PHILIPPINE L STITUTE for DEVELOPMENT STUDIES Working Paper 83-01

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Company Registration and Monitoring Department

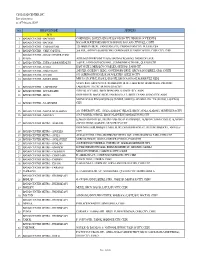

Republic of the Philippines Department of Finance Securities and Exchange Commission SEC Building, EDSA, Greenhills, Mandaluyong City Company Registration and Monitoring Department LIST OF CORPORATIONS WITH APPROVED PETITIONS TO SET ASIDE THEIR ORDER OF REVOCATION SEC REG. HANDLING NAME OF CORPORATION DATE APPROVED NUMBER OFFICE/ DEPT. A199809227 1128 FOUNDATION, INC. 1/27/2006 CRMD A199801425 1128 HOLDING CORPORATION 2/17/2006 CRMD 3991 144. XAVIER HIGH SCHOOL INC. 2/27/2009 CRMD 12664 18 KARAT, INC. 11/24/2005 CRMD A199906009 1949 REALTY CORPORATION 3/30/2011 CRMD 153981 1ST AM REALTY AND DEVLOPMENT CORPORATION 5/27/2014 CRMD 98097 20th Century Realty Devt. Corp. 3/11/2008 OGC A199608449 21st CENTURY ENTERTAINMENT, INC. 4/30/2004 CRMD 178184 22ND CENTURY DEVELOPMENT CORPORATION 7/5/2011 CRMD 141495 3-J DEVELOPMENT CORPORATION 2/3/2014 CRMD A200205913 3-J PLASTICWORLD & DEVELOPMENT CORP. 3/13/2014 CRMD 143119 3-WAY CARGO TRANSPORT INC. 3/18/2005 CRMD 121057 4BS-LATERAL IRRIGATORS ASSN. INC. 11/26/2004 CRMD 6TH MILITARY DISTRICT WORLD WAR II VETERANS ENO9300191 8/16/2004 CRMD (PANAY) ASSOCIATION, INC. 106859 7-R REALTY INC. 12/12/2005 CRMD A199601742 8-A FOOD INDUSTRY CORP. 9/23/2005 CRMD 40082 A & A REALTY DEVELOPMENT ENTERPRISES, INC. 5/31/2005 CRMD 64877 A & S INVESTMENT CORPORATION 3/7/2014 CRMD A FOUNDATION FOR GROWTH, ORGANIZATIONAL 122511 9/30/2009 CRMD UPLIFTMENT OF PEOPLE, INC. (GROUP) GN95000117 A HOUSE OF PRAYER FOR ALL NATIONS, INC. CRMD AS095002507 A&M DAWN CORPORATION 1/19/2010 CRMD A. RANILE SONS REALTY DEVELOPMENT 10/19/2010 CRMD A.A. -

2015Suspension 2008Registere

LIST OF SEC REGISTERED CORPORATIONS FY 2008 WHICH FAILED TO SUBMIT FS AND GIS FOR PERIOD 2009 TO 2013 Date SEC Number Company Name Registered 1 CN200808877 "CASTLESPRING ELDERLY & SENIOR CITIZEN ASSOCIATION (CESCA)," INC. 06/11/2008 2 CS200719335 "GO" GENERICS SUPERDRUG INC. 01/30/2008 3 CS200802980 "JUST US" INDUSTRIAL & CONSTRUCTION SERVICES INC. 02/28/2008 4 CN200812088 "KABAGANG" NI DOC LOUIE CHUA INC. 08/05/2008 5 CN200803880 #1-PROBINSYANG MAUNLAD SANDIGAN NG BAYAN (#1-PRO-MASA NG 03/12/2008 6 CN200831927 (CEAG) CARCAR EMERGENCY ASSISTANCE GROUP RESCUE UNIT, INC. 12/10/2008 CN200830435 (D'EXTRA TOURS) DO EXCEL XENOS TEAM RIDERS ASSOCIATION AND TRACK 11/11/2008 7 OVER UNITED ROADS OR SEAS INC. 8 CN200804630 (MAZBDA) MARAGONDONZAPOTE BUS DRIVERS ASSN. INC. 03/28/2008 9 CN200813013 *CASTULE URBAN POOR ASSOCIATION INC. 08/28/2008 10 CS200830445 1 MORE ENTERTAINMENT INC. 11/12/2008 11 CN200811216 1 TULONG AT AGAPAY SA KABATAAN INC. 07/17/2008 12 CN200815933 1004 SHALOM METHODIST CHURCH, INC. 10/10/2008 13 CS200804199 1129 GOLDEN BRIDGE INTL INC. 03/19/2008 14 CS200809641 12-STAR REALTY DEVELOPMENT CORP. 06/24/2008 15 CS200828395 138 YE SEN FA INC. 07/07/2008 16 CN200801915 13TH CLUB OF ANTIPOLO INC. 02/11/2008 17 CS200818390 1415 GROUP, INC. 11/25/2008 18 CN200805092 15 LUCKY STARS OFW ASSOCIATION INC. 04/04/2008 19 CS200807505 153 METALS & MINING CORP. 05/19/2008 20 CS200828236 168 CREDIT CORPORATION 06/05/2008 21 CS200812630 168 MEGASAVE TRADING CORP. 08/14/2008 22 CS200819056 168 TAXI CORP. -

Transforming Philippine Agriculture During Covid-19 and Beyond

Transforming Philippine Agriculture Public Disclosure Authorized During Covid-19 and Beyond JUNE 2020 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Transforming Philippine Agriculture During Covid-19 and Beyond JUNE 2020 Standard Disclaimer This report is a product of the staff of the International Bank for Reconstruction and Development/The World Bank. The findings, interpretations, and conclusions expressed in this report do not necessarily reflect the views of the Executive Directors of The World Bank or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. Photo credit: Cover page: by Scott Sporleder for TAO Philippines, Organic farm in Palawan Chapter pages: Department of Agriculture, Philippine Rural Development Project 1 Acknowledgments This report was produced by a team from the World Bank Group, led by Eli Weiss and co-led by Anuja Kar, and comprising John Nash, Steven Jaffee, Roehl Briones, Carolina Figueroa-Geron, and Paula Beatrice Macandog. Additional inputs were received from Joop Stoutjesdijk, Maria Theresa Quinones, Roberto Martin N. Galang, and Victor Dato. The assessment related to agricultural extension was prepared by a team from the Food and Agriculture Organization (FAO) of the United Nations, led by John Preissing and comprising Jim Hancock, Katarzyna Pankowska, and Alberto Tordesillas Torres. Kathryn Swartz and Kelly Cassaday edited, and Herbert Navasca formatted the report. -

Palengke, Pamilya, Pamayanan

Palengke, Pamilya, Pamayanan 2017 Annual Report CONTENTS IFC Contents / About the Cover 01 Vision & Mission 03 About the Corporation 05 Secretary’s Message 06 Message from the Chairman 07 Operational Highlights 14 Environmental Report Social Report 15 Stakeholder Engagements 16 Commission on Audit 17 Statement of Managements Responsibility for financial Statements 18 Statements of Financial Positions 19 Statements of Comprehensive Income 20 Statements of Changes in Equity 21 Statements of Cash Flows 22 Notes to Financial Statements 40 Board of Directors 44 Management Committee 45 Key Officers VISION 48 Directory of Offices By 2022, we envision Small Business Corporation as the best managed non-bank GOCC for MSME 50 Annual Report Committee development finance. Mission Grow the MSME sector by: • Developing and implementing financing and capacity building support programs for underserved enterprises and for grassroots MSME organizations; and • Advocating for measures and policies that will promote a stronger MSME finance industry. Small Business Corporation 2017 Annual Report 01 ABOUT THE CORPORATION The Small Business Corporation SB Corp is a government corporation created on January 24, 1991 by virtue of Section 11 of RA No. 6977, amended on May 6, 1997 by RA 8289, otherwise known as the Magna Carta for Small and Medium Enterprises. SBGFC is under the policy program and administrative supervision of the Small and Medium Enterprise Development (SMED) Council of the Department of Trade and Industry (DTI), the primary agency responsible for small and medium enterprises in the country. On May 23, 2008, RA 9501 or “An Act to Promote Entrepreneurship by Strengthening Development and Assistance Programs for Micro, Small and Medium Scale Enterprises was signed into law amending for the purpose RA 8289. -

List of Ecpay Cash-In Or Loading Outlets and Branches

LIST OF ECPAY CASH-IN OR LOADING OUTLETS AND BRANCHES # Account Name Branch Name Branch Address 1 ECPAY-IBM PLAZA ECPAY- IBM PLAZA 11TH FLOOR IBM PLAZA EASTWOOD QC 2 TRAVELTIME TRAVEL & TOURS TRAVELTIME #812 EMERALD TOWER JP RIZAL COR. P.TUAZON PROJECT 4 QC 3 ABONIFACIO BUSINESS CENTER A Bonifacio Stopover LOT 1-BLK 61 A. BONIFACIO AVENUE AFP OFFICERS VILLAGE PHASE4, FORT BONIFACIO TAGUIG 4 TIWALA SA PADALA TSP_HEAD OFFICE 170 SALCEDO ST. LEGASPI VILLAGE MAKATI 5 TIWALA SA PADALA TSP_BF HOMES 43 PRESIDENTS AVE. BF HOMES, PARANAQUE CITY 6 TIWALA SA PADALA TSP_BETTER LIVING 82 BETTERLIVING SUBD.PARANAQUE CITY 7 TIWALA SA PADALA TSP_COUNTRYSIDE 19 COUNTRYSIDE AVE., STA. LUCIA PASIG CITY 8 TIWALA SA PADALA TSP_GUADALUPE NUEVO TANHOCK BUILDING COR. EDSA GUADALUPE MAKATI CITY 9 TIWALA SA PADALA TSP_HERRAN 111 P. GIL STREET, PACO MANILA 10 TIWALA SA PADALA TSP_JUNCTION STAR VALLEY PLAZA MALL JUNCTION, CAINTA RIZAL 11 TIWALA SA PADALA TSP_RETIRO 27 N.S. AMORANTO ST. RETIRO QUEZON CITY 12 TIWALA SA PADALA TSP_SUMULONG 24 SUMULONG HI-WAY, STO. NINO MARIKINA CITY 13 TIWALA SA PADALA TSP 10TH 245- B 1TH AVE. BRGY.6 ZONE 6, CALOOCAN CITY 14 TIWALA SA PADALA TSP B. BARRIO 35 MALOLOS AVE, B. BARRIO CALOOCAN CITY 15 TIWALA SA PADALA TSP BUSTILLOS TIWALA SA PADALA L2522- 28 ROAD 216, EARNSHAW BUSTILLOS MANILA 16 TIWALA SA PADALA TSP CALOOCAN 43 A. MABINI ST. CALOOCAN CITY 17 TIWALA SA PADALA TSP CONCEPCION 19 BAYAN-BAYANAN AVE. CONCEPCION, MARIKINA CITY 18 TIWALA SA PADALA TSP JP RIZAL 529 OLYMPIA ST. JP RIZAL QUEZON CITY 19 TIWALA SA PADALA TSP LALOMA 67 CALAVITE ST. -

Lesson 03 Culture Notes.Indd

LESSON 3 Mga Talang Pangkultura: Sa Palengke At the Public Market Have you ever gone shopping at a public market in the Philippines? What was your experience like? On October 13, 2010, a news item in the Philippine Daily Inquirer announced that the vendors of the Langaray Public Market have banned plastic bags and instead started distributing woven bags called bayong to their customers. I still have memories of the bayong from childhood—you went to the palengke, you brought your own bayong. Traditionally, before plastic bags and supermarkets became popular, shoppers went to the market daily (and later, once or twice a week) to buy fresh fish, meat, poultry, vegetable, and fruits. There were also areas when one could buy household items, dresses, even school supplies, and for those who get hungry, small eating places. Vendors rented stalls, and allowed haggling. The palengke, sometimes called the talipapa, is translated into “market,” but perhaps more appropriately, should be called a “wet market,” and it is called “wet” because vendors (especially fish and seafood vendors) are constantly cleaning their stalls, making the ground wet. People go shopping (in Tagalog/Filipino called pamamalengke) in the morning or in late afternoon and the market is usually quiet from noon until around 4 or 5 pm. Produce is sold not just by the kilo, but also through other means of counting items and weight, such as: tumpok (pile), for example, a tumpok of chili peppers; salop (or a ganta, which measures volume, but is roughly equivalent to a kilo), such as a salop of rice; tali (literally, something used for tying things together) or bundle, such as isang taling kangkong (a bundle of swamp cabbage), and por piraso (per piece), for example, isang pirasong luya or a piece of ginger. -

CIS BAYAD CENTER, INC. List of Partners As of February 2020*

CIS BAYAD CENTER, INC. List of partners as of February 2020* NO. BRANCH NAME ADDRESS BCO 1 BAYAD CENTER - BACOLOD COKIN BLDG. LOPEZ JAENA ST.,BACOLOD CITY, NEGROS OCCIDENTAL 2 BAYAD CENTER - BACOOR BACOOR BOULEVARD, BRGY. BAYANAN, BACOOR CITY HALL, CAVITE 3 BAYAD CENTER - CABANATUAN 720 MARILYN BLDG., SANGITAN ESTE, CABANATUAN CITY, NUEVA ECIJA 4 BAYAD CENTER - CEBU CAPITOL 2nd FLR., AVON PLAZA BUILDING, OSMENA BOULEVARD CAPITOL. CEBU CITY, CEBU BAYAD CENTER - DAVAO CENTER POINT 5 PLAZA ATRIUM CENTERPOINT PLAZA, MATINA CROSSING, DAVAO DEL SUR 6 BAYAD CENTER - EVER COMMONWEALTH 2ndFLR., EVER GOTESCO MALL, COMMONWEALTH AVE., QUEZON CITY 7 BAYAD CENTER - GATE2 EAST GATE 2, MERALCO COMPLEX, ORTIGAS, PASIG CITY 8 BAYAD CENTER - GMA CAVITE 2ND FLR. GGHHNC 1 BLDG., GOVERNORS DRVE, BRGY SAN GABRIEL, GMA, CAVITE 9 BAYAD CENTER - GULOD 873 QUIRINO HWAY,GULOD,NOVALICHES, QUEZON CITY 10 BAYAD CENTER - KASIGLAHAN MWCI.SAT.OFFICE, KASIGLAHAN VIL.,BRGY.SAN JOSE,RODRIGUEZ, RIZAL SPACE R-O5 GROUND FLR. REMBRANDT BLDG. LAKEFRONT BOARDWALK, PRESIDIO 11 BAYAD CENTER - LAKEFRONT LAKEFRONT, SUCAT, MUNTINLUPA CITY 12 BAYAD CENTER - LCC LEGAZPI 4TH FLR. LCC MALL, BRGY.DINAGAAN, LEGASPI CITY, ALBAY 13 BAYAD CENTER - LIGAO GROUND FLR. MA-VIC BLDG, SAN ROQUE ST., BRGY. DUNAO, LIGAO CITY, ALBAY MAYNILAD LAS PIÑAS BUSINESS CENTER, MARCOS ALVAREZ AVE. TALON UNO, LAS PIÑAS 14 BAYAD CENTER - M. ALVAREZ CITY 15 BAYAD CENTER - MAYNILAD ALABANG 201 UNIVERSITY AVE., AYALA ALABANG VILLAGE, BRGY. AYALA ALABANG, MUNTINLUPA CITY 16 BAYAD CENTER - MAYSILO 479-F MAYSILO CIRCLE, BRGY. PLAINVIEW, MANDALUYONG CITY LOWER GROUND FLR., METRO GAISANO SUPERMARKET, ALABANG TOWN CENTER, ALABANG- 17 BAYAD CENTER METRO - ALABANG ZAPOTE ROAD, ALABANG, MUNTINLUPA CITY GROUND FLOOR,MARQUEE MALL BLDG, DON BONIFACIO ST., PULUNG MARAGUL, ANGELES 18 BAYAD CENTER METRO - ANGELES CITY 19 BAYAD CENTER METRO - AYALA AYALA CENTER, CEBU ARCHBISHOP REYES AVE., CEBU BUSINESS PARK, CEBU CITY 20 BAYAD CENTER METRO - AYALA FELIZ MARCOS HI-WAY, LIGAYA, CORNER JP RIZAL, PASIG CITY 21 BAYAD CENTER METRO - BANILAD A.S FORTUNA CORNER H. -

![[Date] Documentation of LGU Good Practices Against COVID-19](https://docslib.b-cdn.net/cover/3294/date-documentation-of-lgu-good-practices-against-covid-19-4153294.webp)

[Date] Documentation of LGU Good Practices Against COVID-19

[Company name] [Document title] [Document subtitle] Anna Documentation of LGU Good Practices Against COVID-19 [Date] NCR • Comprehensive Support Services for Local Frontliners, Pasig City • Mobile Palengke, Pasig City • Go Manila! Mobile App: Shifting to E-Payment to Flatten the Covid-19 Curve, Manila City • Using Monitoring Information System to #Beatcovid-19, Makati City • Localized Targeted Mass Testing, Valenzuela City • Provision of Healthy and Nutritious Food Packs to Fight COVID-19, Mandaluyong City • Mobile Botika, Libreng Gamot: Ensuring Access to Medicines, Caloocan City • Marikina Molecular Diagnostics Laboratory, Marikina City • Telemedicine: Project that Promotes Health and Wellness of Locals in Accordance with Strict Social Distancing Protocol Amid COVID-19 Crisis, Taguig City CAR • Revitalizing the Spirit of 'Baddangan’: A Community Response to COVID Crisis, Ifugao • Villagers in Mt. Province Pursue Survival Gardening with Chicken Amidst COVID-19 Pandemic, Mt. Province • Monitoring of Movement in Mountain Province, Mt. Province • Weekly Disinfection of Barangays in Baguio City, Baguio City Region I • Stay-at-Home Challenge, Pinili, Ilocos Norte • Banna-nihan sa ECQ: Empowering Civil Society Organizations, Banna, Ilocos Norte • Quirino Response Team (QRT) in Action, Quirino, Ilocos Sur • Kalinga para sa Kumakalinga, San Fernando City, La Union Region II • Cagayan Valley Rice Farmers Post Higher Earnings, Cagayan Valley • CAMP Learning Workshop Conducted for DOLE RO2 Employees, Tuguegarao City, Cagayan • Bespren sa Agrikultura, -

Fish for the City: Urban Political Ecologies of Laguna Lake

FISH FOR THE CITY: URBAN POLITICAL ECOLOGIES OF LAGUNA LAKE AQUACULTURE A Dissertation by KRISTIAN KARLO CORDOVA SAGUIN Submitted to the Office of Graduate and Professional Studies of Texas A&M University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY Chair of Committee, Christian Brannstrom Committee Members, Norbert Dannhaeuser Wendy Jepson Kathleen O’Reilly Head of Department, Vatche Tchakerian December 2013 Major Subject: Geography Copyright 2013 Kristian Karlo Cordova Saguin ABSTRACT The dissertation tells the story of the production of socionatures through the development of aquaculture in Laguna Lake. The state introduced lake aquaculture to supplement fisherfolk livelihoods and improve fish production in part to provide nearby Metro Manila with its fish requirements. Half a century of aquaculture in the lake, however, has transformed ecologies, landscapes and livelihoods. Flows of fish to the city encounter socioecological contradictions in lake production and urban consumption. This dissertation examines these transformations and how state policies, livelihood activities and fish demands produce particular socionatures. Using the urban political ecology concept of urban metabolism, the dissertation frames the production of Laguna Lake socionatures as a city-lake dynamic. It employs qualitative and multi-sited ethnographic methods to follow Laguna Lake fish from sites of production to consumption and to identify actors, relations and practices that shape access to these flows of fish. The state embarked on projects aided by scientific institutions and foreign donors to enable aquaculture production through simplification of complex lake socioecological processes. These resulted in capitalist fishpen aquaculture expansion that transformed lake ecologies and village livelihoods. Capitalist aquaculture continues to confront nature’s materiality in water-based production, which provides constraints and opportunities for aquaculture expansion. -

Legal Documents

COVER SHEET 0 0 0 0 1 0 8 4 7 6 S.E.C Registration Number P H I L I P P I N E S E V E N C O R P O R A T I O N (Company’s full Name) 7 t h F l r . T h e C o l u m b i a T o w e r O r t i g a s A v e. M a n d a l u y o n g C i t y (Business Address: No. Street City / Town / Province) 724-44-41 to 51 Atty. Evelyn S. Enriquez Corporate Secretary Company Telephone Number Contact Person 1 2 3 1 1 7 . A 0 7 3rd Thursday Month Day FORM TYPE Month Day Fiscal Year Annual Meeting ANNUAL REPORT Secondary License Type, if Applicable Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign -------------------------------------------------------------------------------------------------------------------------------- ---------- To be accomplished by SEC personnel concerned File Number LCU Document I.D. Cashier STAMPS Remarks = pls. use black ink for scanning purposes 1 3 (b) Has been subject to such filing requirements for the past 90 days. Yes X No 13. The aggregate market value of the voting stock held by non- affiliates of the registrant. The aggregate market value of 147,021,978 share of common stock is Php 14,481,664,833.00 based on the bid price of P98.50 per share as of December 27, 2013, the last transaction date for the year under review. -

Slum-Fit? Or, Where Is the Place of the Filipinx Urban Poor in the Philippine City?

Slum-fit? Or, Where is the Place of the Filipinx Urban Poor in the Philippine City? Kaloy M. Cunanan Independent Researcher Philippines [email protected] Abstract Against place-based stigma and neoliberal-localism, this paper asks, where in city models does the Philippine slum fit? In doing so, this paper explores two city models: industrial and postcolonial city. But in both city models, there is undervaluation of the Philippine slum. For this reason, this paper suggests the comprador city as an appraisal and alternative to the industrial and postcolonial city models. The comprador city highlights the oppositional interest in the city. These are between the compradors and the urban poor. The former dominates and reconfigures the Philippine city and nation through its foreign ties. While many of the latter lives in the slums despite they are the labor that creates and develops the city. Keywords comprador; postcolonial; industrial; slum; city model Published with Creative Commons licence: Attribution–Noncommercial–No Derivatives Slum-fit? 36 Iskuwater of the Philippines? Slums1 are the most visible expression of the polarization of wealth and power in the city (Lieberherr-Gardiol, 2006, 276; UN-HABITAT, 2003b). Despite the slum dwellers’ contribution to the city and nation (Alcazaren et. al., 2011; Berner, 1997; M. Davis, 2006; R. Simbulan, 1998; Tadiar, 2004), place-based stigma disparages slums or iskuwater2 communities as “non-places” (Fortin, 2012), “shadow cities” (Neuwirth, [2005] 2016) and “modernity’s other” (Pinches, 1994, 25). Its dwellers are pejoratively labeled “tambay” (bums) (Batan, 2012), “criminals” and “non-citizens” (STWR, 2010, 26-35), even as “rascals” by a Philippine Supreme Court Justice (Galay v. -

AJAD 6.2 FINAL.Indb

Asian Journal of Agriculture and Development, Vol. 6, No. 2 51 The Transformation of Food Retail in the Philippines Glory Dee Romo University of the Philippines Mindanao, Philippines Email: [email protected] Larry Digal University of the Philippines Mindanao, Philippines Email: [email protected] Thomas Reardon Michigan State University, USA Email: [email protected] ABSTRACT From a small base by the end of the 1990s, modern retail (the chains selling at least some food) in the Philippines grew very rapidly in the 2000s, at thrice the rate of the country’s GDP growth. Reaching 13 billion USD of overall sales by 2010, 5.25 billion USD of this amount came from food sales. While much of the policy debate about market development focuses on export markets, we will show that supermarkets in the Philippines already sell twice the value (volume priced at export prices) of food that is exported – and modern retail is growing faster. Modern retail has reached 45 percent of urban food retail – already beyond the share of the middle class in the population, and about 35 percent of the national food market – from a tiny fraction of that fi gure two decades ago. Modern food retail is itself rapidly transforming – with a rise of fresh produce sales, industry concentration, format diversifi cation off-mall into formats that permit greater market penetration, and emerging procurement system modernization. While traditional food retail (and even most aspects of modern food retail) in the Philippines track international experience, the lack of major foreign presence even after retail foreign direct investment (FDI) liberalization in 2000 is a puzzle about which we present hypotheses.