Le Texte Intégral De L'avis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Why Paris Region Is the #1 Destination on the Planet: with 50 Million Visitors Each Year, the Area Is Synonymous with “Art De Vivre”, Culture, Gastronomy and History

Saint-Denis Basilicum and Maison de la Légion d’Honneur © Plaine Commune, Direction du Développement Economique, SEPE, Som VOSAVANH-DEPLAGNE - Plain of Montesson © CSAGBS-EDesaux - La Défense Business district © 11h45 for Defacto - Campus © Ecole Polytechnique Paris/Saclay. J. Barande - © Ville d’Enghien-les-Bains - INSEAD Fontainebleau © Yann Piriou - Charenton-le-Pont – Ivry-sur-Seine © ParisEstMarne&Bois - Bassin de La Villette, Paris Plages © CRT Ile-de-France - Tripelon-Jarry Welcome to Paris Region Paris Region Facts and Figures 2020 lays out a panorama of the region’s economic dynamism and social life, Europe’s business positioning it among the leading regions in Europe and worldwide. & innovation With its fundamental key indicators, the brochure “Paris Region Facts and powerhouse Figures 2020” is a tool for decision and action for companies and economic stakeholders. It is useful to economic and political leaders of the region and to all those who want to have a global vision of this dynamic regional economy. Paris Region Facts and Figures 2020 is a collaborative publication produced by Choose Paris Region, L’Institut Paris Region and the Paris Île-de-France Regional Chamber of Commerce and Industry. Jardin_des_tuileries_Tour_Eiffel_01_tvb CRT IDF-Van Biesen Table of contents 5 Welcome to Paris Region 27 Digital Infrastructure 6 Overview 28 Real Estate 10 Population 30 Transport and Mobility 12 Economy and Business 32 Logistics 18 Employment 34 Meetings and Exhibitions 20 Education 36 Tourism and Quality of life 24 R&D and Innovation Paris Region Facts & Figures 2020 Welcome to Paris Region 5 A dynamic and A business fast-growing region and innovation powerhouse Paris Region, The Paris Region is a truly global region which accounts for 23.3% The highest GDP in the European of France’s workforce, 31% of Union (EU28) in billions of euros. -

Preliminary Results 2020/21 Simon Roberts Chief Executive Officer Kevin O’Byrne Chief Financial Officer Agenda

Preliminary Results 2020/21 Simon Roberts Chief Executive Officer Kevin O’Byrne Chief Financial Officer Agenda 01 02 Financial highlights Operational performance 4 J Sainsbury plc Preliminary Results 2020/21 Financials Operational Performance Retail sales growth by category Grocery General Merchandise Clothing Total Retail FY Sales FY Sales FY Sales FY Sales growth1 up 7.8 % up 8.3% down 8.5% up 7.3 % 9.2% 8.5% 10.5% 1 7.6 % 4.2% 6.8% 0.4% 5.2% 7.4 % 7.1 % Q1 Q2 Q3 Q4 5.1% 7.2 % 7.6 % Q1 Q2 Q3 Q4 6.0% (7.5) % 7.3% Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 (26.7)% Fuel 0.1% Exc. Fuel Inc. Fuel sales sales growth growth 1 Exc. fuel (39.1)% 5 J Sainsbury plc Preliminary Results 2020/21 Financials Operational Performance Group performance overview Retail Financial Services Underlying profit Statutory profit/ operating profit1 operating profit1 before tax loss before tax down 22% down 39% 938 48 586 255 730 FY 356 19/20 FY 19/20 FY 20/21 FY FY FY 20/21 FY FY 19/20 20/21 19/20 20/21 (21) (261) All figures £m 1 Underlying 6 J Sainsbury plc Preliminary Results 2020/21 Financials Operational Performance Group performance overview Free cash flow Working capital Net debt Dividend movement excluding leases per share 1 up 28% down £539m 10.6p 10.6p 784 453 1,179 7.3p 7.4 p 611 640 3.3p 3.2p FY 20/21 FY FY FY FY FY Interim Special Interim Final 19/20 20/21 19/20 19/20 20/21 19/20 20/21 20/21 20/21 (97) All figures £m 1 Special dividend in 2020/21 paid in lieu of final dividend for 2019/20 following the deferral of dividend decision. -

Global Vs. Local-The Hungarian Retail Wars

Journal of Business and Retail Management Research (JBRMR) October 2015 Global Vs. Local-The Hungarian Retail Wars Charles S. Mayer Reza M. Bakhshandeh Central European University, Budapest, Hungary Key Words MNE’s, SME’s, Hungary, FMCG Retailing, Cooperatives, Rivalry Abstract In this paper we explore the impact of the ivasion of large global retailers into the Hungarian FMCG space. As well as giving the historical evolution of the market, we also show a recipe on how the local SME’s can cope with the foreign competition. “If you can’t beat them, at least emulate them well.” 1. Introduction Our research started with a casual observation. There seemed to be too many FMCG (Fast Moving Consumer Goods) stores in Hungary, compared to the population size, and the purchasing power. What was the reason for this proliferation, and what outcomes could be expected from it? Would the winners necessarily be the MNE’s, and the losers the local SME’S? These were the questions that focused our research for this paper. With the opening of the CEE to the West, large multinational retailers moved quickly into the region. This was particularly true for the extended food retailing sector (FMCG’s). Hungary, being very central, and having had good economic relations with the West in the past, was one of the more attractive markets to enter. We will follow the entry of one such multinational, Delhaize (Match), in detail. At the same time, we will note how two independent local chains, CBA and COOP were able to respond to the threat of the invasion of the multinationals. -

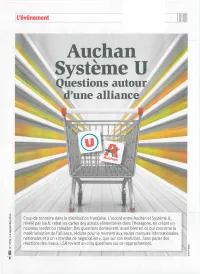

Questions Autour D'une Alliance!^

L'événement 11 Auçhan SystèmQuestions autoue Ur d'une alliance!^ Coup de tonnerre dans la distribution française. L'accord entre Auchan et Système U, révélé par lsa.fr, rebat les cartes des achats alimentaires dans l'Hexagone, en créant un nouveau leader ou coleader. Des questions demeurent, aussi bien en ce qui concerne la matérialisation de l'alliance, réduite pour le moment aux seules marques internationales, nationales et à un «mandat de négociation», que sur son évolution. Sans parler des réactions des rivaux. LSA revient en cinq questions sur ce rapprochement. n L'événement Est-cela naissanced'un nouveau leader ? Par la grâce d'un accord mettant leurs achats en commun via un mandat de négociation confié à la centrale Eurauchan, Serge Papin, patron de Système U, et Vianney Mulliez, président du conseil de ' 1« *' | surveillance d'Auchan, passent en France du statut de challenger à jJ <r> H, H 0 celui de poids lourds de la distribution alimentaire. LES CHIFFRES VENTES CUMULÉES 44,5 Mrds€ (CA TTC avec carburants) 210 hypers, ur le papier, l'addition des chiffres d'affaires comme une concentration, et ne sera pas notifié 1039 supers, d'Auchan et de Système U place le nouvel à l'Autorité de la concurrence. Il n'empêche, leurs 715 proxi Sensemble en position de leader virtuel de la parts de marché cumulées constitueront bien le AUCHAN distribution alimentaire en France. «Système A», véritable poids économique à l'achat des nouveaux 16,8 Mrds€ (-2,6%) comme certains nomment déjà la nouvelle alliance, alliés. Ils détiennent ensemble 21,5 % de part de 139 magasins «pèse» 44,5 Mrds € de chiffre d'affaires TTC avec marché depuis le début de l'année (selon Kantar), SIMPLYMARKET carburants, selon le dernier top 100 de LSA. -

Trade for Development Centre - BTC (Belgian Development Agency)

Trade for Development Centre - BTC (Belgian Development Agency) 1 Trade for Development Centre - BTC (Belgian Development Agency) Author: Facts Figures Future, http://www.3xf.nl Managing Editor: Carl Michiels © BTC, Belgian Development Agency, 2011. All rights reserved. The content of this publication may be reproduced after permission has been obtained from BTC and provided that the source is acknowledged. This publication of the Trade for Development Centre does not necessarily represent the views of BTC. Photo courtesy: © iStockphoto/Mediaphotos Cover: © CTB Josiane Droeghag 2 Trade for Development Centre - BTC (Belgian Development Agency) ......................................................................................................................................... 3 ............................................................................................................................ 4 .................................................................................................................... 5 1.1 Consumption .................................................................................................................... 5 1.2 Imports .............................................................................................................................. 5 1.3 Supplying markets ........................................................................................................... 5 1.4 Exports ............................................................................................................................. -

Fichereseauchequecadhoc.Pdf

FICHE RÉSEAU CARTE OÙ ME FAIRE PLAISIR ? RETROUVEZ TOUS LES MAGASINS PARTENAIRES SUR + de 780 partenaires LA CARTE INTERACTIVE : L’APPLI MOBILE : + de 62 000 points de vente boutiques.cheque-cadhoc.fr à télécharger sur + de 160 sites e-commerce LES ENSEIGNES CADHOC CADHOC AU CŒUR DES VILLES PARMI LES 30 PRÉFÉRÉES DES FRANÇAIS un réseau de + de 10 000 commerces de proximité NOS ENSEIGNES PHARES MODE ADULTE & ENFANTS GRANDE DISTRIBUTION AUCHAN MODE ADULTE & ENFANTS Logo Patone MAISON / DÉCO Logo Quardi PUÉRICULTURE & RÉCRÉATIONS LOISIRS & SPORTS VOYAGES & DÉTENTE GASTRONOMIE GEMO * OOXOO* CASH CONVERTERS* PULSAT CITE DE L’ESPACE RESORT GRANDE DISTRIBUTION GENERALE D’OPTIQUE* OPTIC 2000 * CATENA* RESONANCES CITY SPORT CARREFOUR VOYAGES AUCHAN GERARD PASQUIER * OPTIC DUROC * CENTRAKOR* SAINT MACLOU CLUB MED GYM CENTER PARCS BLANCHE PORTE GRAIN DE MALICE* OPTICAL DISCOUNT COMPTOIR DE FAMILLE * SINGER* CLUB MOVING CLARION®* CARREFOUR GRANDOPTICAL* OPTIQUE MOISE * COMPTOIR DU VILLAGE * SOHO * COOK & GO* COMFORT™* CORA GUERIN JOAILLERIE OR ET PASSION CONFORAMA SOMELIA COURIR FASTHOTEL HYPER U* - SUPER U* H LANDERS OXBOW* CONNEXION STORY* CULTURA FRAM (MARCHE U*) HAPPY CHIC OZENCIA CONRAD ELECTRONIC TOP OFFICE* CULTURE VELO GALERIES LAFAYETTE VOYAGES INTERMARCHE* HEURE & MONTRES PALLIO / PALLIO STORE COTE NATURE* TOUSALON DAFY MOTO* GRAND BLEU SUPERMARCHES MATCH HEYRAUD PARFAIT ALIBI COULEURS DE TOLLENS TRUFFAUT DECATHLON* GRANDES ETAPES FRANÇAISES U EXPRESS HISTOIRE D’OR PARFUM D’O -AGORA UBALDI DECIMAS GROUPE HOTELIER MODE ADULTES ET HUNKEMOLLER -

Datecdec Situation Du Projet Projet Decis Cdec Recours

'$7(&'(& 6,78$7,21 352-(7 '(&,6 5(&2856 '$7(&1(& '(&,6 &1(& '8352-(7 &'(& Extension de 3200 m² la surface de vente du magasin BRIE COMTE ROBERT – ZAC du LEROY MERLIN à BRIE COMTE ROBERT Tuboeuf -ZAC du Tuboeuf, rue de la Butte au Berger- selon la DXWRULVDWLRQ répartition suivante : PðH[WpULHXUV (par le libre accès de la clientèle dans la cour de matériaux agrandie de 323 m²) et PðSRXUOHPDJDVLQ (la surface couverte passera de 5800 m² à 6200 m², la surface extérieure sera de 2800 m² , la surface de show room de 195 m² est inchangée ) La surface de vente globale passera donc de 5995 à 9195 m² (SA LEROY MERLIN France) PROVINS , 15-17 avenue du Extension de 651 m² la surface de vente du magasin Maréchal de Lattre de Tassigny INTERMARCHE (2499 m² après extension) DXWRULVDWLRQ (SA PROVINS DISTRIBUTION (PRODIS) ) PROVINS -3, avenue de la Voulzie Extension de de 300 m² la surface de vente (1000 m² (partie de l’ex local BUT) après extension) du magasin d’équipement de la personne à l’enseigne DEFI MODE DXWRULVDWLRQ (SA JMP EXPANSION) MAREUIL LES MEAUX, lieudit Création d’un ensemble de trois magasins d’une surface de la Hayette, 79, rue des Montaubans vente totale de 1880 m² comprenant un magasin à (ancien site JARDILAND) l’enseigne MAXI TOYS (jeux et jouets) de 800 m², un DXWRULVDWLRQ magasin à l’enseigne AUBERT (puériculture et layette) de 550 m² et un magasin à l’enseigne CASA (arts de la table et décoration) de 530 m² (Sarl PAGESTIM) '$7(&'(& 6,78$7,21 352-(7 '(&,6 5(&2856 '$7(&1(& '(&,6 &1(& '8352-(7 &'(& extension de 290 m² la surface de vente (1440 m² après DAMMARIE LES LYS extension) du magasin de meubles FLY –Rue A. -

VIANNEY MULLIEZ : C’Est Un Beau Cadeau D’Anniversaire, Pour Les 50 Ans De Notre Entreprise, Que De Constater Combien L’Histoire Nous a Donné Raison

VIANNEY MULLIEZ : C’est un beau cadeau d’anniversaire, pour les 50 ans de notre entreprise, que de constater combien l’Histoire nous a donné raison. Chez Auchan, nous n’en tirons aucune vanité, mais comment ne pas nous réjouir du choix judicieux qu’a fait, en 1961, notre fondateur Gérard Mulliez. D’emblée, il nous a doté d’une vision et d’une identité forte en misant résolument sur les valeurs humaines et en décidant que, chez Auchan, jamais on ne transigerait avec celles-ci. ARNAUD MULLIEZ : Des valeurs si ancrées dans notre culture d’entreprise qu’elles font notre réputation et notre fierté. Pour nous, et dans tous nos métiers, il importe que le « process » soit au service de l’Homme et cela ne doit jamais être l’inverse. Cette approche prend tout son L’EÉDITO DE VIANNEY MULLIEZ ET D’ARNAUD MULLIEZ ème Edito sens, au début de ce XXI siècle, dans un monde économique globalisé que la récente crise a ébranlé dans ses certitudes. Les experts, les observateurs expliquent cette crise, qui est d’abord une crise de confiance, par le fait que nombre de managers auraient trop misé sur le profit et le court terme. VIANNEY MULLIEZ : « Il faut absolument remettre l’homme au cœur de l’entreprise » insiste-t-on aujourd’hui. 19612011 Mais, chez Auchan, l’Homme est depuis toujours « la » priorité pour les dirigeants, dans tous nos différents métiers basés sur notre expertise de la consommation et fédérés au sein de notre groupe. Qu’il s’agisse de la grande distribution, de la banque, de l’immobilier commercial ou d’Internet. -

Producer/Retailer Contractual Relationships in the Fishing Sector : Food Quality, Procurement and Prices Stéphane Gouin, Erwan Charles, Jean-Pierre Boude

Producer/retailer Contractual Relationships in the fishing sector : food quality, procurement and prices Stéphane Gouin, Erwan Charles, Jean-Pierre Boude, . European Association of Fisheries Economists To cite this version: Stéphane Gouin, Erwan Charles, Jean-Pierre Boude, . European Association of Fisheries Economists. Producer/retailer Contractual Relationships in the fishing sector : food quality, procurement and prices. 16th Annual Conference of the European Association of Fisheries Economists, European Association of Fisheries Economists (EAFE). FRA., Apr 2004, Roma, Italy. 15 p. hal-02311416 HAL Id: hal-02311416 https://hal.archives-ouvertes.fr/hal-02311416 Submitted on 7 Jun 2020 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Distributed under a Creative Commons Attribution - NonCommercial - NoDerivatives| 4.0 International License t XVIth Annual EAFE Conference, Roma, April 5-7th 2004 I EAFE, Romu, April 5-7th 2004 Producer/retailer Contractual Relationships in the fTshing sector : food quality, procurement and prices Gouin 5., Charles 8., Boude fP. Agrocampus Rennes Département d'Economie Rurale et Gestion 65, rue de Saint Brieuc CS 84215 F 35042 Rennes cedex gouin@agrocampus-rennes. fr boude@agrocampus-rennes. fr and *CEDEM Université de Bretagne Occidentale 12, rue de Kergoat BP 816 29285 Brest cedex erwan. -

Healthier, Tastier Food

HEALTHIER, TASTIER FOOD. NB: FOR OPTIMUM NAVIGATION, PLEASE DOWNLOAD AND VIEW THIS PDF IN ADOBE ACROBAT. ANNUAL REPORT 2021 CONTENTS STRATEGIC REPORT 2 Our purpose Our business today 10 At a glance 12 Chair’s statement 14 Chief Executive’s review 20 Our world 22 Our business model 24 Our strategy 26 Key performance indicators Review of the year 32 Food & Beverage Solutions 36 Primary Products 40 Innovation and Commercial Development 42 Global Operations 44 Chief Financial Officer’s introduction 46 Group financial review 50 Our people 53 Equity, diversity and inclusion 54 Community involvement 56 Environment, health and safety 66 Task Force on Climate-related Financial Disclosures 68 Risk Report GOVERNANCE 80 Board of Directors 84 Executive Committee 86 Corporate governance 101 Nominations Committee Report 104 Audit Committee Report 110 Directors’ Remuneration Report 129 Directors’ Report 131 Directors’ statement of responsibilities FINANCIAL STATEMENTS 134 Independent Auditor’s Report to the members of Tate & Lyle PLC 142 Consolidated income statement 143 Consolidated statement of comprehensive income 144 Consolidated statement of financial position 145 Consolidated statement of cash flows 146 Consolidated statement of changes in equity Tate & Lyle is a global 147 Notes to the consolidated financial statements provider of ingredients 194 Parent Company financial statements and solutions for the USEFUL INFORMATION 202 Group five-year summary 204 Additional information food, beverage and 205 Information for investors 207 Glossary industrial markets. 208 Definitions/explanatory notes DOWNLOAD THE FULL ANNUAL REPORT 2021 Download at www.tateandlyle.com STRATEGIC REPORT NB: FOR OPTIMUM NAVIGATION, PLEASE DOWNLOAD AND VIEW THIS PDF IN ADOBE ACROBAT. -

Retail Food Sector Retail Foods France

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 9/13/2012 GAIN Report Number: FR9608 France Retail Foods Retail Food Sector Approved By: Lashonda McLeod Agricultural Attaché Prepared By: Laurent J. Journo Ag Marketing Specialist Report Highlights: In 2011, consumers spent approximately 13 percent of their budget on food and beverage purchases. Approximately 70 percent of household food purchases were made in hyper/supermarkets, and hard discounters. As a result of the economic situation in France, consumers are now paying more attention to prices. This situation is likely to continue in 2012 and 2013. Post: Paris Author Defined: Average exchange rate used in this report, unless otherwise specified: Calendar Year 2009: US Dollar 1 = 0.72 Euros Calendar Year 2010: US Dollar 1 = 0.75 Euros Calendar Year 2011: US Dollar 1 = 0.72 Euros (Source: The Federal Bank of New York and/or the International Monetary Fund) SECTION I. MARKET SUMMARY France’s retail distribution network is diverse and sophisticated. The food retail sector is generally comprised of six types of establishments: hypermarkets, supermarkets, hard discounters, convenience, gourmet centers in department stores, and traditional outlets. (See definition Section C of this report). In 2011, sales within the first five categories represented 75 percent of the country’s retail food market, and traditional outlets, which include neighborhood and specialized food stores, represented 25 percent of the market. In 2011, the overall retail food sales in France were valued at $323.6 billion, a 3 percent increase over 2010, due to price increases. -

Overseas Packaging Study Tour VAMP.006 1996

Overseas packaging study tour VAMP.006 1996 Prepared by: B. Lee ISBN: 1 74036 973 4 Published: June 1996 © 1998 This publication is published by Meat & Livestock Australia Limited ABN 39 081 678 364 (MLA). Where possible, care is taken to ensure the accuracy of information in the publication. Reproduction in whole or in part of this publication is prohibited without the prior written consent of MLA. MEAT & LIVESTOCK AUSTRALIA CONTENTS 1.0 EXECUTIVE SUMMARY ............................................ 1 2.0 BACKGROUND .................................................... 4 3.0 THE INTERNATIONAL STUDY TOUR .............. .................. 6 3.1 Objectives of the International Study Tour ................................. 6 3.2 Study Tour Itinerary and Dates .......................................... 6 3.3 The Study Team ...................................................... 6 4.0 SUMMARY OF SITE VISITS ......................................... 7 4.1 Taiwan ............................................................. 7 4.2 Hong Kong .......................................................... 8 4.3 France .............................................................. 9 4.4 Holland ............................................................ l 0 4.5 United Kingdom ..................................................... 13 4.6 Canada ............................................................ 15 4.7 Summary Comments of Site Visits by Study Group ......................... 17 5.0 KEY FINDINGS FROM THE STUDY TOUR ....... .................... 18 5.1