Share Buy Back Circular

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

'Islamisation' Myth

DEBUNKING THE 'ISLAMISATION' MYTH ___________________________________________ Edmund Standing DEBUNKING THE ‘ISLAMISATION’ MYTH Why Britain Will Not Become an Islamic State ________________________________________ ________________________________________ About the author Edmund Standing is the author of The BNP and the Online Fascist Network (Centre for Social Cohesion, 2009) and co-author (with Alexander Meleagrou-Hitchens) of Blood & Honour: Britain’s Far-Right Militants (Centre for Social Cohesion & Nothing British, 2010). CONTENTS Preface 3 Introduction 4 I Cultural Pessimism and the ‘Islamisation’ Myth 5 II The Myth of International Muslim Power 8 III The Myth of Muslim Power in Britain 12 IV The Myth of a ‘Demographic Time Bomb’ 25 Conclusion: Against the Culture of Despair 29 References 31 PREFACE I am an atheist, a secularist, and an anti-fascist. I have no interest in defending Islamic religious beliefs, nor the Qur’an (quite the opposite, in fact). I also have no time for those who seek to ‘understand’ Islamism or downplay the abhorrent nature of religious fascism. That said, I am also committed to a rational and just approach to my fellow human beings, seeking to treat them in the same way, regardless of nationality, ethnicity, religious affiliation, and so on. To think Islam as a set of beliefs is false and potentially dangerous is not the same thing at all as thinking that all Muslims are inherently dangerous or that I should view them as qualitatively different to other human beings. In the post-9/11 West, we have seen the worrying growth of a paranoid, bigoted approach to Muslims which increasingly views them as an undifferentiated mass, as an inherent Other, and as a powerful fifth column conspiring to destroy the West and enslave it to Sharia law. -

Addison Lee Is Sold for £300 Million. Did Dac Drivers Miss Their Chance

3 1 0 2 y a M Addison Lee is sold for £300 million. Did DaC drivers miss their chance to cash in with this man? See ‘What If’ on page 3… Call Sign May 2013 Page 2 NASH’S NUMBERS From Alan Nash (A95) Heathrow departure terminals - last updated in May 2012 and prompted by Virgin now operating Little Red. New version correct as of 02/04/2013 from data obtained via BAA website. ** British Airways: All BA flights depart Terminal 5 except those listed below. The following British Airways flights depart Terminal 3: Bangkok, Bucharest, Budapest, Gibraltar, Helsinki, Lisbon, Prague, Vienna and Warsaw . The following British Airways flights depart Terminal 1: Amman, Baku, Belfast, Cairo, Dublin, Hanover, Luxembourg, Lyon, Marseille, Rotterdam, Tbilisi and Tel Aviv. Contact no: 0844 493 0787. *** United Airlines. All United Airways depart Terminal 1 except those listed below. The following United Airlines flights depart Terminal 4: Houston and New York (Newark). Contact No. 0845 844 4777 Heathrow terminals by airline excluding BA & United Airlines (see above). Whilst this table looks like last May’s Call Sign article, 8 airlines have gone, there are 2 new airlines, 12 telephone number changes and BA now operate out of T1 as well as T3 and T5... Call Sign May 2013 Page 3 from the editor’s desk Car sitting? capital investment being an example, but added You may have heard that Aspect , a London prop - that since we were all interested in the same thing erty maintenance firm, has been employing young – ie success - Sovereign were confident that opin - people with clean driving licences to 'van-sit' their ions would be sought on a broad basis with deci - fleet of vehicles so that while the engineer is inside sions taken openly and sensibly. -

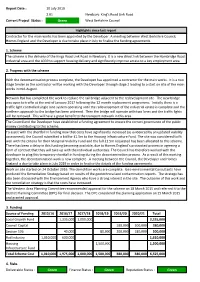

Item 6 Appendix 1 Composite Scheme Reports

Report Date : 10 July 2019 2.01 Newbury: King's Road Link Road Current Project Status : Green West Berkshire Council Highlights since last report Contractor for the main works has been appointed by the Developer. A meeting between West Berkshire Council, Homes England and the Developer is due to take place in July to finalise the funding agreements. 1. Scheme The scheme is the delivery of the Kings Road Link Road in Newbury. It is a new direct link between the Hambridge Road industrial area and the A339 to support housing delivery and significantly improve access to a key employment area. 2. Progress with the scheme With the decontamination process complete, the Developer has appointed a contractor for the main works. It is a two stage tender so the contractor will be working with the Developer through stage 2 leading to a start on site of the main works in mid-August. Network Rail has completed the work to replace the rail bridge adjacent to the redevelopment site. The new bridge was open to traffic at the end of January 2017 following the 12 month replacement programme. Initially there is a traffic light controlled single lane system operating until the redevelopment of the industrial estate is complete and the northern approach to the bridge has been widened. Then the bridge will operate with two lanes and the traffic lights will be removed. This will have a great benefit to the transport network in this area. The Council and the Developer have established a funding agreement to ensure the correct governance of the public money contributing to this scheme. -

Local Cycling & Walking Infrastructure Plan

Local Cycling & Walking Infrastructure Plan LCWIP 1 Contents Foreword 3 1 Introduction 4 2 Integration with Active Travel Policy 7 3 Active Travel context 9 4 Network planning for cycling 14 5 Network planning for walking 24 6 Infrastructure improvements 26 7 Prioritisation, integration and next steps 30 Appendicies Appendix A Summary of Relevant Policy and Guidance 32 Appendix B Cycle Route Network Plans 36 Appendix C Eastern Area Cycle Routes 39 – Audit Key Findings and Recommended Improvements Appendix D Newbury and Thatcham Prioritised 42 Strategic Cycle Routes – Audit Key Findings and Recommended Improvements Appendix E Newbury and Thatcham 69 Key Walking Route Network Plan Appendix F Newbury and Thatcham Prioritised 70 Key Walking Routes – Audit Key Findings and Recommended Improvements 2 LCWIP Foreword West Berkshire Council is pleased to present our district. This joined-up approach covered our Local Cycling and Walking Infrastructure cross-boundary routes and commuter zones on Plan (LCWIP) to act as a blueprint for future the urban fringe of Reading. We have adopted active travel routes in our district. It sets our a similar approach identifying walking and ambition to create a network of high-quality cycling routes in the settlements of Newbury interconnected cycle routes and walking zones and Thatcham and this report will prioritise the to encourage greater uptake of sustainable improvements of both urban areas together in travel modes. a comprehensive strategy for investment. By adopting the long-term approach provided The LCWIP has focused on identifying key by the LCWIP we can ensure that planning corridors connecting residential areas (both policy, public health, highway improvements, existing and proposed) to destinations such regeneration and developments are better as town centres, local centres, schools, linked to a coherent strategy that will employment sites and transport hubs. -

The Prime Minister's Holocaust Commission Report

Britain’s Promise to Remember The Prime Minister’s Holocaust Commission Report Britain’s Promise to Remember The Prime Minister’s Holocaust Commission Report January 2015 2 Britain’s Promise to Remember The Prime Minister’s Holocaust Commission Report Front cover image: Copyright John McAslan and Partners © Crown copyright 2015 You may re-use this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. Visit www.nationalarchives.gov.uk/doc/open-government-licence, write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected]. This publication is available from www.gov.uk Any enquiries regarding this publication should be sent to: Cabinet Office 70 Whitehall London SW1A 2AS Tel: 020 7276 1234 If you require this publication in an alternative format, email [email protected] or call 020 7276 1234. Contents 3 CONTENTS Foreword 5 Executive Summary 9 Introduction 19 Holocaust Education and Commemoration Today 25 Findings 33 Recommendations 41 Delivery and Next Steps 53 Appendix A Commissioners and Expert Group Members 61 Appendix B Acknowledgements 62 4 Prime Minister’s Holocaust Commission – Summary of evidence Foreword 5 FOREWORD At the first meeting of the Holocaust Commission exactly one year ago, the Prime Minister, David Cameron, set out the task for the Commission. In response, one of my fellow Commissioners, Chief Rabbi Ephraim Mirvis, noted that the work of this Commission was a sacred duty to the memory of both victims and survivors of the Holocaust. One year on, having concluded its work in presenting this report, I believe that the Commission has fulfilled that duty and has provided a set of recommendations which will give effect to an appropriate and compelling memorial to the victims of the Holocaust and to all of those who were persecuted by the Nazis. -

Page9-National.Qxd (Page 1)

DAILY EXCELSIOR, JAMMU MONDAY, MAY 18, 2020 (PAGE 9) Rajdhani specials carry nearly Decentralisation of cities can help address Govt’s economic package to go a long way 3.5 lakh passengers in 5 days migrant workers' woes: Gadkari in making India self-reliant: Amit Shah NEW DELHI, May 17: NEW DELHI, May 17: model for other parts of the coun- NEW DELHI, May 17: Disaster Response Funds to the try and can arrest mass exodus of tune of Rs 11,000 crore. Rajdhani Specials carried nearly 3.5 lakh passengers in last five Union Home Minister Amit Finance Minister Nirmala days, generating a revenue of over Rs 69 crore for Indian At a time when the trauma of workers in search of "greener pas- migrant workers are coming to tures". Shah on Sunday said the Sitharaman on Sunday Railways, said officials. the fore amid the coronavirus- "In Maharashtra's Dharavi announcement of the fifth and announced plans to privatise The Rajdhani Special train service started by the national carri- induced lockdown, Union minis- 1.5 lakh people depend on final tranche of an economic PSUs in non-strategic sectors er on May 12 to ferry stranded people between Delhi and other ter Nitin Gadkari has said "decen- leather work....The upcoming package by the Modi govern- and suspend loan default-trig- major cities of the country has seen a major demand from the mid- tralisation of cities" and develop- Delhi-Mumai Expressway goes ment will go a long way in real- gered bankruptcy filings for one dle class with most of them running on full capacity. -

2A Brummell Road, Speen, Newbury, Berkshire, Rg14

2A BRUMMELL ROAD, SPEEN, NEWBURY, BERKSHIRE, RG14 1TN 2A Brummell Road Guide Price £525,000 Speen, Newbury, Berkshire, RG14 1TN Approximately 1/2 mile to Newbury Town Centre Approximately 1 1/2 miles to Newbury Railway Station with Links to London Paddington (approximately 1 Hour) and the West Country Detached Freehold Chalet Style House Open Plan Living/Dining Room Kitchen Three Bedrooms (Two on Ground Floor) Mezzanine Room Store Room En-Suite Wet Room/Bathroom Main Bathroom Shower Room Garage Gas Central Heating Low Maintenance Garden Situation The property is located in a sought after residential area approximately 1/2 a mile from Newbury Town Centre. Newbury is a pretty market town well renowned for its racecourse, situated on the banks of the River Kennet. The Kennet and Avon canal runs through the town. The town centre itself has a range of national and independent retailers, supermarkets, restaurants, a weekly market and the Corn Exchange, which has regular plays and concerts. Both the town centre and surrounding countryside offer a wide range of leisure and sporting facilities. Newbury is superbly situated approximately an hour by road from London and Bristol on junction 13 of the M4. Approximately 45 minutes from both Oxford and Southampton on the A34. Newbury also has a mainline railway station with fast trains to London (Paddington) in approximately 60 minutes. The Property This outstanding detached home offers modern open plan living accommodation with the added flexibility of both ground floor and first floor Bedrooms. The property is presented for Sale in first class order and has been comprehensively improved and upgraded in recent years including some clever upgrades for persons with limited mobility. -

The Sunday Times Rich List 2008 Top 150

The Sunday Times Rich List 2008 Top 150 Return here from 2pm on Tuesday, April 29 to see full interactive table of Britain’s richest 2,000 Rank 2007 Rank Name Worth Source of wealth 1 1 Lakshmi Mittal and family £27,700m Steel 2 2 Roman Abramovich £11,700m Oil 3 3 The Duke of Westminster £7,000m Property 4 4 Sri and Gopi Hinduja £6,200m Industry 5 Alisher Usmanov £5,726m Steel 6 Ernesto and Kirsty Bertarelli £5,650m Pharmaceuticals 7 6 Hans Rausing and family £5,400m Packaging 8 8 John Fredriksen £4,650m Shipping 9 7 Sir Philip and Lady Green £4,330m Retailing 10 9 David and Simon Reuben £4,300m Property 11 Leonard Blavatnik £3,974m Industry 12 12= Sean Quinn and family £3,730m Property 13 12= Charlene and Michel de Carvalho £3,630m Inheritance 14 15 Kirsten and Jorn Rausing £3,500m Inheritance 15 Sammy and Eyal Ofer £3,336m Shipping 16 19 Vladimir Kim £2,987m Mining 17 17 Earl Cadogan and family £2,930m Property 18 Nicky Oppenheimer £2,870m Diamonds 19 16 Joe Lewis £2,800m Foreign exchange 20 11 Sir Richard Branson £2,700m Transport 21= 5 David Khalili £2,500m Art 21= Lev Leviev £2,500m Property 23 42 Anil Agarwal £2,450m Mining 24 20 Bernie and Slavica Ecclestone £2,400m Motor racing 25 10 Jim Ratcliffe £2,300m Chemicals 26 21 Mahdi al-Tajir £2,200m Metals 27 18 Nadhmi Auchi £2,150m Finance 28 51= Alan Parker £2,086m Duty-free shopping 29 23 Thor Bjorgolfsson £2,070m Pharmaceuticals 30 Mikhail Gutseriyev £2,015m Industry 31= 36= Laurence Graff £2,000m Diamonds 31= 14 Simon Halabi £2,000m Property 31= 24 Poju Zabludowicz £2,000m Property -

Introduction Model

WELCOME Grainger plc, one of the UK’s leading residential property companies and the UK’s largest listed residential landlord, has been selected by Network Rail and West Berkshire Council to develop the site. Located between the railway station and Market Street the site includes the existing bus station and council car park. Grainger has appointed a team of consultants to look at various technical aspects of the site. As part of this team, architects and masterplanners John Thompson & Partners (JTP) is working with the local community to create a Vision for the ‘urban village’ and its relationship with the town centre. This process began with a Community Planning Weekend, held in July 2015, when it was decided to establish the Market Street, Newbury Community Forum. This exhibition has been prepared for the first Community Forum. This event is an opportunity to see and discuss the latest proposals, including a new physical Introduction model. Our ideas continue to develop, so we welcome your feedback on the proposals presented here. Team members are on hand to discuss your ideas, experience and comments; feedback forms are also available. Supplementary Planning Document Adopted 9 June 2005 Market Street Urban Village, Newbury: Planning and Design Brief Defining the Site 2.12 The site offers a major opportunity to ‘fix’ the missing link between the station gateway and the town centre, to improve the 2.09 The site boundary for the planning and design brief is identified in interface between Market Street and the Kennet Shopping Centre Figure 3 and covers approximately 8 hectares. The Market Street and the wider quarters framework identified in the Newbury 2025 PLANNING CONTEXT site is located in the southern part of the town centre, between Vision. -

2017 West Berkshire Council

West Berkshire Council 2017 Air Quality Annual Status Report (ASR) In fulfilment of Part IV of the Environment Act 1995 Local Air Quality Management August 2017 LAQM Annual Status Report 2017 West Berkshire Council Local Authority Suzanne McLaughlin Officer Public Protection Partnership Department (Environmental Quality Team) West Berkshire Council, Market Street, Address Newbury, Berkshire, RG14 5LD Telephone 01635 503242 E-mail [email protected] Report Reference WBASR 2017 number Date August 2017 LAQM Annual Status Report 2017 West Berkshire Council Executive Summary: Air Quality in Our Area Air Quality in West Berkshire Air pollution is associated with a number of adverse health impacts. It is recognised as a contributing factor in the onset of heart disease and cancer. Additionally, air pollution particularly affects the most vulnerable in society: children and older people, and those with heart and lung conditions. There is also often a strong correlation with equalities issues, because areas with poor air quality are also often the less affluent areas1,2. The annual health cost to society of the impacts of particulate matter alone in the UK is estimated to be around £16 billion3. Nitrogen dioxide (NO2) is the main pollutant of concern. The levels in 2016 have shown general increase on 2015 levels. There was an exceedance of the ratified 3 continuous monitiored NO2 annual mean in 2016. The level was 41.7 µg/m so did exceed the Air Quality objective level of 40 µg/m3 . There were 21 exceedances of the 1-hour objective. This exceeded the objective permitted level of 18 exceedances. For 2016 the ratified and adjusted diffusion tubes annual mean levels did show levels above the objective at 6 locations (7 tubes) . -

Entrepreneurship in the UK

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Blanchflower, David G.; Shadforth, Chris Working Paper Entrepreneurship in the UK IZA Discussion Papers, No. 2818 Provided in Cooperation with: IZA – Institute of Labor Economics Suggested Citation: Blanchflower, David G.; Shadforth, Chris (2007) : Entrepreneurship in the UK, IZA Discussion Papers, No. 2818, Institute for the Study of Labor (IZA), Bonn, http://nbn-resolving.de/urn:nbn:de:101:1-20080401126 This Version is available at: http://hdl.handle.net/10419/34524 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu IZA DP No. 2818 Entrepreneurship in the UK David G. Blanchflower Chris Shadforth DISCUSSION PAPER SERIES DISCUSSION PAPER May 2007 Forschungsinstitut zur Zukunft der Arbeit Institute for the Study of Labor Entrepreneurship in the UK David G. -

125488 Nephrite Prospectus Intro.Qxp

THIS DOCUMENT AND ANY ACCOMPANYING DOCUMENTS ARE IMPORTANT AND REQUIRE YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take, you are recommended to seek immediately your own personal financial advice from your stockbroker, bank manager, solicitor, accountant, fund manager or other appropriate independent financial adviser, who is authorised under the Financial Services and Markets Act 2000 (“FSMA”) if you are in the United Kingdom or, if not, from another appropriately authorised independent financial adviser. If you sell or have sold or otherwise transferred all of your Existing Shares (other than ex-rights) before 14 January 2010 (the “Ex-Rights Date”), please send this document, together with any Provisional Allotment Letter, duly renounced, if and when received, at once to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for delivery to the purchaser or transferee except that such documents should not be sent to any jurisdiction where to do so might constitute a violation of local securities laws or regulations, including but not limited to, subject to certain exceptions, the Excluded Territories. If you sell or have sold or otherwise transferred only part of your holding of Existing Shares (other than ex-rights) before the Ex-Rights Date, you should refer to the instruction regarding split applications in Part III (“Terms and Conditions of the Rights Issue”) of this document and in the Provisional Allotment Letter, if and when received. This document, which comprises a prospectus relating to the Rights Issue prepared in accordance with the Prospectus Rules, has been approved by the Financial Services Authority (the “FSA”) in accordance with Section 87A of FSMA PRA3 4.7 and made available to the public in accordance with Rule 3.2 of the Prospectus Rules.