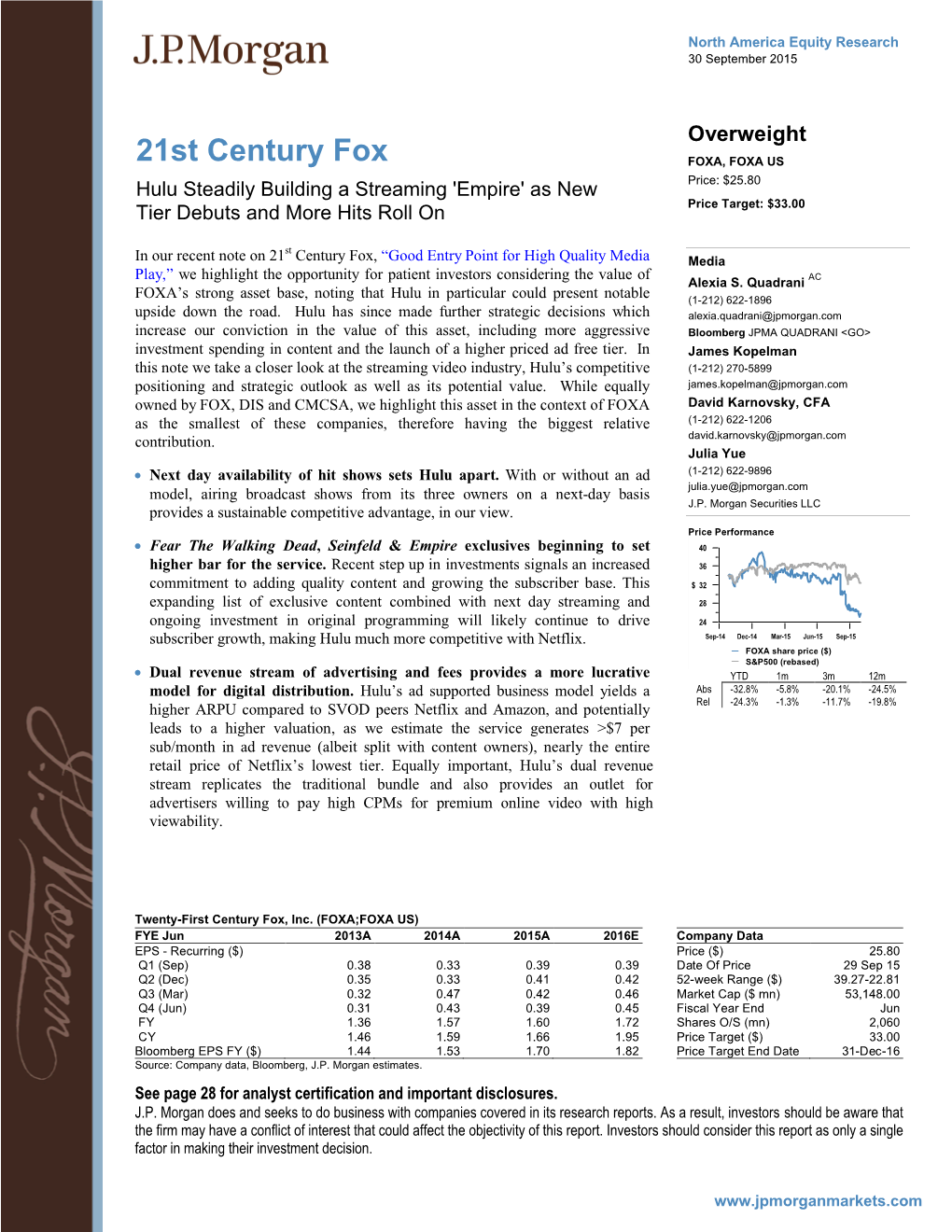

JPM-Equity-Research-Report-Hulu.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ABC ME Program Guide: Week 28 Index

1 | P a g e ABC ME Program Guide: Week 28 Index Index Program Guide .............................................................................................................................................................. 3 Sunday, 4 July 2021 ............................................................................................................................................... 3 Monday, 5 July 2021 ............................................................................................................................................. 7 Tuesday, 6 July 2021 ........................................................................................................................................... 11 Wednesday, 7 July 2021 ...................................................................................................................................... 15 Thursday, 8 July 2021 .......................................................................................................................................... 19 Friday, 9 July 2021 ............................................................................................................................................... 23 Saturday, 10 July 2021 ........................................................................................................................................ 27 NOTE: Program times may differ in some states if viewing on VAST or Foxtel. More information can be found at ABC Help. 2 | P a g e ABC ME Program Guide: Week 28 Sunday, 4 July 2021 Program -

OCTOBER 2015 David Haring, Editor & Photographer • Design by Hilliker Designs

DLC HOSTS Colleagues FROM Madagascar DUKE ANDREA KatZ, Curator, LIVING ANIMAL COLLECTIONS LEMUR CENTER In May and June, the Duke Lemur Center discuss ways that we can collaborate further to achieve com- (DLC) had the pleasure and great honor to mon conservation goals. The discussions were expanded host two Malagasy colleagues: Eric Robso- when Eric and Bernard attended the Prosimian Taxon Advi- manitrandrasana of the Ministry of the Envi- sory Group’s annual meeting with several members of the ronment, Ecology, Oceans and Forests and DLC technician staff. As a result, in July an official “Accord Bernard Iambana, Manager of Zoo Ivoloina/ of Collaboration” between the Government of Madagascar, Conservation Manager, Madagascar Fauna and American (AZA) and European (EAZA) groups was final- Flora Group. We would like to express our ized- to promote global ex situ and in situ conservation of most heartfelt thanks to the Kris and Peter the critically endangered blue-eyed black lemur (Eulemur Norvig Family Fund for supporting this inter- flavifrons). Named on the 2012, 2013 and 2014 IUCN List of national exchange. the 25 Most Endangered Primates, this species desperately The purpose of their visit was to learn first- needs cooperative global management to survive. And as hand about the DLC’s best practices for lemur the only North American institution successfully breeding care and management. In Madagascar, Eric is blue-eyed black lemurs, the DLC stands ready to do all we the coordinator of a new government initiative possibly can. to improve husbandry standards and breeding management for hundreds of lemurs that are kept in Madagascar’s zoos and private wildlife parks. -

Weekend Glance

Friday, Dec. 1, 2017 Vol. 11 No. 43 12040 Foster Road, Norwalk, CA 90650 Norwalk Norwalk City Council votes restaurant to give themselves grades Donut King 12000 Rosecrans Ave. NOVEMBER 30 12 more months in office Date Inspected: 11/17/17 FridayWeekend74˚ Neighborhood Watch meeting Grade: B CITY COUNCIL: Council members at a DATE: Thursday, Nov. 30 Glance choose to extend elections one year Buy Low Market TIME: 6:30 pm under legislation signed by Gov. Jerry Saturday 75˚⁰ LOCATION: Paddison Elementary 10951 Rosecrans Ave. 68 Brown. Date Inspected: 11/13/17 Friday DECEMBER 2 Grade: B By Raul Samaniego SnowFest and Christmas Tree Contributor Wienerschnitzel Sunday 71˚70⁰ Lighting 11660 Imperial Hwy. Saturday DATE: Saturday, Dec. 2 NORWALK – The Norwalk City Date Inspected: 11/15/17 TIME: 12-8 pm Council voted 5-0 on November Grade: A 21, to approve Ordinance 17-1698 LOCATION: City Hall lawn which called for the changing of Waba Grill Holiday Sonata Election Dates to comply with 11005 Firestone Blvd. California Senate Bill 415. DATE: Saturday, Dec. 2 Date Inspected: 11/16/17 TIME: 4-9 pm For Norwalk residents, it means Grade: A that with the approval of the Norwalk’s next election will be in 2020. Photo courtesy city of LOCATION: Uptown Whittier ordinance, “all five council members Norwalk Ana’s Bionicos have added another 12 months to 11005 Firestone Blvd. DECEMBER 5 their terms,” according to City Clerk numbered years to even, it could California’s history. Date Inspected: 11/16/17 Theresa Devoy increase the voter turnout for those City Council meeting This transition was mandated Grade: A elections. -

THE NATIONAL ACADEMY of TELEVISION ARTS & SCIENCES ANNOUNCES NOMINATIONS for the 44Th ANNUAL DAYTIME EMMY® AWARDS

THE NATIONAL ACADEMY OF TELEVISION ARTS & SCIENCES ANNOUNCES NOMINATIONS FOR THE 44th ANNUAL DAYTIME EMMY® AWARDS Daytime Emmy Awards to be held on Sunday, April 30th Daytime Creative Arts Emmy® Awards Gala on Friday, April 28th New York – March 22nd, 2017 – The National Academy of Television Arts & Sciences (NATAS) today announced the nominees for the 44th Annual Daytime Emmy® Awards. The awards ceremony will be held at the Pasadena Civic Auditorium on Sunday, April 30th, 2017. The Daytime Creative Arts Emmy Awards will also be held at the Pasadena Civic Auditorium on Friday, April 28th, 2017. The 44th Annual Daytime Emmy Award Nominations were revealed today on the Emmy Award-winning show, “The Talk,” on CBS. “The National Academy of Television Arts & Sciences is excited to be presenting the 44th Annual Daytime Emmy Awards in the historic Pasadena Civic Auditorium,” said Bob Mauro, President, NATAS. “With an outstanding roster of nominees, we are looking forward to an extraordinary celebration honoring the craft and talent that represent the best of Daytime television.” “After receiving a record number of submissions, we are thrilled by this talented and gifted list of nominees that will be honored at this year’s Daytime Emmy Awards,” said David Michaels, SVP, Daytime Emmy Awards. “I am very excited that Michael Levitt is with us as Executive Producer, and that David Parks and I will be serving as Executive Producers as well. With the added grandeur of the Pasadena Civic Auditorium, it will be a spectacular gala that celebrates everything we love about Daytime television!” The Daytime Emmy Awards recognize outstanding achievement in all fields of daytime television production and are presented to individuals and programs broadcast from 2:00 a.m.-6:00 p.m. -

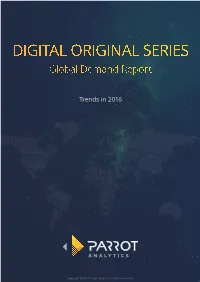

DIGITAL ORIGINAL SERIES Global Demand Report

DIGITAL ORIGINAL SERIES Global Demand Report Trends in 2016 Copyright © 2017 Parrot Analytics. All rights reserved. Digital Original Series — Global Demand Report | Trends in 2016 Executive Summary } This year saw the release of several new, popular digital } The release of popular titles such as The Grand Tour originals. Three first-season titles — Stranger Things, and The Man in the High Castle caused demand Marvel’s Luke Cage, and Gilmore Girls: A Year in the for Amazon Video to grow by over six times in some Life — had the highest peak demand in 2016 in seven markets, such as the UK, Sweden, and Japan, in Q4 of out of the ten markets. All three ranked within the 2016, illustrating the importance of hit titles for SVOD top ten titles by peak demand in nine out of the ten platforms. markets. } Drama series had the most total demand over the } As a percentage of all demand for digital original series year in these markets, indicating both the number and this year, Netflix had the highest share in Brazil and popularity of titles in this genre. third-highest share in Mexico, suggesting that the other platforms have yet to appeal to Latin American } However, some markets had preferences for other markets. genres. Science fiction was especially popular in Brazil, while France, Mexico, and Sweden had strong } Non-Netflix platforms had the highest share in Japan, demand for comedy-dramas. where Hulu and Amazon Video (as well as Netflix) have been available since 2015. Digital Original Series with Highest Peak Demand in 2016 Orange Is Marvels Stranger Things Gilmore Girls Club De Cuervos The New Black Luke Cage United Kingdom France United States Germany Mexico Brazil Sweden Russia Australia Japan 2 Copyright © 2017 Parrot Analytics. -

Network Totals

Network Totals Total CBS 66 SYNDICATED 66 Netflix 51 Amazon 49 NBC 35 ABC 33 PBS 29 HBO 12 Disney Channel 12 Nickelodeon 12 Disney Junior 9 Food Network 9 Verizon go90 9 Universal Kids 6 Univision 6 YouTube RED 6 CNN en Español 5 DisneyXD 5 YouTube.com 5 OWN 4 Facebook Watch 3 Nat Geo Kids 3 A&E 2 Broadway HD 2 conversationsinla.com 2 Curious World 2 DIY Network 2 Ora TV 2 POP TV 2 venicetheseries.com 2 VICELAND 2 VME TV 2 Cartoon Network 1 Comcast Watchable 1 E! Entertainment 1 FOX 1 Fuse 1 Google Spotlight Stories/YouTube.com 1 Great Big Story 1 Hallmark Channel 1 Hulu 1 ION Television 1 Logo TV 1 manifest99.com 1 MTV 1 Multi-Platform Digital Distribution 1 Oculus Rift, Samsung Gear VR, Google Daydream, HTC Vive, Sony 1 PSVR sesamestreetincommunities.org 1 Telemundo 1 UMC 1 Program Totals Total General Hospital 26 Days of Our Lives 25 The Young and the Restless 25 The Bold and the Beautiful 18 The Bay The Series 15 Sesame Street 13 The Ellen DeGeneres Show 11 Odd Squad 8 Eastsiders 6 Free Rein 6 Harry 6 The Talk 6 Zac & Mia 6 A StoryBots Christmas 5 Annedroids 5 All Hail King Julien: Exiled 4 An American Girl Story - Ivy & Julie 1976: A Happy Balance 4 El Gordo y la Flaca 4 Family Feud 4 Jeopardy! 4 Live with Kelly and Ryan 4 Super Soul Sunday 4 The Price Is Right 4 The Stinky & Dirty Show 4 The View 4 A Chef's Life 3 All Hail King Julien 3 Cop and a Half: New Recruit 3 Dino Dana 3 Elena of Avalor 3 If You Give A Mouse A Cookie 3 Julie's Greenroom 3 Let's Make a Deal 3 Mind of A Chef 3 Pickler and Ben 3 Project Mc² 3 Relationship Status 3 Roman Atwood's Day Dreams 3 Steve Harvey 3 Tangled: The Series 3 The Real 3 Trollhunters 3 Tumble Leaf 3 1st Look 2 Ask This Old House 2 Beat Bugs: All Together Now 2 Blaze and the Monster Machines 2 Buddy Thunderstruck 2 Conversations in L.A. -

TELÉFONOS 7870-9639 Y 7879-7787

OFERTA DE SERIES ANIMADAS TELÉFONOS 7870-9639 y 7879-7787 LLAMAR DESPUÉS DE LAS 10am HASTA LAS 8pm DE LUNES A SÁBADO SI NO ESTAMOS LE DEVOLVEREMOS LA LLAMADA PARA GRABAR EN MEMORIA Y DISCO DURO DIRÍJASE A LA CALLE BELASCOAIN # 317 BAJOS, ESQUINA A SAN RAFAEL. ESTA ABIERTO DESDE LAS 10am HASTA LAS 8pm. NUESTRO PLACER ES COMPLACER A NUESTROS CLIENTES. PRECIOS EN MEMORIA O DISCO DURO. 1 $ EN MONEDA NACIONAL POR CAPITULO MENSAJERIA GRATIS A TODOS LOS MUNICIPIOS DE LA HABANA Llevamos pedidos a su casa sin costo adicional siempre y cuando su pedido sea de 175 $ MN en adelante. ¡Gratis! la actualización del Antivirus. LLÁMENOS YA AL 78-70-96-39 Y AL 78-79-77-87 VISITE NUESTRO SITIO WEB seriesroly.com South Park [ADULTOS] País(es): USA Género(s): Comedia Sinopsis: South Park es una serie PARA ADULTOS de comedia animada distribuida por WarnerBros. Trata sobre las aventuras de cuatro niños que viven en el pequeño pueblollamado South Park, Colorado. South Park hace sátira y crítica de muchos aspectosde la cultura estadounidense y eventos históricos recientes, reta a las firmescreencias, y los tabúes y muy frecuentemente hace uso del humor negro. DOBLADA Temporada 1-6(13+18+17+17+14+17 Capítulos)[1997-*] Temporada 18(10 Capítulos)[2014] Temporada 21-23(10+10+10 Capítulos)[2017-2019] SUBTITULADA Temporada 7-16(15+14+14+14+14+14+14+14+14+14 Capítulos)[*-2011] Temporada 17-23(10+10+10+10+10+10+10 Capítulos)[2013-2019] Star Wars The Clone Wars País(es): USA Género(s): Fantástico, Comedia, Drama, Ciencia Ficción, Aventuras Sinopsis: Situada entre Star Wars Episodio II: El ataque de los clones y Star Wars Episodio III:La venganza de los Sith. -

45Th Annual Daytime Emmy Award Nominations Were Revealed Today on the Emmy Award-Winning Show, the Talk, on CBS

P A G E 1 6 THE NATIONAL ACADEMY OF TELEVISION ARTS & SCIENCES ANNOUNCES NOMINATIONS FOR THE 45th ANNUAL DAYTIME EMMY® AWARDS Mario Lopez & Sheryl Underwood to Host Daytime Emmy Awards to be held on Sunday, April 29 Daytime Creative Arts Emmy® Awards Gala on Friday, April 27 Both Events to Take Place at the Pasadena Civic Auditorium in Southern California New York – March 21, 2018 – The National Academy of Television Arts & Sciences (NATAS) today announced the nominees for the 45th Annual Daytime Emmy® Awards. The ceremony will be held at the Pasadena Civic Auditorium on Sunday, April 29, 2018 hosted by Mario Lopez, host and star of the Emmy award-winning syndicated entertainment news show, Extra, and Sheryl Underwood, one of the hosts of the Emmy award-winning, CBS Daytime program, The Talk. The Daytime Creative Arts Emmy Awards will also be held at the Pasadena Civic Auditorium on Friday, April 27, 2018. The 45th Annual Daytime Emmy Award Nominations were revealed today on the Emmy Award-winning show, The Talk, on CBS. “The National Academy of Television Arts & Sciences is excited to be presenting the 45th Annual Daytime Emmy Awards, in the historic Pasadena Civic Auditorium,” said Chuck Dages, Chairman, NATAS. “With an outstanding roster of nominees and two wonderful hosts in Mario Lopez and Sheryl Underwood, we are looking forward to a great event honoring the best that Daytime television delivers everyday to its devoted audience.” “The record-breaking number of entries and the incredible level of talent and craft reflected in this year’s nominees gives us all ample reasons to celebrate,” said David Michaels, SVP, and Executive Producer, Daytime Emmy Awards. -

A Consumer-Based Examination of Netflix Inc. Original Programming and Streaming Strategy

Streaming is the New Black: A Consumer-based Examination of Netflix Inc. Original Programming and Streaming Strategy A Thesis Submitted to the Faculty of Drexel University by Lindsay B. Strott in partial fulfillment of the requirements for the degree of Master of Science in Television Management March 2015 © Copy Right 2015 Lindsay B. Strott. All Rights Reserved i Acknowledgements Thank you to my thesis advisor Dr. Lydia Timmins and program director Al Tedesco for your guidance throughout my studies and the thesis writing process. I would also like to thank my family, friends, and classmates for their support and encouragement. ii Table of Contents List of Tables ............................................................................................................. vii List of Figures ........................................................................................................... viii List of Appendices ...................................................................................................... xi Abstract ...................................................................................................................... xii Chapter 1 : Introduction ............................................................................................ 1 1.1 Introduction ............................................................................................................. 1 1.2 Statement of the Problem ........................................................................................ 4 1.3 Background ............................................................................................................ -

Wisconsin-2018-Spring-Update.Pdf

Sales Workshop Taps Business Badger Network to Give Students a Head Start P. 6 WISCONSIN SCHOOL OF BUSINESS UPDATESPRING 2018 Unique Approach Sets Apart WSB’s Master of Accountancy Program P. 16 8 TO WATCH UNDER 40 Meet WSB alumni who are making their mark P. 8 History’s Witness Roger Ervin takes a business approach to global relief effortsP. 18 LETTER FROM THE DEAN ABOUT BARRY GERHART Barry Gerhart has been a member of the WSB faculty since 2000. He has served as chair of the Department of Management and Human Resources and was founding director of the Strategic Human Resource Management specialization in the Wisconsin Full-Time MBA Program. He will serve as interim dean until a permanent dean is identified by a search that will begin in September. To learn more about Barry, visit go.wisc.edu/wsb- gerhart When I was in the Ph.D. program at the experience, improving student access and opportunities, University of Wisconsin–Madison, I was maintaining and growing faculty excellence, and always struck by how faculty and staff went out of their expanding and improving research. way to make everyone feel at home and helped create a We’re already doing significant work to enhance connection I knew would last a lifetime. business students’ educational experience, such as As the interim Albert O. Nicholas Dean of the expanding applied learning opportunities, incorporating Wisconsin School of Business, I understand the interest interdisciplinary content into our curricula, and opening you and thousands of other alumni have about what we the Learning Commons. Our faculty continue to do here and our plans for the future. -

Before the FEDERAL COMMUNICATIONS COMMISSION WASHINGTON, D.C

Before the FEDERAL COMMUNICATIONS COMMISSION WASHINGTON, D.C. 20554 In the Matter of ) ) Promoting the Availability of Diverse and ) MB Docket No. 16-41 Independent Sources of Video Programming ) ) COMMENTS OF THE WRITERS GUILD OF AMERICA, WEST, INC. Garrett Andrew Schneider, PhD Research and Public Policy Analyst Writers Guild of America, West, Inc. 7000 West Third Street Los Angeles, CA 90048 March 30, 2016 Table of Contents I. Summary and Introduction ............................................................................................... 2 II. The Issue of Programming Independence and Diversity Must Be More Broadly Assessed .......................................................................................................................................... 4 III. Analyzing Network and Program Independence ............................................................ 8 A. Network Carriage ................................................................................................................... 9 B. Content Supply ..................................................................................................................... 12 IV. Diversity ........................................................................................................................... 15 V. The Commission Can Take Meaningful Action to Promote Programming from Diverse and Independent Sources ............................................................................................. 17 Appendix ..................................................................................................................................... -

GET DAILY NEWS on TELEVISION DRAMA *LIST 0415-ALT LIS 1006 LISTINGS 3/26/15 1:46 PM Page 17

LIST_0415_COVER_LIS_1006_LISTINGS 3/26/15 3:16 PM Page 1 WWW.WORLDSCREENINGS.COM APRIL 2015 MIPTV EDITION TVLISTINGS THE LEADING SOURCE FOR PROGRAM INFORMATION MIP_APP_2013 copy_Layout 1 3/25/15 6:11 PM Page 1 World Screen App For iPhone and iPad DOWNLOAD IT NOW Program Listings | Stand Numbers | Event Schedule | Daily News Photo Blog | Hotel and Restaurant Directories | and more... Sponsored by Brought to you by *LIST_0415-ALT_LIS_1006_LISTINGS 3/26/15 1:45 PM Page 3 TV LISTINGS 3 3 In This Issue 4K MEDIA dir.; Stephen Kelley, dir., dist.; Federico Vargas, 53 West 23rd St., 11/Fl. dir., dist. PROGRAM HIGHLIGHTS 3 23 New York, NY 10010, U.S.A. Wild Kratts (Animated adventure comedy, 4K Media IMPS Tel: (1-212) 590-2100 9 Story Media Group Incendo 92x22 min., 26 new eps. coming soon) The INK Global Kratt brothers leap into animated action as 4 ITV Studios Global Entertainment A+E Networks they travel to different corners of the world ABC Commercial 24 to get up close with amazing animals. ABS-CBN International Distribution ITV-Inter Medya Peg + Cat (Animated preschool, 80x12 min., 50 Kanal D Stand: R7.B12 new eps. coming soon) Follows Peg and her side- 6 Keshet International AFL Productions Lightning Entertainment Contact: Kristen Gray, SVP, ops. & business & kick, Cat, as they embark on adventures while Alfred Haber Distribution legal affairs; Jennifer Coleman, VP, lic. learning basic math concepts and skills. all3media international & American Cinema International 25 mktg.; Jonitha Keymoore, pgm. sales dir. Get Ace (Animated comedy, 52x11 min., 52 Lightning International new eps. coming soon) Nerdy high schooler 8 Lionsgate Entertainment Animation from Spain Looking Glass International Ace McDougal is catapulted into adventure Armoza Formats m4e/Telescreen when he’s accidentally fitted with some cool, ARTE France ultra high-tech, experimental braces.