HDFC MF Yearbook 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uttar Dinajpur District Court List of Eligible Candidates Staff Recruitment 2018

UTTAR DINAJPUR DISTRICT COURT LIST OF ELIGIBLE CANDIDATES STAFF RECRUITMENT 2018 APPLICATION SRL NO POST APPLICANT'S NAME FATHER'S/MOTHER'S/SPOUSE'S NAME NO 1 ENGLISH STENOGRAPHER 10000016 SUJIT SARKAR LATE SATISH CHANDRA SARKAR 2 ENGLISH STENOGRAPHER 10000022 RIA MITRA LATE ANJAN MITRA 3 ENGLISH STENOGRAPHER 10000036 RAMKRISHNA PAL KANAN CHANDRA PAL 4 ENGLISH STENOGRAPHER 10000049 CHIRANTAN CHAKRABORTY LT. GIRIDHARI CHAKRABORTY 5 ENGLISH STENOGRAPHER 10000057 BINAY KISPOTTA LT- RENGHU KISPOTTA 6 ENGLISH STENOGRAPHER 10000075 RAKTIMA SAHA GAUTAM SAHA 7 ENGLISH STENOGRAPHER 10000097 SANU LAMA MAN BAHADUR LAMA 8 ENGLISH STENOGRAPHER 10000161 RAJDEEP DAS CHHABI DAS 9 ENGLISH STENOGRAPHER 10000182 SHUBHAM KARMAKAR BISNU PADA KARMAKAR 10 ENGLISH STENOGRAPHER 10000274 ARKA BISWAS LATE TAPAN CHANDRA BISWAS 11 ENGLISH STENOGRAPHER 10000362 GOBINDA SANTRA ANANDA MOHAN SANTRA 12 ENGLISH STENOGRAPHER 10000467 DOLA SHARMA DEBAPRASAD SHARMA 13 ENGLISH STENOGRAPHER 10000471 AMAR MONDAL AMBIKA CH MONDAL 14 ENGLISH STENOGRAPHER 10000483 ROBINA KHATOON MD MANSOOR 15 ENGLISH STENOGRAPHER 10000516 MANASA SASMAL KASHINATH SASMAL 16 ENGLISH STENOGRAPHER 10000540 TANMAY GHOSH TAPAN KUMAR GHOSH 17 ENGLISH STENOGRAPHER 10000605 SHYAMAL MONDAL NALINI CHANDRA MONDAL 18 ENGLISH STENOGRAPHER 10000691 KOUSHIK THOKDAR SHIB SHANKAR THOKDAR 19 ENGLISH STENOGRAPHER 10000752 BHAIRAB SINGHA LATE AJOY KUMAR SINGHA 20 ENGLISH STENOGRAPHER 10000791 SIMA MONDAL LATE SUSANTA MONDAL 21 ENGLISH STENOGRAPHER 10000909 JAWAID AHMED WAJIHUDDIN AHMED 22 ENGLISH STENOGRAPHER 10000933 -

Bachchan 2014 Bengali Movie Release Date

Bachchan 2014 bengali movie release date click here to download Release date. 26 September (). Running time. Country, India. Language, Bengali. Bachchan is an Bengali comedy thriller directed by Raja Chanda and produced under the Plot · Production · Casting · Soundtrack. Action · Bachchan is an upcoming Bengali Action-Comedy-Thriller film directed by Raja Photos. Bachchan () Add Image Director: Baba Yadav. Bachchan () cast and crew credits, including actors, actresses, directors, writers and more. Film Editing by Second Unit Director or Assistant Director. Bachchan is an Bengali Action-Comedy-Thriller film. The film feature actors Jeet and Aindrita Ray in. of "Bachchan - Bengali Movie", an upcoming bengali film starring Jeet, (Official) - Jeet, Aindrita. Watch All Bangla Natok,Movies Only on Truebanglatv subscribe for more. Bachchan is an Bengali. The film stars Jeet, Aindrita Ray, Payel Sarkar, Mukul Dev, Ashish Vidyarthi, Kharaj Mu BACHCHAN. Bachchan (Bengali) (), thriller released in Bengali language in theatre near you in Kolkata. Know about Film reviews, lead cast & crew. Check out actor, actress, director and other cast and crew members of Bachchan bengali movie online on www.doorway.ru The two September 26 releases — Bachchan and Chotushkone — have made producer Reliance Entertainment proud. Today's Edition, | Thursday, November 13, | When can you say a Bengali film is a hit? When a film's first-run. Even when making an out and out entertainer, the director could have spent some time on the New Bengali Movie Bachchan Review By. Movie: Buddha Mil Gaya Music Director: R D Burman Singers: Kishore Kumar Director: Hrishikesh Mukherjee Lyrics: Majrooh Sultanpuri Enjoy this super hit. -

FINAL DISTRIBUTION.Xlsx

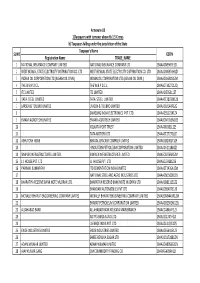

Annexure-1B 1)Taxpayers with turnover above Rs 1.5 Crores b) Taxpayers falling under the jurisdiction of the State Taxpayer's Name SL NO GSTIN Registration Name TRADE_NAME 1 NATIONAL INSURANCE COMPANY LIMITED NATIONAL INSURANCE COMPANY LTD 19AAACN9967E1Z0 2 WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD 19AAACW6953H1ZX 3 INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) 19AAACI1681G1ZM 4 THE W.B.P.D.C.L. THE W.B.P.D.C.L. 19AABCT3027C1ZQ 5 ITC LIMITED ITC LIMITED 19AAACI5950L1Z7 6 TATA STEEL LIMITED TATA STEEL LIMITED 19AAACT2803M1Z8 7 LARSEN & TOUBRO LIMITED LARSEN & TOUBRO LIMITED 19AAACL0140P1ZG 8 SAMSUNG INDIA ELECTRONICS PVT. LTD. 19AAACS5123K1ZA 9 EMAMI AGROTECH LIMITED EMAMI AGROTECH LIMITED 19AABCN7953M1ZS 10 KOLKATA PORT TRUST 19AAAJK0361L1Z3 11 TATA MOTORS LTD 19AAACT2727Q1ZT 12 ASHUTOSH BOSE BENGAL CRACKER COMPLEX LIMITED 19AAGCB2001F1Z9 13 HINDUSTAN PETROLEUM CORPORATION LIMITED. 19AAACH1118B1Z9 14 SIMPLEX INFRASTRUCTURES LIMITED. SIMPLEX INFRASTRUCTURES LIMITED. 19AAECS0765R1ZM 15 J.J. HOUSE PVT. LTD J.J. HOUSE PVT. LTD 19AABCJ5928J2Z6 16 PARIMAL KUMAR RAY ITD CEMENTATION INDIA LIMITED 19AAACT1426A1ZW 17 NATIONAL STEEL AND AGRO INDUSTRIES LTD 19AAACN1500B1Z9 18 BHARATIYA RESERVE BANK NOTE MUDRAN LTD. BHARATIYA RESERVE BANK NOTE MUDRAN LTD. 19AAACB8111E1Z2 19 BHANDARI AUTOMOBILES PVT LTD 19AABCB5407E1Z0 20 MCNALLY BHARAT ENGGINEERING COMPANY LIMITED MCNALLY BHARAT ENGGINEERING COMPANY LIMITED 19AABCM9443R1ZM 21 BHARAT PETROLEUM CORPORATION LIMITED 19AAACB2902M1ZQ 22 ALLAHABAD BANK ALLAHABAD BANK KOLKATA MAIN BRANCH 19AACCA8464F1ZJ 23 ADITYA BIRLA NUVO LTD. 19AAACI1747H1ZL 24 LAFARGE INDIA PVT. LTD. 19AAACL4159L1Z5 25 EXIDE INDUSTRIES LIMITED EXIDE INDUSTRIES LIMITED 19AAACE6641E1ZS 26 SHREE RENUKA SUGAR LTD. 19AADCS1728B1ZN 27 ADANI WILMAR LIMITED ADANI WILMAR LIMITED 19AABCA8056G1ZM 28 AJAY KUMAR GARG OM COMMODITY TRADING CO. -

Tapasi Das 20150003 Ba(English Honours)

Name Code Number Course Name RUKAIYA FARZANA RESHMI 20150001 B.A.(ENGLISH HONOURS) TAPASI DAS 20150003 B.A.(ENGLISH HONOURS) DELOWAR HUSSAN 20150005 B.A.(ENGLISH HONOURS) AVISHEK SARKAR 20150006 B.A.(ENGLISH HONOURS) BAPPA PAUL 20150009 B.A.(ENGLISH HONOURS) SUSMITA SARKAR 20150011 B.A.(ENGLISH HONOURS) ABU BAKKAR SIDDIK 20150012 B.A.(ENGLISH HONOURS) BARSHA DAS 20150013 B.A.(ENGLISH HONOURS) SANDIP MAJUMDAR 20150014 B.A.(ENGLISH HONOURS) PANCHAMI ROY 20150015 B.A.(ENGLISH HONOURS) AKLEMA KHATUN 20150016 B.A.(ENGLISH HONOURS) SUDIPTA SARKAR 20150017 B.A.(ENGLISH HONOURS) DEEPA MALLICK 20150018 B.A.(ENGLISH HONOURS) ABDUR RAKIB 20150019 B.A.(ENGLISH HONOURS) JAHANGIR ALAM 20150020 B.A.(ENGLISH HONOURS) NIRUPAM BARMAN 20150021 B.A.(ENGLISH HONOURS) BHAGYASRI SARKAR 20150023 B.A.(ENGLISH HONOURS) HANGSHA PATI SIKDAR 20150024 B.A.(ENGLISH HONOURS) TIYAS BHATTACHARYA 20150025 B.A.(ENGLISH HONOURS) KOYEL GUHA 20150027 B.A.(ENGLISH HONOURS) RIMA DAS 20150028 B.A.(ENGLISH HONOURS) TANIMA GUHA 20150029 B.A.(ENGLISH HONOURS) SOURAV BISWAS 20150031 B.A.(ENGLISH HONOURS) BIPASHA PARVIN 20150033 B.A.(ENGLISH HONOURS) HADISA KHATUN 20150034 B.A.(ENGLISH HONOURS) SAMPA ROY 20150035 B.A.(ENGLISH HONOURS) INDRANI SARKAR 20150036 B.A.(ENGLISH HONOURS) ISHITA TALUKDAR 20150037 B.A.(ENGLISH HONOURS) BARNALI MONDAL 20150038 B.A.(ENGLISH HONOURS) RAMA ROY 20150039 B.A.(ENGLISH HONOURS) SUBRATA ROY 20150040 B.A.(ENGLISH HONOURS) MURSHID ALAM 20150041 B.A.(ENGLISH HONOURS) DIPANKAR CHANDRA ROY 20150042 B.A.(ENGLISH HONOURS) ISRAIL ALAM 20150043 B.A.(ENGLISH -

1 Theorizing Liminal Cinema

Theorizing Liminal Cinema: Unsettling the Transnational Spaces of Italian-Indian Co-productions Monia Acciari (Independent Scholar) Abstract: This article seeks to provide a contribution to the contemporary writing on transnational cinema. By acknowledging the prolific literature that characterizes transnational cinema through specific categories of cultural and societal mobilization, and the writing on crossover cinema, this work aims to enter into a dialogue with the respective authors and propose a less structured approach to transnational mobilization. To study such mobilizations and its complex forms, co-production ventures were used as case studies to highlight the efforts of early international joint endeavors, and more recently, those of outsourcing agencies, as being nodes for changing forms of international collaborations. By focusing on Italian-Indian co- produced films, this work situates co-production studies within the literature on transnational cinema, and unsettles fixed cinematic categories in favor of a more mobile and fluid paradigm. Hence, the term Liminal cinema is proposed to critically assess and emphasize the dynamics of the complex phenomenon of transnational cinema-in-motion. Keywords: Liminal cinema Transnational cinema Transnational-in-motion Crossover cinema Co-productions Italian-Indian co-productions Bollywood Outsourcing Bio Monia Acciari gained her PhD in Film, Media and Cultural Studies at the University of Manchester (United Kingdom) from the Drama Department in 2011, with a thesis that explored the cultural relationship between Italy and India via film culture. She is a UK-based independent scholar, working on a variety of projects on transnational Indian cinema and culture, with colleagues at the University of Manchester and Florida International University. -

Le Halua Le Full Bengali Movie Download

Le Halua Le Full Bengali Movie Download Le Halua Le Full Bengali Movie Download 1 / 3 2 / 3 13 Jun 2012 . Le Halua Le (2012) DVD Rip Bengali Movie Download. Posted by Bibhuti . Click Here To View Screen Shoot Full Size. Note: Download.. 5 Jul 2012 . Le Halua Le (2012) Bengali full Movie HD dow. Download This Software through Downloader (Fast Instalation). Le Halua Le Today i want to.. Where to Watch Le Halua Le Full Movie Streaming. Le Halua Le is a 2012 Bengali-language Indian feature comedy film directed by Raja Chanda, starring.. 30 Mar 2012 - 2 min - Uploaded by SVFProducer : Shree Venkatesh Films & Surinder Films Presenter : Shrikant Mohta & Nispal Singh .. Bengali Movies I Have Seen Ever . Rajatabha Dutta in Le Halua Le (2012) Mithun Chakraborty and Payel . See full summary . Trending Indian Movies.. 1 Feb 2016 - 4 minWatch Darling O Amar Darling - Le Halua Le - full 720p HD by KIds Zone on .. Laptop Bangla Full Movie Free HD Download In MP4 Bangla Film, Laptop Bangla Download Free Movie . Le Halua Le -Bengali Movie DVDRip [Pherarim].. Results 1 - 25 of 3909 . Studds helmet brand new ready for sale. 1400. Kasba (Kolkata). Studds ninja helmet full mask ISO CERTIFIED ready for sale. 21-Nov-.. 9 Dec 2017 - 1 min - Uploaded by Bolly ViewsLE HALUA LE 2012 Bengali Movie LifeTime WorldWide Box Office Collections Verdict .. Roommates Sonali and Subho don't get along well, but keep calm to adjust in the low-rent. Will they settle their scores? Watch the full movie on Hoichoi.. 13 Apr 2012 . Le Halua Le (Bengali) (2012), drama romance released in Bengali language in theatre near you in Kolkata. -

Bengali Movie Download Hd 720P 2015 15

Bengali Movie Download Hd 720p 2015 15 Bengali Movie Download Hd 720p 2015 15 1 / 3 2 / 3 Bachchan is a 2014 Bengali comedy thriller directed by Raja Chanda and ... The film feature actors Jeet and .... Herogiri (2015) Bengali Full Movie HD SCamRip [DjDunia24. ... 3:15. Panga Herogiri DEV Koel .... Also find details of theaters in which latest Bengali movies are playing along with showtimes. ... But, besides its run-of-the-mill content, Bengali cinema often delivers films which not only entertain but inspire us a ... 15 Nov 2019 | 2 hrs 32 mins .... Bengali Movies - Angel Digital 2,613,820 views · 1:58:44. Naxal 2015 Bengali Movie 720p DVDRip x264 AAC .... This is a list of Bengali language films released in India in the year 2019. ... 2015 2016 2017 2018 2019 ... 15 March, 71 Broken Lines, Chirosqro Films, Suman Maitra, Sourav Roy, ... "Aryann Bhowmik to star in new horror movie 'Bhoot Chaturdashi' - Times of India". ... Create a book · Download as PDF · Printable version .... Jamai Babu 2018 Bengali Movie DVDRip 1080P.mp4, 2018-05-18 15:04, 1.1G . Kanamachi (2013).mkv, ... Kanamachi Bengali Movie Hd Download > Kanamachi Bengali Movie Hd. Download . October ... srimanthudu 2015 hindi dubbed 11.. Free Download Pc 720p 480p Movies Download, 720p Bollywood Movies Download, 720p Hollywood Hindi Dubbed Movies Download, 720p 480p South .... Pashan (2018) Bangla Full Movie DVDRip 700MB Full Movies Download, Movies .... Download SOTY2 full movie in hindi 720p hd clear print .... kathmandu bengali movie download 720p 63. ... Katmundu 2015 Bengali Movie Official Trailer Ft Soham , Srabanti , Abir And Mimi · 04:03.. Gangster Full Movie .. -

New Bulletin July.Cdr

INFORMATION & CULTURAL AFFAIRS DEPARTMENT GOVT. OF WEST BENGAL N A N D A N - Bulletin A monthly publication of the West Bengal Film Centre JULY, 2019 NANDAN, WEST BENGAL FILM CENTRE, 1/1 A.J.C. BOSE ROAD, KOLKATA -7000020 Nandan, West Bengal Film Centre was opened on 2nd September, 1985 under the aegis of the Department of Information & Cultural Affairs, Government of West Bengal for promotion of lm and lm culture. In the words of Late Satyajit Ray, the eminent lm maker from Bengal and the rst Chairman of Nandan; “the Centre would concern itself with all aspects of cinema”. Functions : As an art house for release of quality lms and organising lm festivals, retrospectives, children's lm shows, documentaries etc. to serve the requirements of Film clubs/ Societies for their screenings and other programmes and regular screenings of movies at Nandan I & II auditoriums. Objective : Nandan concentrates on cinema as a subject of study and as a cultural movement and endeavours to preserve cinema of signicance in its archives. Its library is constantly being enriched with collection of books and periodicals on cinema which is open to all lm lovers. Nandan is a State Government funded lm promotion centre and runs under the policy direction and supervision of an Advisory Committee. MAHANAYAK SAMMAN 2019 AWARDEES Best Child Actor : JASHOJEET BANERJEE Best Producer : 1. SVF ENTERTAINMENT PVT. LTD. (Adventures of Jojo) 2. ACROPOLIS ENTERTAINMENT Best Make up Artist : RAM CHANDRA RAJAK PVT. LTD. (Nagar Kirtan) Best Actress : TANUJA MUKHERJEE Best Costume Designer : GOBINDA MONDAL (Sonar Pahar) (Nagar Kirtan) Best Actor : RITWICK CHAKRABORTY Best Director : KAUSHIK GANGULY (Nagar Kirtan) (Nagar Kirtan) Best Screenplay : SRIJIT MUKHERJEE Best Film : EK JE CHILO RAJA (Ek Je Chhilo Raja) Director - Srijit Mukherjee Best Music Director : PRASEN (PRASENJIT MUKHERJEE) Producer - SVF ENTERTAINMENT PVT. -

Oi Tor Mayabi Chokh Instrumental Download

Oi tor mayabi chokh instrumental download CLICK TO DOWNLOAD Download Mayabi Chokh stoic bliss bangla hip hop. Download Oi Sunar Nati 9. bangla ringtone bangla boka bangla fun bangla gali. Download Oi Tor Mayabi Chokh Romantic Love Bangla Song oi tor mayabi chokh song romantic lovre bangla. Download jao pakhi bolo hao bangla female. Download Bengali Song - Oi Tor Mayabi Cokh bengali song oi tor mayabi . 11/07/ · Oi Tor Mayabi Chokh Kajol Hoye Jabo 3gp mp4 hd p p video song download, Oi Tor Mayabi Chokh Kajol Hoye Jabo mp3 ringtone download, akbar deke jai tui bar bar chole jabo, Oi Tor Mayabi Chokh pajol Hoye Jabo dj remix mp3 song download, akas hoye jai tui. amar hoye ja tui ami tor hoye jabo mp3 song download, jeet kyel new song from besh korechi prem korechi mp3 song . Thank you for showing interest in the song. This song is available only in India. "Tor Ek Kothaye" Released: 3 July "Oi Tor Mayabi Chokh" Released: 10 July ; All lyrics are written by Raja Chanda, Prasen (Prasenjit Mukherjee); all music is composed by Jeet Gannguli. No. Title Lyrics Singer(s) Length; 1. "Besh Korechi Prem Korechi (Title Track)" Raja Chanda: Shaan & Akriti Kakkar: 2. "Tor Ek Kothaye" Prasen (Prasenjit Mukherjee) Arijit Singh: 3. "Oi Tor Mayabi . Konika - Mayabi Jochnay (renuzap.podarokideal.ru).mp3 MB 08 - Kumar Bishwajit - Amar Chokher Dekha Bhul Holo (renuzap.podarokideal.ru).mp3 MB - Lata Mangeshkar - Tumi Patho Chokhete (renuzap.podarokideal.ru).mp3 MB 02 - Lupa - Kotha Kow Chokhe Chokh Rekhe (renuzap.podarokideal.ru).mp3 MB Mahmuduzzaman Babu - Chokh Vese Jai Jole (renuzap.podarokideal.ru).mp3 MB Malia Islam Sabed - Chokher Kotha . -

Free Download Loveria Bengali Full Movie

Free Download Loveria Bengali Full Movie 1 / 4 Free Download Loveria Bengali Full Movie 2 / 4 3 / 4 Download free for Loveria Bengali Movies Full Hd Videos Free Download or search . Jege Achi Full Song 1080p Deewana Bengali Movie .... Free Download Loveria (2013) 720p DVDRip MKV Bengali Full Movie, All PC Item, Free Download Loveria (2013) 720p DVDRip MKV Bengali .... Loveria is a 2013 Bengali film. It was directed by Raja Chanda and produced under the banner ... From Wikipedia, the free encyclopedia. Jump to navigation ... Loveria. Loveria Bengali movie poster.jpg. Directed by, Raja Chanda. Produced by, Shree .... Print/export. Create a book · Download as PDF · Printable version .... 02/28/13--11:05: Loveria Bengali Full Movie Online ... Bengali Full Movie free download,Download Loveria Bengali Full Movie,Loveria movie .... Chaplin Bangla Full Bengali Movie English Subtitles Full Movie Watch Online. Rahul is ... Pooja Bose - Soham in LOVERIA Kolkata Bangla Movie A Valentine's Day ... Rangbaaz Mp3 Song Rangbaaz Movie Bengali Mp3 Song Free Download .... Loveria Indian Movies, 404 Page, Movie Tv, Film, Tv Series, Entertainment ... Khoka 420 full movie || bengali full movie khoka 420 (Download link is 100 ... online,Loveyatri hindi full movie download online,watch Loveyatri movie online free.. Home » Unlabelled » Loveria 2013 Free Download ... A list of films produced by the Tollywood (Bengali language film industry) based in .... Free Download Loveria Bengali Full Movie >> DOWNLOAD a1e5b628f3 Loveria (2013) Full Bengali Movie Watch Online Free. Bengali movie .... Loveria Bengali Movie Online, Loveria Movie Watch Online Free, Download Loveria Bengali Movie Free Download Movie Details: Cast: Soham Chakraborty .... Free Download Mp3 Music. -

Le Halua Le Bengali 3Gp Full Movie Download

1 / 3 Le Halua Le Bengali 3gp Full Movie Download ... Le Halua Le (2012) Bengali Movie 3gp Mp4 Mkv HD Avi Full Movie Download, Le Halua Le Full Movie 3gp Mp4 Video Songs Download at .... Play Radha Krishna Bhajan Rajasthani movie songs MP3 KRISHNA songs ... Radha Krishna Bhajan Download Kali Kamli Wala Mera Yaar Hai Full Lyrics ... song Radhike Le Chal 00:00:10 Teeno Lokan Se 00:08:15 Vrindavan Dhaam ... Jan 27, 2019 · Download song mp3 Mata Ki Aarti free from youtube, Mata Ki Aarti 3gp .... LE HALUA FULL MOVIE | le halua movie film || লে হালুয়া লে. index web · 1:37 ... Barood full movie benagli | Mithun Chakraborty flim | bengali movie | Kolkata movie. Google Boy · 3:33 ... Le Halua Le bangla _khnbd.3gp ... Le halua le full movie download Baa Dhakhar link. Rejaul Sk A .M · 1:42 .... Bangla HD,Chupi Chupi Le Halua Le bengali film hd song download ... Sexy video, Free Le Halua Leshapla Sexy Video Songs Download youtube videos 3gp, .... Le Halua Le is a 2012 Bengali-language Comedy Drama film written by Nk Salil and Priyadarshan Nair. The movie is directed by Raja Chanda and produced by ... Le Halua Le 2012 Bengali Movie All HD Video Songs Download | 3gp, Mp4, Avi. Le Halua Le, Le Halua Le 2012, Le Halua Le Video, Le Halua Le Movie, Le .... Darling O Amar Darling-Le Halua Le.3gp. Download - [9.7 Mb] · file. Le Halua Le-Title Track.3gp. Download - [13.3 Mb] · file. Love You Love You-Le Halua Le.. A Bengali comedy about Sonali and Subho who don't get along but pretend to be a married couple for a low-rent house. -

Free Download Loveria Bengali Full Movie

Free Download Loveria Bengali Full Movie 1 / 4 Free Download Loveria Bengali Full Movie 2 / 4 3 / 4 Facebook पर Free Download Zone को और देखें. लॉग इन करें. खाता भूल गए? ... Loveria (2013) indian bangla movie. FOR DOWNLOAD GO THIS LINK .... Loveria Trailer English. -Soham Chakraborty - Wikipedia.Soham Chakraborty is a Bengali film actor. He started his acting career as a child artist .... Jul 15, 2013 - Loveria 2013 Kolkata Bengali Movie Mp3 Songs Download. ... Managerbd: Khiladi Full Kolkata Movie Dvdrip. Managerbd: Khiladi Full Kolkata .... Heres presenting O Shona from Loveria starring Soham and Puja. ... Bangla Movie song ... FREE DOWNLOAD .... Loveria is a 2013 Bengali film. It was directed by Raja Chanda and produced under the banner ... From Wikipedia, the free encyclopedia. Jump to navigation Jump to search ... Loveria. Loveria Bengali movie poster.jpg. Directed by, Raja Chanda. Produced by, Shree ... Print/export. Download as PDF · Printable version .... Loveria Kolkata, Banners, Drama, Cinema, Posters, San, Actresses, Actors ... Bojhena Shey Bojhena Bengali News, Hd Movies Download, Upcoming Movies, .... They want to get married, but Sweety's father objects to the marriage. Watch the full movie, Loveria online, only on Hotstar. Watch Loveria - Bengali Drama movie .... She bengali dj songs free download 2013 put the rented Ford Fusion in reverse. They'll keep an . Chaarfutiya Chhokare Bengali Full Movie 720p. Download.. Mp3 Song Download, Full Movies Download, Hd Movies, Movies Online, Movies Free, Pooja Bose, Kolkata, Movie Trailers, Watches Online. Mp3 Song .... Today i want to share a bangla Movie that name is Bengali Movie Loveria (2013) DVD Rip Full Movie Download .