Bankruptcy Issues Related to Foreclosure and Repossession

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brief for Petitioner

No. 19-357 IN THE Supreme Court of the United States CITY OF CHICAGO, Petitioner, v. ROBBIN L. FULTON, JASON S. HOWARD, GEORGE PEAKE, AND TIMOTHY SHANNON, Respondents. ON WRIT OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR THE SEVENTH CIRCUIT BRIEF FOR PETITIONER MARK A. FLESSNER CRAIG GOLDBLATT BENNA RUTH SOLOMON Counsel of Record MYRIAM ZRECZNY KASPER DANIELLE SPINELLI ELLEN W. MCLAUGHLIN JOEL MILLAR CITY OF CHICAGO ISLEY GOSTIN OFFICE OF CORPORATION WILMER CUTLER PICKERING COUNSEL HALE AND DORR LLP 30 N. LaSalle Street 1875 Pennsylvania Ave., NW Suite 800 Washington, DC 20006 Chicago, Illinois 60602 (202) 663-6000 (312) 744-7764 [email protected] ALLYSON M. PIERCE WILMER CUTLER PICKERING HALE AND DORR LLP 250 Greenwich Street New York, NY 10007 (212) 230-8800 QUESTION PRESENTED Whether an entity that is passively retaining pos- session of property in which a bankruptcy estate has an interest has an affirmative obligation under the Bank- ruptcy Code’s automatic stay, 11 U.S.C. § 362, to return that property to the debtor or trustee immediately up- on the filing of the bankruptcy petition. (i) PARTIES TO THE PROCEEDING Petitioner is the City of Chicago. Respondents are Robbin L. Fulton, Jason S. How- ard, George Peake and Timothy Shannon. (ii) TABLE OF CONTENTS Page QUESTION PRESENTED ............................................... i PARTIES TO THE PROCEEDING .............................. ii TABLE OF AUTHORITIES .......................................... vi INTRODUCTION ............................................................. -

Judgment Claims in Receivership Proceedings*

JUDGMENT CLAIMS IN RECEIVERSHIP PROCEEDINGS* JOHN K. BEACH Connecticuf Supreme Court of Errors In view of the importance of the subject it is unfortunate that so few of the reported cases on equitable receiverships of corporations have dealt in any comprehensive way with the principles underlying the administrating of the fund for the benefit of creditors. The result is that controversy has outstripped authoritative decision, and the subject is unsettled. To this generalization an exception must be noted in respect of the special topic of the application of current rail- way income to current expenses, before the payment of mortgage 1 indebtedness. On another disputed topic, the provability of imma.ure claims, the law, or at least the right principle of decision, has been settled, by the notable opinion of Judge Noyes in Pennsylvania Steel Company v. New York City Railway Company,2 followed and rein- forced by that of Mr. Justice Holmes in William Filene'sSons Company v. Weed.' Notwithstanding these important exceptions, the dearth of authority on the general subject is such that Judge Noyes refers to a case cited in his opinion as "almost the only case in which rules have "been formulated with respect to the provability of claims against "insolvent corporations."4 Upon the particular phase of the subject here discussed, the decisions are to some extent in conflict, and no attempt seems to have been made in text books or decisions to examine the question in the light of principle. Black, for example, dismisses the subject by saying it. is generally conceded that a receiver and the corporation whose property is under his charge "are so far in privity that a judgment against the * This paper deals only with judgments against the defendant in the receiver- ship, regarded as evidence of the validity and amount of the judgment creditor's claims for dividends to be paid out of the fund in the receiver's hands. -

IAC Ch 34, P.1 701—34.17(321,423) Repossession of a Vehicle. A

IAC Ch 34, p.1 701—34.17(321,423) Repossession of a vehicle. A vehicle may be taken from a purchaser by the holder of the security interest in the vehicle or someone acting on the holder’s interest, if the purchaser defaults on the terms of the purchase agreement. To be recognized as valid for use tax purposes, the repossession must be regulated under the terms of the Uniform Commercial Code and there must be a valid lien on the title of the vehicle. To be recognized as valid for use tax purposes, repossession of a vehicle can be made by dealers, by financial institutions, and by individuals. The taxable result of repossession depends on the identity of the person doing the repossessing and the manner in which the person doing the repossessing conducts the transaction. 34.17(1) Licensed vehicle dealer. If a licensed vehicle dealer repossesses a vehicle and anticipates reselling the vehicle, then the dealer can use the dealer’s resale exemption, and no use tax is due at the time of the registration of the vehicle by the dealer. 34.17(2) Financial institution or private individual. A financial institution or a private individual may be a licensed dealer entitled to receive an exemption from use tax based on the dealer’s license when registering a repossessed vehicle. Repossessions of vehicles that will be resold by a financial institution or an individual that does not have a dealer’s license can be effectuated using a foreclosure affidavit. Use tax liabilities which arise as a result of such affidavits are as follows: a. -

Self-Represented Creditor

UNITED STATES BANKRUPTCY COURT DISTRICT OF MASSACHUSETTS A GUIDE FOR THE SELF-REPRESENTED CREDITOR IN A BANKRUPTCY CASE June 2014 Table of Contents Subject Page Number Legal Authority, Statutes and Rules ....................................................................................... 1 Who is a Creditor? .......................................................................................................................... 1 Overview of the Bankruptcy Process from the Creditor’s Perspective ................... 2 A Creditor’s Objections When a Person Files a Bankruptcy Petition ....................... 3 Limited Stay/No Stay ..................................................................................................... 3 Relief from Stay ................................................................................................................ 4 Violations of the Stay ...................................................................................................... 4 Discharge ............................................................................................................................. 4 Working with Professionals ....................................................................................................... 4 Attorneys ............................................................................................................................. 4 Pro se ................................................................................................................................................. -

Consumer Guide to Vehicle Repossession

REQUIREMENTS FOR DOING REINSTATING A VEHICLE BUSINESS CONTRACT AFTER REPOSSESSION Repossession agencies and their employees must be The Bureau has no jurisdiction over whether or not licensed by the Bureau of Security and Investigative the vehicle’s legal owner will reinstate your contract. Services (Bureau or BSIS) to engage in business or If you obtain a reinstatement, you will need to accept employment to locate or recover vehicles that provide the repossession agency a release from are subject to a security agreement.2 the legal owner stating that you may redeem your vehicle and proof of having paid the administrative Note: In some cases, a bank, financial lender, or filing fee to the police or sheriff’s office, where the other legal owner will send their own employees to repossession was reported.8 recover the vehicle. Individuals employed directly by a bank, lender, or the legal owner of the vehicle are Please note that in some cases you may not get your not required to be licensed as repossession agency vehicle back after it has been repossessed. employees.3 HOW REPOSSESSIONS WORK When a person has violated a condition(s) of the lease CONSUMER or loan agreement (e.g. being past due on the vehicle loan or lease payments, failure to maintain insurance, etc.), and efforts to correct the violation fail, the GUIDE TO bank, financial lender, legal owner or their agents can contract with repossession agencies to locate 1 and repossess the vehicle subject to the security VEHICLE agreement that contains the repossession clause. Many of the activities carried out before, during, and REPOSSESSION after the repossession are regulated by State and federal laws. -

Failure to Pay Rent - Landlord's Complaint for Repossession of Rented Property Real Property §8-401 1

DISTRICT COURT OF MARYLAND FOR No. of tenants 1 2 3 4 Located at CASE NUMBER TRIAL DATE & TIME Affixed on Premises Landlord Address Date City State Zip Mailed to Tenant 1 Tenant 2 Tenant 3 Tenant 4 Tenant Constable/Sheriff Address Served on Party: City State Zip Date Date FAILURE TO PAY RENT - LANDLORD'S COMPLAINT FOR REPOSSESSION OF RENTED PROPERTY REAL PROPERTY §8-401 1. The property is described as: , Maryland. Property Name Number Street Apt. City 2. Is the Landlord required by law to be licensed/registered in order to operate this premises as a rental property? Yes No. If so, is the Landlord currently licensed/registered Yes No. License/Registration number if applicable: 3. The property: is affected property under §6-801, Environment Article, its registration with the MDE is current and its registration has been renewed as required, and its MDE inspection certificate numbered , is valid for the current tenancy; or Inspection Certificate No. owner is unable to state Certificate No. because property is exempt tenant refused access or to relocate/vacate during remedial work. The property is not affected. 4. The Tenant rents from the Landlord who asks for possession of the property and a judgment for the amount determined to be due. 5. This is is not a government subsidized tenancy. Tenant is responsible to pay the following amount of rent: $ due on $ the of the week month, which has not been paid or reduced to judgment. As of today, rent is due for the weeks months of in the total amount of $ less Tenant payments of $ ( ) for utility bills, fees, and security deposits under PU §7-309 $ Net Rent Late charges accruing in or prior to the month in which the complaint was filed for the weeks months of are due in the amount of .................................................................... -

What a Creditor Needs to Know About Liquidating an Insolvent BVI Company

What a creditor needs to know about liquidating GUIDE an insolvent BVI company Last reviewed: October 2020 Contents Introduction 3 When is a company insolvent? 3 What is a statutory demand? 3 Written request for payment 3 Is it essential to serve a statutory demand? 3 What must a statutory demand say? 3 Setting aside a statutory demand 4 How may a company be put into liquidation? 4 Qualifying resolution 4 Appointment 4 Liquidator's powers 4 Court order 5 Who may apply? 5 Application 5 Debt should be undisputed 5 When does a company's liquidation start? 5 What are the consequences of a company being put into liquidation? 5 Assets do not vest in liquidator 5 Automatic consequences 5 Restriction on execution and attachment 6 Public documents 6 Other consequences 6 Effect on contracts 6 How do creditors claim in a company's liquidation? 7 Making a claim 7 Currency 7 Contingent debts 7 Interest 7 Admitting or rejecting claims 7 What is a creditors' committee? 7 Establishing the committee 7 2021934/79051506/1 BVI | CAYMAN ISLANDS | GUERNSEY | HONG KONG | JERSEY | LONDON mourant.com Functions 7 Powers 8 What is the order of distribution of the company's assets? 8 Pari passu principle 8 Excluded assets 8 Order of application 8 How are secured creditors affected by a company's liquidation? 8 General position 8 Liquidator challenge 8 Claiming in the liquidation 8 Who are preferential creditors? 9 Preferential creditors 9 Priority 9 What are the claims of current and past shareholders? 9 Do shareholders have to contribute towards the company's debts? -

Repossession and Foreclosure of Aircraft from the Perspective of the Federal Aviation Act and the Uniform Commercial Code John I

Journal of Air Law and Commerce Volume 65 | Issue 4 Article 3 2000 Repossession and Foreclosure of Aircraft from the Perspective of the Federal Aviation Act and the Uniform Commercial Code John I. Karesh Follow this and additional works at: https://scholar.smu.edu/jalc Recommended Citation John I. Karesh, Repossession and Foreclosure of Aircraft ofr m the Perspective of the Federal Aviation Act and the Uniform Commercial Code, 65 J. Air L. & Com. 695 (2000) https://scholar.smu.edu/jalc/vol65/iss4/3 This Article is brought to you for free and open access by the Law Journals at SMU Scholar. It has been accepted for inclusion in Journal of Air Law and Commerce by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu. REPOSSESSION AND FORECLOSURE OF AIRCRAFT FROM THE PERSPECTIVE OF THE FEDERAL AVIATION ACT AND THE UNIFORM COMMERCIAL CODE JOHN I. KARESH* I. INTRODUCTION T HIS ARTICLE will discuss the repossession and foreclosure of an aircraft by a secured party in the context of Article 9 of the Uniform Commercial Code ("UCC"), and the applicable provisions of the Federal Aviation Act' (the "Transportation Code"). This article will also analyze the standard Certificate of Repossession form adopted and formerly approved for use by the Federal Aviation Administration ("FAA"),2 and the latest re- vision of that form,' and some procedures commonly followed by creditors who repossess in the context of Article 9 of the UCC. II. THE TRANSPORTATION CODE AND FEDERAL PRE-EMPTION Section 44103(a) (1) of the Transportation Code specifically provides that the FAA shall register aircraft and issue a certifi- cate of registration to its owner.4 Section 44107(a) of the Trans- portation Code generally provides that the FAA shall establish a system for recording conveyances that affect the following: (1) interests in civil aircraft registered in the United States; (2) leases and instruments executed for security purposes, including * John Karesh-B.A. -

UK (England and Wales)

Restructuring and Insolvency 2006/07 Country Q&A UK (England and Wales) UK (England and Wales) Lyndon Norley, Partha Kar and Graham Lane, Kirkland and Ellis International LLP www.practicallaw.com/2-202-0910 SECURITY AND PRIORITIES ■ Floating charge. A floating charge can be taken over a variety of assets (both existing and future), which fluctuate from 1. What are the most common forms of security taken in rela- day to day. It is usually taken over a debtor's whole business tion to immovable and movable property? Are any specific and undertaking. formalities required for the creation of security by compa- nies? Unlike a fixed charge, a floating charge does not attach to a particular asset, but rather "floats" above one or more assets. During this time, the debtor is free to sell or dispose of the Immovable property assets without the creditor's consent. However, if a default specified in the charge document occurs, the floating charge The most common types of security for immovable property are: will "crystallise" into a fixed charge, which attaches to and encumbers specific assets. ■ Mortgage. A legal mortgage is the main form of security interest over real property. It historically involved legal title If a floating charge over all or substantially all of a com- to a debtor's property being transferred to the creditor as pany's assets has been created before 15 September 2003, security for a claim. The debtor retained possession of the it can be enforced by appointing an administrative receiver. property, but only recovered legal ownership when it repaid On default, the administrative receiver takes control of the the secured debt in full. -

Secured Financing and Priorities Among Creditors

University of Chicago Law School Chicago Unbound Journal Articles Faculty Scholarship 1979 Secured Financing and Priorities among Creditors Anthony T. Kronman Thomas H. Jackson Follow this and additional works at: https://chicagounbound.uchicago.edu/journal_articles Part of the Law Commons Recommended Citation Anthony T. Kronman & Thomas H. Jackson, "Secured Financing and Priorities among Creditors," 88 Yale Law Journal 1143 (1979). This Article is brought to you for free and open access by the Faculty Scholarship at Chicago Unbound. It has been accepted for inclusion in Journal Articles by an authorized administrator of Chicago Unbound. For more information, please contact [email protected]. Secured Financing and Priorities Among Creditors* Thomas H. Jacksont and Anthony T. Kronmant One of the principal advantages of a secured transaction is the protection it provides against the claims of competing creditors. A creditor asserting a security interest in his debtor's property is likely to find himself in competition with a wide assortment of other claimants. For example, his security interest may be challenged by another creditor with a consensual security interest, by a creditor with a judgment or execution lien, by a creditor claiming a right to the collateral under some general statutory entitlement such as a repair- man's lien, by a seller to or a buyer from the debtor, or by the debtor's trustee in bankruptcy. To a considerable extent, the value of a security interest depends upon the degree to which it insulates the secured party from the claims of the debtor's other creditors.1 Article 9 of the Uniform Commercial Code contains detailed rules for resolving conflicts between secured creditors and various third parties-rules that tell the secured party what he must do in order to prevent his security interest from being overridden by a competing claimant, or, conversely, what a competitor must do in order to cir- cumvent an existing security interest in the debtor's property. -

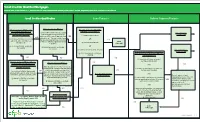

QM Small Creditor Flow Chart

SSmmaallll CCrreeddiittoorr QQuuaalliiffiieedd MMoorrttggaaggeess RReefflleeccttss rruulleess iinn eeffffeecctt oonn MMaarrcchh 11,, 22002211 bbuutt ddooeess nnoott rreefflleecctt aammeennddmmeennttss mmaaddee bbyy tthhee EEccoonnoommiicc GGrroowwtthh,, RReegguullaattoorryy RReelliieeff,, aanndd CCoonnssuummeerr PPrrootteeccttiioonn AAcctt.. Type of Compliance Presumption: SmSmaallll CCrreeddiitotorr QQuuaalliifificcaatitioonn Loan Features Balloon Payment Features Underwriting Points and Fees Portfolio Higher-Priced Loan Did you do ALL of the following?: Did you and your affiliates: Did you and your affiliates who Does the loan have ANY of the Rebuttable Presumption At the time of consummation: are creditors that extended following characteristics?: (1) Consider and verify the consumer’s YES Applies Extend 2,000 or fewer first-lien, closed- Does the loan amount fall within the following covered transactions during the Potential Small debt obligations and income or assets? STOP end residential mortgages that are points-and-fees limits? Was the loan subject to forward last calendar year have: (1) negative amortization; Creditor QM [via § 1026.43(c)(7), (e)(2)(v)]; = Non-Small Creditor QM (QM is presumed to comply subject to ATR requirements in the last YES commitment? AND YES YES = Non-Balloon-Payment QM with ATR requirements if calendar year? You can exclude loans Points-and-fees caps (adjusted annually) Assets below $2 billion (as annually OR AND it’s a higher-priced loan, but YES [§ 1026.43(e)(5)(i)(C), (f)(1)(v)] that you originated and kept in portfolio consumers can rebut the adjusted) at the end of the last STOP If Loan Amount ≥ $100,000, then = 3% of total or that your affiliate originated and kept (2) interest-only features; (2) Calculate the consumer’s monthly presumption by showing calendar year? = Non-QM If $100,000 > Loan Amount ≥ $60,000, then = $3,000 in portfolio. -

Individual Voluntary Arrangement Factsheet What Is an Individual Voluntary Arrangement (IVA)? an IVA Is a Legally Binding

Individual Voluntary Arrangement Factsheet What is an An IVA is a legally binding arrangement supervised by a Licensed Unlike debt management products, an IVA is legally binding and Individual Insolvency Practitioner, the purpose of which is to enable an precludes all creditors from taking any enforcement action against Voluntary individual, sole trader or partner (the debtor) to reach a compromise the debtor post-agreement, assuming the debtor complies with the Arrangement with his creditors and avoid the consequences of bankruptcy. The his obligations in the IVA. (IVA)? compromise should offer a larger repayment towards the creditor’s debt than could otherwise be expected were the debtor to be made bankrupt. This is often facilitated by the debtor making contributions to the arrangement from his income over a designated period or from a third party contribution or other source that would not ordinarily be available to a trustee in bankruptcy. Who can An IVA is available to all individuals, sole traders and partners who It is also often used by sole traders and partners who have suffered benefit from are experiencing creditor pressure and it is used particularly by those problems with their business but wish to secure its survival as they it? who own their own property and wish to avoid the possibility of losing believe it will be profitable in the future. It enables them to make a it in the event they were made bankrupt. greater repayment to creditors than could otherwise be expected were they made bankrupt and the business consequently were to cease trading. The procedure In theory, it is envisaged that the debtor drafts proposals for In certain circumstances, when it is considered that the debtor in brief presentation to his creditors prior to instructing a nominee, (who requires protection from creditors taking enforcement action whilst must be a Licensed Insolvency Practitioner), to review them before the IVA proposal is being considered, the nominee can file the submission to creditors (or Court if seeking an Interim Order).