Merafong – Gauteng

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Survey of Race Relations in South Africa: 1968

A survey of race relations in South Africa: 1968 http://www.aluka.org/action/showMetadata?doi=10.5555/AL.SFF.DOCUMENT.BOO19690000.042.000 Use of the Aluka digital library is subject to Aluka’s Terms and Conditions, available at http://www.aluka.org/page/about/termsConditions.jsp. By using Aluka, you agree that you have read and will abide by the Terms and Conditions. Among other things, the Terms and Conditions provide that the content in the Aluka digital library is only for personal, non-commercial use by authorized users of Aluka in connection with research, scholarship, and education. The content in the Aluka digital library is subject to copyright, with the exception of certain governmental works and very old materials that may be in the public domain under applicable law. Permission must be sought from Aluka and/or the applicable copyright holder in connection with any duplication or distribution of these materials where required by applicable law. Aluka is a not-for-profit initiative dedicated to creating and preserving a digital archive of materials about and from the developing world. For more information about Aluka, please see http://www.aluka.org A survey of race relations in South Africa: 1968 Author/Creator Horrell, Muriel Publisher South African Institute of Race Relations, Johannesburg Date 1969-01 Resource type Reports Language English Subject Coverage (spatial) South Africa, South Africa, South Africa, South Africa, South Africa, Namibia Coverage (temporal) 1968 Source EG Malherbe Library Description A survey of race -

1-35556 3-8 Padp1 Layout 1

Government Gazette Staatskoerant REPUBLIC OF SOUTH AFRICA REPUBLIEK VAN SUID-AFRIKA August Vol. 566 Pretoria, 3 2012 Augustus No. 35556 PART 1 OF 3 N.B. The Government Printing Works will not be held responsible for the quality of “Hard Copies” or “Electronic Files” submitted for publication purposes AIDS HELPLINE: 0800-0123-22 Prevention is the cure G12-088869—A 35556—1 2 No. 35556 GOVERNMENT GAZETTE, 3 AUGUST 2012 IMPORTANT NOTICE The Government Printing Works will not be held responsible for faxed documents not received due to errors on the fax machine or faxes received which are unclear or incomplete. Please be advised that an “OK” slip, received from a fax machine, will not be accepted as proof that documents were received by the GPW for printing. If documents are faxed to the GPW it will be the senderʼs respon- sibility to phone and confirm that the documents were received in good order. Furthermore the Government Printing Works will also not be held responsible for cancellations and amendments which have not been done on original documents received from clients. CONTENTS INHOUD Page Gazette Bladsy Koerant No. No. No. No. No. No. Transport, Department of Vervoer, Departement van Cross Border Road Transport Agency: Oorgrenspadvervoeragentskap aansoek- Applications for permits:.......................... permitte: .................................................. Menlyn..................................................... 3 35556 Menlyn..................................................... 3 35556 Applications concerning Operating -

The Mineral Industry of South Africa in 1999

THE MINERAL INDUSTRY OF SOUTH AFRICA By George J. Coakley Mining and downstream minerals processing remained more than $3.3 billion was committed for new projects in 2000, keystones of the economy of the Republic of South Africa in chiefly in gold and PGM, and an additional $4.9 billion was 1999. With a population of 43.4 million, South Africa had a under consideration for future investment. gross domestic product (GDP) per capita of $6,900 based on purchasing power parity estimates for 1998.1 Of total exports of Production all goods, which were valued at $28 billion, gold exports accounted for 14.1%, and other minerals and metals exports, for In 1999, South Africa was one of the largest and most diverse about an additional 28%. According to the Minerals Bureau of minerals producers in the world. As listed in table 1, changes in South Africa, the primary mining sector contributed $7.7 output levels were mixed. Gold production decreased a further billion, or 6.5%, to the GDP. Adding the multiplier effects of 3% between 1998 and 1999 as the industry continued to services and goods supplied by industries that support the rationalize production to reduce operating costs in response to mining sector would increase the contribution to GDP by the continued depressed gold price. Production of most of the another 14%. The contribution to the GDP would also be other major metals was up from 1% to 10% compared with that significantly higher if the value-added mineral-processing of 1998. Output of iron ore, lead, steel, and vanadium declined. -

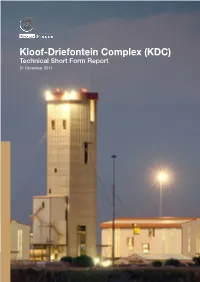

Kloof-Driefontein Complex (KDC) Technical Short Form Report 31 December 2011

Kloof-Driefontein Complex (KDC) Technical Short Form Report 31 December 2011 2 Salient features ¨ Mineral Resources at 63.8 Moz (excluding Tailing Storage Facility ounces of 3.7 Moz). ¨ Mineral Reserves at 13.7 Moz (excluding Tailing Storage Facility ounces of 2.9 Moz). ¨ Safe steady state production strategy driving quality volume. ¨ Accelerate extraction of higher grade Mineral Reserves to bring value forward. ¨ Optimise surface resources extraction strategy. ¨ Long-life franchise asset anchoring gold production to 2028 (17 years). The KDC has a world class ore body with long-life Mineral Resources and Mineral Reserves (17 years) which has produced in excess of 181 Moz from the renowned Witwatersrand Basin, the most prolific gold depository in the world. Geographic location KDC West Mining Right KDC East Mining Right Carletonville Pretoria Johannesburg Welkom Kimberley Bloemfontein Durban KDC East = Kloof G.M. Port Elizabeth KDC West = Driefontein G.M. Cape Town Gold Fields: KDC Gold Mine – Technical Short Form Report 2011 3 Geographic location IFC 1. Overview 1. Overview Page 1 Gold Fields Limited owns a 100% interest in GFI Mining South Africa (Pty) Limited (GFIMSA), which holds a 100% interest in KDC (Kloof- 2. Key aspects Page 2 Driefontein Complex). The mine is situated between 60 and 80 kilometres west of 3. Operating statistics Page 3 Johannesburg near the towns of Westonaria and Carletonville in the Gauteng Province of Page 4 South Africa. KDC is a large, well-established 4. Geological setting and mineralisation shallow to ultra-deep level gold mine with workings that are accessed through, 12 shaft 5. Mining Page 7 systems (five business units – BU’s) that mine various gold-bearing reefs from open ground 6. -

MSDF 2019 Annexure a IMPLEMENTATION

MERAFONG CITY MUNICIPAL SPATIAL DEVELOPMENT FRAMEWORK 2019 ANNEXURE A IMPLEMENTATION PLAN CAPITAL INVESTMENT FRAMEWORK The Capital Expenditure Framework (CEF) as a component of the Municipal Spatial Development Framework (MSDF) is a requirement in terms of Section 21(n) of the Spatial Planning and Land Use Management Act, 2013. The intention of the Capital Investment Framework (CIF) is to close the gap between the spatial strategy and implementation on the ground. This is to be achieved using the spatial strategy and the detail provided in the Municipal Spatial Development Framework as the basis upon which other sector plans can be built, thus ensuring integration through a shared platform. A Capital Expenditure Framework has 4 key components namely spatial alignment, quantification of growth, technical assessment and financial alignment. This is the first attempt at an improved Capital Expenditure Framework and whilst the spatial component has been completed satisfactorily, the financial and infrastructure components are not at a satisfactory level. The municipality strives to adopt the new Integrated Urban Development Grant (IUDG) and as such the infrastructure and financial components will have to be added in coming years. This attempt is seen as a base to start from and expand upon. Many of the calculations and information available has not been included and some of it, such as the human settlement calculations are included in other parts of the MSDF. The municipality has a very difficult task of balancing its budget between the needs of social development, economic development and urban efficiency. The needs of the present must also be weighed against sustainability and viability in the future. -

The Development of Appropriate Procedures Towards and After Closure of Underground Gold Mines from a Water Management Perspective

THE DEVELOPMENT OF APPROPRIATE PROCEDURES TOWARDS AND AFTER CLOSURE OF UNDERGROUND GOLD MINES FROM A WATER MANAGEMENT PERSPECTIVE Report to the WATER RESEARCH COMMISSION by W Pulles, S Banister and M van Biljon on hehalf of PULLES HOWARD & DE LANGE INCORPORATED RISON GROUNDWATER CONSULTING cc WRC Report No: 1215/1/05 ISBN No: 1-77005-237-2 MARCH 2005 Disclaimer This report emanates from a project financed by the Water Research Commission (WRC) and is approved for publication. Approval does not signify that the contents necessarily reflect the views and policies of the WRC or the members of the project steering committee, nor does mention of trade names or commercial products constitute endorsement or recommendation for use. i EXECUTIVE SUMMARY A need was identified by the Water Research Commission to undertake research into the issue of mine closure planning from a water management perspective in the South African gold mining industry. Initially a project was conceived that was based on undertaking a more detailed study on the development of a coherent and integrated closure planning process for a case study region – the Klerksdorp-Orkney-Stilfontein-Hartebeestfontein (KOSH) area. This approach was eventually abandoned due to the unwillingness of the gold mines in this region (other than Anglogold) to participate in the project. The project methodology was subsequently modified and approved by the project Steering Committee to rather study the complete South African gold mining industry and develop a closure planning methodology that would have application throughout the industry. In support of such an industry-wide study, an assessment would be undertaken of the current status of closure planning contained within the mine EMPRs. -

Westonaria SAPS in Carletonville Cluster

10 July 2009, RANDFONTEIN HERALD Page 5 Westonaria SAPS in Carletonville cluster Westonaria — Following the incor- above crimes reported in the whole poration of Merafong into Gauteng, cluster, on a weekly basis. Carletonville SAPS has now be- This team will work from the Uni- come the accountable station for all cus Building under the command of other stations in its cluster, includ- Superintendent Reginald Shabangu. ing Westonaria. "The Roadblock Task team consists The Carletonville SAPS cluster of 20 members from each of the consists of Khutsong, Fochville, station's crime prevention units and Wedela and now Westonaria police will concentrate their efforts on major station. routes such as the N12 and the Carletonville SAPS spokesman, P111." Sergeant Busi Menoe, says there will She adds that the main purpose of also be an overall commander for the this task team will be to prevent whole cluster. crimes such as house robberies, car "At this stage there is an interim hijackings and business robberies. acting cluster commander, Director "They will also be on the look-out Fred Kekana, who is based at the for stolen property and vehicles." Station Commissioner, Director Patricia Rampota, salutes Captain Richard Vrey during the Randfontein Westonaria station." Menoe says these members are di- SAPS medal parade. Menoe adds that two task teams vided into two groups under the com- have also been established to fight mand of captains Robert Maphasha crime in the whole cluster, namely the and Lot Nkoane. SAPS members honoured at parade Trio Task team and the Roadblock "The two groups will work flexi- Task team. -

TAU Industries' Prospecting Applications

MCFMagaliesburg Community Forum TAU INDUSTRIES’ PROSPECTING Applications: 1. Koesterfontein - DMR GP10498PR 2. Kaalfontein - DMR GP10505PR 3. Zuickerbosch - DMR GP10504PR MAIN MCF COMMENTRARY DOCUMENT 06 Nov 2018 REV C001 Magaliesburg Community Forum [email protected] Draft EIA/EMP Complaints and Comments // Magaliesburg Community Forum Use of this Document This document has been prepared by the MCF for the exclusive information sharing between the DMR and other state organs and decision makers to voice the concerns of the MCF’s members who form part of the Interested and Affected Parties of the three Tau Industries prospecting applications in the Magaliesburg region, which forms part of the Mogale City Local Municipality (MCLM). If there is a need to present any of this information to any other public or third party person (including the general public), a written response and approval must be obtained from the MCF prior to publication of this information, content and data, either in whole or in part. The MCF reserves the right to amend, add additional comments, and raise additional concerns or provide updates where needed and / or not captured due to the time allowed to review all of the DRAFT EIA and EAP information. These documents should not be seen as complete and as either standalone comments or concerns of the MCF, their members and all the I&AP. TAU Industries’ Prospecting Applications - via Joan Projects 0 MCF Ref: C001 TAU Industries – Draft EAP and EMP reports Magaliesburg Community Forum TABLE OF CONTENTS 1 Executive Summary .......................................................................................................... 3 2 Background on Gold Mining Impacts ............................................................................. 4 3 Who is MCF ..................................................................................................................... -

Merafong Municipal Spatial Development Framework

2016 - 2021 2016 - 2021 Merafong Municipal Spatial Development Framework Produced by Christiaan de Jager Spatial Planning & Environmental Management Section Merafong City Local Municipality MERAFONG |MSDF 0 Compiled by Christiaan de Jager Table of Contents 1. INTRODUCTION AND BACKGROUND ............................................................................................... 2 2. NATIONAL, PROVINCIAL AND DISTRICT SCALE POLICY GUIDELINES .................................................. 9 3. THE STUDY AREA .......................................................................................................................... 28 4. SPATIAL ANALYSIS ........................................................................................................................ 29 5. SPATIAL DIRECTIVES ..................................................................................................................... 55 6. THE SDF MAP ............................................................................................................................. 124 ANNEXURE A IMPLEMENTATION PLAN ANNEXURE B NODES AND CORRIDORS ANNEXURE C LOCAL SPATIAL DEVELOPMENT DIRECTIVES MERAFONG |MSDF 1 1. INTRODUCTION AND BACKGROUND In terms of chapter 5 of the Municipal Systems Act, 2000 (Act 32 of 2000), the municipality’s Integrated Development Plan “…must reflect a Spatial Development Framework which must include the provision for basic guidelines for a Land Use Management System for the municipality”. The Merafong Municipal Spatial Development Framework -

A Review of the Sequential Grid Mining Method Employed at Elandsrand Gold Mine

A review of the sequential grid mining method employed at Elandsrand Gold Mine by M.F. Handley*, J.A.J. de Lange**, F. Essrich†, and J.A. Banning‡ Synopsis Sequential grid mining has been employed as the primary mining strategy at the AngloGold West Wits Elandsrand Mine since the inception of stoping operations from the sub-vertical shaft system in 1988. Little has been published on sequential grid mining as a mining strategy since, and the purpose of this paper is to describe sequential grid mining, its history, its implementation at Elandsrand, and the outcome to date. The results obtained using sequential grid mining have been evaluated from seismic data, productivity statistics, and rock related accident statistics. Comparisons with neighbouring mines, namely Western Deep Levels and Deelkraal, have been made to substantiate the improved conditions observed at Elandsrand, and to compare sequential grid mining directly with longwall mining in similar conditions and at similar depths. Sequential grid mMining is shown to be cost-effective, more flexible, and safer than longwall mining in similar conditions, at least on the Ventersdorp Contact Reef in the western part of the Carletonville Goldfield. More work is necessary to establish it as the favoured mining strategy at depths exceeding 3000 metres, and for reefs other than the Ventersdorp Contact Reef. Figure 1—Location of Elandsrand Gold Mining Company Limited Deelkraal and Western Deep Levels will not Introduction be included in the forthcoming discussion— except for a comparison of the seismic Elandsrand Gold Mining Company Limited was response to longwall mining and sequential incorporated in 1974 to mine the Ventersdorp grid mining—because neither played a part in Contact Reef (VCR) on a mining lease of 2619 the development of sequential grid mining. -

Vote 06 : Social Development

Vote 6: Social Development VOTE 6 DEPARTMENT OF SOCIAL DEVELOPMENT Infrastructure to be appropriated by Vote R44 469 000 Responsible MEC MEC for Social Development, Agriculture and Rural Development Administering department Department of Social Development Accounting officer Head of Department 1. STRATEGIC OVERVIEW OF INFRASTRUCTURE PROGRAMME Strategic overview The Department of Social Development’s infrastructure programme continues to be underpinned by the principle of providing accessible developmental services to Gauteng communities in need. The 2012/13 financial year was marked by the demerger from the Department of Health and the re-establishment of Social Development as a separate department, which will enable it to provide a unique contribution towards the attainment of the Province’s developmental goals. For the 2013 MTEF term, the department’s infrastructure plans are focussed on providing support to the achievement of Provincial Outcome’s 6 and 7: • Outcome 6: Sustainable human settlements and improved quality of life; and • Outcome 7: Responsive, accountable, efficient and effective local government. The department achieved substantial success with the completion of outstanding elements of the Prioritised Townships Programme and was able to give more attention to the development and implementation of plans for the upgrade and refurbishment of the network of residential childcare facilities and local and regional service offices. Significant acquisitions for the year included the two former Schools of Industry in Lesedi Local Municipality, Heidelberg which are in need of extensive rehabilitation works and upgrading that would enable the accommodation of females and children with special needs/disabilities. A new direction for the programme now requires attention to the needs identified in the rural nodes, the planning for which will be conducted during the 2013/14 financial year to ensure readiness for implementation in the 2014/15 financial year. -

Gauteng No Fee Schools 2021

GAUTENG NO FEE SCHOOLS 2021 NATIONAL NAME OF SCHOOL SCHOOL PHASE ADDRESS OF SCHOOL EDUCATION DISTRICT QUINTILE LEARNER EMIS 2021 NUMBERS NUMBER 2021 700910011 ADAM MASEBE SECONDARY SCHOOL SECONDARY 110, BLOCK A, SEKAMPANENG, TEMBA, TEMBA, 0407 TSHWANE NORTH 1 1056 700400393 ALBERTINA SISULU PRIMARY SCHOOL PRIMARY 1250, SIBUSISO, KINGSWAY, BENONI, BENONI, 1501 EKURHULENI NORTH 1 1327 24936, CNR ALEKHINE & STANTON RD, PROTEA SOUTH, 700121210 ALTMONT TECHNICAL HIGH SCHOOL SECONDARY JOHANNESBURG CENTRAL 1 1395 SOWETO, JOHANNESBURG, 1818 2544, MANDELA & TAMBO, BLUEGUMVIEW, DUDUZA, NIGEL, 700350561 ASSER MALOKA SECONDARY SCHOOL SECONDARY GAUTENG EAST 1 1623 1496 2201, MAMASIYANOKA, GA-RANKUWA VIEW, GA-RANKUWA, 700915064 BACHANA MOKWENA PRIMARY SCHOOL PRIMARY TSHWANE WEST 1 993 PRETORIA, 0208 22640, NGUNGUNYANE AVENUE, BARCELONA, ETWATWA, 700400277 BARCELONA PRIMARY SCHOOL PRIMARY GAUTENG EAST 1 1809 BENONI, 1519 577, KAALPLAATS, BARRAGE, VANDERBIJLPARK, 700320291 BARRAGE PRIMARY FARM SCHOOL PRIMARY SEDIBENG WEST 1 317 JOHANNESBURG, 1900 11653, LINDANI STREET, OLIEVENHOUTBOSCH, CENTURION, 700231522 BATHABILE PRIMARY FARM SCHOOL PRIMARY TSHWANE SOUTH 1 1541 PRETORIA, 0175 700231530 BATHOKWA PRIMARY SCHOOL PRIMARY 1, LEPHORA STREET, SAULSVILLE, PRETORIA, PRETORIA, 0125 TSHWANE SOUTH 1 1081 25, OLD PRETORIA ROAD BAPSFONTEIN, BAPSFONTEIN, 700211276 BEKEKAYO PRIMARY FARM SCHOOL PRIMARY EKURHULENI NORTH 1 139 BENONI, BENONI, 1510 2854, FLORIDA STREET, BEVERLY HILLS, EVATON WEST, 700320937 BEVERLY HILLS SECONDARY SCHOOL SECONDARY SEDIBENG WEST 1 1504