Chapter 11 ) WASHINGTON PRIME GROUP INC., Et Al.,1 ) Case No

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

Copy of Chipotle Restuarant List

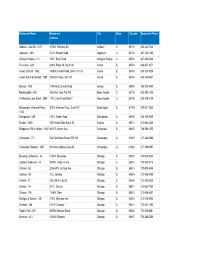

Restaurant Name Restaurant City State Zipcode Restaurant Phone Address Addison - Lake 53 - 1819 1078 N. Rohlwing Rd Addison IL 60101 630-282-7220 Algonquin - 399 412 N. Randall Road Algonquin IL 60102 847-458-1030 Arlington Heights - 131 338 E. Rand Road Arlington Heights IL 60004 847-392-8328 Fox Valley - 624 848 N. Route 59, Suite 106 Aurora IL 60504 630-851-3271 Aurora Orchard - 1462 1480 N Orchard Road, Suite 114-116 Aurora IL 60506 630-723-5004 Aurora Kirk & Butterfield - 1888 2902 Kirk Road, Unit 100 Aurora IL 60504 630-429-9437 Berwyn - 1753 7140 West Cermak Road Berwyn IL 60402 708-303-5049 Bloomingdale - 858 396 West Army Trail Rd. Bloomingdale IL 60108 630-893-2108 Fairfield and Lake Street - 2884 170 E Lake Street Suite C Bloomingdale IL 60108 630-529-5128 Bloomington Veterans Prkwy - 305 N. Veterans Pkwy., Suite 101 Bloomington IL 61704 309-661-7850 1035 Bolingbrook - 529 274 S. Weber Road Bolingbrook IL 60490 630-759-9359 Bradley - 2609 1601 Illinois State Route 50 Bradley IL 60914 815-932-3225 Bridgeview 87th & Harlem - 3047 8813 S. Harlem Ave Bridgeview IL 60455 708-598-1555 Champaign - 771 528 East Green Street, STE 101 Champaign IL 61820 217-344-0466 Champaign Prospect - 1837 903 West Anthony Drive #A Champaign IL 61820 217-398-0997 Broadway & Belmont - 36 3181 N. Broadway Chicago IL 60657 773-525-5250 Clybourn Commons - 42 2000 N. Clybourn Ave. Chicago IL 60614 773-935-5710 Orchard - 52 2256-58 N. Orchard Ave. Chicago IL 60614 773-935-6744 Jackson - 88 10 E. -

Mad River Station 2717 Miamisburg Centerville Road, Dayton, Ohio 45459

MAD RIVER STATION 2717 MIAMISBURG CENTERVILLE ROAD, DAYTON, OHIO 45459 Mad River Station benefits from its strong location at the intersection of State Route 725 and Mad River Road. The property is adjacent to the Dayton Mall, a 1.3 million square foot center anchored by DSW, Elder- Beerman, JCPenney, Macy’s, Old Navy and Sears. Mad River Station is in the Miami Township of Dayton, Ohio, and is part of the Dayton MSA. PROPERTY INFORMATION LEASING INFORMATION Type Community Shopping Center JOHN MCMAHON GLA 157,742 +/- SF [email protected] Parking 700 Spaces 914.288.3311 Anchors Office Depot, Pier 1 Imports, Barnes & Noble (not owned) 411 Theodore Fremd Ave Suite 300 Rye, NY 10580 MAD RIVER STATION 2717 MIAMISBURG CENTERVILLE ROAD, DAYTON, OHIO 45459 AVAILABLE SPACES LEASED SPACES NOT OWNED AMAR INDIAN RESTAURANT AVAILABLE AVAILABLE ZONE AVAILABLE 1 2 AVAILABLE EYE-MART 3 TENNIS AVAILABLE 4 AVAILABLE AVAILABLE 5 6 7 8 9 10 11 12 AVAILABLE 17 15 18 MONUMENT SIGN AVAILABLE 13 14 MAD RIVER RD (Not Owned) PYLON 16 MIAMISBURG CENTERVILLE RD KEY TENANT ROSTER 1. Amar LEASEDIndian RestaurantAVAILABLE ............................. 6,696 sf 7. Tennis Zone ................................................. 3,014sf 13. Available ................................................. 10,111 sf 2. Available .....................................................N 1,512 sf 8. Available ..................................................... 3,922 sf 14. Starbucks ................................................. 2,289 sf 3. Available .................................................... -

Miami Township Montgomery County, Ohio Strategic Plan

Miami Township Montgomery County, Ohio Strategic Plan Updated 2017 1 Table of Contents Mission Statement ………………………………………………………….3 Introduction of Miami Township.............................................................4 2017 Priorities of Miami Township Elected Officials ………….….……..7 Miami Township Parks ……………………………………….…….7 Miami Township Staffing ………………………………………......8 Branding and Public Image ………………………………………..8 Economic Development and Blighted/Aging Areas……….……..9 Communications …………….……………………………………..10 Infrastructure………………………………………………………...11 Administration Department ……………………………………………..…12 Community Development Department……………………………….…..15 Information Technology Department….................................................20 Compliance Department …...................................................................23 Finance Department ………………………………………….…………....26 Police Department ………………………………………………………….28 Public Works Department…………………………….…………………....31 Miami Valley Fire District…………………………………………………...35 Conclusion…………………………………………………………………...36 2 Mission Statement Miami Township’s Mission is to provide excellent services to our residents and businesses, emphasizing integrity, efficiency and fiscal responsibility, positioning the township for future growth and continued success. 3 INTRODUCTION OF MIAMI TOWNSHIP Who We Are: Miami Township, Montgomery County, is the seventh largest township in the State of Ohio with an unincorporated population of 29,131. It is both rural and urban with the convenience of city life and the openness -

Simon Property Group, Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2007 SIMON PROPERTY GROUP, INC. (Exact name of registrant as specified in its charter) Delaware 001-14469 04-6268599 (State or other jurisdiction of (Commission File No.) (I.R.S. Employer incorporation or organization) Identification No.) 225 West Washington Street Indianapolis, Indiana 46204 (Address of principal executive offices) (ZIP Code) (317) 636-1600 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12 (b) of the Act: Name of each exchange Title of each class on which registered Common stock, $0.0001 par value New York Stock Exchange 6% Series I Convertible Perpetual Preferred Stock, $0.0001 par value New York Stock Exchange 83⁄8% Series J Cumulative Redeemable Preferred Stock, $0.0001 par value New York Stock Exchange Securities registered pursuant to Section 12 (g) of the Act: None Indicate by check mark if the Registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act). Yes ፤ No អ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes អ No ፤ Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

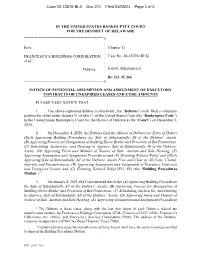

FRANCESCA's HOLDINGS CORPORATION, Et Al.,1

Case 20-13076-BLS Doc 288 Filed 01/08/21 Page 1 of 8 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE In re: Chapter 11 Case No. 20-13076 (BLS) FRANCESCA’S HOLDINGS 1 CORPORATION, et al., (Jointly Administered) Debtors. Hearing Date: February 18, 2021 at 10:00 a.m. (ET) Objection Deadline: January 22, 2021 at 4:00 p.m. (ET) APPLICATION FOR ENTRY FOR AN ORDER PURSUANT TO 11 U.S.C. §§ 328(a) AND 1103 AUTHORIZING AND APPROVING THE EMPLOYMENT OF PROVINCE, LLC AS FINANCIAL ADVISOR TO THE OFFICIAL COMMITTEE OF UNSECURED CREDITORS NUNC PRO TUNC TO DECEMBER 14, 2020 The Official Committee of Unsecured Creditors (the “Committee”) of the above-captioned debtors and debtors-in-possession (collectively, the “Debtors”) hereby files this application (the “Application”) for entry of an order, substantially in the form attached hereto as Exhibit A, pursuant to sections 328(a) and 1103(a) of title 11 of the United States Code (the “Bankruptcy Code”), Rule 2014 of the Federal Rules of Bankruptcy Procedure (the “Bankruptcy Rules”), and Rule 2014-1 of the Local Rules of Bankruptcy Practice and Procedure of the United States Bankruptcy Court for the District of Delaware (the “Local Rules”) authorizing and approving the employment of Province, LLC (f/k/a Province, Inc.) (“Province” or the “Firm”) as financial advisor to the Committee in connection with the Debtors’ chapter 11 cases, effective as of December 14, 2020. In support of the Application, the Committee also files the declaration of Edward Kim (the “Kim Declaration”), attached hereto as Exhibit B and incorporated herein by reference. -

Community Guide & Business Directory

2019-2020 Community Guide & Business Directory DISCOVER LINCOLNWOOD! LIVE • PLAY • SHOP • DINE Proud Mercedes-Benz Dealer for Six Decades Pictured Left to Right: George Loeber, Executive Vice-President; Michael Loeber, President. PROUDL Y SER experience MA VING THE C TTERS! OMMUNITY F OR O VER 25 YEARS Proud Mercedes-Benz Dealer for Six Decades DISCOVER a senior living community you’ll love today and all your tomorrows. Pictured Left to Right: George Loeber, Executive Vice-President; Michael Loeber, President. Open the door to luxury senior living. 847-686-2888 Independent Living | Assisted Living | Skillied Nursing & Rehabilitation | Memory Care AL License #52605 | 7000 North McCormick Boulevard | Lincolnwood, IL 60712 WWW.SENIORLIFESTYLE.COM Welcome Dear Lincolnwood Chamber 4433 W. TOUHY AVE. LINCOLNWOOD, ILLINOIS 60712 Partners & Friends: We are pleased to present the new edition of the Lincolnwood WHAT’S INSIDE THE GUIDE Chamber of Commerce 2019-2020 Community Resource Guide. This complimentary, hand-delivered publication connects you to WELCOME 4 the center of the Village of Lincolnwood. FROM THE OFFICE OF THE 6 MAYOR At your fingertips is contact information for various business ABOUT THE CHAMBER & CHAMBER BOARD members of the Chamber, as well as easy access to useful OF DIRECTORS 8 information assembled from numerous community HELPFUL NUMBERS 10 stakeholders including the Chamber of Commerce, the Village of Lincolnwood, the Lincolnwood Public Library, Oakton LINCOLNWOOD IS ABOUT LOCATION 12 Community College, School District 74 and Niles Township High HISTORY 14 School District 219. PARKS & RECREATION 16 More than 5,000 copies are delivered door-to-door with an additional 1,000 copies distributed throughout the year via LINCOLNWOOD SCHOOL DISTRICT 74 18–19 Village Hall new resident packages, at member businesses LINCOLNWOOD MAP 20–21 and at numerous Chamber-sponsored events. -

SF/SF Science Fiction/San Francisco the Nothing Special, Sorta Weekly News Zine for the San Francisco Bay Area

SF/SF Science Fiction/San Francisco The nothing special, sorta weekly news zine for the San Francisco Bay Area. Issue 5 August 17, 2005 email: [email protected] Editor: Jack Avery TOC But since this is pretty much the same cool dude for as long as I keep reading definition of SF activity that every SF Philip K. Dick. eLOCs ............................................1-4 genzine has ever used, I think that is fair Of course, if I were to do a similar BASFA Minutes ................................. 5 enough. listing of SF events for the Sunderland Schedule........................................6-27 Do you that this higher level of area, it would pretty much be a blank piece activity is real, or is it just a perception of paper. About all I could come up with eLOCs from my end? If just my perception, I over the last month would have been the guess that would make it a reflection of midnight queue for “that book” at the local Peter Sullivan writes from Great Britain: your success in rooting out events and Ottakers bookshop (renamed “Potterkers” whatnot for the listings, so maybe you for the night). There may be an SF society Dear Jack, ought to say yes! at the local university, but even if there is, Just a quick note to thank you for the If it really is the case that San Francisco they will all be on holiday at the moment. efforts you are putting into SFSF, and to and the Bay Area generally are more “SF- So, to finish where we started, SFSF is let you know that they are appreciated, active,” I guess this just reflects the link worthwhile, even to fen like me who are far even by people (like me) who are unlikely between Science Fiction and the counter- away from the Bay Area, in that it allows to ever go to San Francisco more than culture generally. -

271 Filed 01/06/21 Page 1 of 5

Case 20-13076-BLS Doc 271 Filed 01/06/21 Page 1 of 5 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ------------------------------------------------------------ x : In re: : Chapter 11 : FRANCESCA’S HOLDINGS CORPORATION, Case No. 20-13076 (BLS) 1 : et al., : : Debtors. Jointly Administered : : Re: D.I. 45, 266 ------------------------------------------------------------ x NOTICE OF POTENTIAL ASSUMPTION AND ASSIGNMENT OF EXECUTORY CONTRACTS OR UNEXPIRED LEASES AND CURE AMOUNTS PLEASE TAKE NOTICE THAT: 1. The above-captioned debtors (collectively, the “Debtors”) each filed a voluntary petition for relief under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the District of Delaware (the “Court”) on December 3, 2020. 2. On December 4, 2020, the Debtors filed the Motion of Debtors for Entry of Orders (I)(A) Approving Bidding Procedures for Sale of Substantially All of the Debtors’ Assets, (B) Approving Process for Designation of Stalking Horse Bidder and Provision of Bid Protections, (C) Scheduling Auction for, and Hearing to Approve, Sale of Substantially All of the Debtors’ Assets, (D) Approving Form and Manner of Notices of Sale, Auction and Sale Hearing, (E) Approving Assumption and Assignment Procedures and (F) Granting Related Relief and (II)(A) Approving Sale of Substantially All of the Debtors’ Assets Free and Clear of All Liens, Claims, Interests and Encumbrances, (B) Approving Assumption and Assignment of Executory Contracts and Unexpired Leases -

Citadel Vs Clemson (9/16/1978)

Clemson University TigerPrints Football Programs Programs 1978 Citadel vs Clemson (9/16/1978) Clemson University Follow this and additional works at: https://tigerprints.clemson.edu/fball_prgms Materials in this collection may be protected by copyright law (Title 17, U.S. code). Use of these materials beyond the exceptions provided for in the Fair Use and Educational Use clauses of the U.S. Copyright Law may violate federal law. For additional rights information, please contact Kirstin O'Keefe (kokeefe [at] clemson [dot] edu) For additional information about the collections, please contact the Special Collections and Archives by phone at 864.656.3031 or via email at cuscl [at] clemson [dot] edu Recommended Citation University, Clemson, "Citadel vs Clemson (9/16/1978)" (1978). Football Programs. 131. https://tigerprints.clemson.edu/fball_prgms/131 This Book is brought to you for free and open access by the Programs at TigerPrints. It has been accepted for inclusion in Football Programs by an authorized administrator of TigerPrints. For more information, please contact [email protected]. OFFICIAL PROGRAM • MEMORIAL STADIUM • SEPTEMBER 16, 1978 vs THE CITADEL Eastern Distribution is people who know how to handle things People who can get anything at all from one place to another on the right timetable, and in perfect condition. Murphy MacLean, Vice President/Florida, and Sherry Herren, Vice President/S. C. Eastern Distribution Office Manager Dianne Moore, Sales Representative Sherry Turner, and Controller Carrol Garrett Yes, the Eastern people on Harold Segars' Greenville, S. C, and Jacksonville, Fla., distribution team get things done, whether they're arranging the same-day movement of something you want out in a hurry, or consolidating loads to save you money through lower rates. -

Store # State City Mall/Shopping Center Name Address Date

Store # State City Mall/Shopping Center Name Address Date 2918 AL ALABASTER COLONIAL PROMENADE 340 S COLONIAL DR Now Open! 2218 AL HOOVER RIVERCHASE GALLERIA 2300 RIVERCHASE GALLERIA Now Open! 219 AL MOBILE BEL AIR MALL MOBILE, AL 36606-3411 Now Open! 2840 AL MONTGOMERY EASTDALE MALL MONTGOMERY, AL 36117-2154 Now Open! 2956 AL PRATTVILLE HIGH POINT TOWN CENTER PRATTVILLE, AL 36066-6542 Now Open! 2875 AL SPANISH FORT SPANISH FORT TOWN CENTER 22500 TOWN CENTER AVE Now Open! 2869 AL TRUSSVILLE TUTWILER FARM 5060 PINNACLE SQ Now Open! 2709 AR FAYETTEVILLE NW ARKANSAS MALL 4201 N SHILOH DR Now Open! 1961 AR FORT SMITH CENTRAL MALL 5111 ROGERS AVE Now Open! 2914 AR LITTLE ROCK SHACKLEFORD CROSSING 2600 S SHACKLEFORD RD Now Open! 663 AR NORTH LITTLE ROCK MCCAIN SHOPPING CENTER 3929 MCCAIN BLVD STE 500 Now Open! 2879 AR ROGERS PINNACLE HLLS PROMDE 2202 BELLVIEW RD Now Open! 2936 AZ CASA GRANDE PROMNDE AT CASA GRANDE 1041 N PROMENADE PKWY Now Open! 157 AZ CHANDLER MILL CROSSING 2180 S GILBERT RD Now Open! 251 AZ GLENDALE ARROWHEAD TOWNE CENTER 7750 W ARROWHEAD TOWNE CENTER Now Open! 2842 AZ GOODYEAR PALM VALLEY CORNERST 13333 W MCDOWELL RD Now Open! 2940 AZ LAKE HAVASU CITY SHOPS AT LAKE HAVASU 5651 HWY 95 N Now Open! 2419 AZ MESA SUPERSTITION SPRINGS MALL 6525 E SOUTHERN AVE Now Open! 2846 AZ PHOENIX AHWATUKEE FOOTHILLS 5050 E RAY RD Now Open! 1480 AZ PHOENIX PARADISE VALLEY MALL 4510 E CACTUS RD Now Open! 2902 AZ TEMPE TEMPE MARKETPLACE 1900 E RIO SALADO PKWY STE 140 Now Open! 1130 AZ TUCSON EL CON SHOPPING CENTER 3501 E BROADWAY Now Open! 90 -

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 Gamestop Dimond Center 80

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 GameStop Dimond Center 800 East Dimond Boulevard #3-118 Anchorage AK 99515 665 1703 (907) 272-7341 GameStop Anchorage 5th Ave. Mall 320 W. 5th Ave, Suite 172 Anchorage AK 99501 665 6139 (907) 332-0000 GameStop Tikahtnu Commons 11118 N. Muldoon Rd. ste. 165 Anchorage AK 99504 665 6803 (907) 868-1688 GameStop Elmendorf AFB 5800 Westover Dr. Elmendorf AK 99506 75 1833 (907) 474-4550 GameStop Bentley Mall 32 College Rd. Fairbanks AK 99701 665 3219 (907) 456-5700 GameStop & Movies, Too Fairbanks Center 419 Merhar Avenue Suite A Fairbanks AK 99701 665 6140 (907) 357-5775 GameStop Cottonwood Creek Place 1867 E. George Parks Hwy Wasilla AK 99654 665 5601 (205) 621-3131 GameStop Colonial Promenade Alabaster 300 Colonial Prom Pkwy, #3100 Alabaster AL 35007 701 3915 (256) 233-3167 GameStop French Farm Pavillions 229 French Farm Blvd. Unit M Athens AL 35611 705 2989 (256) 538-2397 GameStop Attalia Plaza 977 Gilbert Ferry Rd. SE Attalla AL 35954 705 4115 (334) 887-0333 GameStop Colonial University Village 1627-28a Opelika Rd Auburn AL 36830 707 3917 (205) 425-4985 GameStop Colonial Promenade Tannehill 4933 Promenade Parkway, Suite 147 Bessemer AL 35022 701 1595 (205) 661-6010 GameStop Trussville S/C 5964 Chalkville Mountain Rd Birmingham AL 35235 700 3431 (205) 836-4717 GameStop Roebuck Center 9256 Parkway East, Suite C Birmingham AL 35206 700 3534 (205) 788-4035 GameStop & Movies, Too Five Pointes West S/C 2239 Bessemer Rd., Suite 14 Birmingham AL 35208 700 3693 (205) 957-2600 GameStop The Shops at Eastwood 1632 Montclair Blvd.