Mty Food Group Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consolidated Financial Statements of MTY Food Group Inc

Consolidated financial statements of MTY Food Group Inc. November 30, 2019 and 2018 Independent auditor’s report To the Shareholders of MTY Food Group Inc. Our opinion In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the financial position of MTY Food Group Inc. and its subsidiaries (together, the Company) as at November 30, 2019 and 2018, and its financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards (IFRS). What we have audited The Company’s consolidated financial statements comprise: ● the consolidated statements of income for the years then ended; ● the consolidated statements of comprehensive income for the years then ended; ● the consolidated statements of changes in shareholders’ equity for the years then ended; ● the consolidated statements of financial position as at November 30, 2019 and 2018; ● the consolidated statements of cash flows for the years then ended; and ● the notes to the consolidated financial statements, which include a summary of significant accounting policies. Basis for opinion We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the consolidated financial statements section of our report. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Independence We are independent of the Company in accordance with the ethical requirements that are relevant to our audit of the consolidated financial statements in Canada. We have fulfilled our other ethical responsibilities in accordance with these requirements. -

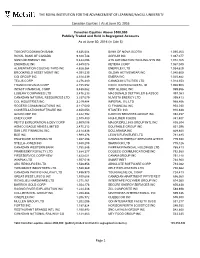

THE ROYAL INSTITUTION for the ADVANCEMENT of LEARNING/Mcgill UNIVERSITY

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Canadian Equities │ As at June 30, 2016 Canadian Equities Above $500,000 Publicly Traded and Held in Segregated Accounts As at June 30, 2016 (in Cdn $) TORONTO DOMINION BANK 9,836,604 BANK OF NOVA SCOTIA 1,095,263 ROYAL BANK OF CANADA 9,328,748 AGRIUM INC 1,087,077 SUNCOR ENERGY INC 5,444,096 ATS AUTOMATION TOOLING SYS INC 1,072,165 ENBRIDGE INC 4,849,078 KEYERA CORP 1,067,040 ALIMENTATION COUCHE-TARD INC 4,628,364 ENERFLEX LTD 1,054,629 BROOKFIELD ASSET MGMT INC 4,391,535 GILDAN ACTIVEWEAR INC 1,040,600 CGI GROUP INC 4,310,339 EMERA INC 1,025,882 TELUS CORP 4,276,480 CANADIAN UTILITIES LTD 1,014,353 FRANCO-NEVADA CORP 4,155,552 EXCO TECHNOLOGIES LTD 1,008,903 INTACT FINANCIAL CORP 3,488,562 WSP GLOBAL INC 999,856 LOBLAW COMPANIES LTD 3,476,233 MACDONALD DETTWILER & ASSOC 997,083 CANADIAN NATURAL RESOURCES LTD 3,337,079 NUVISTA ENERGY LTD 995,413 CCL INDUSTRIES INC 3,219,484 IMPERIAL OIL LTD 968,856 ROGERS COMMUNICATIONS INC 3,117,080 CI FINANCIAL INC 954,030 CONSTELLATION SOFTWARE INC 2,650,053 STANTEC INC 910,638 GOLDCORP INC 2,622,792 CANYON SERVICES GROUP INC 892,457 ONEX CORP 2,575,400 HIGH LINER FOODS 841,407 PEYTO EXPLORATION & DEV CORP 2,509,098 MAJOR DRILLING GROUP INTL INC 838,304 AGNICO EAGLE MINES LIMITED 2,475,212 EQUITABLE GROUP INC 831,396 SUN LIFE FINANCIAL INC 2,414,836 DOLLARAMA INC 829,840 BCE INC 1,999,278 LEON'S FURNITURE LTD 781,495 ENGHOUSE SYSTEMS LTD 1,867,298 CANADIAN ENERGY SERVICES &TECH 779,690 STELLA-JONES INC 1,840,208 SHAWCOR LTD 775,126 -

National Retailer & Restaurant Expansion Guide Spring 2016

National Retailer & Restaurant Expansion Guide Spring 2016 Retailer Expansion Guide Spring 2016 National Retailer & Restaurant Expansion Guide Spring 2016 >> CLICK BELOW TO JUMP TO SECTION DISCOUNTER/ APPAREL BEAUTY SUPPLIES DOLLAR STORE OFFICE SUPPLIES SPORTING GOODS SUPERMARKET/ ACTIVE BEVERAGES DRUGSTORE PET/FARM GROCERY/ SPORTSWEAR HYPERMARKET CHILDREN’S BOOKS ENTERTAINMENT RESTAURANT BAKERY/BAGELS/ FINANCIAL FAMILY CARDS/GIFTS BREAKFAST/CAFE/ SERVICES DONUTS MEN’S CELLULAR HEALTH/ COFFEE/TEA FITNESS/NUTRITION SHOES CONSIGNMENT/ HOME RELATED FAST FOOD PAWN/THRIFT SPECIALTY CONSUMER FURNITURE/ FOOD/BEVERAGE ELECTRONICS FURNISHINGS SPECIALTY CONVENIENCE STORE/ FAMILY WOMEN’S GAS STATIONS HARDWARE CRAFTS/HOBBIES/ AUTOMOTIVE JEWELRY WITH LIQUOR TOYS BEAUTY SALONS/ DEPARTMENT MISCELLANEOUS SPAS STORE RETAIL 2 Retailer Expansion Guide Spring 2016 APPAREL: ACTIVE SPORTSWEAR 2016 2017 CURRENT PROJECTED PROJECTED MINMUM MAXIMUM RETAILER STORES STORES IN STORES IN SQUARE SQUARE SUMMARY OF EXPANSION 12 MONTHS 12 MONTHS FEET FEET Athleta 46 23 46 4,000 5,000 Nationally Bikini Village 51 2 4 1,400 1,600 Nationally Billabong 29 5 10 2,500 3,500 West Body & beach 10 1 2 1,300 1,800 Nationally Champs Sports 536 1 2 2,500 5,400 Nationally Change of Scandinavia 15 1 2 1,200 1,800 Nationally City Gear 130 15 15 4,000 5,000 Midwest, South D-TOX.com 7 2 4 1,200 1,700 Nationally Empire 8 2 4 8,000 10,000 Nationally Everything But Water 72 2 4 1,000 5,000 Nationally Free People 86 1 2 2,500 3,000 Nationally Fresh Produce Sportswear 37 5 10 2,000 3,000 CA -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

House Officers' Expenditures Report-From April 1, 2018 to March

HOUSE OFFICERS’ EXPENDITURES REPORT April 1, 2018 to March 31, 2019 The House Officers’ Expenditures Report for fiscal year 2018-2019 outlines House Officers’ expenditures processed by the House Administration between April 1, 2018 and March 31, 2019. These expenditures are subject to the policies of the Board of Internal Economy that are in effect when the expenses are incurred. The current budgetary allocations and policies are explained in the House Officers and Recognized Parties chapter of the Members’ Allowances and Services Manual available on ourcommons.ca. House Officers’ and National Caucus Research Offices’ expenditures are divided into five categories, as follows: 1. Employees’ salaries: This category includes the salaries of House Officers’ employees. 2. Service contracts: This category includes the costs for professional, technical and administrative services provided to House Officers. 3. Travel: This category includes transportation, per diem and accommodation expenses incurred by House Officers and their employees. o The Detailed Travel Expenditures Report provides information about House Officers' and employees' travel expenditures processed between April 1, 2018 and March 31, 2019. 4. Hospitality: This category includes expenses for meals, refreshments and receptions, as well as other expenses related to extending hospitality. It also includes the cost of gifts given as a matter of protocol. o The Detailed Hospitality Expenditures Report provides information about House Officers' hospitality expenditures processed between April 1, 2018 and March 31, 2019. 5. Office: This category includes expenses such as computers, equipment, telecommunication services, office supplies and training. For more information about the House Officers’ Expenditures Report, please refer to the Frequently Asked Questions. -

Training Coordinator Job Description Direct Report Relationship: Vice President, Training & Customer Service Location: Scottsdale, Arizona FLSA Status: Exempt

Training Coordinator Job Description Direct Report Relationship: Vice President, Training & Customer Service Location: Scottsdale, Arizona FLSA Status: Exempt Equal Opportunity Employer M/F/D/V TRAINING COORDINATOR POSITION SUMMARY Help maximize the efforts and effectiveness of the Kahala Training Team by managing franchisee training registration, identifying gaps and efficiencies in processes, developing resources and providing training support. This position supports all of the Quick Service Restaurant (QSR) brands under the Kahala Brands umbrella (e.g., Cold Stone Creamery, Blimpie, TacoTime, Planet Smoothie, Pinkberry, etc.). TRAINING COORDINATOR KEY RESPONSIBILITIES Oversee all training registrations, communicating regularly with franchisees, training stores, field and office team Maintain training records Proctor monthly ServSafe exams Provide team support (e.g., room set up, scheduling, formatting PowerPoints) for the successful execution of classroom training and other training efforts Ensure training stores have the information and resources needed to successfully train franchisees Process training store payments Work with our print vendor to maintain and order all brand resources Manage content on franchisee portal Continuously provide innovative training solutions (e.g., quizzes, handouts, best practices, apps, etc.) Support team in executing company-wide events TRAINING COORDINATOR PERSONAL ATTRIBUTES Optimistic, enthusiastic and service-minded (to model values of the hospitality industry) Strong organizational -

CP's North American Rail

2020_CP_NetworkMap_Large_Front_1.6_Final_LowRes.pdf 1 6/5/2020 8:24:47 AM 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 Lake CP Railway Mileage Between Cities Rail Industry Index Legend Athabasca AGR Alabama & Gulf Coast Railway ETR Essex Terminal Railway MNRR Minnesota Commercial Railway TCWR Twin Cities & Western Railroad CP Average scale y y y a AMTK Amtrak EXO EXO MRL Montana Rail Link Inc TPLC Toronto Port Lands Company t t y i i er e C on C r v APD Albany Port Railroad FEC Florida East Coast Railway NBR Northern & Bergen Railroad TPW Toledo, Peoria & Western Railway t oon y o ork éal t y t r 0 100 200 300 km r er Y a n t APM Montreal Port Authority FLR Fife Lake Railway NBSR New Brunswick Southern Railway TRR Torch River Rail CP trackage, haulage and commercial rights oit ago r k tland c ding on xico w r r r uébec innipeg Fort Nelson é APNC Appanoose County Community Railroad FMR Forty Mile Railroad NCR Nipissing Central Railway UP Union Pacic e ansas hi alga ancou egina as o dmon hunder B o o Q Det E F K M Minneapolis Mon Mont N Alba Buffalo C C P R Saint John S T T V W APR Alberta Prairie Railway Excursions GEXR Goderich-Exeter Railway NECR New England Central Railroad VAEX Vale Railway CP principal shortline connections Albany 689 2622 1092 792 2636 2702 1574 3518 1517 2965 234 147 3528 412 2150 691 2272 1373 552 3253 1792 BCR The British Columbia Railway Company GFR Grand Forks Railway NJT New Jersey Transit Rail Operations VIA Via Rail A BCRY Barrie-Collingwood Railway GJR Guelph Junction Railway NLR Northern Light Rail VTR -

Archived Content

Untitled Document This content was archived on June 24, 2013. Archived Content Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page. file:///C|/Documents%20and%20Settings/ASLOBODY/Desktop/Working%20folder/archive-eng.html2013-06-20 12:59:43 PM Trans Fat Monitoring Program Second Set of Trans Fat Monitoring Data July 2008 Bureau of Nutritional Sciences Food Directorate Health Products and Food Branch Health Canada Table of contents Section 1: bread products Table 1: Fatty acid composition of garlic breads collected in 2007 ............................................................................................................................. 3 Section 2: margarines and spreads Table 2: Fatty acid composition of garlic spreads collected in 2007............................................................................................................................ 5 Table 3: Fatty acid composition of soft (tub) margarines collected in 2005and 2007.................................................................................................. 6 Section 3: margarines and fats used for baking applications Table 4: Fatty acid composition of hard (print) margarines collected in 2005 and 2007 ......................................................................................... -

March 1, 2017 the Honorable John Bel Edwards Governor, State Of

March 1, 2017 The Honorable John Bel Edwards Governor, State of Louisiana P.O. Box 94004 Baton Rouge, LA 70804-9004 Dear Governor Edwards: I am pleased to submit to you the enclosed Annual Report from the Council for the Development of French in Louisiana dated March 1, 2017. Submission of this report is a requirement of Act No. 679 and sums up “actions taken and progress made toward achieving the purposes and duties established for the council.” Respectfully, William Arceneaux, Ph.D. President Cc: President John A. Alario, Jr. Speaker Taylor Barras Senator Dan “Blade” Moorish Representative Nancy Landry ANNUAL REPORT COUNCIL FOR THE DEVELOPMENT OF FRENCH IN LOUISIANA (CODOFIL) March 1, 2017 Governance Board All twenty-three seats on CODOFIL’s board are filled. The most recent board meeting was held December 10, 2016. Budget CODOFIL’s Existing Operating Budget for FY16 was $609,286 ((maximum budget authority for collecting/spending funds) - not actual funding. Staff The CODOFIL staff is currently comprised of 5 people: a full-time executive director, a full-time communications director, a full-time education program consultant, a full-time cultural program coordinator, and a full-time administrative coordinator. This staffing level is adequate to address the agency’s mandates but may be in need of extra human resources to better fulfill CODOFIL’s mandates. Office relocation CODOFIL continues to rent temporary office space at Lafayette City-Parish government’s International Center. Renovation is underway at the former headquarters of CODOFIL at 217 West Main Street in Lafayette. Projected return to the old office is early 2018. -

EXCLUSIVE 2019 International Pizza Expo BUYERS LIST

EXCLUSIVE 2019 International Pizza Expo BUYERS LIST 1 COMPANY BUSINESS UNITS $1 SLICE NY PIZZA LAS VEGAS NV Independent (Less than 9 locations) 2-5 $5 PIZZA ANDOVER MN Not Yet in Business 6-9 $5 PIZZA MINNEAPOLIS MN Not Yet in Business 6-9 $5 PIZZA BLAINE MN Not Yet in Business 6-9 1000 Degrees Pizza MIDVALE UT Franchise 1 137 VENTURES SAN FRANCISCO CA OTHER 137 VENTURES SAN FRANCISCO, CA CA OTHER 161 STREET PIZZERIA LOS ANGELES CA Independent (Less than 9 locations) 1 2 BROS. PIZZA EASLEY SC Independent (Less than 9 locations) 1 2 Guys Pies YUCCA VALLEY CA Independent (Less than 9 locations) 1 203LOCAL FAIRFIELD CT Independent (Less than 9 locations) No response 247 MOBILE KITCHENS INC VISALIA CA Independent (Less than 9 locations) 1 25 DEGREES HB HUNTINGTON BEACH CA Independent (Less than 9 locations) 1 26TH STREET PIZZA AND MORE ERIE PA Independent (Less than 9 locations) 1 290 WINE CASTLE JOHNSON CITY TX Independent (Less than 9 locations) 1 3 BROTHERS PIZZA LOWELL MI Independent (Less than 9 locations) 2-5 3.99 Pizza Co 3 Inc. COVINA CA Independent (Less than 9 locations) 2-5 3010 HOSPITALITY SAN DIEGO CA Independent (Less than 9 locations) 2-5 307Pizza CODY WY Independent (Less than 9 locations) 1 32KJ6VGH MADISON HEIGHTS MI Franchise 2-5 360 PAYMENTS CAMPBELL CA OTHER 399 Pizza Co WEST COVINA CA Independent (Less than 9 locations) 2-5 399 Pizza Co MONTCLAIR CA Independent (Less than 9 locations) 2-5 3G CAPITAL INVESTMENTS, LLC. ENGLEWOOD NJ Not Yet in Business 3L LLC MORGANTOWN WV Independent (Less than 9 locations) 6-9 414 Pub -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

Community Mourns the Death of Acadian Founder of Pizza Chain

23 avril 2020 – CBC New Brunswick Community mourns the death of Acadian founder of pizza chain Moncton's Bernard Imbeault was the founder of Pizza Delight Bernard Imbeault was named Entrepreneur of the Year by the Conseil économique du Nouveau-Brunswick (CENB) in 2012. (Radio-Canada) As a young entrepreneur, Bernard Imbeault and his friends bought a small pizza take-out in Shediac in 1969. With Imbeault's guidance, it would grow into the Pizza Delight chain. Imbeault became the co-founder of Imvescor, which at its peak owned and operated hundreds of restaurants across Canada, which included Scores, Mikes and Bâton Rouge. Bernard Imbeault died in palliative care Tuesday night, according to his family. Imbeault, 75, had been suffering from Parkinson's disease for the past 13 years. Roger Fournier, the CEO of Triangle Kitchen in Dieppe, met Imbeault in the 60s. Fournier says Imbeault was generous, energetic, and a hard worker. 23 avril 2020 – CBC New Brunswick Bernard Imbeault was the founder of the Pizza Delight chain of restaurants. (Pierre Fournier/CBC News) "He didn't really love money, but he loved success," Fournier said. "He loved to have new enterprises." Fournier says he travelled extensively with Imbeault, who would often visit other businesses. "He was always seeing a business as something that he had to go inside and see what was making them tick and what was making them successful," Fournier said. "And this was a way he'd always been." But Imbeault never forgot his roots. "His trademark was generosity, he was very helpful with different causes in the city and elsewhere in Canada.