Pregled Trgovine

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Trading Summary First Quarter of 2017

Trading Summary First quarter of 2017 Zagreb, April 2017. This publication was prepared and published by the Zagreb Stock Exchange Inc., Ivana Lučića 2a/22, Zagreb (hereinafter: Exchange). The publication is intended to provide information to the public and shall not be deemed to constitute an offer or invitation to buy or advice on trade or investment in financial instruments or opinion on the terms of the purchase or sale of any financial instrument mentioned therein whether favourable or not, nor should it be relied on as a substitute for own judgement or assessment by any user of this publication. The Exchange waives responsibility and liability for any damage which might arise out of the use of information contained therein. Further use of information available in this publication is permitted by the Exchange provided that the source is cited. Copyright © 2017. Zagreb Stock Exchange Zagreb Ivana Lučića 2a/22 All rights reserved. Content: 1 TRADING .................................................................................................................................. 1 1.1 COMPARISION WITH PREVIOUS QUARTER .............................................................................................................. 1 1.2 COMPARISON WITH PREVIOUS YEAR ..................................................................................................................... 2 1.3 MONTHLY TRADING OVERVIEW ........................................................................................................................... 4 -

Possibilities of Applying Markowitz Portfolio Theory on the Croatian Capital Market

POSSIBILITIES OF APPLYING MARKOWITZ PORTFOLIO THEORY ON THE CROATIAN CAPITAL MARKET Dubravka Pekanov Starčević, Ph.D. J. J. Strossmayer University of Osijek, Faculty of Economics in Osijek E-mail: [email protected] Ana ZRNIć, Ph.D. Student, J. J. Strossmayer University of Osijek, Faculty of Economics in Osijek E-mail: [email protected] Tamara Jakšić, BEcon, student J. J. Strossmayer University of Osijek, Faculty of Economics in Osijek E-mail: [email protected] POSSIBILITIES OF APPLYING MARKOWITZ PORTFOLIO THEORY ON THE CROATIAN CAPITAL... MARKOWITZ PORTFOLIO THEORY ON THE CROATIAN POSSIBILITIES OF APPLYING Abstract In order to achieve the maximum possible profit by taking the lowest possible risk, investors build a stock portfolio consisting of a specific number of stocks which, according to the principle of diversification, significantly reduce the risk of loss. To build a portfolio, in developed capital markets investors have used the Markowitz portfolio optimization model for many years that enables us to find an optimal risk-return trade-off by selecting certain stock combinations. Despite the development of the Zagreb Stock Exchange, i.e., the central trading venue in the Republic of Croatia, the Croatian capital market is still under- developed. It is characterized by numerous shortcomings such as low liquidity, lack of transparency, high stock price volatility and insufficient traffic. Accord- ingly, the aim of this paper is to provide an insight into the functioning of the Dubravka Pekanov Starčević • Ana Zrnić • Tamara Jakšić: Dubravka Pekanov Starčević • Ana Zrnić Tamara 520 Croatian capital market and to examine the possibility of building an optimal stock portfolio by using the Markowitz model. -

Beat Project

BEAT PROJECT WP 3 – Cross Border cluster development on maritime technologies/Blue Technologies for knowledge sharing Activity 3.1. Assessment of conditions for transnational cluster development_DM 3.1.2 List of Organizations European Regional Development Fund www.italy-croatia.eu/acronym CROATIANS COMPANIES ............................................................................................................................................ 3 SHIPPING (SEA) ............................................................................................................................................................... 3 SHIP AND CARGO AGENTS .............................................................................................................................................. 5 CREW AND VESSEL MANAGEMENT .............................................................................................................................. 10 MOORING, PILOT AND TUG SERVICES .......................................................................................................................... 15 PORT OPERATORS ......................................................................................................................................................... 17 CARGO CONTROL AND INSPECTION ............................................................................................................................. 19 SHIP INSPECTION ......................................................................................................................................................... -

FIMA Daily Insight

FIMA Daily Insight IN FOCUS - ZAGREB STOCK EXCHANGE January 8, 2013 Stocks on ZSE traded higher today. CROBEX increased 0.24% to ZSE STOCK MARKET 1,808.40 pts while blue chip CROBEX10 gained 0.21% to 1,010.86 pts. CROBEX Last 1.808,4 Regular stock turnover amounted to HRK 14.4 million. % daily 0,24% Integrated telecom HT (HTRA CZ) topped the liquidity board collecting % YTD 3,91% HRK 4.3 million in turnover. The price increased 0.9% to HRK 210.70. CROBEX10 last 1010,9 Fertilizers producer Petrokemija (PTKMRA CZ) also came to focus again % daily 0,21% with HRK 1.5 million in turnover while price gained 5.5% to HRK 240.0. % YTD 4,05% Petrokemija was in investors’ focus few months ago, after speculations on Government selling its share of 1.7 million shares (50.6% of capital). Stock Turnov er (HRK m) 14,37 A few days ago Mladen Pejnović, head of the State Office for State Total MCAP (HRK bn) 194,39 Property Management confirmed government’s plans to privatize Source: w w w .zse.hr Petrokemija. Auto-parts producer AD Plastik (ADPLRA CZ) came to focus trading in -4,0% -2,0% 0,0% 2,0% 4,0% 6,0% blocks. The price advanced 1% to HRK 115.99 on HRK 1.3 million in PTKM-R-A ATPL-R-A turnover. AD Plastik currently trades at P/E=7.7, P/S=0.7 and DDJH-R-A P/Bv=0.7. VPIK-R-A LKPC-R-A Tobacco and tourism Adris group preferred share (ADRSPA CZ) was VIRO-R-A KORF-R-A also in investors’ focus with HRK 0.7 million in turnover while price KNZM-R-A slipped 1.3% to HRK 262.20. -

Pregled Trgovine

Monthly report May 2017 Zagreb, June 2017 This publication was prepared and published by the Zagreb Stock Exchange Inc., Ivana Lučića 2a/22, Zagreb (hereinafter: Exchange). The publication is intended to provide information to the public and shall not be deemed to constitute an offer or invitation to buy or advice on trade or investment in financial instruments or opinion on the terms of the purchase or sale of any financial instrument mentioned therein whether favourable or not, nor should it be relied on as a substitute for own judgement or assessment by any user of this publication. The Exchange waives responsibility and liability for any damage which might arise out of the use of information contained therein. Further use of information available in this publication is permitted by the Exchange provided that the source is cited. Copyright © 2017. Zagreb Stock Exchange Zagreb Ivana Lučića 2a/22 All rights reserved. Content: 1. GENERAL CHARACTERISTICS ................................................................................................... 1 2. TURNOVER AND MARKET CAPITALIZATION BY SECTOR ....................................................... 3 3. STOCKS WITH THE LARGEST MARKET CAPITALIZATION ........................................................ 4 4. MOST ACTIVE STOCKS BY TURNOVER .................................................................................... 5 5. STOCKS PERFORMANCE .......................................................................................................... 6 6. EQUITY BLOCK TURNOVER..................................................................................................... -

Pregled Podataka O Planovima Gospodarenja Otpadom

PREGLED PODATAKA O PLANOVIMA GOSPODARENJA OTPADOM SVIBANJ 2011. Pregled podataka o planovima gospodarenja otpadom Zagreb, svibanj 2011. PREGLED PODATAKA O PLANOVIMA GOSPODARENJA OTPADOM Svibanj 2011. Pregled podataka o planovima gospodarenja otpadom Zagreb, svibanj 2011. SADRFAJ SAFETAK. ................................................................................................................... .- 2 - I UVOD. .......................................................................................................................... .- 3 - 1.1. PLAN GOSPODARENJA OTPADOM – PRAVNA OSNOVA ........................................................................... 4 1.1.1. PLANOVI FUPANIJA, GRADOVA I OPĆINA .................................................................................................... 4 1.1.2.PLANOVI PROIZVOĐAČA OTPADA ................................................................................................................ 5 II PLANOVI I IZVJEEĆA O PROVEDBI/IZVREENJU PLANOVA FUPANIJA, GRADOVA I OPĆINA. .................................................................................................. .- 6 - 2.1. PREGLED BROJA FUPANIJA, GRADOVA I OPĆINA KOJE SU IZRADILI PLAN GOSPODARENJA OTPADOM I IZVJEEĆE O PROVEDBI/IZVREENJU PLANA GOSPODARENJA OTPADOM .................... 6 III PLANOVI PROIZVOĐAČA I/ILI POSJEDNIKA OTPADA. ........................................ .- 9 - 3.1. PREGLED BROJA PRAVNIH SUBJEKATA/TVRTKI KOJI SU IZRADILI PLAN GOSPODARENJA OTPADOM U RH ................................................................................................................................................. -

CEE Investment Opportunities: Slovenia & Croatia Investor

CEE investment opportunities: Slovenia & Croatia Investor Day Site visits Monday, 23 May 2016 Slovenia: Krka & Gorenje Timetable: 08:00– 17:15 Krka is among the top generic pharmaceutical companies in the world. Its business is the production and sale of prescription pharmaceuticals, non- prescription products and animal health products. 08:00 Departure from Hotel International (Zagreb) 10:00 Krka tour Gorenje is one of the leading European home 11:00 Departure from Krka appliance manufacturers with a history 13:00 Lunch break spanning more than 60 years. Home 14:00 Gorenje tour appliances under global brands Gorenje and 15:00 Departure from Gorenje Asko and six regional brands (Atag, Pelgrim, Upo, Mora, Etna and Körting) elevate the 17:15 Arrival at Hotel International (Zagreb) quality of life of users in 90 countries worldwide. Croatia: Podravka, Ledo & Atlantic Grupa Timetable: 08:00 – 16:45 Podravka produces the well-known Vegeta, as well as thousands of other products in its diverse catalogue. T h e Podravka brands are recognisable and a favourite in both Croatian and foreign markets. 08:00 Departure from Hotel International (Zagreb) 10:00 Podravka tour Ledo is the largest Croatian producer of 11:00 Departure from Podravka industrial-scale ice cream and the largest 13:00 Lunch break distributor of frozen foods. 14:00 Ledo tour Atlantic Grupa is one of the most dynamic 15:00 Departure from Ledo business systems in the region, with a 15:30 Atlantic Grupa tour significant portion of its business activities in 16:30 Departure from Atlantic Grupa the EU. 16:45 Arrival at Hotel International (Zagreb) For further details, please contact your WOOD sales representative or Karolina Drach-Kowalczyk at [email protected] . -

Podravka Group Business Results for 1-12 2020 Period

Podravka Group business results for 1-12 2020 period Investor Relations Sales revenues growth in both segments on a year level in HRKm Sales revenues by segment 12M 2019 12M 2020 +2.1% 5.000 4.409 4.503 4.500 +2.1% 4.000 3.454 3.527 3.500 3.000 2.500 2.000 +2.2% 1.500 955 976 1.000 500 0 Group Food Pharma Podravka Group in 1-12 20201,2: Food segment in 1-12 20201,2: Pharmaceuticals segment in 1-12 20201,2: • Own brands → 2.5% higher sales, • Own brands → 3.1% higher sales, due to of the increased • Own brands → 0.3% higher sales, due to the increase in demand for food products. The revenue growth was recorded by demand for pharmaceutical products, primarily OTC drugs • Other sales → 1.9% lower sales, almost all BU, with the biggest absolute growth recorded by BU category, Culinary and BU Baby food, sweets and snacks, • Total Podravka Group → 2.1% higher sales. • Other sales → 10.7% higher sales, as a result of higher sales of • Other sales → 11.2% lower revenues, due to lower sales of trade goods in the markets of Bosnia and Herzegovina and trade goods (some markets), closure of Gastro channel Croatia, (HoReCa and institutional customers - schools, kindergartens, restaurants, hotels) in Croatia and Slovenia (April and May), • Total Pharma → 2.2% higher sales. difficulties in the HoReCa in 3Q (weak tourist season) and re- closure of HoReCa in November, • Total Food → 2.1% higher sales. 1Given the Podravka Group’s range of products, situation caused by COVID-19 disease positively impacted the sales revenues trends in 1Q, but this impact cannot be clearly distinguished from the impact of regular demand for products. -

Raiffeisen Weekly Report, Nr. 32/2017

Raiffeisen Weekly Report Number 32 September 4th, 2017 Real Q2 GDP growth rate at 2.8%yoy GDP real growth rate The first Q2 17 GDP estimate reported continuation of economic growth at a 4 faster pace with real GDP rising by +2.8%yoy. The positive contribution came 3 from domestic demand (+3.3%) while the contribution of net-foreign demand was 2 negative (–0.5%), as a result of higher real growth rate of imports (4.6%yoy) 1 compared to the exports (3.6%yoy), confirming the relatively high import de- % 0 pendence of the Croatian economy. –1 Breakdown by components showed that the largest positive contribution to the –2 GDP volume change came from household consumption with the highest rate –3 since Q1 08 (+3.8%yoy in real terms). Strong household consumption levels Q2 12 Q1 13 Q2 13 Q1 14 Q2 14 Q1 15 Q2 15 Q1 16 Q3 16 Q1 17 Q2 17 Q3 12 Q4 12 Q3 13 Q4 13 Q3 14 Q4 14 Q3 15 Q4 15 Q2 16 Q4 16 are not much of a surprise since high-frequency indicators reported a solid re- Sources: CBS, Economic RESEARCH/RBA tail trade growth, increasing optimism, improvements in consumer confidence, growth of employment, declining unemployment and an increase in disposable income. One should mention that household consumption growth was not ac- companied by an increase in the levels of borrowing and loans, as was the Retail trade, real changes, yoy case in the pre-crisis period. Government consumption increased by 1.7%yoy 8 in real terms while GFCF real growth decelerated to 3.2%yoy, possibly because 7 particular companies postponed their investment decisions due to the uncertainty 6 related to Agrokor. -

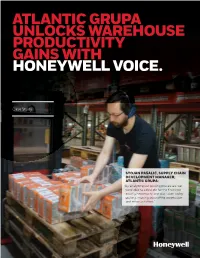

Atlantic Grupa Case Study

ATLANTIC GRUPA UNLOCKS WAREHOUSE PRODUCTIVITY GAINS WITH HONEYWELL VOICE. Case Study STOJAN PAŠALIĆ, SUPPLY CHAIN DEVELOPMENT MANAGER, ATLANTIC GRUPA: “By analyzing our picking processes, we were able to calculate for the first time exactly how much time was taken up by picking, moving around the warehouse and other activities.” OVERVIEW Headquartered in Zagreb, Croatia, Atlantic Grupa is one of the largest fast-moving consumer goods (FMCG) producers and distributors in Southeast Europe. Founded in 1991, the company operates in eight countries and exports products — both its own and other brands — to more than 40 markets around the globe. Steady acquisitions, combined with a well-earned reputation for quality goods and excellent service, have resulted in solid year-over-year growth for the company. To keep pace with demand, Atlantic Grupa sought a voice-directed, order-picking solution that would boost productivity and reduce errors in its distribution operations. Atlantic Grupa ultimately invested in Honeywell Voice for its built-in integration flexibility, pick-up-and-go capabilities and superior data insights. BACKGROUND Atlantic Grupa was experiencing growing pains. Order volumes solution for order picking at its warehouses in Zagreb and Split. By were rising by roughly 10 percent per year, requiring that freeing the eyes and hands of its pickers, Atlantic Grupa aimed to employees complete between 350,000 to 400,000 picks per streamline processes, boost productivity, and reduce error rates. month. While permanent staff increases were not a long-term Within short order of implementing Honeywell Voice, Atlantic option, training temporary employees to address peak season Grupa achieved its goals. -

Winter in Prague Tuesday 5 December to Friday 8 December 2017

emerging europe conference Winter in Prague Tuesday 5 December to Friday 8 December 2017 Our 2017 event held over 4 informative and jam-packed days, will continue the success of the previous five years and host almost 3,000 investor meetings, with over 160 companies representing 17 countries, covering multiple sectors. For more information please contact your WOOD sales representative: WOOD & Company Save Warsaw +48 222 22 1530 the Date! Prague +420 222 096 452 conferences 2017 London +44 20 3530 0611 [email protected] Participating companies in 2016 - by country Participating companies in 2016 - by sector Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Asseco Poland AT&S Budapest Stock Exchange Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka AT&S CA Immobilien Magyar Telekom Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim CME Conwert MOL Group Electrica Cimsa Arcelik Banca Transilvania Cyfrowy Polsat S.A. Erste Bank OTP Bank Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Luxoft Immofinanz Wizz Air Hidroelectrica Dogan Holding Atlantic Grupa BGEO Aeroflot Magyar Telekom PORR Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Zachodni WBK Cimsa O2 Czech Republic RHI Kazakhstan OMV Petrom Ford Otosan CCC Bucharest Stock Exchange Ciech Orange Polska Uniqa Insurance Group Steppe Cement Romgaz Garanti Coca-Cola Icecek Budapest Stock Exchange Dogus Otomotiv OTE Vienna -

CEE CIS Committee Decision

INDEX COMMITTEE DECISIONS Topic: CEE & CIS Index Committee Decisions From: Wiener Börse AG / Market & Product Development Date: December 17, 2008 New RFs for all indices were determined on the basis of closing prices of December 17, 2008. All adjustments will be implemented after the close of the trading session on December 19, 2008. The Index Committee has decided upon the following adjustments: CTX, CECE, SCECE, CECETR , CECExt effective December 22, 2008 New Number Name ISIN New FF New RF of Shares CENTRAL EUROP. MEDIA BMG200452024 36.024.273 0,75 CEZ CZ0005112300 0,37 ERSTE GROUP BANK AT0000652011 317.012.763 1,00 HTX, CECE, SCECE, CECETR , CECExt effective December 22, 2008 New Number Name ISIN New FF New RF of Shares FHB MORTGAGE BANK HU0000078175 0,75 MAGYAR OLAJ GAZI HU0000068952 0,65 OTP BANK HU0000061726 0,75 0,57 RICHTER GEDEON HU0000067624 0,88 PTX, CECE, SCECE, CECETR , CECExt effective December 22, 2008 New Number Name ISIN New FF New RF of Shares AGORA PLAGORA00067 46.391.570 TVN PLTVN0000017 169.154.223 0,50 SETX, CECExt effective December 22, 2008 New Number Name ISIN New FF New RF of Shares ERICSSON N.TESLA HRERNTRA0000 0,50 INA HRINA0RA0007 0,10 PODRAVKA HRPODRRA0004 0,50 AIK BANKA RSAIKBE79302 1,00 ATLANTSKA PLOVIDBA HRATPLRA0008 1,00 Please note: Due to the suspension of Banca Transilvania, the committee has decided that there will be no determination of new representation factors in the course of the December committee. NTX effective December 22, 2008 New Number Name ISIN New FF New RF of Shares ERSTE GROUP BANK AT0000652011 317.012.763 OTP BANK HU0000061726 0,75 OMV AG AT0000743059 0,50 VOESTALPINE AT0000937503 164.599.032 CENTRAL EUROP.