Press Release Sabyasachi Couture

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Effect of Consumption-Context and Product Attributes on Social Value Perception of Luxury Clothes for Indian Female Consumers Raghav Manocha

Effect of consumption-context and product attributes on social value perception of luxury clothes for Indian female consumers Raghav Manocha To cite this version: Raghav Manocha. Effect of consumption-context and product attributes on social value perception of luxury clothes for Indian female consumers. Business administration. Université Panthéon-Sorbonne - Paris I, 2020. English. NNT : 2020PA01E001. tel-03119250 HAL Id: tel-03119250 https://tel.archives-ouvertes.fr/tel-03119250 Submitted on 23 Jan 2021 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. ECOLE DOCTORALE DE MANAGEMENT PANTHÉON-SORBONNE n°559 Effect of consumption-context and product attributes on social value perception of luxury clothes for Indian female consumers. Effets du contexte de consommation et des caractéristiques des produits sur la perception de la valeur sociale des vêtements de luxe pour les consommatrices indiennes. Thèse de Doctorat présentée en vue de l’obtention du grade de docteur en sciences de gestion par « Raghav MANOCHA » dirigée par Mme Raphaëlle LAMBERT-PANDRAUD Professeure ESCP Business School Soutenance le 29 Juin 2020 Devant un jury composé de : Rapporteurs: M. Gilles LAURENT Research Fellow, ESSEC, Professeur Emérite, HEC Mme Liselot HUDDERS Assistant Professor, Ghent University Suffragants: Mme Sandrine MACE Professeure, ESCP Business School Mme Anne MICHAUT Professeure Associée, HEC 1 L’Université n’entend donner aucune approbation ou improbation aux opinions émises dans les thèses. -

Famous Indian Fashion Designers and How They Made It Big- Part 1 | Shiksha

Famous Indian fashion designers and how they made it big - Part 1 Shiksha Internal Authors Updated on Dec 29, 2016 16:36 IST Famous Indian fashion designers and how they made it big - Part 1 The Indian fashion industry has witnessed a sudden boom and massive takers all across the globe in recent years. From a time where Indian fashion was not acknowledged anywhere in the world to a time when the Indian national dress – Saree is increasingly been credited to be the sexiest and most regal attire a woman can don, our very own fashion industry has come a long way. And we can easily credit this to our stylish, creative and very talented fashion designers. So, for all fashion design aspirants or people like you and me who love to dress-up and look good, Shiksha spills the beans on how some famous fashion designers became the celebs they are today, on Indian as well as Disclaimer: This PDF is auto-generated based on the information available on Shiksha as on 02-Sep-2021. international platforms. Manish Arora Born in the ‘City of Dreams’, Mumbai, Manish Arora was pursuing a graduation degree in commerce when the fashion bug bit him and he went on to join the National Institute of Fashion Technology (NIFT) at New Delhi. He is known to have graduated from NIFT with the ‘Best Student Award’ in 1994. Image courtesy: @im_manisharora on Twitter.com The world for the first time saw the works of Manish Arora in 1997 when he started his own label called – Manish Arora. -

Curriculum Vitae

CURRICULUM VITAE PERSONAL INFORMATION: Name: Sabyasachi Mukherjee Date of Birth: 4th February, 1986 Nationality: Indian Official Address: School of Mathematics, Tata Institute of Fundamental Research, 1 Homi Bhabha Road, Colaba, Mumbai 400005, India Email: [email protected], [email protected] Phone: (+91) 2222782218 Current position: Reader at Tata Institute of Fundamental Research, India since July 2019. ACADEMIC INFORMATION: 1. 2004-2007 : Bachelor of Science (Mathematics (Honours), Physics, and Computer Science) from University of Calcutta, India with First Class; degree awarded on 23rd July, 2007. 2. 2007-2009 : Master of Science (Pure Mathematics) from University of Calcutta, India with First Class; degree awarded on 15th September, 2009. 3. 2009-2010 : Ph.D. coursework in Mathematics at Ramakrishna Mission Vivekananda University, India with 8.75 grade points out of 10 (Grade Sheet issued on 27th May, 2010). 4. 2010-2011 : ‘Master mention Mathématiques et Informatique’ (Masters in Mathematics and Informatics) from Université Paris 13, France with 15.18 grade points out of 20 with mention ‘Bien’; degree awarded on 2nd December, 2011. 5. 2012-2015 : Ph.D. in Mathematics with special distinction from Jacobs University Bremen, Germany; degree awarded on 20th August, 2015. 6. 2015-2019: Lecturer in Institute for Mathematical Sciences, Stony Brook University, USA. Ph.D. thesis: Title: Antiholomorphic dynamics: topology of parameter spaces, and discontinuity of straightening. Ph.D. adviser: Dierk Schleicher, Jacobs University, Bremen, Germany. Jury: John Hamal Hubbard (Cornell University), Alan Huckleberry (Ruhr-Universität Bochum/Jacobs University), Hiroyuki Inou (Kyoto University), Keivan Mallahi-Karai (Jacobs University), John Milnor (Stony Brook University), Dierk Schleicher (Jacobs University). -

![Christian Louboutin Exhibition[Niste] Press Kit](https://docslib.b-cdn.net/cover/1513/christian-louboutin-exhibition-niste-press-kit-2711513.webp)

Christian Louboutin Exhibition[Niste] Press Kit

CHRISTIAN LOUBOUTIN EXHIBITION[NISTE] PRESS KIT CHRISTIAN LOUBOUTIN EXHIBITION TH TH 26 FEBRUARY - 26 JULY PALAIS DE LA PORTE DORÉE 293 AVENUE DAUMESNIL - 75012 PARIS MÉTRO 8 • TRAMWAY 3A • BUS 46 • PORTE DORÉE LEXPOSITION.CHRISTIANLOUBOUTIN.COM | 1 | CHRISTIANCHRISTIAN LOUBOUTIN LOUBOUTIN L’EXHIBITION[NISTE] EXHIBITION[NISTE] PRESSPress KITKit TABLE OF CONTENTS PRESS RELEASE p. 3 THE POSTER p. 4 INTRODUCTION BY HÉLÈNE ORAIN, EXECUTIVE DIRECTOR OF THE PALAIS DE LA PORTE DORÉE p. 5 THE EXHIBITION p. 6 BY OLIVIER GABET, CURATOR OF THE EXHIBITION THE PALAIS DE LA PORTE DORÉE p. 7 AS SEEN BY CHRISTIAN LOUBOUTIN EXHIBITION ITINERARY p. 8 CHRISTIAN LOUBOUTIN p. 14 BIOGRAPHY OLIVIER GABET p. 15 BIOGRAPHY ARTISTS AND CRAFTSPEOPLE IN THE EXHIBITION p. 16 VISUALS AVAILABLE FOR PRESS p. 20 THE PALAIS DE LA PORTE DORÉE p. 35 THE MAISON CHRISTIAN LOUBOUTIN p. 35 BOOK: CHRISTIAN LOUBOUTIN EXHIBITION[IST] p. 36 ARTE DOCUMENTARY p. 38 NORDSTROM p. 39 MAIN SPONSOR OF THE EXHIBITION PRACTICAL INFORMATION p. 40 || 2 || CHRISTIANCHRISTIAN LOUBOUTIN LOUBOUTIN L’EXHIBITION[NISTE] EXHIBITION[NISTE] PRESSPress KITKit THE POSTER « L’Exhibition[niste] is a title that came to me quite quickly. It is a play on the idea of an exhibit and the act of exhibitionism. An exhibit, meaning to expose or display to the public and exhibitionism as drawing attention to oneself. Both are quite close, but I like the more subversive notion that in exhibiting my work I am exposing myself in a more intimate way. I’ve put a lot of myself in this project from both a professional and personal perspective. -

FINAL DISTRIBUTION.Xlsx

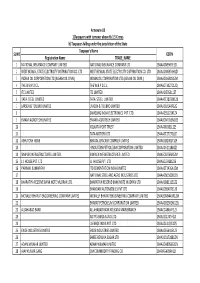

Annexure-1B 1)Taxpayers with turnover above Rs 1.5 Crores b) Taxpayers falling under the jurisdiction of the State Taxpayer's Name SL NO GSTIN Registration Name TRADE_NAME 1 NATIONAL INSURANCE COMPANY LIMITED NATIONAL INSURANCE COMPANY LTD 19AAACN9967E1Z0 2 WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD 19AAACW6953H1ZX 3 INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) 19AAACI1681G1ZM 4 THE W.B.P.D.C.L. THE W.B.P.D.C.L. 19AABCT3027C1ZQ 5 ITC LIMITED ITC LIMITED 19AAACI5950L1Z7 6 TATA STEEL LIMITED TATA STEEL LIMITED 19AAACT2803M1Z8 7 LARSEN & TOUBRO LIMITED LARSEN & TOUBRO LIMITED 19AAACL0140P1ZG 8 SAMSUNG INDIA ELECTRONICS PVT. LTD. 19AAACS5123K1ZA 9 EMAMI AGROTECH LIMITED EMAMI AGROTECH LIMITED 19AABCN7953M1ZS 10 KOLKATA PORT TRUST 19AAAJK0361L1Z3 11 TATA MOTORS LTD 19AAACT2727Q1ZT 12 ASHUTOSH BOSE BENGAL CRACKER COMPLEX LIMITED 19AAGCB2001F1Z9 13 HINDUSTAN PETROLEUM CORPORATION LIMITED. 19AAACH1118B1Z9 14 SIMPLEX INFRASTRUCTURES LIMITED. SIMPLEX INFRASTRUCTURES LIMITED. 19AAECS0765R1ZM 15 J.J. HOUSE PVT. LTD J.J. HOUSE PVT. LTD 19AABCJ5928J2Z6 16 PARIMAL KUMAR RAY ITD CEMENTATION INDIA LIMITED 19AAACT1426A1ZW 17 NATIONAL STEEL AND AGRO INDUSTRIES LTD 19AAACN1500B1Z9 18 BHARATIYA RESERVE BANK NOTE MUDRAN LTD. BHARATIYA RESERVE BANK NOTE MUDRAN LTD. 19AAACB8111E1Z2 19 BHANDARI AUTOMOBILES PVT LTD 19AABCB5407E1Z0 20 MCNALLY BHARAT ENGGINEERING COMPANY LIMITED MCNALLY BHARAT ENGGINEERING COMPANY LIMITED 19AABCM9443R1ZM 21 BHARAT PETROLEUM CORPORATION LIMITED 19AAACB2902M1ZQ 22 ALLAHABAD BANK ALLAHABAD BANK KOLKATA MAIN BRANCH 19AACCA8464F1ZJ 23 ADITYA BIRLA NUVO LTD. 19AAACI1747H1ZL 24 LAFARGE INDIA PVT. LTD. 19AAACL4159L1Z5 25 EXIDE INDUSTRIES LIMITED EXIDE INDUSTRIES LIMITED 19AAACE6641E1ZS 26 SHREE RENUKA SUGAR LTD. 19AADCS1728B1ZN 27 ADANI WILMAR LIMITED ADANI WILMAR LIMITED 19AABCA8056G1ZM 28 AJAY KUMAR GARG OM COMMODITY TRADING CO. -

Sabyasachi Sarees and Weddings Are the Raging Mantra for The

10/3/2019 Sabyasachi Sarees and Weddings Are the Raging Mantra for the Brides and Here's a Lookbook to Flaunt on Your D-day 10/3/2019 Sabyasachi Sarees and Weddings Are the Raging Mantra for the Brides and Here's a Lookbook to Flaunt on Your D-day Sabyasachi Sarees and Weddings Are the Raging Mantra for the Brides and Here's a Lookbook to Flaunt on … ARE YOU A VENDOR? and newspapers or even a folder of screenshots on their phones for deciding the Budget decor and the bridal attire and the Mehndi ceremony dress or the sangeet look. PLANNING TOOLS WEDDING VENUES WEDDING VENDORS BRIDES GROOMS WEDDING IDEAS Almost more than half of these attires and collections of bridal clothing aunted in Wedding Website LOG IN SIGN UP FOR FREE the photos and cutouts belong to Sabyasachi and this name runs in all our minds when we imagine ourselves walking down the aisle. His collections are all about Plan on the go with the WeddingWire app Wedding / Wedding Ideas / Wedding fashion / The Bride SEARCH imperial glamour and gorgeous precision of technicalities in designing works. iPhone Android What we found is a 'romance' in prints – be it his persuasive passion of oral handmade prints on bright colours, light ivory sarees with oral motifs or even an odd striped print (be it on a dupatta or a saree). We THE BRIDE MOST POPULAR ON WEDDINGWIRE Sabyasachi Sarees and Weddings Are the explore it all and the kind of cues that a bride-to-be should take for her own choices in bridal trousseau. -

Object Labels

This 19th-century jacket was donated to MFIT by Geoffrey Beene. It likely came from his company’s reference collection — similar to Traphagen’s own study collection. The ensemble beside it shows how Beene may have adapted the detailed seaming, voluminous sleeves, and quilting of the jacket into contemporary fashion. This pairing demonstrates that by the 1980s, design-by-adaptation was a standard practice throughout the fashion industry. Jacket Silk 1890-1895, USA The Museum at FIT, 91.20.3 Gift of Geoffrey Beene Geoffrey Beene Coat and dress Wool, silk Fall 1983 The Museum at FIT, 2013.29.2 Gift of Sally Kahan This ensemble from James Galanos’s collection of spring/summer 1970 features warrior and lion motifs inspired by ancient Greek pottery. The accompanying fabric is a sample by textile designer Tzaims Luksus from the same collection. It also draws inspiration from classical Greek art and artifacts. Galanos, a first-generation American, practiced design-by-adaptation using his own Greek heritage. James Galanos Evening dress and overskirt Silk 1970 The Museum at FIT, 86.80.1 Gift of Maurice S Polkowitz Tzaims Luksus Textile designed for James Galanos Silk 1970 The Museum at FIT, 114.98.78.2 Gift of Elaine P. Kend “The Greek Way of Galanos” Reproduction from Vogue, June 1, 1970 The geometric piecework and color-blocking of this ensemble are reminiscent of Hard-Edge Abstraction, characterized by harshly juxtaposed colors. John Kloss, who shared a studio with contemporary artist Robert Indiana early on in his career, often drew inspiration from various aspects of modern art, such as colors, forms, and techniques. -

UCLA Electronic Theses and Dissertations

UCLA UCLA Electronic Theses and Dissertations Title Making Designs on Fashion: Producing Contemporary Indian Aesthetics Permalink https://escholarship.org/uc/item/5jr2g7qj Author Varma, Meher Publication Date 2015 Peer reviewed|Thesis/dissertation eScholarship.org Powered by the California Digital Library University of California UNIVERSITY OF CALIFORNIA Los Angeles Making Designs on Fashion: Producing Contemporary Indian Aesthetics A dissertation submitted in partial satisfaction of the requirements for the degree Doctor of Philosophy in Anthropology by Meher Varma 2015 ABSTRACT OF THE DISSERTATION Making Designs on Fashion: Producing Contemporary Indian Aesthetics by Meher Varma Doctor of Philosophy in Anthropology University of California, Los Angeles, 2015 Professor Sherry B. Ortner, Chair This dissertation is about the making of the Indian fashion designer and highlights how the birth of the industry has fashioned new subjects and subjectivities. It traces constitutive shifts and tensions in the fashion industry over the last three decades, including the rise of bridal wear or couture, the appropriation of craft and resistances to it, and the return of ready-to-wear production via e-commerce. I argue that the professional identity of the fashion designer was crafted in opposition to the low-skilled darzi (tailor) and distinct from the ‘traditional’ craftsman with low cultural capital. However, while the designer’s identity was originally celebrated as modern, creative, and entrepreneurial, paradoxically, the most successful designers are those who appropriate and prioritize craft above his or her own skill. To make this argument, this dissertation engages with, and contributes to, scholarship on class and caste in India, anthropological literature on fashion and other creative industries, as well as work on kinship and family. -

The High Court at Calcutta 150 Years : an Overview

1 2 The High Court at Calcutta 150 Years : An Overview 3 Published by : The Indian Law Institute (West Bengal State Unit) iliwbsu.in Printed by : Ashutosh Lithographic Co. 13, Chidam Mudi Lane Kolkata 700 006 ebook published by : Indic House Pvt. Ltd. 1B, Raja Kalikrishna Lane Kolkata 700 005 www.indichouse.com Special Thanks are due to the Hon'ble Justice Indira Banerjee, Treasurer, Indian Law Institute (WBSU); Mr. Dipak Deb, Barrister-at-Law & Sr. Advocate, Director, ILI (WBSU); Capt. Pallav Banerjee, Advocate, Secretary, ILI (WBSU); and Mr. Pradip Kumar Ghosh, Advocate, without whose supportive and stimulating guidance the ebook would not have been possible. Indira Banerjee J. Dipak Deb Pallav Banerjee Pradip Kumar Ghosh 4 The High Court at Calcutta 150 Years: An Overview तदॆततत- क्षत्रस्थ क्षत्रैयद क्षत्र यद्धर्म: ।`& 1B: । 1Bद्धर्म:1Bत्पटैनास्ति।`抜֘टै`抜֘$100 नास्ति ।`抜֘$100000000स्ति`抜֘$1000000000000स्थक्षत्रैयदत । तस्थ क्षत्रै यदर्म:।`& 1Bण । ᄡC:\Users\सत धर्म:" ।`&ﲧ1Bशैसतेधर्मेण।h अय अभलीयान् भलीयौसमाशयनास्ति।`抜֘$100000000 भलीयान् भलीयौसमाशयसर्म: ।`& य राज्ञाज्ञा एवम एवर्म: ।`& 1B ।। Law is the King of Kings, far more powerful and rigid than they; nothing can be mightier than Law, by whose aid, as by that of the highest monarch, even the weak may prevail over the strong. Brihadaranyakopanishad 1-4.14 5 Copyright © 2012 All rights reserved by the individual authors of the works. All rights in the compilation with the Members of the Editorial Board. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retrieval system, without permission from the copyright holders. -

Press Release Sabyasachi Calcutta

Press Release Sabyasachi Calcutta LLP July 06, 2021 Ratings Facilities/Instruments Amount (Rs. crore) Ratings1 Rating Action Revised from CARE A- (Single A Minus) CARE AA-; Stable 2.89 and removed from Credit watch with Long Term Bank Facilities (Double A Minus; (Reduced from 3.33) Positive Implications; Stable outlook Outlook: Stable) assigned CARE AA-; Stable / Revised from CARE A- / CARE A2+ CARE A1+ (Single A Minus / A Two Plus) and Long Term / Short Term 60.00 (Double A Minus; removed from Credit watch with Bank Facilities Outlook: Stable/ A Positive Implications; Stable outlook One Plus) assigned 62.89 (Rs. Sixty-Two Crore Total Bank Facilities and Eighty-Nine Lakhs Only) Details of instruments/facilities in Annexure-1 Detailed Rationale & Key Rating Drivers The revision in the ratings assigned to the Bank Facilities of Sabyasachi Calcutta LLP (SC LLP; erstwhile Sabyasachi Couture) takes into account significantly improved financial flexibility of SC LLP with acquisition of 51% interest by Aditya Birla Fashion and Retail Ltd (ABFRL), a retail venture of Mr. Kumar Mangalam Birla led Aditya Birla group. The revision further takes into account the strategic importance of SC LLP for ABFRL as ABFRL aims at increasing its presence in ethnic wear through this acquisition, has shared senior management team with SC LLP, and finance and treasury functions being handled by representatives of ABFRL. Further, retention of Rs.75 crore in SC LLP (out of the purchase consideration of Rs.398 crore) has led to stronger liquidity and capital structure providing headroom for expansion plans of SC LLP. The creative and strategic rights will be retained by Mr. -

Appellate Jurisdiction

Appellate Jurisdiction Daily Supplementary List Of Cases For Hearing On Wednesday, 24th of February, 2021 CONTENT SL COURT PAGE BENCHES TIME NO. ROOM NO. NO. HON'BLE CHIEF JUSTICE THOTTATHIL B. 1 On 24-02-2021 1 RADHAKRISHNAN 1 DB -I At 10:45 AM HON'BLE JUSTICE ARIJIT BANERJEE HON'BLE JUSTICE RAJESH BINDAL 16 On 24-02-2021 2 7 HON'BLE JUSTICE ANIRUDDHA ROY DB - II At 10:45 AM HON'BLE JUSTICE I. P. MUKERJI 3 On 24-02-2021 3 19 HON'BLE JUSTICE MD. NIZAMUDDIN DB - III At 10:45 AM HON'BLE JUSTICE I. P. MUKERJI 37 On 24-02-2021 4 24 HON'BLE JUSTICE MD. NIZAMUDDIN DB - III At 10:45 AM HON'BLE JUSTICE HARISH TANDON 2 On 24-02-2021 5 25 HON'BLE JUSTICE KAUSIK CHANDA DB- IV At 10:45 AM HON'BLE JUSTICE SUBRATA TALUKDAR 11 On 24-02-2021 6 36 HON'BLE JUSTICE SAUGATA BHATTACHARYYA DB - VI At 10:45 AM HON'BLE JUSTICE TAPABRATA CHAKRABORTY 28 On 24-02-2021 7 40 HON'BLE JUSTICE TIRTHANKAR GHOSH DB - VII At 10:45 AM HON'BLE JUSTICE ARINDAM SINHA 4 On 24-02-2021 8 79 HON'BLE JUSTICE SUVRA GHOSH DB - VIII At 10:45 AM HON'BLE JUSTICE ARIJIT BANERJEE 238 On 24-02-2021 9 86 HON'BLE JUSTICE JAY SENGUPTA DB At 03:00 PM 13 On 24-02-2021 10 HON'BLE JUSTICE RAJASEKHAR MANTHA 96 SB - III At 10:45 AM 8 On 24-02-2021 11 HON'BLE JUSTICE SABYASACHI BHATTACHARYYA 112 SB - IV At 10:45 AM 15 On 24-02-2021 12 HON'BLE JUSTICE RAJARSHI BHARADWAJ 139 SB - VII At 10:45 AM 19 On 24-02-2021 13 HON'BLE JUSTICE SHAMPA SARKAR 148 SB - VIII At 10:45 AM 10 On 24-02-2021 14 HON'BLE JUSTICE RAVI KRISHAN KAPUR 154 SB - IX At 10:45 AM 23 On 24-02-2021 15 HON'BLE JUSTICE ARINDAM MUKHERJEE 161 SB - X At 10:45 AM 18 On 24-02-2021 16 HON'BLE JUSTICE BISWAJIT BASU 169 SB - XI At 10:45 AM SL NO. -

Sabyasachi Artisanal Designs India Private Limited

+91-9830881375 SABYASACHI ARTISANAL DESIGNS INDIA PRIVATE LIMITED https://www.indiamart.com/sabyasachi-couture/ Sabyasachi Mukherjee, designer from Kolkata is making waves in the Indian fashion horizon. After +2 from St.Xaviers college, he graduated from NIFT Kolkata with three major awards in 1999. About Us Sabyasachi Mukherjee, designer from Kolkata is making waves in the Indian fashion horizon. After +2 from St.Xaviers college, he graduated from NIFT Kolkata with three major awards in 1999. Just after graduation, Sabyasachi launched his own label by the same name and currently has retails at New Delhi -Carma & Ogaan, ; Mumbai -Melange & Ensemble ; Kolkata-Espee & Intrigue, and Hyderabad- Origins and Oorja. Following graduation, after three months he launched his eponymous label, and his designs currently retail in various major stores. In 2001, Sabyasachi won the Femina British Council most outstanding young Designer of India award, which took him to London for an internship with Georgina Von Etzdorf, a designer based in Salisbury. He made his international label by winning the grand winner award at Mercedes New Asia fashion week in Singapore in 2003. In 2004, he took part in the Kuala Lampur fashion week, and Lakme India Fashion Week (LIFW). He earned the distinction of being the only Indian designer invited to showcase at the Milan Fashion Week 2004 and was voted by Asia Inc, a Singapore based business magazine, as one of the ten most influential Indians in Asia. For more information, please visit https://www.indiamart.com/sabyasachi-couture/aboutus.html OTHER PRODUCTS P r o d u c t s & S e r v i c e s Designer Dress Dress Mens Kurta Pajama Ladies Designer Dress F a c t s h e e t Nature of Business :Manufacturer CONTACT US SABYASACHI ARTISANAL DESIGNS INDIA PRIVATE LIMITED Contact Person: Ainvrila 80/2, Topsia Road South Maruti Bagan Kolkata - 700046, West Bengal, India +91-9830881375 https://www.indiamart.com/sabyasachi-couture/.