The Evolution of the Financial Services Industry and Its Impact on U.S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sedgwick, Detert, Moran & Arnold

SEDGWICK, DETERT, MORAN & ARNOLD NICHOLAS W. HELDT (Bar No. 083601) 2 DIANE T. GORCZYCA (Bar No. 201203) One Embarcadero Center, 16th Floor 3 San Francisco, CA 94111-3628 Telephone: (415) 781-7900 4 Facsimile: (415) 781-2635 5 Attorneys for Defendant RSR WHOLESALE GUNS, INC. 6 7 8 SUPERIOR COURT OF THE STATE OF CALIFORNIA 9 FOR THE CITY AND COUNTY OF SAN FRANCISCO 10 11 THE PEOPLE OF THE STATE OF ) CASE NO. 303753 CALIFORNIA, et aI., ) 12 ) RSR WHOLESALE GUNS, INC.'S Plaintiffs, ) RESPONSES TO PLAINTIFFS' FIRST 13 ) SET OF FORM INTERROGATORIES vs. ) 14 ) ARCADIA MACHINE & TOOL, et aI., ) 15 ) Defendants. ) 16 ) 17 18 PROPOUNDING PARTY: Plaintiffs PEOPLE OF THE STATE OF CALIFORNIA 19 RESPONDING PARTY: Defendant RSR WHOLESALE GUNS, INC. 20 SET NUMBER: ONE (1) 21 Defendant RSR WHOLESALE GUNS, INC. (hereinafter "RSR" or 22 "Defendant") responds to Plaintiffs' First Set of Form Interrogatories as follows: 23 FORM INTERROGATORY NO. 1.1: 24 State the name, ADDRESS, telephone number, and relationship to you of each 25 PERSON who prepared or assisted in the preparation of the responses to these interrogatories. 26 (Do not identify anyone who simply typed or reproduced the response.) SEDGWICK. 27 RESPONSE TO INTERROGATORY NO. 1.1: DETERT. MORAN & ARNOLD 28 The responses to these interrogatories were prepared by outside counsel to One Embarcadero Center Sixteenth Floor San F..... ci.sco, California 94111.,'!628 - 1 - TeL 415. 781 . 7900 PRO-SF/51086 RSR WHOLESALE GUNS, INC.'S RESPONSES TO PLAINTIFFS' FIRST SET OF FORM INTERROGATORiES RSR, Nicholas W. Heldt and Diane T. Gorczyca of Sedgwick, Detert, Moran & Arnold, based 2 on infonnation provided by RSR's Senior Vice President and in-house legal counsel, Michael 3 Saporito. -

SAN FRANCISCO 2Nd Quarter 2014 Office Market Report

SAN FRANCISCO 2nd Quarter 2014 Office Market Report Historical Asking Rental Rates (Direct, FSG) SF MARKET OVERVIEW $60.00 $57.00 $55.00 $53.50 $52.50 $53.00 $52.00 $50.50 $52.00 Prepared by Kathryn Driver, Market Researcher $49.00 $49.00 $50.00 $50.00 $47.50 $48.50 $48.50 $47.00 $46.00 $44.50 $43.00 Approaching the second half of 2014, the job market in San Francisco is $40.00 continuing to grow. With over 465,000 city residents employed, the San $30.00 Francisco unemployment rate dropped to 4.4%, the lowest the county has witnessed since 2008 and the third-lowest in California. The two counties with $20.00 lower unemployment rates are neighboring San Mateo and Marin counties, $10.00 a mark of the success of the region. The technology sector has been and continues to be a large contributor to this success, accounting for 30% of job $0.00 growth since 2010 and accounting for over 1.5 million sf of leased office space Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 2012 2012 2012 2013 2013 2013 2013 2014 2014 this quarter. Class A Class B Pre-leasing large blocks of space remains a prime option for large tech Historical Vacancy Rates companies looking to grow within the city. Three of the top 5 deals involved 16.0% pre-leasing, including Salesforce who took over half of the Transbay Tower 14.0% (delivering Q1 2017) with a 713,727 sf lease. Other pre-leases included two 12.0% full buildings: LinkedIn signed a deal for all 450,000 sf at 222 2nd Street as well 10.0% as Splunk, who grabbed all 182,000 sf at 270 Brannan Street. -

Resolution Plan 2018 Public Section

RESOLUTION PLAN 2018 PUBLIC SECTION TABLE OF CONTENTS Page INTRODUCTION ......................................................................................................................... 1 1. Names of Material Entities .................................................................................... 3 2. Description of Core Business Lines ....................................................................... 3 3. Summary Financial Information Regarding Assets, Liabilities, Capital, and Major Funding Sources. .................................................................................. 4 4. Description of Derivatives and Hedging Activities ............................................... 7 5. Memberships in Material Payment, Clearing, and Settlement Systems ................ 7 6. Description of Foreign Operations......................................................................... 8 7. Identities of Material Supervisory Authorities ...................................................... 8 8. Identities of Principal Officers ............................................................................... 9 9. Corporate Governance Structure and Processes Related to Resolution Planning ............................................................................................................... 10 10. Material Management Information Systems ........................................................ 11 11. High Level Description of Resolution Strategy ................................................... 12 -i- INTRODUCTION Section -

Wells Fargo International Equity Fund

QUARTERLY MUTUAL FUND COMMENTARY Q4 2020 | All information is as of 12/31/2020 unless otherwise indicated. Wells Fargo International Equity Fund Quarterly review GENERAL FUND INFORMATION ● The International Equity Fund underperformed the MSCI ACWI ex USA Index (Net) Ticker: WFENX and the MSCI ACWI ex USA Value Index (Net) for the quarter that ended December 31, 2020. Portfolio managers: Dale A. Winner, ● Performance was driven largely by stock selection, with positive contributions coming CFA®; and Venk Lal from investments in the industrials and materials sectors as well as in China/Hong Subadvisor: Wells Capital Kong and Canada. Management Inc. ● Positions in information technology (IT) and health care as well as in France and Japan Category: Foreign large value detracted from performance. Market review FUND STRATEGY ● Maintains a core equity style that International equity markets initially declined in October before advancing 19.6% in the emphasizes bottom-up stock final two months of the year as multiple COVID-19 vaccines reached 90%+ efficacy and selection based on rigorous, uncertainty surrounding the U.S. presidential election receded, resulting in a 17.0% in-depth, fundamental company return for the MSCI All Country World ex USA Index (Net) in the fourth quarter, the research highest quarterly return since the third quarter of 2009. In this environment, the Global ● Uses a bottom-up research process Purchasing Managers’ Index (PMI) reached 53.3 in October, the highest level since that targets companies with August 2018, but fell back to 52.7 in December, still in expansionary territory. Emerging underestimated earnings growth markets outperformed developed markets and sovereign yields saw mixed fluctuations potential or those trading at during the period, including the U.S. -

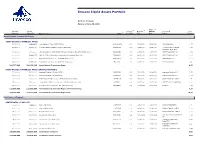

Invesco Liquid Assets Portfolio

Invesco Liquid Assets Portfolio Portfolio Holdings Data as of June 30, 2021 4 2 3 Final Principal Market 1 Coupon/ Maturity Maturity Associated % of Amount Value ($) Name of Issue CUSIP Yield (%) Date Date Issuer Portfolio Asset Backed Commercial Paper ASSET-BACKED COMMERCIAL PAPER 25,000,000 24,998,958 Ionic Capital III Trust (CEP-UBS AG) 46220WUG9 0.13 07/16/2021 07/16/2021 UBS GROUP AG 1.27 37,777,000 37,774,140 Lexington Parker Capital Company (Multi-CEP) 52953AUV5 0.15 07/29/2021 07/29/2021 Lexington Parker Capital 1.93 Company (Multi-CEP) 10,500,000 10,500,000 LMA Americas LLC (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QXR6 0.05 10/25/2021 10/25/2021 CREDIT AGRICOLE SA 0.54 40,000,000 39,992,272 LMA SA (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QW30 0.24 09/03/2021 09/03/2021 CREDIT AGRICOLE SA 2.04 20,000,000 20,000,000 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JW26 0.14 09/02/2021 09/02/2021 BNP PARIBAS SA 1.02 55,000,000 54,964,250 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JY81 0.14 11/08/2021 11/08/2021 BNP PARIBAS SA 2.80 188,277,000 188,229,620 Asset-Backed Commercial Paper 9.60 ASSET-BACKED COMMERCIAL PAPER (INTEREST BEARING) 50,000,000 50,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VG1 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 2.55 25,000,000 25,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VL0 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 1.27 10,000,000 10,000,000 Bedford Row Funding Corp. -

Midcap Financial Secures Credit Facility and Strategic Relationship with Silicon Valley Bank

MidCap Financial Secures Credit Facility and Strategic Relationship with Silicon Valley Bank MidCap Financial, LLC, a leading commercial finance company focused exclusively on middle market healthcare companies, announced it has closed a credit facility with Silicon Valley Bank, the premier commercial bank for companies in the technology, life science, and venture capital industries and a subsidiary of SVB Financial Group (Nasdaq: SIVB). The facility is a three year, revolving loan that provides financing against MidCap’s life sciences loans. The credit facility is part of an overall strategic relationship, pursuant to which MidCap and Silicon Valley Bank will collaborate on senior debt transactions with healthcare service providers and life sciences companies. “We are pleased to have Silicon Valley Bank as a partner,” said Will Gould, President, Specialty Finance, of MidCap Financial. “Many of our professionals have worked closely with the people at SVB for years, so formalizing these relationships is a natural fit. We believe that combining SVB’s premiere status in the banking community serving the life sciences and venture capital industries with our healthcare lending expertise will enable us jointly to provide best in class service to our customers for all of their financial needs.” ”In everything we do, we aim to provide the best products, services and connections to help our clients grow,” said Pete Scott, Region Manager specializing in life sciences for Silicon Valley Bank. “Dedicated to the life science sector, we are pleased to deepen our relationship with MidCap Financial in order to give our life science clients even more options and opportunities to succeed.” Silicon Valley Bank’s nationwide Life Science Practice banks more than 50 percent of all early stage life cycle companies. -

2020 Edition 01 03 05 07 10 12

THE GREATER PHOENIX TECH STORY 2020 EDITION 01 03 05 07 10 12 The Greater Population Workforce Education Coworking Greater Phoenix Tech Phoenix Roots Tech Story TABLE OF CONTENTS 14 15 17 19 20 21 23 Data Company Cost of Venture Regulatory Operational Quality of Centers Profiles Doing Capital Policy Affordability Life Business and Private Equity THE GREATER PHOENIX TECH STORY 01 ©2020 GPEC & CBRE 02 >> Greater Phoenix is an emerging tech market. The region is sought after for its talent, collaborative environment, business-friendly culture and quality of life. Emerging tech companies choose Greater Phoenix to establish their footprints, test their technologies and scale. Over the last 70 years, Greater Phoenix has created a diversified tech ecosystem home to R&D, high- tech manufacturing, software companies and next-generation technologies. Today, there are roughly 500 software companies that call Greater Phoenix home. Companies including GoDaddy, Carvana, and LifeLock went from startups to household names right in our own backyard. New and innovative companies from coast to coast and around the globe seek Greater Phoenix where they can secure top talent and provide a high quality of life for their employees. STORY PHOENIX TECH THE GREATER Talent and Education Collaboration Startups and established tech firms alike find The Greater Phoenix ecosystem has enabled that Greater Phoenix works for them. Over long-time businesses, emerging disruptors, 85,000 high-tech employees are in the region. educational institutions and the public to work Tech companies can leverage the large and together to better the region. In Phoenix, it is talented workforce fueled by Arizona State easy to be new. -

Healthcare Investments and Exits | Mid-Year Report 2020 6 Date

MIDANUAL-YEAR REPORT Healthcare 2020 Investments and Exits Biopharma | HealthTech | Dx/Tools | Device Follow @SVB_Financial Engage #SVBHealthcare MID-YEAR Table of Contents REPORT 2020 Page Page Page Page 3 5 24 35 Highlights Investments Exits 2020 Outlook HealthcareHealthcare Investments Investments and & Exits | Mid-Year Report 2020 2 Healthcare Investments: Mid-Year 2020 Venture fundraising in healthcare soared to $10.4B in the first half of 2020, nearly Silicon Valley Bank Market Stats* matching 2019’s full-year record. Mezzanine “Mezz” markups and great IPO performance have driven outsized returns, allowing investors to raise new funds, many of which were larger than their previous fund. Company investment also spiked. 1H 2020 produced the largest two-quarter investment 53% period ever for venture-backed healthcare companies. Biopharma and dx/tools saw increases in investment vs. 1H 2019, despite financial market turbulence and negative of all VC-backed US impacts to many companies due to COVID-19. healthcare companies that raised rounds in 1H 2020 Biopharma Series A was stable in the first half, while overall investment is on pace for worked with SVB. record dollars in 2020. We continued to see a significant number of large crossover-led mezzanine financings in Q1 and Q2 2020. This mezzanine activity exceeds 2019’s pace and is a strong, positive sign for continued IPO activity. of the $15B in venture funding HealthTech investments remained steady in 1H 2020 but showed an 18% increase in deals raised in the US in 1H 2020 was vs. 1H 2019, solidifying healthtech as the most prolific deal sector. Alternative care, which $1 0B by companies that work with SVB. -

Quarterly Report DNB Bank ASA 3Q19

DNB Bank A company in the DNB Group Third quarter report 2019 (Unaudited) Q3 Financial highlights Income statement DNB Bank Group 3rd quarter 3rd quarter January-September Full year Amounts in NOK million 2019 2018 2019 2018 2018 Net interest income 10 150 9 299 29 367 27 634 37 388 Net commissions and fees 1 536 1 431 4 799 4 721 6 605 Net gains on financial instruments at fair value 1 523 611 3 622 905 1 351 Other operating income 612 581 1 839 1 939 2 522 Net other operating income 3 672 2 623 10 260 7 564 10 478 Total income 13 822 11 922 39 627 35 198 47 866 Operating expenses (5 318) (5 114) (16 108) (15 189) (20 681) Restructuring costs and non-recurring effects (134) (26) (177) (106) (565) Pre-tax operating profit before impairment 8 370 6 782 23 343 19 902 26 620 Net gains on fixed and intangible assets (40) (3) (43) 480 529 Impairment of financial instruments (1 247) (11) (2 014) 374 139 Pre-tax operating profit 7 083 6 769 21 286 20 756 27 288 Tax expense (1 417) (1 354) (4 257) (4 151) (4 976) Profit from operations held for sale, after taxes (36) (42) (117) (63) (204) Profit for the period 5 631 5 373 16 912 16 542 22 109 Balance sheet 30 Sept. 31 Dec. 30 Sept. Amounts in NOK million 2019 2018 2018 Total assets 2 576 850 2 307 710 2 387 216 Loans to customers 1 673 924 1 598 017 1 561 867 Deposits from customers 983 472 940 087 995 154 Total equity 215 989 207 933 200 665 Average total assets 2 543 839 2 434 354 2 454 510 Key figures and alternative performance measures 3rd quarter 3rd quarter January-September Full year 2019 -

Top Investors Dallas Regional Chamber

DALLAS REGIONAL CHAMBER | TOP INVESTORS DALLAS REGIONAL CHAMBER REGIONAL DALLAS JBJ Management Norton Rose Fulbright Silicon Valley Bank The Fairmont Hotel Top Investors JE Dunn Construction NTT DATA Inc. Simmons Bank The Kroger Co. Jim Ross Law Group PC Omni Dallas Hotel Slalom The University of The Dallas Regional Chamber (DRC) recognizes the following companies and organizations for their membership investment at JLL Omniplan, Inc. Smoothie King Texas at Arlington one of our top levels. Companies in bold print are represented on the DRC Board of Directors. For more information about the Jones Day Omnitracs, LLC SMU - Southern Methodist Thompson & Knight LLP University benefits of membership at these levels call (214) 746-6600. JPMorgan Chase & Co. Oncor Thompson Coburn Southern Dock Products Katten Muchin Rosenman LLP On-Target Supplies Thomson Reuters Southern Glazer’s Wine and KDC Real Estate Development & & Logistics Ltd TIAA Spirits 1820 Productions Bell Nunnally Crowe LLP Google Investments Options Clearing Corporation T-Mobile | Southwest Airlines 4Front Engineered Solutions BGSF CSRS goPuff TOP INVESTORS Ketchum Public Relations Origin Bank Tom Thumb - Albertsons 7-Eleven, Inc. Billingsley Company CyrusOne Granite Properties Southwest Office Systems, Inc. Kilpatrick Townsend ORIX Corporation USA Town of Addison A G Hill Partners LLC BKD LLP Dallas Baptist University Grant Thornton LLP & Stockton LLP Spacee Inc. OYO Hotels and Homes Toyota Motor North America ABC Home & Commercial bkm Total Office of Texas Dallas College Green Brick Partners Kimberly-Clark Corporation Spectra Pacific Builders Transworld Business Advisors - Services Kimley-Horn and Associates Spencer Fane LLP Blackmon Mooring & BMS CAT Dallas Cowboys Football Club Greenberg Traurig Pape-Dawson Downtown Dallas Accenture Ltd. -

2008 – December

DEPARTMENT OF FINANCIAL INSTITUTIONS SUMMARY OF PENDING APPLICATIONS AS OF DECEMBER 2008 APPLICATION TYPE PAGE NO. BANK APPLICATION NEW BANK 1 ACQUISITION OF CONTROL 2 CONVERSION TO STATE CHARTER 3 NEW BRANCH 3 NEW PLACE OF BUSINESS 8 NEW EXTENSION OFFICE 10 HEAD OFFICE RELOCATION 10 HEAD OFFICE REDESIGNATION 11 BRANCH OFFICE RELOCATION 11 PLACE OF BUSINESS RELOCATION 13 DISCONTINUANCE OF BRANCH OFFICE 13 DISCONTINUANCE OF PLACE OF BUSINESS 15 APPLICATION PURSUANT TO SECTION 772 16 INDUSTRIAL BANK APPLICATION CONVERSION TO STATE CHARTER 16 ACQUISITION OF CONTROL 16 NEW BRANCH 17 HEAD OFFICE RELOCATION 17 DISCONTINUANCE OF BRANCH 17 DISCONTINUANCE OF PLACE OF BUSINESS 17 CHANGE OF NAME 18 PREMIUM FINANCE COMPANY APPLICATION NEW PREMIUM FINANCE COMPANY 18 ACQUISITION OF CONTROL 19 MAIN OFFICE RELOCATION 20 FOREIGN (OTHER NATION) BANK APPLICATION NEW OFFICE 20 DISCONTINUANCE 20 FOREIGN (OTHER STATE) BANK APPLICATION NEW FACILITY 21 CREDIT UNION APPLICATION NEW CREDIT UNION 22 MERGER 22 NEW BRANCH OF FOREIGN (OTHER STATE) CREDIT UNION 23 TRANSMITTER OF MONEY ABROAD APPLICATION NEW TRANSMITTER 23 ACQUISITION OF CONTROL 23 VOLUNTARY SURRENDER OF LICENSE 24 1 BANK APPLICATION NEW BANK Filed: 2 Approved: 4 Opened: 1 AMERICAN CEDARS BANK 500 North Central Avenue, Glendale, Los Angeles County Correspondent: David E. Abshier LECG 550 South Hope Street, Suite 2150 Los Angeles, CA 90071 (213) 243-3700 Filed: 9/28/07 EL CAMINO BANK 20946 Devonshire Street, Chatsworth, Los Angeles County Correspondent: James H. Avery The Avery Company LLC P.O. Box 3009 San Luis Obispo, CA 93403 (805) 544-5477 Filed: 5/9/08 FORD GROUP BANK 3501 Jamboree Road, Newport Beach, Orange County Correspondent: Charles E. -

US PE Lending League Tables

US PE Lending League Tables Q1 2020 Contents Credits & Contact PitchBook Data, Inc. Introduction 3 John Gabbert Founder, CEO Adley Bowden Vice President, US region 4-7 Market Development & Analysis PE deals 8-10 Content Aria Nikkhoui Data Analyst II Debt 11-12 Madison Bond Senior Research Associate, Debt Industry 13-14 Bhushan Artani Research Associate, Debt Keenan Durham Data Set Team Law firms 15 Lead, Debt Contact PitchBook Research [email protected] Cover design by Kelilah King Click here for PitchBook’s report methodologies. Introduction The US PE Lending League Tables are not only one of our PDF with similar interactive online rankings only. As a few younger editions of quarterly publications, but also they technical kinks remain to be worked out, we are currently represent a unique perspective on the credit markets. still producing the PDF edition of Lending League Tables They also can proffer a pulse on private lending’s health only. overall; for example, tallies have grown considerably more interesting in light of the pandemic that began to impact As always, we welcome your feedback, so do not hesitate transactional volume toward the end of Q1 2020. Future to reach out to [email protected]. editions will offer good indicators of where activity was able to stay most resilient as volatility surged. In addition, at the start of this year, we launched our Garrett James Black first-ever interactive league tables. We are focusing Senior Manager, Custom Research on gathering user feedback and associated data on & Publishing performance