPRINGS ASSEMBLAGE 350-420 PA L M C A N Y O N PALM SPRINGS, CA 188,179 SF (4.32 ACRES) DEVELOPMENT SITE +/- 1,300 FEET OF FRONTAGE ON PALM CANYON AND INDIAN DRIVES SOUTH BELERADO ROAD SOUTH PALM CANYON DRIVE WEST RAMON ROAD SOUTH INDIAN CANYON DRIVE TIMOTHY L BOWER MARCO ROSSETTI GABRIELLE LARDIERE Senior Vice President Senior Associate +1 310 550 2605 +1 310 550 2521 +1 760 578 4723 [email protected] [email protected] [email protected] Lic. 01911073 Lic. 00864693 Lic. 01805951 CAPITAL MARKETS TABLE OF CONTENTS EXECUTIVE SUMMARY Investment Summary Investment Highlights AERIAL OVERVIEW THE PROPERTY Current Improvements Site Plan MARKET OVERVIEW Regional Overview | Coachella Valley Submarket Overview | City of Palm Springs APPENDIX Zoning Code Palm Springs, CA WEST ARENAS ROAD SITE SOUTH BELERADO ROAD SOUTH PALM CANYON DRIVE SOUTH INDIAN CANYON DRIVE WEST RAMON ROAD N EXECUTIVE SUMMARY Investment Summary Investment Highlights EXECUTIVE SUMMARY INVESTMENT SUMMARY CBRE has been retained on an exclusive basis to present the opportunity to acquire an unequaled investment/mixed-use development site at the Southern Gateway to Palm Springs’ resurgent Downtown commercial core. The site currently consists of 4 parcels of land totaling approximately 188,500 square feet (4.32 acres) with 1,300 feet of combined frontage along Palm Canyon and Indian Drives. This prime site has potential for retail, office and residential development, and boasts spectacular street front visibility as well as mountain and Coachella Valley views. The site offers interim cash flow to an investor, with retail tenants such as Rite Aid and BBVA Compass Bank. -

Chapter 11 CORINTHIAN COLLEGES, INC., Et Al. Case

Case 15-10952-KJC Doc 712 Filed 08/05/15 Page 1 of 2014 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE In re: Chapter 11 CORINTHIAN COLLEGES, INC., et al.1 Case No. 15-10952-CSS Debtor. AFFIDAVIT OF SERVICE STATE OF CALIFORNIA } } ss.: COUNTY OF LOS ANGELES } SCOTT M. EWING, being duly sworn, deposes and says: 1. I am employed by Rust Consulting/Omni Bankruptcy, located at 5955 DeSoto Avenue, Suite 100, Woodland Hills, CA 91367. I am over the age of eighteen years and am not a party to the above-captioned action. 2. On July 30, 2015, I caused to be served the: a) Notice of (I) Deadline for Casting Votes to Accept or Reject the Debtors’ Plan of Liquidation, (II) The Hearing to Consider Confirmation of the Combined Plan and Disclosure Statement and (III) Certain Related Matters, (the “Confirmation Hearing Notice”), b) Debtors’ Second Amended and Modified Combined Disclosure Statement and Chapter 11 Plan of Liquidation, (the “Combined Disclosure Statement/Plan”), c) Class 1 Ballot for Accepting or Rejecting Debtors’ Chapter 11 Plan of Liquidation, (the “Class 1 Ballot”), d) Class 4 Ballot for Accepting or Rejecting Debtors’ Chapter 11 Plan of Liquidation, (the “Class 4 Ballot”), e) Class 5 Ballot for Accepting or Rejecting Debtors’ Chapter 11 Plan of Liquidation, (the “Class 5 Ballot”), f) Class 4 Letter from Brown Rudnick LLP, (the “Class 4 Letter”), ____________________________________________________________________________________________________________________________________________________________________________________________________________ 1 The Debtors in these cases, along with the last four digits of each Debtor’s federal tax identification number, are: Corinthian Colleges, Inc. -

Brookfield Properties' Retail Group Overview

Retail Overview Brookfield Properties’ Retail Group Overview We are Great Gathering Places. We embrace our cultural core values of Humility, Attitude, Do The Right Thing, H Together and Own It. HUMILITY Brookfield Properties’ retail group is a company focused A ATTITUDE exclusively on managing, leasing, and redeveloping high- quality retail properties throughout the United States. D DO THE RIGHT THING T TOGETHER O HEADQUARTERS CHICAGO OWN IT RETAIL PROPERTIES 160+ STATES 42 INLINE & FREESTANDING GLA 68 MILLION SQ FT TOTAL RETAIL GLA 145 MILLION SQ FT PROFORMA EQUITY MARKET CAP $20 BILLION PROFORMA ENTERPRISE VALUE $40 BILLION Portfolio Map 2 7 1 4 3 5 3 6 2 1 2 1 1 2 1 3 3 3 1 1 2 4 1 2 1 3 2 1 1 10 4 2 5 1 4 10 2 3 3 1 48 91 6 5 6 2 7 6 4 5 11 7 4 1 1 1 2 2 2 5 7 1 2 1 2 1 1 1 1 6 1 3 5 3 4 15 19 2 14 11 1 1 3 2 1 2 1 1 3 6 2 1 3 4 18 2 17 3 1 2 1 3 2 2 5 3 6 8 2 1 12 9 7 5 1 4 3 1 2 1 2 16 3 4 13 3 1 2 6 1 7 9 1 10 5 4 2 1 4 6 11 5 3 6 2 Portfolio Properties 1 2 3 3 3 1 7 4 Offices 13 12 2 Atlanta, GA 7 3 1 1 Chicago, IL Baltimore, MD 8 5 2 Dallas, TX 4 Los Angeles, CA 6 New York, NY 8 2 9 5 Property Listings by State ALABAMA 7 The Oaks Mall • Gainesville 3 The Mall in Columbia • Columbia (Baltimore) 9 Brookfield Place • Manhattan WASHINGTON 8 Pembroke Lakes Mall • Pembroke Pines 4 Mondawmin Mall • Baltimore 10 Manhattan West • Manhattan 1 Riverchase Galleria • Hoover (Birmingham) 1 Alderwood • Lynnwood (Seattle) 5 Towson Town Center • Towson (Baltimore) 11 Staten Island Mall • Staten Island 2 The Shoppes at Bel Air • Mobile (Fort Lauderdale)