The Us Grocery Industry in the 2020S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Final Debriefing About Case N. 16 Amazon (State N. and Name of the Selected Company) Analyzed by Alfonso - Name –Navarro Miralles- Surname

Final debriefing about case n. 16 Amazon (state n. and name of the selected company) Analyzed by Alfonso - name –Navarro Miralles- surname Scientific articles/papers State at least n.1 scientific article/paper you selected to support your analysis and recommendations N. Title Author Journal Year, Link number 1. 17/06/2017 https://www.elconfidencial.com/tecnologia/2017-06-17/amazon-whole-foods-supermercados-amazon-go_1400807/ 2. 2/06/2020 https://r.search.yahoo.com/_ylt=AwrP4o3VEdleYUMAKhxU04lQ;_ylu=X3oDMTByZmVxM3N0BGNvbG8DaXIyBHBvcwMxBHZ0aWQDBHNlYwNzYw- -/RV=2/RE=1591312982/RO=10/RU=https%3a%2f%2flahora.gt%2famazon-coloca-sus-bonos-al-interes-mas-bajo-jamas-pagado-por-una-empresa-en-ee- uu%2f/RK=2/RS=Zx5.zD_yM_46ddGLB3MWurVI_Yw- 3. 2/04/2019 https://r.search.yahoo.com/_ylt=AwrJS5g3EtleXmwAKj9U04lQ;_ylu=X3oDMTByaW11dnNvBGNvbG8DaXIyBHBvcwMxBHZ0aWQDBHNlYwNzcg-- /RV=2/RE=1591313079/RO=10/RU=https%3a%2f%2fwww.merca20.com%2famazon-lanzo-una-agresiva-estrategia-de-mercadotecnia-en-whole- foods%2f/RK=2/RS=iypqQZFlpG12X9jM7BsXb1VPVx8- Describe the company’s strategic profile and its industry Applying the tools of analysis covered in the whole textbook, identify and evaluate the company’s strategic profile, strategic issues/problems that merit attention (and then propose, in the following section, action recommendations to resolve these issues/problems). Jeff Bezos founded the electronic commerce company Amazon in 1995, a name chosen for his taste for the Amazon River. Their service was somewhat novel to netizens, resulting in the increase in visits fastly. Only in the first month of operation, and to Bezos' own happiness, had books been sold in all corners of the United States. Months later it reached 2,000 daily visitors, a figure that would multiply abysmally in the next year. -

FIC-Prop-65-Notice-Reporter.Pdf

FIC Proposition 65 Food Notice Reporter (Current as of 9/25/2021) A B C D E F G H Date Attorney Alleged Notice General Manufacturer Product of Amended/ Additional Chemical(s) 60 day Notice Link was Case /Company Concern Withdrawn Notice Detected 1 Filed Number Sprouts VeggIe RotInI; Sprouts FruIt & GraIn https://oag.ca.gov/system/fIl Sprouts Farmers Cereal Bars; Sprouts 9/24/21 2021-02369 Lead es/prop65/notIces/2021- Market, Inc. SpInach FettucIne; 02369.pdf Sprouts StraIght Cut 2 Sweet Potato FrIes Sprouts Pasta & VeggIe https://oag.ca.gov/system/fIl Sprouts Farmers 9/24/21 2021-02370 Sauce; Sprouts VeggIe Lead es/prop65/notIces/2021- Market, Inc. 3 Power Bowl 02370.pdf Dawn Anderson, LLC; https://oag.ca.gov/system/fIl 9/24/21 2021-02371 Sprouts Farmers OhI Wholesome Bars Lead es/prop65/notIces/2021- 4 Market, Inc. 02371.pdf Brad's Raw ChIps, LLC; https://oag.ca.gov/system/fIl 9/24/21 2021-02372 Sprouts Farmers Brad's Raw ChIps Lead es/prop65/notIces/2021- 5 Market, Inc. 02372.pdf Plant Snacks, LLC; Plant Snacks Vegan https://oag.ca.gov/system/fIl 9/24/21 2021-02373 Sprouts Farmers Cheddar Cassava Root Lead es/prop65/notIces/2021- 6 Market, Inc. ChIps 02373.pdf Nature's Earthly https://oag.ca.gov/system/fIl ChoIce; Global JuIces Nature's Earthly ChoIce 9/24/21 2021-02374 Lead es/prop65/notIces/2021- and FruIts, LLC; Great Day Beet Powder 02374.pdf 7 Walmart, Inc. Freeland Foods, LLC; Go Raw OrganIc https://oag.ca.gov/system/fIl 9/24/21 2021-02375 Ralphs Grocery Sprouted Sea Salt Lead es/prop65/notIces/2021- 8 Company Sunflower Seeds 02375.pdf The CarrIngton Tea https://oag.ca.gov/system/fIl CarrIngton Farms Beet 9/24/21 2021-02376 Company, LLC; Lead es/prop65/notIces/2021- Root Powder 9 Walmart, Inc. -

Trader Joe's Vs. Whole Foods Market

MIT Students Trader Joe’s vs. Whole Foods Market: A Comparison of Operational Management 15.768 Management of Services: Concepts, Design, and Delivery 1 Grocery shopping is more diversified and evolved than ever before. Individuals across the nation have access to everything from exotic products to unique delivery services. Often, specialty stores have limited locations whereas specialty services have a limited reach. However, two retailers have expanded to hundreds of locations while adhering to unexpected market positioning for previously untargeted market segments. Whole Foods Market and Trader Joe’s have become household names while also innovating beyond regional and national traditional chains. Despite comparable size in terms of locations, each store’s growth has operated using a very different model. This document will address the various facets for both Whole Foods Market and Trader Joe’s in order to understand how each business model has won a piece of the market pie and share of wallet. Whole Foods Market Background and History In 1978, John Mackey had a vision to build a store that would meet his desire for whole, natural foods as part of the movement away from artificial, processed foods. Mackey was a college dropout, but against all odds he was able to borrow $45,000 in capital financing and open his first store for what would become Whole Foods in Austin, Texas.1 By all accounts it has been an incredible success and the most recent annual report (2009) reveals that there are 284 stores across most of the United States with a handful in Canada and Great Britain.2 2009 2008 2007 2006 Sales (000s) $8,031,620 $7,953,912 $6,591,773 $5,607,376 1 http://www.wholefoodsmarket.com/company/history.php 2 Whole Foods Market Annual Report (2009), pg. -

Whole Foods Market Unacceptable Ingredients for Food (As of March 15, 2019)

Whole Foods Market Unacceptable Ingredients for Food (as of March 15, 2019) 2,4,5-trihydroxybutyrophenone (THBP) benzoyl peroxide acesulfame-K benzyl alcohol acetoin (synthetic) beta-cyclodextrin acetone peroxides BHA (butylated hydroxyanisole) acetylated esters of mono- and diglycerides BHT (butylated hydroxytoluene) activated charcoal bleached flour advantame bromated flour aluminum ammonium sulfate brominated vegetable oil aluminum potassium sulfate burnt alum aluminum starch octenylsuccinate butylparaben aluminum sulfate caffeine (extended release) ammonium alum calcium benzoate ammonium chloride calcium bromate ammonium saccharin calcium disodium EDTA ammonium sulfate calcium peroxide apricot kernel/extract calcium propionate artificial sweeteners calcium saccharin aspartame calcium sorbate azo dyes calcium stearoyl-2-lactylate azodicarbonamide canthaxanthin bacillus subtilis DE111 caprocaprylobehenin bacteriophage preparation carmine bentonite CBD/cannabidiol benzoates certified colors benzoic acid charcoal powder benzophenone Citrus Red No. 2 Page 1 of 4 cochineal foie gras DATEM gardenia blue diacetyl (synthetic) GMP dimethyl Silicone gold/gold leaf dimethylpolysiloxane heptylparaben dioctyl sodium sulfosuccinate (DSS) hexa-, hepta- and octa-esters of sucrose disodium 5'-ribonucleotides high-fructose corn syrup/HFCS disodium calcium EDTA hjijiki disodium dihydrogen EDTA hydrogenated oils disodium EDTA inosine monophosphate disodium guanylate insect Flour disodium inosinate iron oxide dodecyl gallate kava/kava kava EDTA lactic acid esters of monoglycerides erythrosine lactylated esters of mono- and diglycerides ethoxyquin ma huang ethyl acrylate (synthetic) methyl silicon ethyl vanillin (synthetic) methylparaben ethylene glycol microparticularized whey protein derived fat substitute ethylene oxide monoammonium glutamate eugenyl methyl ether (synthetic) monopotassium glutamate FD&C Blue No. 1 monosodium glutamate FD&C Blue No. 2 myrcene (synthetic) FD&C Colors natamycin (okay in cheese-rind wax) FD&C Green No. -

Update on How Whole Foods Market Is Responding to COVID-19 March 13, 2020

Update on How Whole Foods Market Is Responding to COVID-19 March 13, 2020 LEADERSHIP MESSAGE The following message was posted on behalf of the E-Team. Dear Team Members, As we continue to closely monitor the COVID-19 situation and respond in real-time, we wanted to call your attention to the communication below, which has also been posted on our website for customers and external stakeholders. We are pleased to share an update on funding for Team Members who may be impacted by COVID- 19 and in need of additional support. Our parent company, Amazon, has matched Team Members’ generous contributions to the Team Member Emergency Fund (TMEF) with an additional $1.617M. In support of our Shared Fate Leadership Principle, these funds will help ease the burden on Team Members who need critical support for themselves and their families. For more information or assistance in applying, please reach out to your Team Member Services Executive Leader or point of contact. Thank you for your continued dedication and hard work during these challenging times. Your health and wellbeing remain our top priority, and we will continue to provide updates via Innerview about the additional steps and measures we implement as the situation continues to unfold. Thank you, The E-Team X March 13, 2020 How Whole Foods Market is Responding to COVID-19 To our Whole Foods Market community and customers: We want to make sure you know what to expect when visiting our stores in the coming weeks, as well as how we’re responding to the evolving coronavirus (COVID-19) situation, both as a retailer and employer. -

Kroger: Value Trap Or Value Investment - a Deep Due Diligence Dive

Kroger: Value Trap Or Value Investment - A Deep Due Diligence Dive seekingalpha.com /article/4115509-kroger-value-trap-value-investment-deep-due-diligence-dive Chuck 10/23/2017 Walston The acquisition of Whole Foods Market, announced by Amazon ( AMZN) last June sent shockwaves through the grocery industry. 1/20 When the deal was finalized in August, Amazon announced plans to lower the prices of certain products by as much as a third. The company also hinted at additional price reductions in the future. Amazon Prime members will be given special savings and other in-store benefits once the online retail giant integrates its point of sale system into Whole Foods stories. 2/20 Analysts immediately predicted a future of widespread margin cuts across the industry. Well before Amazon's entry into stick and brick groceries, Kroger ( KR) experienced deterioration in comparable store sales. 3/20 (Source: Kroger Investor Presentation slideshow) (Source: SEC Filings via SA contributor Quad 7 Capital) Additionally, Kroger's recent results reflect gross margin compression. 4/20 (Source: SEC Filings via SA contributor Quad 7 Capital) After the takeover, Whole Foods initiated a price war. According to Reuters, prices at a Los Angeles Whole Foods store are lower on some products than comparable goods sold in a nearby Ralph's store owned by Kroger. The Threat From Amazon Research conducted by Foursquare Labs Inc. indicates the publicity surrounding Amazon's recent acquisition of Whole Foods, combined with the announcement of deep price cuts, resulted in a 25% surge in customer traffic. Not content to attack conventional grocers with their panoply of online food services and margin cuts, Amazon registered a trademark application for a meal-kit service. -

Store Name Address Zip Code

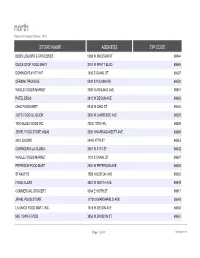

north Based on Grocery Stores - 2013 STORE NAME ADDRESS ZIP CODE BOB'S LIQUORS & GROCERIES 5069 W MADISON ST 60644 QUICK STOP FOOD MART 2751 W PRATT BLVD 60645 DOMINICK'S #147/1147 1340 S CANAL ST 60607 CERMAK PRODUCE 5220 S PULASKI RD 60632 WHOLE FOODS MARKET 3300 N ASHLAND AVE 60657 PATEL BROS 2610 W DEVON AVE 60659 OHIO FOOD MART 5345 W OHIO ST 60644 JOE'S FOOD & LIQUOR 3626 W LAWRENCE AVE 60625 TWO BLUE FOODS INC 702 E 100TH PL 60628 JEWEL FOOD STORE #3349 2520 N NARRAGANSETT AVE 60639 200 LIQUORS 204 E 47TH ST 60653 CARNICERIA LA GLORIA 2551 W 51ST ST 60632 WHOLE FOODS MARKET 1101 S CANAL ST 60607 PETERSON FOOD MART 2534 W PETERSON AVE 60659 STANLEY'S 1558 N ELSTON AVE 60622 FOOD 4 LESS 4821 W NORTH AVE 60639 COMMERCIAL GROCERY 3004 E 100TH ST 60617 JEWEL FOOD STORE 11730 S MARSHFIELD AVE 60643 LA UNICA FOOD MART, INC. 1515 W DEVON AVE 60660 MID TOWN FOODS 3855 W DIVISION ST 60651 Page 1 of 50 09/26/2021 north Based on Grocery Stores - 2013 WARD 28 50 2 23 44 50 37 39 8 36 3 14 2 50 32 37 10 34 40 27 Page 2 of 50 09/26/2021 north Based on Grocery Stores - 2013 7400 S HALSTED FOOD AND LIQUORS, INC. 7400 S HALSTED ST 60621 THREE BROTHER 900 N FRANCISCO AVE 60622 CUENCA'S BAKERY & GROCERIES 4229 W MONTROSE AVE 60641 JEWEL FOOD STORES #3262 4660 W IRVING PARK RD 60641 ROMAN BROS 1 INC 6978 N CLARK ST 60626 TAI NAM CORPORATION 4925 N BROADWAY 60640 LA JALISCIENCE 3239 W 26TH ST 60623 HOLLYWOOD TOWER MKT 5701 N SHERIDAN RD 60660 A & R FOOD MART 5952 W GRAND AVE 60639 S. -

Optionalistapril2019.Pdf

Account Number Name Address City Zip Code County Signed Affidavit Returned Affidavit Option Final Notice Sent DL20768 Vons Market 1430 S Fairfax Ave Los Angeles 90019 Los Angeles 4/28/17 OPTION A 4/19/17 DL20769 Sunshine Liquor 5677 W Pico Blvd Los Angeles 90019 Los Angeles 4/25/17 OPTION A 4/19/17 DL20771 Selam Market 5534 W Pico Blvd Los Angeles 90019 Los Angeles 4/27/17 OPTION A 4/19/17 DL61442 7-Eleven Food Store 1075 S Fairfax Ave Los Angeles 90019 Los Angeles 5/8/17 OPTION A 4/19/17 DL63467 Walgreens Drug Store 5843 W Pico Blvd Los Angeles 90019 Los Angeles 5/2/17 OPTION A 4/19/17 DL141090.001 Jordan Market 1449 Westwood Blvd Los Angeles 90024 Los Angeles 7/28/14 OPTION A 7/17/14 DL220910.001 Target 10861 Weyburn Ave Los Angeles 90024 Los Angeles 12/4/14 OPTION A DL28742 7-Eleven 1400 Westwood Blvd Los Angeles 90024 Los Angeles 3/24/15 OPTION A 7/17/14 DL28743 Tochal Mini Market 1418 Westwood Blvd Los Angeles 90024 Los Angeles 7/29/14 OPTION A 7/17/14 DL28745 Bristol Farms 1515 Westwood Blvd Los Angeles 90024 Los Angeles 12/3/14 OPTION A 7/17/14 DL41783 Stop Market 958 Gayley Ave Los Angeles 90024 Los Angeles 7/21/14 OPTION A 7/17/14 DL54515 Ralphs Fresh Fare 10861 Weyburn Ave Los Angeles 90024 Los Angeles 11/24/14 OPTION A 7/17/14 DL55831 Chevron 10984 Le Conte Ave Los Angeles 90024 Los Angeles 11/24/14 OPTION A 7/17/14 DL60416 Whole Foods Market 1050 Gayley Ave Los Angeles 90024 Los Angeles 8/7/14 OPTION A 7/17/14 DL61385 CVS/pharmacy 1001 Westwood Blvd Los Angeles 90024 Los Angeles 4/23/15 OPTION A 7/17/14 DL61953 CVS/pharmacy -

FTC V. Whole Foods Market (D.C. Cir.)

PUBLIC COPY - SEALED MATERIAL DELETED ORAL ARGUMENT NOT YET SCHEDULED No. 07-5276 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT FEDERAL TRADE COMMISSION, Plaintiff-Appellant, v. WHOLE FOODS MARKET, INC., and WILD OATS MARKETS, INC., Defendants-Appellees. Appeal from the United States District Court for the District of Columbia, Civ. No. 07-cv-Ol021-PLF PROOF BRIEF FOR APPELLANT FEDERAL TRADE COMMISSION JEFFREY SCHMIDT WILLIAM BLUMENTHAL Director General Counsel Bureau of Competition JOHN D. GRAUBERT KENNETH L. GLAZER Principal Deputy General Counsel Deputy Director JOHNF.DALY MICHAEL J. BLOOM Deputy General Counsel for Litigation Director of Litigation MARILYN E. KERST THOMAS J. LANG Attorney THOMAS H. BROCK Federal Trade Commission CATHARINE M. MOSCATELLI 600 Pennsylvania Ave., N.W. MICHAEL A. FRANCHAK Washington, D.C. 20580 JOAN L. HElM Ph. (202) 326-2158 Attorneys Fax (202) 326-2477 CERTIFICATE AS TO PARTIES, RULINGS, AND RELATED CASES Pursuant to Circuit Rule 28(1)(1), Appellant Federal Trade Commission certifies as follows: (A) PARTIES FEDERAL TRADE COMMISSION (Plaintiff) WHOLE FOODS MARKET, INC. (Defendant) WILD OATS MARKETS, INC. (Defendant) APOLLO MANAGEMENT HOLDING LP (Intervenor) DELHAIZE AMERICA. INC. (Interested Party) H.E. BUTT GROCERY COMPANY (Intervenor) KROGER CO. (Intervenor) PUBLIX SUPER MARKETS, INC. (Intervenor) SAFEWAY INC. (Intervenor) SUPERVALU INC (Intervenor) TRADER JOE'S COMPANY (Intervenor) TARGET CORPORATION (Movant) WAL-MART STORES, INC. (Intervenor) WINN-DIXIE STORES INC (Intervenor) WEGMANS FOOD MARKETS, INC. (Movant) AMICI CURIAE AMERICAN ANTITRUST INSTITUTE CONSUMER FEDERATION OF AMERICA ORGANIZATION FOR COMPETITIVE MARKETS (B) RULING UNDER REVIEW Federal Trade Commission v. Whole Foods Market, Inc., 502 F. -

Whole Foods Market: a Strategic Analysis

Whole Foods Market: A Strategic Analysis Adrienne Lee Richard Linowes Spring 2009 General University Honors 5/6/2009 1 WHOLE FOODS MARKET: Strategic Company Analysis EXECUTIVE SUMMARY Whole Foods Market, Inc . has long been admired as an innovative company with quality standards, a devotion to community and environmental responsiveness, a healthy growth model and highly-regarded employment practices . However, the company has faced recent difficulties as a result of the economic recession, increasing competition, and complications from acquisitions . To revitalize the company from historical lows in its toughest year in history, Whole Foods Market must reassess its costs, refocus its expansion strategies, and promote its brand to compete for the diminishing consumer spending dollar . During the changes in strategic initiatives, it is also important for the company to keep Whole Foods Market’s mission and its brand value intact. The chain is known for its high standards, quality, and ethical practices; this image is at stake when any changes in brand or reputation are made. It is of utmost importance to balance the positioning in order to increase awareness and sales, but at the same time avoid diminishing the brand and message of the company. Without the value behind the Whole Foods brand, the company will not survive—recession or not. If Whole Foods can successfully complete these initiatives that include major restructuring while also generating public relations buzz that coincides with its vision of quality and goodwill, the specialty food retailer will be well-positioned to experience rapid growth again when the economy turns around. COMPANY BACKGROUND Whole Foods Market, Inc . -

Discounters Go Digital: How Can Aldi and Lidl Tackle Grocery E-Commerce?

DECEMBER 8, 2016 Discounters Go Digital: How Can Aldi and Lidl Tackle Grocery E-Commerce? Hard discounters Aldi and Lidl are moving into e-commerce in both the grocery and nongrocery categories. This year, Aldi announced it will move into the Chinese market purely through e-commerce, while Lidl Germany is planning to trial a grocery click-and-collect service in Berlin. These are our key takeaways on balancing no-frills discount with the added costs of e-commerce: 1) If discounters are willing to invest to build scale in grocery e- commerce, using “dark stores” dedicated to picking online orders seems to be a better option than picking from regular stores, due to the small size of the discounters’ stores. 2) New delivery options are lowering the costs of home delivery: using “Uberized” third-party couriers would be a more cost-effective, low- investment and scalable model than using temperature controlled, company-owned delivery trucks. This model is already being used by AmazonFresh in the UK. 3) We believe one significant challenge will be the deleveraging effect of smaller average basket sizes online: the highly limited choice offered by Aldi and Lidl will almost certainly yield lower online order values than at nondiscount rivals. This would make the economics of online retail even more detrimental for discounters than they are for their nondiscount peers. DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY 1 [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved. DECEMBER 8, 2016 Introduction We are now seeing a flurry of E-Commerce and hard discount are fast-growing channels in a number of activity from discounters, markets. -

Unstoppable ALDI: Walmart's Biggest Threat?

THE NEWSLETTER FOR FOOD & BEVERAGE INDUSTRY PROFESSIONALS Unstoppable ALDI: Walmart’s Biggest Threat? ALDI continues to be the most brand-based shopper marketing), ALDI focuses the entire underestimated grocery retailer in shopping experience on a simple aggregation of cost the U.S. market. In CPG circles, it is savings, a slow and steady cartwheeling trade-down ritual easy to understand why. ALDI is a whose foundation, price leadership, has been rigidly control label retail operator, selling defended in virtually every market they’ve entered. primarily, if not entirely, their own privately branded knockoffs of The deletion of brand as a shopping variable is something established American foods. CPG that ALDI has perfected like no other store label program companies track retailers they can in the U.S. They accomplish this by simulating the color sell to, not those they can’t. scheme and front panel symbolism of their NBE- equivalent UPCs in very exacting detail. In doing so, they ALDI’s retail strategy has combined a control label trigger near instant equivalency between a name-brand, National Brand Equivalent (NBE) portfolio with an iconic, UPC and the one they are selling as a replacement. equally impressive deletion of conventional supermarket services: Examples of ALDI’s Classic Product Design Approach There are no counter service departments; everything is packaged and everything is self-service. No shelving means no stockboys to hire; product is wheeled in on pallets by forklift, unwrapped and quickly signed. 1 Carts must be paid for by deposit (25 cents) and returned by the shopper to eliminate staff needed to ALDI NBE 17oz: $1.59 (limited-time pricing) Frosted Flakes at Walmart 19oz: $3.38 (www.walmart.com) wrangle shopping carts.