In Re Nuvelo, Inc. Securities Litigation 07-CV-04056-Order

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fibrolase: Trials and Tribulations

Toxins 2010, 2, 793-808; doi:10.3390/toxins2040793 OPEN ACCESS toxins ISSN 2072-6651 www.mdpi.com/journal/toxins Review Fibrolase: Trials and Tribulations Francis S. Markland 1,2,* and Steve Swenson 1,2 1 Department of Biochemistry and Molecular Biology, Cancer Research Laboratory, Keck School of Medicine, University of Southern California, 1303 N. Mission Rd., Los Angeles, CA 90033, USA 2 USC/Norris Comprehensive Cancer Center, Keck School of Medicine, University of Southern California, Los Angeles, CA 90033, USA; E-Mail: [email protected] * Author to whom correspondence should be addressed; E-Mail: [email protected]; Tel.: +1-(323) 224-7981; Fax: +1-(323) 224-7679. Received: 11 March 2010; in revised form: 31 March 2010 / Accepted: 19 April 2010 / Published: 20 April 2010 Abstract: Fibrolase is the fibrinolytic enzyme isolated from Agkistrodon contortrix contortrix (southern copperhead snake) venom. The enzyme was purified by a three-step HPLC procedure and was shown to be homogeneous by standard criteria including reverse phase HPLC, molecular sieve chromatography and SDS-PAGE. The purified enzyme is a zinc metalloproteinase containing one mole of zinc. It is composed of 203 amino acids with a blocked amino-terminus due to cyclization of the terminal Gln residue. Fibrolase shares a significant degree of homology with enzymes of the reprolysin sub-family of metalloproteinases including an active site homology of close to 100%; it is rapidly inhibited by chelating agents such as EDTA, and by alpha2-macroglobulin (). The enzyme is a direct-acting thrombolytic agent and does not rely on plasminogen for clot dissolution. Fibrolase rapidly cleaves the A()-chain of fibrinogen and the B()-chain at a slower rate; it has no activity on the -chain. -

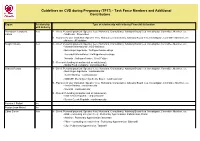

Guidelines on CVD During Pregnancy (TF17) - Task Force Members and Additional Contributors

Guidelines on CVD during Pregnancy (TF17) - Task Force Members and Additional Contributors Expert Relationship Type of relationship with industry Financial declaration with Industry Blomstrom-Lundqvist Yes A - Direct Personal payment: Speaker fees, Honoraria, Consultancy, Advisory Board fees, Investigator, Committee Member, etc. Carina - Medtronic : Pacemaker B - Payment to your Institution: Speaker fees, Honoraria, Consultancy, Advisory Board fees, Investigator, Committee Member, etc. - Atricure : AF ablation Borghi Claudio Yes A - Direct Personal payment: Speaker fees, Honoraria, Consultancy, Advisory Board fees, Investigator, Committee Member, etc. - Menarini International : ACE-inhibitors - Boheringer Ingelheim : Antihypertensive drugs - Recordati International : Antihypertensive drugs - Novartis : Antihypertensive, Heart Failure D - Research funding (departmental or institutional). - Barilla Food Company : Lactotripeptides Cifkova Renata Yes A - Direct Personal payment: Speaker fees, Honoraria, Consultancy, Advisory Board fees, Investigator, Committee Member, etc. - Boehringer-Ingelheim : cardiovascular - Daiichi Sankyo : cardiovascular - MSD-SP, Boehringer Ingelheim, Bayer : cardiovascular B - Payment to your Institution: Speaker fees, Honoraria, Consultancy, Advisory Board fees, Investigator, Committee Member, etc. - Daiichi Sankyo : cardiovascular - Novartis : cardiovascular D - Research funding (departmental or institutional). - Krka Czech Republic : cardiovascular - Servier Czech Republic : cardiovascular Ferreira J Rafael No -

In Re Nuvelo, Inc. Securities Litigation 07-CV-04056-Declaration of Mark

BERGER & MONTAGUE, P.C. Sherrie R. Savett Carole A. Broderick Phyllis M. Parker 1622 Locust Street Philadelphia, PA 19103 Tel: (215) 875-3000 Fax: (215) 875-4604 Email: [email protected] cbroderick@bm ,net [email protected] IZARD NOBEL LLP ROBBINS GELLER RUDMAN Jeffrey S. Nobel & DOWD LLP Mark P. Kindall, Bar No 138703 Darren J. Robbins Nancy A. Kulesa Dennis J. Herman 29 South Main Street Eli R. Greenstein Suite 215 S. Ashar Ahmed West Hartford, Ct 06107 Post-Montgomery Center Tel: (860) 493-6292 One Montgomery Street, Suite 1800 Fax: (860) 493-6290 San Francisco, CA 94104 Email: [email protected] Tel: (415) 288-4545 [email protected] Fax: (415) 288-4534 [email protected] Email: [email protected] dennisb@rgrdlaw,corn [email protected] aahmed@rgrdlaw com Co-Lead Counsel for Plaintiffs Liaison Counsel UNITED STATES DISTRICT COURT NORTHERN DISTRICT OF CALIFORNIA SAN FRANCISCO DIVISION In re NUVELO, INC. SECURITIES Master File No 07-CV-04056-VRW LITIGATION CLASS ACTION DECLARATION OF MARK P. KINDALL IN SUPPORT OF PLAINTIFFS' MOTION FOR CLASS CERTIFICATION DATE: March .3, 2011 I TIME: 10:00 a.rn. I COURTROOM: 6 DECLARATION OF MARK P KINDALL IN SUPPORT OF PLArNTIFFS' MOTION FOR CLASS CERTIFICATION - 07-CV-04056-VRW DECLARATION OF MARK P. KINDALL IN SUPPORT OF PLAINTIFFS' MOTION FOR CLASS CERTIFICATION 2 3 I, Mark P. Kindall, hereby declare as follows: 4 1. I am a partner at the law firm of Izard Nobel LLP, which was appointed Co-Lead 5 Counsel for Plaintiffs in this litigation on September 19, 2007. I have personal knowledge of the 6 facts set forth herein. -

The Development of Stroke Therapeutics: Promising Mechanisms and Translational Challenges

Neuropharmacology 56 (2009) 329–341 Contents lists available at ScienceDirect Neuropharmacology journal homepage: www.elsevier.com/locate/neuropharm Review The development of stroke therapeutics: Promising mechanisms and translational challenges Margaret M. Zaleska a, Mary Lynn T. Mercado a, Juan Chavez b, Giora Z. Feuerstein b, Menelas N. Pangalos a, Andrew Wood a,* a Discovery Neuroscience, Wyeth Research, CN8000, Princeton, NJ 08543, USA b Translational Medicine, Wyeth Research, Collegeville, PA, USA article info abstract Article history: Ischemic stroke is the second most common cause of death worldwide and a major cause of disability. Received 8 August 2008 Intravenous thrombolysis with rt-PA remains the only available acute therapy in patients who present Received in revised form within 3 h of stroke onset other than the recently approved mechanical MERCI device, substantiating the 29 September 2008 high unmet need in available stroke therapeutics. The development of successful therapeutic strategies Accepted 6 October 2008 remains challenging, as evidenced by the continued failures of new therapies in clinical trials. However, significant lessons have been learned and this knowledge is currently being incorporated into improved Keywords: pre-clinical and clinical design. Furthermore, advancements in imaging technologies and continued Ischemia Neuroprotection progress in understanding biological pathways have established a prolonged presence of salvageable Regeneration penumbral brain tissue and have begun to elucidate the natural repair response initiated by ischemic Inflammation insult. We review important past and current approaches to drug development with an emphasis on Neuroimaging implementing principles of translational research to achieve a rigorous conversion of knowledge from Translational medicine bench to bedside. We highlight current strategies to protect and repair brain tissue with the promise to Drug development provide longer therapeutic windows, preservation of multiple tissue compartments and improved clinical success. -

The Bottom 99

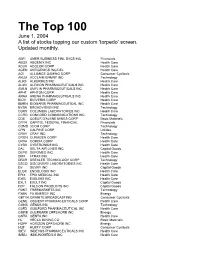

The Top 100 June 1, 2004 A list of stocks topping our custom 'torpedo’ screen. Updated monthly. ABFI AMER BUSINESS FINL SVCS INC Financials ABGX ABGENIX INC Health Care ADLR ADOLOR CORP Health Care AGEN ANTIGENICS INC/DEL Health Care AGI ALLIANCE GAMING CORP Consumer Cyclicals AKLM ACCLAIM ENMNT INC Technology ALKS ALKERMES INC Health Care ALXN ALEXION PHARMACEUTICALS INC Health Care AMLN AMYLIN PHARMACEUTICALS INC Health Care APHT APHTON CORP Health Care ARNA ARENA PHARMACEUTICALS INC Health Care BIOV BIOVERIS CORP Health Care BMRN BIOMARIN PHARMACEUTICAL INC Health Care BVSN BROADVISION INC Technology CBRX COLUMBIA LABORATORIES INC Health Care CCRD CONCORD COMMUNICATIONS INC Technology CDE COEUR D'ALENE MINES CORP Basic Materials CFFN CAPITOL FEDERAL FINANCIAL Financials COMS 3COM CORP Technology CPN CALPINE CORP Utilities CRAY CRAY INC Technology CRGN CURAGEN CORP Health Care CRXA CORIXA CORP Health Care CYBX CYBERONICS INC Health Care DAL DELTA AIR LINES INC Capital Goods DEPO DEPOMED INC Health Care DMX I-TRAX INC Health Care DRXR DREXLER TECHNOLOGY CORP Technology DSCO DISCOVERY LABORATORIES INC Health Care DV DEVRY INC Capital Goods ELGX ENDOLOGIX INC Health Care EPIX EPIX MEDICAL INC Health Care EXEL EXELIXIS INC Health Care EXLT EXULT INC Capital Goods FCP FALCON PRODUCTS INC Capital Goods FMKT FREEMARKETS INC Technology FXEN FX ENERGY INC Energy GBTVK GRANITE BROADCASTING Consumer Cyclicals GENE OSCIENT PHARMACEUTICALS CORP Health Care GGNS GENUS INC Technology GLFD GUILFORD PHARMACEUTICAL INC Health Care GMRK GULFMARK OFFSHORE -

Healthcare Conference

25th Annual HEALTHCARE CONFERENCE Healthcare Westin St. Francis San Francisco January 8–11, 2007 JPMorgan cordially invites you to attend the 25th Annual Healthcare Conference, January 8 –11, 2007, at the Westin St. Francis in San Francisco. JPMorgan’s premier conference on the healthcare industry will feature more than 260 public and private companies over four days of simultaneous sessions. In addition, the conference will host topical panel discussions featuring leading industry experts. Preliminary List of Invited Presenting Companies Actelion Ltd Baxter International Inc. Cooper Companies Aetna Incorporated BD (Becton, Dickinson) Coventry Affymetrix, Inc. Beckman Coulter, Inc. Dade Behring Holdings, Inc. Alcon, Inc. Bioenvision, Inc. DaVita Inc. Align Technology, Inc. Biogen Idec deCODE genetics, Inc. Allscripts Healthcare Solutions Inc. Biomet, Inc. Digene Altana Boston Scientific Corporation Digirad Corporation — US American Medical Systems Holdings Inc. Bristol-Myers Squibb Company Diversa Corporation Amerigroup Corp. Cambrex Corporation DJO Incorporated AmerisourceBergen Cardinal Health, Inc. Dyax Corp. Amgen, Inc. Caremark Rx, Inc. Eclipsys Corporation AMN Healthcare Services, Inc. Celgene Corporation Edwards Lifesciences Corporation AmSurg Corporation Cell Genesys Elan Corporation, plc Anadys Pharmaceuticals CENTENE Corporation Eli Lilly and Company Applied Biosystems Group Cephalon, Inc. Emdeon Ariad Pharmaceuticals, Inc. Cerner Corporation Emergency Medical Services Corporation AstraZeneca Group plc Charles River Laboratories, -

Schedule 14A Information

QuickLinks -- Click here to rapidly navigate through this document SCHEDULE 14A INFORMATION Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 Filed by the Registrant ý Filed by a Party other than the Registrant o Check the appropriate box: o Preliminary Proxy Statement o Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) ý Definitive Proxy Statement o Definitive Additional Materials o Soliciting Material Pursuant to §240.14a-12 GILEAD SCIENCES, INC. (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): ý No fee required. o Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0- 11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: o Fee paid previously with preliminary materials. o Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: GILEAD SCIENCES, INC. -

How Scientist/Founders Lead Successful

HOW SCIENTIST/FOUNDERS LEAD SUCCESSFUL BIOPHARMACEUTICAL ORGANIZATIONS: A STUDY OF THREE COMPANIES Lynn Johnson Langer A DISSERTATION Submitted to the Ph.D. in Leadership & Change Program of Antioch University in partial fulfillment of the requirements for the degree of Doctor of Philosophy May, 2008 This is to certify that the dissertation entitled: HOW SCIENTIST/FOUNDERS LEAD SUCCESSFUL BIOPHARMACEUTICAL ORGANIZATIONS: A STUDY OF THREE COMPANIES prepared by Lynn Johnson Langer is approved in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Leadership & Change. Approved by: ______________________________________________________________________ Alan E. Guskin, Ph.D., Chair date ______________________________________________________________________ Jon Wergin, Ph.D., Committee Member date ______________________________________________________________________ Mitch Kusy, Ph.D., Committee Member date ______________________________________________________________________ Alice Sapienza, DBA, External Reader date Copyright 2008 Lynn Johnson Langer All rights reserved Acknowledgements I arrive at this place in my journey to becoming a scholar supported in love and friendship by so many people. I must thank first and foremost my husband, Eric Langer, who has supported me in many ways, but particularly with my education. I thank my daughter, Julia Annemarie, my study partner. We shout across the hall to each other, complaining and laughing about all the work. I thank her for her support and the opportunity to be a role model. She never once complained about the plays and events I missed because I was away at a residency. I thank my son, Adam and his wife, Megan who through their lives, remind me to follow my dreams. I thank my son, Benjamin, who shows me that through hard work, we can accomplish great things. -

UR-Coeus Sponsor List

UR-Coeus Sponsor Table (alphabetical by sponsor name) Sponsor Sponsor Code Sponsor Type 2138 21st Century Medicine CORP Sponsor Type Key 1 3M CORP CORP = Corporate 3803 4S3 Bioscience Inc CORP FED = Federal 5207 A. F. Associates Family Medicine ONFA FND = Foundation 2602 A. P. Pharma CORP IND = Individuals 2 A.L. Mailman Foundation FND NYS = New York State 2023 AA Implant Dentistry Research Foundation ONFA OLG = Other Local Gov't 3 AAA Fnd for Traffic Safety ONFA ONFA = Other Non-Fed Agency 2329 aaiPharma Inc CORP VHA = Voluntary Health Agency 3257 Aamjiwnaang First Nations Community ONFA 5345 Aarhus University Hospital ONFA 3713 Aaron Copland Fund for Music, Inc. ONFA 4 AARP Andrus Fdn FND 3853 AB Sciences CORP 3378 AB Vector, Inc CORP 899 Abbott Diagnostics CORP 3864 Abbott Fund FND 14 Abbott Laboratories CORP 5126 AbbVie, Inc. CORP 5854 Abeona Therapeutics CORP 5063 Abington Medical Specialists ONFA 5331 Abington Memorial Hospital ONFA 2835 ABIOMED, Inc. CORP 3687 Ablation Frontiers CORP 5118 Ablynx NV CORP 2053 ABMRF/Fnd for Alcohol Research ONFA 2171 Abortion Rights Mobilization ONFA 3361 Abraxix BioScience, LLC CORP 4953 Abt Associates, Inc. CORP 5037 Academic Gastrointestinal Cancer Consortium ONFA 15 Academic Med Ctr Cons ONFA 3733 Academic Pediatric Association ONFA 3160 Academy of Orofacial Pain ONFA 2122 Academy of Prosthodontics Foundation ONFA 3663 Acadia Pharmaceuticals, Inc. CORP 3273 Accelerate Brain Cancer Cure ONFA 5584 Acceleron Pharma Inc. CORP 5601 Accelovance, Inc. CORP 5940 Accreditation Council Grad Med Educ ONFA 5832 Accriva Diagnostics CORP 3888 AccuGenomics, Inc. CORP 5656 Acerta Pharma CORP 6101 Acessa Health, Inc. -

Kyowa Hakko Kirin Co ., Ltd Fiscal 2008 First Half Results

Kyowa Hakko Kirin Co ., Ltd Fiscal 2008 First Half Results October 30, 2008 President and Chief Executive Officer Yuzuru Matsuda Statements on results, forecasts and R&D status contained in this presentation represent judgments based on information available at the current time. Actual results may differ significantly due to a variety of factors such as economic conditions and exchange rate fluctuations. Separate service 65% 1 companies HD: Kirin by Other businesses Held by Kirin HD: Held by Kyowa Kirin: 35% subsidiary of Kirin Holdings Business integration 2011.1.1owned wholly a Will become 2009.4.1 Kirin Kyowa Foods Launched Kirin Food-Tech Other subsidiaries KYOWA HAKKO FOOD SPECIALTIES Kirin Co., Ltd. Kyowa Hakko Kirin Holdings KYOWA HAKKO CHEMICAL Mercian KYOWA HAKKO BIO Kirin Beverage Kirin Brewery Business structure (200810.1 ~) z z Outline of Fiscal 2008 firstfirst halfhalf rresultsesults Operating Recurring (¥bn) Net sales Net income income income FY08 H1 247.7 29.1 30.3 8.2 +55.1 +10.9 +12.2 -2.7 Change (+28.6%) (+59.8%) (+67.9%) (-25. 0%) FY07 H1 192.6 18.2 18.0 11.0 z Pharmaceuticals Sales and profits up due to Kirin Pharma integration, receipt of oneone--offoff payment from Amgen, etc. z Bio-Chemicals Sales and profits up due to growth in amino acids for intravenous liquids and pharmaceutical raw materials, and increased sales of health care products z Chemicals Sales up due to price revisions following rapid rise in fuel and raw materials prices but increased depreciation expense contributed to lower operating income z Food -

Transforming Clinical Trials in Cardiovascular Disease Mission Critical for Health and Economic Well-Being

VIEWPOINT Transforming Clinical Trials in Cardiovascular Disease Mission Critical for Health and Economic Well-being Elliott M. Antman, MD Perhaps the most exciting opportunity for CVD research- ers is to capitalize on the advances in systems and computa- Robert A. Harrington, MD tional biology that can inform first-in-human, proof-of- S EMPHASIZED BY THE BIPARTISAN POLICY CENTER, concept, and phase 2 dose-ranging trials in ways that were not healthcareexpendituresareanticipatedtoreach20% previously possible.4 Examples include using biomarkers, ge- of US gross domestic product by 2020 and are a netic observations, and definitions of pathophenotypes to adapt major threat to the sustainability of the health care the treatments being investigated. This is particularly rel- Asystem and to the economic productivity and stability of the evant to new treatments being explored for managing dyslip- country. Although death rates attributable to cardiovascular dis- idemia (eg, PCSK9 inhibition), diabetes, ischemic heart dis- ease (CVD) have declined by almost one-third over the last 11⁄2 ease, and heart failure—all topics that are among the 19 studies decades, CVD remains the leading cause of death and the bur- presented in the Clinical Science: Special Reports sessions at den of CVD remains unacceptably high, especially consider- the AHA meeting.2 As emphasized by the FDA in a draft guid- ing the aging of the population.1 The economic effects of the ance document, adaptive designs are encouraged during the burden of CVD are profound because managing -

In Re Nuvelo, Inc. Securities Litigation 07-CV-04056-Second

1 COUGHLIN STOIA GELLER RUDMAN & ROBBINS LLP 2 DENNIS J. HERMAN (220163) ELI R. GREENSTEIN 3 100 Pine Street, Suite 2600 4 San Francisco, CA 94111 Telephone : 415/288-4545 5 Fax: 415/288-4534 [email protected] 6 elig^a,csgrr.com 7 Liaison Counsel 8 BERGER & MONTAGE, P.C. IZARD NOBEL, LLP 9 SHERRIE R. SAVETT JEFFREY S. NOBEL CAROLE A. BRODERICK MARK P. KINDALL 10 BARBARA A. PODELL NANCY A. KULESA PHYLLIS M. PARKER SETH R. KLEIN 11 1622 Locust Street One Corporate Center 12 Philadelphia, PA 19103 One Church Street, Suite 1700 Telephone: 215/875-300 Hartford, CT 06103 13 Fax: 215/875-4604 Telephone: 860/493-6292 ssaveft@,,bm.net Fax: 860/493-6290 14 cbroderick@,bm.net [email protected] 15 bpodell@,,bm.et [email protected] pparker(&,,bm.net nkulesa(a,snilaw.com 16 [email protected] 17 Co-Lead Counsel for Plaintiffs 18 UNITED STATES DISTRICT COURT 19 NORTHERN DISTRICT OF CALIFORNIA 20 21 In re NUVELO, INC. SECURITIES Master File No. 3:07-cv-04056-VRW LITIGATION 22 CLASS ACTION 23 This Document Relates To: SECOND CONSOLIDATED COMPLAINT FOR VIOLATIONS OF THE FEDERAL 24 ALL ACTIONS. SECURITIES LAWS 25 26 27 28 1 TABLE OF CONTENTS 2 I. INTRODUCTION ...................................................................................................1 3 II. JURISDICTION AND VENUE ............................................................................ 15 4 III. PARTIES ............................................................................................................... 16 5 IV. CONFIDENTIAL WITNESSES ..........................................................................