WEL Networks Annual Report 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pdf Hearing 22

1 Before the Hearing Panel Appointed by Waikato District Council to Hear Submissions on the Proposed Waikato District Plan In the matter of: the Resource Management Act 1991 And: Submissions and Further Submissions Lodged on the Proposed Waikato District Plan by Meridian Energy Limited Statement of Evidence of Christine Anne Foster Called by Meridian Energy Limited HEARING 22 - INFRASTRUCTURE 28 September 2020 PROPOSED WAIKATO DISTRICT PLAN: HEARING 22 – EVIDENCE OF C FOSTER FOR MERIDIAN ENERGY LTD 1 1. Introduction 1.1. My name is Christine Anne Foster. I am a Planning Consultant and sole director of CF Consulting Services Limited, based in Wellington. My qualifications and experience are as set out in my statement of evidence to Hearing Number 3. 1.2. This statement of evidence is within my area of expertise as a resource management planner, except where I state that I rely on the evidence of others. I reaffirm my commitment, stated in my evidence to Hearing Number 3, to abide the Code of Conduct for Expert Witnesses set out in the 2014 Environment Court Practice Note (and, in particular section 7 in relation to an expert’s duty to the Court). I have not omitted to consider material facts known to me that might alter or detract from the opinions that I express. 2. Definition of ‘Infrastructure’ Submission Point: 580.1 Section 42A Report: Report D0, paragraphs 194 and 195 2.1 Meridian’s submission point requested that large-scale wind farms be explicitly listed within the definition of ‘infrastructure’. As an alternative, the submission point requested that the definition explicitly include all of the ancillary activities necessary to support large-scale wind farms. -

Statement of Preliminary Issues – 17 August 2021

ISBN 978-1-869459-13-0 Statement of Preliminary Issues Mercury NZ Limited / Trustpower Limited’s retail business 17 August 2021 Introduction 1. On 3 August 2021, we registered an application from Mercury NZ Limited (Mercury) seeking clearance to acquire Trustpower Limited’s (Trustpower) retail business (the Proposed Acquisition). 1 2. The Commission will give clearance if it is satisfied that the Proposed Acquisition will not have, or would not be likely to have, the effect of substantially lessening competition in a market in New Zealand. 3. This statement of preliminary issues sets out the issues we currently consider to be important in deciding whether or not to grant clearance. 2 4. As set out in the Framework section below, our assessment of the Proposed Acquisition is limited to the impact of the transaction on competition in New Zealand markets. Except to the extent it is relevant to the Proposed Acquisition, our clearance process does not involve assessment of the competitive workability of the relevant markets in general. 5. We invite interested parties to provide comments on the likely competitive effects of the Proposed Acquisition. We request that parties who wish to make a submission do so by close of business on 31 August 2021 . The parties and the Proposed Acquisition 6. Mercury and Trustpower both generate electricity and sell electricity to a range of customers and are two of the five traditional ‘gentailers’ that operate in New Zealand.3 In addition to electricity, Mercury and Trustpower also supply, to varying degrees, other utility services such as gas and broadband. -

Disclosure of Contracts

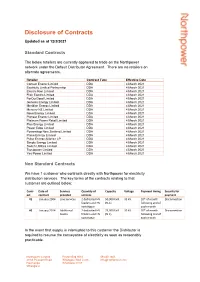

Disclosure of Contracts Updated as at 12/3/2021 Standard Contracts The below retailers are currently approved to trade on the Northpower network under the Default Distributor Agreement. There are no retailers on alternate agreements. Retailer Contract Type Effective Date Contact Energy Limited DDA 4 March 2021 Ecotricity Limited Partnership DDA 4 March 2021 Electric Kiwi Limited DDA 4 March 2021 Flick Electric Limited DDA 4 March 2021 ForOurGood Limited DDA 4 March 2021 Genesis Energy Limited DDA 4 March 2021 Meridian Energy Limited DDA 4 March 2021 Mercury NZ Limited DDA 4 March 2021 Nova Energy Limited DDA 4 March 2021 Pioneer Energy Limited DDA 4 March 2021 Platinum Power Retail Limited DDA 4 March 2021 Plus Energy Limited DDA 4 March 2021 Power Edge Limited DDA 4 March 2021 Powershop New Zealand Limited DDA 4 March 2021 Prime Energy Limited DDA 4 March 2021 Pulse Energy Alliance LP DDA 4 March 2021 Simply Energy Limited DDA 4 March 2021 Switch Utilities Limited DDA 4 March 2021 Trustpower Limited DDA 4 March 2021 Yes Power Limited DDA 4 March 2021 Non Standard Contracts We have 1 customer who contracts directly with Northpower for electricity distribution services. The key terms of the contracts relating to that customer are outlined below: Contr Date of Services Quantity of Capacity Voltage Payment timing Security for act contract provided services payment #1 January 2004 Line Services 2 dedicated HV 50,000 kVA 33 kV 20th of month Disconnection feeders and HV (N-1) following end of switchgear each month #2 January 2014 Additional 2 dedicated HV 25,000 kVA 33 kV 20th of month Disconnection Assets feeders and HV (N-1) following end of switchgear each month In the event that supply is interrupted to this customer the Distributor is required to resume the conveyance of electricity as soon as reasonably practicable. -

FY20 Full Year Results Presentation 20 August 2020

FY20 Full Year Results Presentation 20 August 2020 Marc England – CHIEF EXECUTIVE OFFICER Chris Jewell – CHIEF FINANCIAL OFFICER GENESIS ENERGY LIMITED AGENDA 1 Year in Review 2 Financial Performance and Guidance 3 Strategy Update and Outlook 4 Supplementary Information Genesis Energy Limited FY20 Full Year Result Presentation 2. 1. Year in Review GENESIS ENERGY LIMITED Results at a glance 1 EBITDAF m Retail $ ➢ Genesis’ residential gross customer churn down 3.5 ppt to 24.1% and net churn down 1.6 ppt to 14.8% ➢ Continued Retail momentum - netbacks up in all fuels, Electricity up 7%, Gas up 10% and LPG up 10% ➢ Customers choosing to purchase more than 1 fuel grew to over 121,000, up 3% NPAT m $ ➢ Over 77% of customers now choosing to interact digitally ➢ Launch of new customer Care Package for those most vulnerable post-COVID-19 Final dividend Wholesale cps ➢ 2nd lowest January to June North Island inflow sequence in 95 years, hydro generation down 20% to 491 GWh . Gross ➢ Thermal generation up 12%, fuel portfolio costs up 20% yield of ➢ Average FY20 thermal fuel cost up 7% but has commenced a decline and is down 3% on HY20 to $79/MWh % ➢ Our adaptive flexible generation and fuels portfolio defended low hydrology and high fuel cost impacts ➢ Tekapo upgrades successfully completed and its intake gate capital project reached the half-way point As at 18 August 2020 Operating expenses Kupe down $1m m $ ➢ Field production down 10% due to planned November 30-day outage and February perforation project Finance ➢ Well perforation project completed successfully. -

Electricity Distributors' Performance from 2008 to 2011

ISBN no. 978-1-869453-02-2 Project no. 14.20/13107 Public version Electricity distributors’ performance from 2008 to 2011 Date: 29 January 2013 2 Chapter 1 Introduction 4 Helping customers understand how their electricity distributor is performing 4 We have focused on some key areas of performance 4 We use public information to give an overview of distributors’ performance 5 Structure of this report 5 We would like to hear how useful you found this report 5 Chapter 2 Overview of New Zealand’s electricity industry 6 The main parts of the electricity industry supply chain 6 Key features of the New Zealand electricity distribution sector 7 Chapter 3 Our role in the electricity industry 11 How we regulate electricity distributors in New Zealand 11 Chapter 4 Overview of industry performance 14 Prices, revenue and demand 16 How reliable is electricity distribution in New Zealand? 25 Expenditure 28 3 On 5 February 2013 we made some corrections to the paper. The table below summarises the changes. Distributor Change Buller corrected information in Table 7.1 Electricity Invercargill corrected information in Table 13.1; replaced $7.5m with $1m in commentary under Figure 13.3 MainPower corrected information in Table 16.1 Orion corrected information in Table 22.1; replaced ‘Electra’ with ‘Orion’ in notes to Figures 22.13 and 22.14 OtagoNet corrected information in Table 23.1 Powerco corrected information in Table 24.1 The Power Company corrected information in Table 25.1 Vector corrected information in Table 29.1; added note under Figure 29.1; corrected Figure 29.17 WEL Networks corrected information in Table 31.1 Wellington corrected wording above Figure 32.17 Westpower corrected information in Table 33.1 Introduction 4 Chapter 1 Introduction Helping customers understand how their electricity distributor is performing We have written this report primarily for customers of electricity distribution services, by which we mean people who have, and pay for, a connection to an electricity distribution network.1 This includes both households and businesses. -

WEL Networks Annual Report 2018

2018 WEL Networks and subsidiaries Annual Report 0800 800 935 | wel.co.nz ISSN 2463-4646 (print) ISSN 2463-4646 (print) 02 2018 WEL Networks | Annual Report THIS IS THE ANNUAL REPORT OF WEL NETWORKS LIMITED Dated this 6th day of June 2018 Signed for and on behalf of the Board of Directors ROB CAMPBELL Chairman TONY STEELE Director wel.co.nz CONTENTS PROFILE 03 CHAIRMAN’S REPORT 05 WEL NETWORKS CHIEF EXECUTIVE REPORT 07 ULTRAFAST FIBRE CHIEF EXECUTIVE REPORT 09 QUICK FACTS AND KEY PERFORMANCE INDICATORS 11 DIRECTOR PROFILES AS AT 31 MARCH 2018 21 CORPORATE GOVERNANCE 25 SUSTAINABILITY 26 DIRECTOR DISCLOSURES OF INTEREST 27 WEL ENERGY TRUST 29 THE HEADLINES 31 FINANCIAL STATEMENTS 35 AUDITORS’ REPORT 87 DIRECTORS’ REPORT AND STATUTORY INFORMATION 90 DIRECTORY 95 02 2018 WEL Networks | Annual Report 2018 WEL Networks | Annual Report 03 PROFILE The WEL Group is focused on delivering innovative utility services to enable our communities to thrive. Our electricity network has been serving the Waikato for 100 years distributing power from the national grid, supplying over 160,000 people with electricity services through 90,000 connections. We play a vital part in the economic and social development of the region by recognising and investing in new technologies that will revolutionise our network and future proof our region. The safety of our staff and communities is our highest network that is available to deliver ultra-fast broadband priority and we are committed to ensuring everyone services to more than 200,000 households, schools, makes it home safely every day. businesses and healthcare facilities within the Waikato, Taranaki and Bay of Plenty regions. -

EEA Conf Programme 2021

Conference Programme - Provisional - 17 May 2021 WEDNESDAY, 30 JUNE 2021 8.30am REGISTRATION & TRADE EXHIBITION OPENS ROOM 3 ROOM 4 ROOMS 2 TO 4 9.30am CONFERENCE OPENING 9.35am Jo Hendy, Chief Executive, Climate Change Commission 10.10am Nigel Barbour, Chief Executive, Orion NZ Ltd 10.45am ROOM 1 ROOM 2 ROOM 3 ROOM 4 CARBON ZERO SMART TECHNOLOGY FUTURE GRIDS PANEL SESSION 11.00am Architecture of the Future Low-Carbon, ConductorDown – A groundbreaking safety solution for New approaches to network planning. ‘Protection and Automation’ - Resilient, Electrical Power System. overhead distribution networks. Richard Kingsford, WEL Networks System Restoration Challenges Dr. Radnya Mukhedkar, University of Rodger Griffiths, Electronet Technology CIGRE Panel and Workshop Session Canterbury 11.30am Perverse incentives creating an impact on Death to the Hard-Wired Signal: The rise of Lessons learned during the Australian network performance and New Zealand’s zero IEC61850 Communications transformation towards renewable generation carbon future. Nathan Rich, Connetics Ltd through a prism of New Zealand power systems Dougal McQueen, Aurora Energy & Aleida analysis engineer Powell, University of Otago Alexander Apukov, Mitton Electronet 12.00pm The effects on the wider electricity network of Enhancing rating studies through soil digital twin. The use, development and improvement of heating decarbonisation projects. Nu’man Rashid, Unison Networks Ltd approaches for generation balancing to meet peak Campbell Rae, Connetics Ltd demand. Katherine Moore, Transpower NZ Ltd 12.30pm LUNCH ASSET MANAGEMENT INNOVATION FUTURE ENERGY SECURITY INNOVATIVE TECHNOLOGY SMART TECHNOLOGY 1.30pm Rethinking test data and reporting. An Electricity network infrastructure resilience through the Implementation of Whangamata’s standby battery Analysis of an Intelligent Merging Unit Based on IEC Introduction to our common data environment for lens of seismicity. -

Annual Report

2017 WEL Networks Annual Report 0800 800 935 | wel.co.nz ISSN 2463-4646 (print) 02 2017 WEL Networks | Annual Report THIS IS THE ANNUAL REPORT OF WEL NETWORKS LIMITED Dated this 25th day of May 2017 Signed for and on behalf of the Board of Directors MARGARET DEVLIN Chairman PAUL MCGILVARY Chairman Audit and Risk Committee CONTENTS VISION 02 COMPANY PROFILE 03 QUICK FACTS 04 KEY PERFORMANCE INDICATORS 06 CHAIRMAN’S REPORT 11 CHIEF EXECUTIVE’S REPORT 13 IN THE NEWS 16 DIRECTOR PROFILES 19 CORPORATE GOVERNANCE 21 DIRECTORS’ DISCLOSURES OF INTEREST 22 EXECUTIVE MANAGEMENT 23 WEL ENERGY TRUST 26 FINANCIAL STATEMENTS 28 AUDITORS’ REPORT 70 DIRECTORS’ REPORT AND STATUTORY INFORMATION 73 DIRECTORY 76 02 2017 WEL Networks | Annual Report VISION PROVIDING HIGH QUALITY, RELIABLE UTILITY SERVICES VALUED BY OUR CUSTOMERS WHILST PROTECTING AND ENABLING OUR COMMUNITY 2017 WEL Networks | Annual Report 03 COMPANY PROFILE At WEL Networks we’ve kept the lights on in Waikato communities for nearly 100 years. Our core focus is to distribute power from the national grid, connecting over 160,000 people to electricity services through 89,000 installation connection points. Each year we invest around $45 million to keep our assets in top condition and our crews work around the clock to maintain our network. As our communities grow we continue to play an We’re a trusted member of the community employing essential role in the region’s economic and social approximately 240 employees with a range of expertise; development. We identify and invest in new technologies from Live Line Mechanics, Faults Technicians and Technical that benefit our people, modernise our network and Planners, to in-house Health & Safety professionals, future proof our communities. -

2019 Annual Report Summarises the Operations, Activities and Financial Position of the Marlborough Lines Group for the Year Ended 30 June 2019

2019 ANNUAL REPORT MARLBOROUGH LINES HAS INVESTMENTS IN ELECTRICITY NETWORKS, VITICULTURE AND WINE. WE RECOGNISE BEING CONSUMER OWNED IMPOSES ADDITIONAL CHALLENGES... WE WILL MEET THEM. STANDING STANDING TALL IV section LINE MECHANIC – NIC WILLIAMS AND ARBORIST – KYLE MARFELL, POISED AND READY FOR ACTION. section 1 MARLBOROUGH LINES SEVENTH BEST 304 reliability in New Zealand of 29 networks and Strong support remotely operated much better than New Zealand’s largest city and links with our switches community Internationally recognised HIGH LEVELS management systems QUALITY for quality, health and safety and the OF CUSTOMER ASSETS environment SATISFACTION 85% of customers satisfied/very satisfied overall $125M in electricity discounts No deferred prudent paid to our consumers maintenance or since 1999 capital expenditure $15.77 value per share increased from $1.51 $30M in 1999 to $15.77 in dividends paid Measured our carbon to the Marlborough No debt in the footprint since 2008 Electric Power Trust Parent Company and actively sought from our investments to reduce it since 2010 SUCCESSFUL INVESTMENTS 50% 100% All major 33/11kV substations housed ownership of ownership of indoors with zero noise emission and integrated Nelson Electricity Yealands Wine Group within the environment 2 section A NEW DAY DAWNS AT YEALANDS SEAVIEW VINEYARD AND WINERY IN SEDDON. section 3 YEALANDS WINE GROUP Seaview Vineyard is the single LARGEST VINEYARD IN NEW ZEALAND Is still growing with newly planted areas scheduled to produce within the NEXT THREE YEARS Is -

THE GENESIS ENERGY SHARE OFFER PROSPECTUS DATED 13 MARCH 2014 Important Information

THE GENESIS ENERGY THE SHARE OFFER GENESIS ENERGY PROSPECTUS DATED 13 MARCH 2014 DATED PROSPECTUS SHARE OFFER INITIAL PUBLIC OFFERING OF ORDINARY SHARES IN GENESIS ENERGY LIMITED PROSPECTUS DATED 13 MARCH 2014 we’re in it for you IMPORTANT INFORMATION IMPORTANT NOTICE —the signed consent of the Auditor to the audit report Genesis Energy, their respective offi cers, the directors This document (“Prospectus”) relates to the Off er by appearing in this Prospectus; of Genesis Energy or any other person referred to in this the Crown of ordinary shares in Genesis Energy Limited. —the signed consent of Ernst & Young Transaction Prospectus with respect to the achievement of the results A description of the Off er and the Shares is set out in Advisory Services Limited to the investigating set out in any such statement, or that the underlying Section 7.1 Details of the Off er. accountant’s report appearing in this Prospectus; assumptions used will in fact be realised. —the signed consent of Beca Limited to the This document is a prospectus for the purposes of the independent engineer’s report appearing in SUPPLEMENTARY DISCLOSURE AND Securities Act and the Securities Regulations and is this Prospectus; WITHDRAWAL RIGHT prepared as at, and dated, 13 March 2014. —the signed consent of Gaff ney, Cline & Associates If any signifi cant adverse developments occur This Prospectus is an important document and should be (Consultants) Pte Limited to the independent expert’s prior to the Allotment Date, the Crown and Genesis read carefully before deciding whether or not to invest in report appearing in this Prospectus; Energy may advise investors of those developments Genesis Energy. -

Genesis Energy Limited (GNE) – Hedge Contract Agreed with Meridian Energy

MARKET RELEASE Date: 8 July 2014 Release: Immediate Genesis Energy Limited (GNE) – hedge contract agreed with Meridian Energy Genesis Energy has signed a “swaption” electricity hedge contract to provide dry year cover for Meridian Energy for four years from 1 January 2015. The 150MW swaption follows on from the existing 200MW swaption between Genesis Energy and Meridian Energy which expires in October 2014. The new four-year agreement has a provision to terminate after the first two years in the event Meridian’s contract with NZ Aluminium Smelters sees a reduction in volume. The structure of the new agreement allows for 100MW to be available year round, with an additional 50MW available from 1 April to 30 October in each year of the contract. Genesis Energy’s prospective financial information (PFI) was prepared on the assumption that the existing 200MW swaption would not be replaced with a similar instrument. The new agreement is therefore expected to have a positive impact on Genesis Energy’s FY2015 PFI. Genesis Energy’s Chief Executive, Albert Brantley, said the agreement provides a useful independent revenue stream and enables enhanced economic utilisation of its diverse portfolio of hydro and thermal power generation located in both the North and South Islands of New Zealand. ENDS For media enquiries, please contact: Richard Gordon Public Affairs Manager Genesis Energy P: 09 951 9280 M: 021 681 305 For investor relations enquiries, please contact: Rodney Deacon Investor Relations Manager Genesis Energy P: 09 571 4970 M: 021 631 074 About Genesis Energy Genesis Energy (NZX: GNE) is a diversified New Zealand energy company. -

Contracts Disclosure 2019 9/07/2019 1 2

Disclosure of Contracts relevant to Northpower’s Electricity Lines Business Updated 9 July 2019 This disclosure is made in accordance with clauses 2.4.9 to 2.4.17 of the Electricity Distribution Information Disclosure Determination 2012 (EDIDD 2012) published by the Commerce Commission which requires Northpower to publicly disclose “Prescribed Terms & Conditions” of Northpower’s standard and non- standard contracts relating to the supply of Electricity Lines Services. Contracts with Electricity Retailers Northpower’s contractual arrangement for the provision of Lines Services to most end-use consumers connected to the Northpower network is on an interposed basis. The electricity retailers are “interposed” between Northpower and the end-use consumers, meaning that Northpower has contracts with the electricity retailers and the electricity retailers have individual contracts with the end-use consumers. Table 1 following lists the electricity retailers who have contracts with Northpower for line services to supply consumers on the Northpower network and, for completeness, some additional details. Table 1: Electricity Retailers who have contracts with Northpower for line services (Listed in alphabetical order) Retailer Services provided Basis of contract Contract date Body Corporate Power Lines services Model Use of System July 2018 Limited Agreement 2012 Contact Energy Limited Lines services Model Use of System January 2008 Agreement 2005 Ecotricity Limited Lines services Model Use of System September 2015 Agreement 2005 Electric Kiwi Limited