Study of Retail Market Conditions - April 2017 Acknowledgement Credit

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brochure and to the Documents Required by Section 718.503, Florida Statutes, to Be Furnished by a Developer to a Buyer Or Lessee

OBTAIN THE PROPERTY REPORT REQUIRED BY THE FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE, IF ANY, OF THIS PROPERTY. ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING THE REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. AUBERGE BEACH 1 DEVELOPED BY VISIONARIES page 10 THE AUTHENTIC LUXURY OF AUBERGE page 14 ORIGINAL WORKS OF CONTEMPORARY ART page 22 FEATURES & AMENITIES page 48 FORT LAUDERDALE LIFESTYLE page 62 AUBERGE BEACH 2 SEE LEGAL DISCLAIMERS ON BACK COVER AUBERGE BEACH AUBERGE BEACH 4 5 SEE LEGAL DISCLAIMERS ON BACK COVER INDULGE IN THE ELEGANCE OF BEACHFRONT LIVING AUBERGE BEACH RESIDENCES & SPA FORT LAUDERDALE JOINS AN INTERNATIONAL PORTFOLIO OF AWARD-WINNING PROPERTIES IN NORTH AMERICA Auberge Beach Residences & Spa brings the ultimate personal service ensures that residents’ every need is in luxury living to Fort Lauderdale’s most extraordinary catered to with ease. Unique among even the finest beachfront property. Exquisitely designed residences, a luxury residential properties, Auberge Beach Residences rich array of indoor and outdoor amenities, a tempting & Spa will offer a host of exclusive cultural and culinary selection of restaurants, and a world-class Auberge- experiences that have been thoughtfully crafted to branded dining and spa are perfectly located directly enhance residents’ lifestyle and engage their senses. on 450 linear feet of pristine Atlantic Ocean beachfront. From sunup to sundown and deep into the night, Throughout Auberge Beach Residences & Spa, a curated residents will enjoy living life to its fullest and creating collection of contemporary art creates an atmosphere memories that will last a lifetime. -

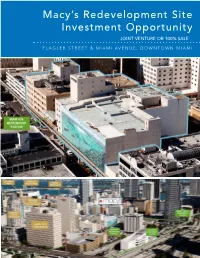

Macy's Redevelopment Site Investment Opportunity

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna Businesses searching for space in Miami's urban core have more options than they might think. While vacancy rates are down across the board, significant chunks of space are available in several Class A buildings in downtown and the Brickell Avenue financial district. "There are more alternatives available for those companies that take the time to appropriately investigate the market," said Chris Lovell, a senior managing director with Savills Studley in Miami. Leasing space on an upper floor with a view may be difficult since only six buildings on Brickell have a full floor above the 20th story available for lease. For tenants that can live without the view, there is plenty of open space to choose from. Four downtown Class A buildings have at least 75,000 square feet of contiguous space available, one Class A building on Brickell has a 65,000- square-foot block — "and we don't have tenants of that size standing in line to the claim the space," Lovell said. Savills Studley has found many of the large available blocks are in older downtown buildings. "You're always going to have buildings that are going to have certain pockets available," said Tere Blanca, founder of Miami-based Blanca Commercial Real Estate Inc. She said the market is responding well to the new Miami Central project, which is under construction with 60 percent of its office component pre- leased. The mixed-use development will serve as Brightline's downtown train station and will add 286,000 square feet of office space in two buildings. -

Echo Brickell Condos Fact Sheet

FACT SHEET Address 1451 Brickell Avenue, Miami, FL 33131 Project Description Echo Brickell is a boutique, residential high-rise in the epicenter of Miami’s fastest growing metropolitan neighborhood, located on the coveted East side of Brickell Avenue. Echo Brickell is the result of a first- time collaboration between acclaimed architect Carlos Ott and the esteemed innovators at yoo Studio. With only 180 residences, Echo Brickell is the most exclusive architectural icon south of New York. The fully finished, exquisitely designed residences feature summer kitchens and top-of-the-line appliances. Expansive terraces bring the outside in and marble flooring throughout the living spaces elevates the level of grandeur. These limited edition residences bring together innovative architecture and modern interior design to create a living space that’s impeccable, exciting and unique. Echo Brickell’s state-of-the-art residences will redefine the standard of excellence for South Florida high- rise living. Developer Echo Brickell is a joint venture between Property Markets Group and JDS Development Group. Founded in 1991 by Kevin Maloney, Property Markets Group (“PMG”) has direct hands-on experience in the acquisition, renovation, financing, operation, and marketing of residential and commercial real estate. A development firm of national scope, PMG has over 150 real estate transactions during its 20-year history. Team Conceptual Design: Carlos Ott Interior Design: yoo Studio Architect of Record: Cohen Freedman Encinosa ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. -

Echo Brickell

ECHO BRICKELL ECHO BRICKELL Call: +1.786.383.1553 Call: +1.786.383.1553 ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. OBTAIN THE PROPERTY REPORT REQUIRED BY FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE , IF ANY, OF THIS PROPERTY . EAST/SOUTHEAST VIEW VIEWS ACTUAL VIEWS MAY VARY AND CANNOT BE GUARANTEED. VIEWS SHOWN CANNOT BE RELIED UPON AS THE ACTUAL VIEW FROM ANY PARTICULAR UNIT WITHIN THE CONDOMINIUM. ORAL REPRESENTATIONS CAN- NOT BE RELIED UPON AS CORRECTLY STATING REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. OBTAIN THE PROPERTY REPORT REQUIRED BY FEDERAL LAW AND READ IT BEFORE SIGNING ANYTHING. NO FEDERAL AGENCY HAS JUDGED THE MERITS OR VALUE, IF ANY, OF THIS PROPERTY. OVERVIEW ECHO Brickell is a boutique residential high-rise in the epicenter of Miami’s fastest growing metropolitan neighborhood, located on the coveted East side of Brickell Avenue. Echo Brickell’s 157 state-of-the-art residences redefine opulent living in Miami’s most exciting locale. With conceptual design from mastermind Carlos Ott, ECHO Brickell is a host of privilege at every turn. Echo Brickell’s interiors introduce an exciting new concept to the world - fusing world renowned architect, Carlos Ott and yoo design studio, in a first time collaboration to create a limited edition collection: Carlos Ott + yoo . -

Miami Condos Most at Risk Sea Level Rise

MIAMI CONDOS MIAMI CONDOS MOST AT RISK www.emiami.condos SEA LEVEL RISE RED ZONE 2’ 3’ 4’ Miami Beach Miami Beach Miami Beach Venetian Isle Apartments - Venetian Isle Apartments - Venetian Isle Apartments - Island Terrace Condominium - Island Terrace Condominium - Island Terrace Condominium - Costa Brava Condominium - -Costa Brava Condominium - -Costa Brava Condominium - Alton Park Condo - Alton Park Condo - Alton Park Condo - Mirador 1000 Condo - Mirador 1000 Condo - Mirador 1000 Condo - Floridian Condominiums - Floridian Condominiums - Floridian Condominiums - South Beach Bayside Condominium - South Beach Bayside Condominium - South Beach Bayside Condominium - Portugal Tower Condominium - Portugal Tower Condominium - Portugal Tower Condominium - La Tour Condominium - La Tour Condominium - La Tour Condominium - Sunset Beach Condominiums - Sunset Beach Condominiums - Sunset Beach Condominiums - Tower 41 Condominium - Tower 41 Condominium - Tower 41 Condominium - Eden Roc Miami Beach - Eden Roc Miami Beach - Eden Roc Miami Beach - Mimosa Condominium - Mimosa Condominium - Mimosa Condominium - Carriage Club Condominium - Carriage Club Condominium - Carriage Club Condominium - Marlborough House - Marlborough House - Marlborough House - Grandview - Grandview - Grandview - Monte Carlo Miami Beach - Monte Carlo Miami Beach - Monte Carlo Miami Beach - Sherry Frontenac - Sherry Frontenac - Sherry Frontenac - Carillon - Carillon - Carillon - Ritz Carlton Bal Harbour - Ritz Carlton Bal Harbour - Ritz Carlton Bal Harbour - Harbor House - Harbor House -

MIRACLE MILE - Between Le Jeune Rd

TERRANOVA www.terranovacorp.com | 305.695.8700 801 Arthur Godfrey Road, Suite 600 Miami Beach, FL 33140 BY THE NUMBERS LINCOLN ROAD - Between Alton Road and Washington Ave. 525,477 sf 6.2% $203.34 of AVERAGE VACANCY RATE Inventory ASKING NET RENT COLLINS AVENUE - Between 5th Street and 10th Street 201,297 sf 4.3% $88.56 of AVERAGE VACANCY RATE Inventory ASKING NET RENT OCEAN DRIVE - Between 5th Street and 15th Street. 165,768 sf $97.53 of 3.0% VACANCY RATE AVERAGE Inventory ASKING NET RENT MIRACLE MILE - Between Le Jeune Rd. and Douglas Rd. 440,886 sf $44.60 of 6.2% VACANCY RATE AVERAGE Inventory ASKING NET RENT LAS OLAS BOULEVARD - Between SE 6th Ave. to SE 16th Ave. 367,803 sf 5.3% $36.17 of AVERAGE VACANCY RATE Inventory ASKING NET RENT CLEMATIS STREET - Between Olive Ave. and Quadrille Blvd. 329,086 sf $23.22 of 12.2% VACANCY RATE AVERAGE Inventory ASKING NET RENT WORTH AVENUE - Between Ocean Blvd. and Coconut Row 319,387 sf $75.61 of 2.4% AVERAGE VACANCY RATE Inventory ASKING NET RENT FLAGLER STREET - Between Biscayne Blvd. and NW First Ave. 372,541 sf $29.25 of 10.1% VACANCY RATE AVERAGE Inventory ASKING NET RENT SOUTH MIAMI - Between US-1 and SW 57th Ave. 244,082 sf 0% N/A of AVERAGE Inventory VACANCY RATE ASKING NET RENT TAKING TO THE STREET: URBAN RETAILSCAPE IN SOUTH FLORIDA Occupancy and asking rents have renovation and revival, compared to kept an upward trend in South the other streets. -

Le Parc at Brickell Condos Brochure

BIG CITY LIVING WITHOUT THE BIG CITY HASSLE. UNA VIDA COSMOPÓLITA SIN LOS INCONVENIENTES DE VIVIR EN LA CIUDAD THE NEW NATURE Seconds away from the thriving energy of downtown Miami and the Brickell OF BRICKELL CITY LIVING. Financial District, the unique sanctuary of Le Parc beckons. LA NUEVA NATURALEZA DE LA VIDA EN BRICKELL. A sleek boutique building of glass and stainless steel directly across from the gorgeous Simpson Park makes a quiet, yet confident statement that your idea of city living is about to change. A tan solo segundos del vibrante centro de Miami y del distrito financiero de Brickell, el santuario único de Le Parc, resalta. Un elegante edificio boutique de vidrio y acero inoxidable justo enfrente al hermoso Simpson Park, hace una tranquila, pero al mismo tiempo firme, declaración de que su ideal de vida en la ciudad está a punto de cambiar. GREEN AND QUIET, YET CONNECTED. ECOLÓGICO Y TRANQUILO EN LA CIUDAD. BUILDING AMENITIES 12-story building with 128 residences: studios, Gated entry and security key card access Clubroom and state-of-the-art fitness center one to three bedrooms and nine-expansive inside the building townhomes Business lounge with conference room Party room available for the resident’s Privileged location with unobstructed views of enjoyment Kid’s entertainment room Simpson Park Pool deck on fourth floor Pet-friendly environment Elegant double-height lobby and Interior designs by renowned Ligne Roset Roof-top sky lounge with Jacuzzi CARACTERÍSTICAS DEL EDIFICIO 12 pisos de altura con 128 residencias Entrada -

Brickell Flatiron Brochure ENGLISH.Pdf

Patricio Javier Orloff, P.A. Cervera Real Estate Miami: 305.726.8155 Buenos Aires: 11.5129.6649 [email protected] www.flatironbrickellmiami.com ORAL REPRESENTATIONS CANNOT BE RELIED UPON AS CORRECTLY STATING THE REPRESENTATIONS OF THE DEVELOPER. FOR CORRECT REPRESENTATIONS, MAKE REFERENCE TO THIS BROCHURE AND TO THE DOCUMENTS REQUIRED BY SECTION 718.503, FLORIDA STATUTES, TO BE FURNISHED BY A DEVELOPER TO A BUYER OR LESSEE. BRICKELL FLATIRON ENVISIONING A LANDMARK Refreshing the Miami Skyline Presenting a new paradigm in luxurious living. Downtown Miami’s hottest neighborhood celebrates a property that represents a true architectural icon. Brickell Flatiron is an urban oasis developed by Ugo Colombo's CMC Group and designed by Luis RevueltaRI Revuelta Architecture International: the tower of soaring glass is defined by its sweeping exposures, which punctuate its romantic renaissance- revival interiors. Artist's Rendering Artist's Rendering BRICKELL FLATIRON BRICKELL FLATIRON BRICKELL A Lively Composition of Commerce and Culture. As Miami’s Financial District, Brickell remains a sophisticated and culturally significant community packed with creative types and tastemakers of every stripe. BRICKELL FLATIRON LOCATION A Walk-around Neighborhood BRICKELL FLATIRON Located in the heart of Downtown Miami, Brickell Flatiron is ideally situated within walking distance of Mary Brickell Village and Brickell City Centre — offering residents unparalleled access to a wide array of fashionable conveniences — with picturesque sidewalk cafés, fine dining, shopping, markets, outdoor and cultural activities along the way. BRICKELL FLATIRON Artist's Rendering BRICKELL FLATIRON A More Playful Line Brickell Flatiron’s innovative architectural design introduces flowing curvilinear forms to accommodate spacious floor plans. -

1450 BRICKELL FACTS Large Missile

At the entrance MIAMI · FLORIDA to the Brickell Setting the5415, 5455Highest Standard in Class A Office Buildings Financial District, 1450 Brickell offers Class A corporate headquarters prominence with panoramic water views, commuter convenience and unparalleled infrastructure for business continuity. 1450BRICKELL.COM 5415, 5455 SETTING THE HIGHEST STANDARD 1450 Brickell is a 35-story, 626,750 RSF Class A Office High Rise Tower at the entrance to Brickell Avenue 1450BRICKELL.COM 5415, 5455 CONVENIENT ACCESS AWAY FROM NEAR TOP HOTELS, RESTAURANTS, TRAFFIC CONGESTION OF DRAWBRIDGES RESIDENTIAL, AND RETAIL Brickell Ave. 18 th SW 7 St. Exit 1-B Brickell Key SW 8th St. S. Miami Ave. B I 15 17 Brickell Key SW 7th Ave. Metromover SW 2nd Ave. S. Miami Ave. 16 H SW 11th St. SW 1th Ave. Brickell City Center SW 8th St. 13 Brickell Ave. SW 9th Ave. 12 11 15th Rd. Metromover Shops At Mary Brickell Village 14 C SW 10th St. F G Coral Way 10 Simpson th SW 26 Rd. Park 9 SW 12th St. D S. Miami Ave. 8 S. Miami Ave. SW 15th Rd. 7 S. Miami Ave. th 5415, 5455 SW 12 Ave. 6 C 5 Exit 1-A A 4 Brickell Ave. 3 I Simpson 2 Park Coral Way 1 U.S. 1 Brickell Hammock S. Miami Ave. E Alice C. Wainwright 5415, 5455 5415, 5455 LESS DRIVE TIME... MORE BUSINESS 1. Echo Brickell Residences 9. JW Marriot A. From Brickell Avenue F. From S.W. 15th Road 2. PM Fish & Steak House 10. Nusr-Et Steakhouse going North G. -

SLS Lux Brickell Condos Brochure

TM Brickell CityCentre scintillating High fashion, fine dining, and chic entertainment all come together in Brickell, Miami’s most exciting and sophisticated downtown neighborhood. Elite corporate headquarters and top international financial institutions attract the most powerful and savvy business people, and LIFESTYLE the 5 million square foot Brickell CityCentre caters to clientele with refined taste. scenarios SEE LEGAL DISCLAIMERS ON BACK COVER INTRODUCING SLS LUX: DESIGNED TO INDULGE THE SENSES Just steps away from upcoming Brickell CityCentre, Miami’s newest and most extravagant shopping and lifestyle destination, SLS LUX offers residents ultimate access in an oasis of exclusive privileges. Sophisticated designer interiors, original works of art by contemporary masters, private rooftop pool terraces, celebrity chef restaurants, and limousine service to a chic private beach club are among the many features, amenities, and services designed to indulge the most discriminating clientele. BUILDING FEATURES • Located in the heart of Brickell between upcoming Brickell CityCentre’s high-end retail and restaurants and the Mary Brickell Village shopping center. • 57-story tower designed by internationally renowned architecture firm Arquitectonica, featuring the first LED façade by prominent lighting artist Ana Martinez. • Interiors designed by Yabu Pushelberg. • Museum-quality art in all common areas, including works by renowned artists such as Fernando Botero and Matias Duville, among others, and exterior art mural installation by Fabian Burgos. • Ground floor restaurant by celebrated chef Katsuya Uechi and cocktail lounge by SBar. • 450 luxury condominiums featuring private elevators. • A limited collection of 12 Penthouse Residences on the top three floors with 12 foot ceilings, custom gourmet kitchens and panoramic skyline, Biscayne Bay, and Atlantic Ocean views. -

Luxury Condo Markets Sprout in Downtowns

Brian Bandell | Senior Reporter | South Florida Business Journal Luxury condo markets sprout in downtowns South Florida beaches were once the prime domain for luxury condo units listing for $1 million or more. But bustling downtowns and neighboring communities have become strong players in the market. The influx of high-priced units has attracted more wealthy residents near the urban cores of Miami, Fort Lauderdale, Boca Raton and West Palm Beach. And those spending $1 million or more for a condo are likelier to live there – even if part time – as opposed to renting them out for investment purposes. That means a greater stream of deep-pocketed spenders frequenting local businesses. But despite the boon to the local economy, some experts warn of an imminent slowdown in luxury condo sales – especially in Miami – due to an oversaturated market. The current inventory of units on the market could take years to sell off, even as new luxury buildings near completion. With so many units on the market in Miami, those who bought at the beginning of the cycle would likely end up selling their condos at a loss, said Peter Zalewski, a principal with Miami-based Condo Vultures. Many developers are reluctant to start new projects now because they can’t price units at the premium levels reached a few years ago, he added. Despite that, the majority of the units in many of the latest luxury buildings delivered in downtown areas have sold. New standard for downtown Miami The One Thousand Museum condominium, designed by late architect Zaha Hadid, set a new standard for luxury condo sales in downtown Miami, especially on Biscayne Boulevard.