Too Big to Fail US Banks' Regulatory Alchemy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LSD Modulates Music-Induced Imagery Via Changes in Parahippocampal Connectivity

European Neuropsychopharmacology (2016) 26, 1099–1109 www.elsevier.com/locate/euroneuro LSD modulates music-induced imagery via changes in parahippocampal connectivity Mendel Kaelena,n, Leor Rosemana,b, Joshua Kahanc, Andre Santos-Ribeiroa, Csaba Orbana, Romy Lorenzb, Frederick S. Barrettd, Mark Bolstridgea, Tim Williamse, Luke Williamsa, Matthew B. Walla,f,g, Amanda Feildingh, Suresh Muthukumaraswamyi, David J. Nutta, Robin Carhart-Harrisa aCentre for Neuropsychopharmacology, Division of Brain Sciences, Faculty of Medicine, Imperial College London, London W12, UK bThe Computational, Cognitive and Clinical Neuroimaging Laboratory, The Centre for Neuroscience, Division of Brain Sciences, Imperial College London, London W12, UK cSobell Department of Motor Neuroscience & Movement Disorders, Institute of Neurology, University College London, Queen Square, London WC1N 3BG, UK dBehavioral Pharmacology Research Unit, Johns Hopkins School of Medicine, Baltimore, MD 21224, USA eAcademic Unit of Psychiatry, University of Bristol, Bristol BS8 2BN, UK fImanova Centre for Imaging Sciences, Hammersmith Hospital, London W12, UK gClinical Psychopharmacology Unit, University College London, London UK hThe Beckley Foundation, Beckley Park, Oxford OX3 9SY, UK iSchools of Pharmacy and Psychology, University of Auckland, Auckland 1142, New Zealand Received 10 November 2015; received in revised form 15 February 2016; accepted 24 March 2016 KEYWORDS Abstract Effective connectiv- Psychedelic drugs such as lysergic acid diethylamide (LSD) were used extensively in psychiatry ity; in the past and their therapeutic potential is beginning to be re-examined today. Psychedelic LSD; psychotherapy typically involves a patient lying with their eyes-closed during peak drug effects, Mental imagery; while listening to music and being supervised by trained psychotherapists. In this context, music Music; is considered to be a key element in the therapeutic model; working in synergy with the drug to Parahippocampus; evoke therapeutically meaningful thoughts, emotions and imagery. -

STICK MEN - Tony Levin and Pat Mastelo�O, the Powerhouse Bass and Drums of the Group King Crimson for a Few Decades, Bring That Tradi�On to All Their Playing

STICK MEN - Tony Levin and Pat Masteloo, the powerhouse bass and drums of the group King Crimson for a few decades, bring that tradion to all their playing. Levin plays the Chapman Sck, from which the band takes it’s name. Having bass and guitar strings, the Chapman Sck funcons at mes like two instruments. Markus Reuter plays his selfdesigned touch style guitar – again covering much more ground than a guitar or a bass. And Masteloo’s drumming encompasses not just the acousc kit, but a unique electronic setup too, allowing him to add loops, samples, percussion and more. TONY LEVIN - Born in Boston, Tony Levin started out in classical music, playing bass in the Rochester Philharmonic. Then moving into jazz and rock, he has had a notable career, recording and touring with John Lennon, Pink Floyd, Yes, Alice Cooper, Gary Burton, Buddy Rich and many more. He has also released 5 solo CDs and three books. In addion to touring with Sck Men, since more than 30 years is currently a member of King Crimson and Peter Gabriel Band, and jazz bands Levin Brothers and L’Image. His popular website, tonylevin.com, featured one of the web’s first blogs, and has over 4 million visits. PAT MASTELOTTO - Very rarely does a drummer go on to forge the most successful career on the demise of their former hit band. Phil Collins and Dave Grohl have managed it, so too has Pat Masteloo, a self taught drummer from Northern California, who has also been involved with pushing the envelope of electronic drumming. -

U.S. SA-CCR Supervisory Factors for Energy Derivatives a 10% Energy SF Would Align with Forward Contract Credit Risk Evidence

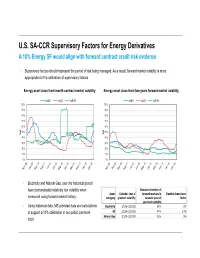

U.S. SA-CCR Supervisory Factors for Energy Derivatives A 10% Energy SF would align with forward contract credit risk evidence • Supervisory factors should represent the period of risk being managed. As a result, forward market volatility is more appropriate for the calibration of supervisory factors Energy asset class front month contract market volatility Energy asset class front two years forward market volatility VolNG VolOil VolPJM VolNG VolOil VolPJM 100% 100% 90% 90% 80% 80% 70% 70% 60% 60% 50% 50% Vol Vol 40% 40% 30% 30% 20% 20% 10% 10% 0% 0% • Electricity and Natural Gas, over the historical period have demonstrated relatively low volatility when Standard deviation of Asset Calendar year of forward markets in Implied Supervisory measured using forward market history. category greatest volatility calendar year of Factor greatest volatility • Using historical data, MS provided data and calculations Electricity 1/1/08-12/31/08 24% 6% to support a 10% calibration in our public comment Oil 1/1/08-12/31/08 47% 13% Natural Gas 1/1/09-12/31/09 32% 9% letter 1 U.S. SA-CCR Supervisory Factors for Energy Derivatives A 10% Energy SF would align with credit risk in energy derivative transactions 1. Cal18 WTI Swap Pricing: Notional BBLs x Cal18 Prices 2. Cal18 WTI MTM vs SA-CCR vs Mean Positive Exposure 150 90 Oil 1 0 /12 450 1 /10 80 1 1 100 /11 /8 1 1 350 /9 /6 70 1 1 /7 /4 1 1 50 /5 /2 60 250 1 1 /3 50 - $MM 150 $MM 40 $/BBL 50 (50) 30 20 -50 (100) 10 -150 (150) 0 Cal18 MTM SA-CCR RWA Exposure at 40% SF Cal18 MTM ($MM) Notional Quantity (BBLs) * SA-CCR RWA Exposure at 10% SF Max Mean Positive Exposure Cal18 Price ($/BBL) 1/# Spot Contribution to MTM • Energy derivative counterparty credit risk exposures decline, • A 10% Supervisory Factor correctly aligns SA-CCR month by month, as the transaction nears maturity since the credit risk measurements with other reliable counterparty remaining total notional quantity declines credit risk measures (i.e. -

Adjustable-Rate Mortgage (ARM) Is a Loan with an Interest Rate That Changes

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Board of Governors of the Federal Reserve System www.federalreserve.gov 0412 Consumer Handbook on Adjustable-Rate Mortgages | i Table of contents Mortgage shopping worksheet ...................................................... 2 What is an ARM? .................................................................................... 4 How ARMs work: the basic features .......................................... 6 Initial rate and payment ...................................................................... 6 The adjustment period ........................................................................ 6 The index ............................................................................................... 7 The margin ............................................................................................ 8 Interest-rate caps .................................................................................. 10 Payment caps ........................................................................................ 13 Types of ARMs ........................................................................................ 15 Hybrid ARMs ....................................................................................... 15 Interest-only ARMs .............................................................................. 15 Payment-option ARMs ........................................................................ 16 Consumer cautions ............................................................................. -

Managing Environmental Liabilities in Bankruptcy

I N S I D E T H E M I N D S Managing Environmental Liabilities in Bankruptcy Leading Lawyers on Identifying Environmental Risks, Implementing Emerging Risk Transfer Strategies, and Navigating Current Trends in U.S. Environmental Liability ©2010 Thomson Reuters/Aspatore All rights reserved. Printed in the United States of America. No part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, except as permitted under Sections 107 or 108 of the U.S. Copyright Act, without prior written permission of the publisher. This book is printed on acid free paper. Material in this book is for educational purposes only. This book is sold with the understanding that neither any of the authors nor the publisher is engaged in rendering legal, accounting, investment, or any other professional service. Neither the publisher nor the authors assume any liability for any errors or omissions or for how this book or its contents are used or interpreted or for any consequences resulting directly or indirectly from the use of this book. For legal advice or any other, please consult your personal lawyer or the appropriate professional. The views expressed by the individuals in this book (or the individuals on the cover) do not necessarily reflect the views shared by the companies they are employed by (or the companies mentioned in this book). The employment status and affiliations of authors with the companies referenced are subject to change. Aspatore books may be purchased for educational, business, or sales promotional use. -

World Bank Document

48165 THE WORLD BANK PRINCIPLES AND GUIDELINES FOR Public Disclosure Authorized EFFECTIVE INSOLVENCY AND CREDITOR RIGHTS SYSTEMS April 2001 Effective insolvency and creditor rights systems are an important element of financial system stability. The Bank accordingly has been working with partner organizations to develop principles on insolvency and creditor rights systems. Those principles will be used to guide system reform and benchmarking in developing countries. The Principles and Guidelines are a distillation of international Public Disclosure Authorized best practice on design aspects of these systems, emphasizing contextual, integrated solutions and the policy choices involved in developing those solutions. While the insolvency principles focus on corporate insolvency, substantial progress has been made in identifying issues relevant to developing principles for bank and systemic insolvency, areas in which the Bank and the Fund, as well as other international organizations, will continue to collaborate in the coming months. These issues are discussed in more detail in the annexes to the paper. The Principles and Guidelines will be used in a series of experimental country assessments in connection with the program to develop Reports on the Observance of Standards and Codes (ROSC), using a common template based on the principles. In addition, the Bank is collaborating with UNCITRAL and other institutions to develop a more elaborate set of implementational guidelines based Public Disclosure Authorized on the principles. If you have -

Chapman Law Review

Chapman Law Review Volume 21 Board of Editors 2017–2018 Executive Board Editor-in-Chief LAUREN K. FITZPATRICK Managing Editor RYAN W. COOPER Senior Articles Editors Production Editor SUNEETA H. ISRANI MARISSA N. HAMILTON TAYLOR A. KENDZIERSKI CLARE M. WERNET Senior Notes & Comments Editor TAYLOR B. BROWN Senior Symposium Editor CINDY PARK Senior Submissions & Online Editor ALBERTO WILCHES –––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––– Articles Editors ASHLEY C. ANDERSON KRISTEN N. KOVACICH ARLENE GALARZA STEVEN L. RIMMER NATALIE M. GAONA AMANDA M. SHAUGHNESSY-FORD ANAM A. JAVED DAMION M. YOUNG __________________________________________________________________ Staff Editors RAYMOND AUBELE AMY N. HUDACK JAMIE L. RICE CARLOS BACIO MEGAN A. LEE JAMIE L. TRAXLER HOPE C. BLAIN DANTE P. LOGIE BRANDON R. SALVATIERRA GEORGE E. BRIETIGAM DRAKE A. MIRSCH HANNAH B. STETSON KATHERINE A. BURGESS MARLENA MLYNARSKA SYDNEY L. WEST KYLEY S. CHELWICK NICHOLE N. MOVASSAGHI Faculty Advisor CELESTINE MCCONVILLE, Professor of Law CHAPMAN UNIVERSITY HAZEM H. CHEHABI ADMINISTRATION JEROME W. CWIERTNIA DALE E. FOWLER ’58 DANIELE C. STRUPPA BARRY GOLDFARB President STAN HARRELSON GAVIN S. HERBERT,JR. GLENN M. PFEIFFER WILLIAM K. HOOD Provost and Executive Vice ANDY HOROWITZ President for Academic Affairs MARK CHAPIN JOHNSON ’05 JENNIFER L. KELLER HAROLD W. HEWITT,JR. THOMAS E. MALLOY Executive Vice President and Chief SEBASTIAN PAUL MUSCO Operating Officer RICHARD MUTH (MBA ’05) JAMES J. PETERSON SHERYL A. BOURGEOIS HARRY S. RINKER Executive Vice President for JAMES B. ROSZAK University Advancement THE HONORABLE LORETTA SANCHEZ ’82 HELEN NORRIS MOHINDAR S. SANDHU Vice President and Chief RONALD M. SIMON Information Officer RONALD E. SODERLING KAREN R. WILKINSON ’69 THOMAS C. PIECHOTA DAVID W. -

Michael Grace / Tapeop Behind the Gear

was getting pretty busy at night building custom mic Behind The Gear preamps for people, so I quit working for that company This Issue’s Prince of Preamps and started out on my own. That remained a garage operation for several years until my brother Eben and I Michael Grace joined forces and became partners. We decided we by Walt Szalva wanted to start a manufacturing company and build preamps on a larger scale so we could take advantage of the economies of scale, being able to buy better components and build things that were not absolutely stressed in terms of cost. That was almost twelve years ago when we came out with the first official Grace Design product, which was the 801 preamp. What kind of problems does a small manufacturer like yourself encounter in terms of designing and building Michael Grace started Grace feedback amplifier, or a trans-impedance amp, and something that a larger manufacturer Design in 1994, a boutique pro these types of amplifiers use a different kind of might not encounter? audio company located in Boulder, negative feedback in the current domain instead of the CO. The story of his rise as a Quality control is the top issue for any manufacturing designer is one born from a love voltage domain. They are able to track really complex company. Being a boutique manufacturer, most of our of music. His need for a preamp to waveforms, resolve rich harmonic structures and track products are fairly expensive and not something that record Grateful Dead concerts transients without the various aberrations of slew rate someone just plunks down on a credit card on a whim drove him to design his first limiting and things that are associated with textbook for their studio. -

True Conservative Or Enemy of the Base?

Paul Ryan: True Conservative or Enemy of the Base? An analysis of the Relationship between the Tea Party and the GOP Elmar Frederik van Holten (s0951269) Master Thesis: North American Studies Supervisor: Dr. E.F. van de Bilt Word Count: 53.529 September January 31, 2017. 1 You created this PDF from an application that is not licensed to print to novaPDF printer (http://www.novapdf.com) Page intentionally left blank 2 You created this PDF from an application that is not licensed to print to novaPDF printer (http://www.novapdf.com) Table of Content Table of Content ………………………………………………………………………... p. 3 List of Abbreviations……………………………………………………………………. p. 5 Chapter 1: Introduction…………………………………………………………..... p. 6 Chapter 2: The Rise of the Conservative Movement……………………….. p. 16 Introduction……………………………………………………………………… p. 16 Ayn Rand, William F. Buckley and Barry Goldwater: The Reinvention of Conservatism…………………………………………….... p. 17 Nixon and the Silent Majority………………………………………………….. p. 21 Reagan’s Conservative Coalition………………………………………………. p. 22 Post-Reagan Reaganism: The Presidency of George H.W. Bush……………. p. 25 Clinton and the Gingrich Revolutionaries…………………………………….. p. 28 Chapter 3: The Early Years of a Rising Star..................................................... p. 34 Introduction……………………………………………………………………… p. 34 A Moderate District Electing a True Conservative…………………………… p. 35 Ryan’s First Year in Congress…………………………………………………. p. 38 The Rise of Compassionate Conservatism…………………………………….. p. 41 Domestic Politics under a Foreign Policy Administration……………………. p. 45 The Conservative Dream of a Tax Code Overhaul…………………………… p. 46 Privatizing Entitlements: The Fight over Welfare Reform…………………... p. 52 Leaving Office…………………………………………………………………… p. 57 Chapter 4: Understanding the Tea Party……………………………………… p. 58 Introduction……………………………………………………………………… p. 58 A three legged movement: Grassroots Tea Party organizations……………... p. 59 The Movement’s Deep Story…………………………………………………… p. -

Derivatives and Risk Management in the Petroleum, Natural Gas, and Electricity Industries

SR/SMG/2002-01 Derivatives and Risk Management in the Petroleum, Natural Gas, and Electricity Industries October 2002 Energy Information Administration U.S. Department of Energy Washington, DC 20585 This report was prepared by the Energy Information Administration, the independent statistical and analytical agency within the U.S. Department of Energy. The information contained herein should be attributed to the Energy Information Administration and should not be construed as advocating or reflecting any policy position of the Department of Energy or any other organization. Service Reports are prepared by the Energy Information Administration upon special request and are based on assumptions specified by the requester. Contacts This report was prepared by the staff of the Energy The Energy Information Administration would like to Information Administration and Gregory Kuserk of the acknowledge the indispensible help of the Commodity Commodity Futures Trading Commission. General Futures Trading Commission in the research and writ- questions regarding the report may be directed to the ing of this report. EIA’s special expertise is in energy, not project leader, Douglas R. Hale. Specific questions financial markets. The Commission assigned one of its should be directed to the following analysts: senior economists, Gregory Kuserk, to this project. He Summary, Chapters 1, 3, not only wrote sections of the report and provided data, and 5 (Prices and Electricity) he also provided the invaluable professional judgment Douglas R. Hale and perspective that can only be gained from long expe- (202/287-1723, [email protected]). rience. The EIA staff appreciated his exceptional pro- ductivity, flexibility, and good humor. -

Long-Term Swings and Seasonality in Energy Markets Working Paper Nº 1929

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by EPrints Complutense Long-term swings and seasonality in energy markets Instituto Manuel Moreno Complutense Department of Economic Analysis and Finance, University of Castilla-La Mancha, Toledo, Spain de Análisis Económico Alfonso Novales Instituto Complutense de Análisis Económico (ICAE), and Department of Economic Analysis, Facultad de Ciencias Económicas y Empresariales, Universidad Complutense, Madrid, Spain Federico Platania Léonard de Vinci Pôle Universitaire, Paris La Défense, France Abstract This paper introduces a two-factor continuous-time model for commodity pricing under the assumption that prices revert to a stochastic mean level, which shows smooth, periodic fluctuations over long periods of time. We represent the mean reversion price by a Fourier series with a stochastic component. We also consider a seasonal component in the price level, an essential characteristic of many commodity prices, which we represent again by a Fourier series. We obtain analytical pricing expressions for futures contracts. Using futures price data on Natural Gas, we provide evidence on the presence of long-term fluctuations and show how to estimate the long-term component simultaneously with a seasonal component using the Kalman filter. We analyse the in-sample and out-of-sample empirical performance of our pricing model with and without a seasonal component and compare it with the Schwartz and Smith (2000) model. Our findings show the in-sample and out-of-sample superiority of our model with seasonal fluctuations, thereby providing a simple and powerful tool for portfolio management, risk management, and derivative pricing. -

Too Big to Fail — U.S. Banks' Regulatory Alchemy

Journal of Business & Technology Law Volume 14 | Issue 2 Article 2 Too Big to Fail — U.S. Banks’ Regulatory Alchemy: Converting an Obscure Agency Footnote into an “At Will” Nullification of Dodd-Frank’s Regulation of the Multi-Trillion Dollar Financial Swaps Market Michael Greenberger Follow this and additional works at: https://digitalcommons.law.umaryland.edu/jbtl Recommended Citation Michael Greenberger, Too Big to Fail — U.S. Banks’ Regulatory Alchemy: Converting an Obscure Agency Footnote into an “At Will” Nullification of Dodd-Frank’s Regulation of the Multi-Trillion Dollar Financial Swaps Market, 14 J. Bus. & Tech. L. 197 () Available at: https://digitalcommons.law.umaryland.edu/jbtl/vol14/iss2/2 This Article is brought to you for free and open access by the Academic Journals at DigitalCommons@UM Carey Law. It has been accepted for inclusion in Journal of Business & Technology Law by an authorized editor of DigitalCommons@UM Carey Law. For more information, please contact [email protected]. Too Big to Fail—U.S. Banks’ Regulatory Alchemy: Converting an Obscure Agency Footnote into an “At Will” Nullification of Dodd-Frank’s Regulation of the Multi-Trillion Dollar Financial Swaps Market MICHAEL GREENBERGER*©1 ΎLaw School Professor, University of Maryland Carey School of Law, and Founder and Director, University of Maryland Center for Health and Homeland Security (“CHHS”); former Director, Division of Trading and Markets, U.S. Commodity Futures Trading Commission. The Institute for New Economic Thinking (“INET”) funded and published this article as a working paper on the Social Sciences Research Network on June 19, 2018 at https://www.ineteconomics.org/uploads/papers/WP_74.pdf.