Beverage Dec 05.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BRAIN on Drugs 101 GATEWAY

BRAIN on DRUGs 101 GATEWAY. TRENDS . Markeng Recognion 2012 1 LT. Ed Moses, Rered 1 Ojecves • Recite number one cancer killer of women {#6 CDC source on slide} • List the three main areas of the brain in order of alcohol impairment {#36 Dr. John Duncan OK U • Idenfy the age of brain maturity {#37 Dr. Daniel Amen of www.amenclinics.com} 2 Target Markeng….Children 3 Our Children Targeted Parents Unaware In the lile world in which children have their existence, whosoever brings them up, there is nothing so finely perceived and so finely felt, as injusce. Charles Dickens 4 More Women Die every year due to Lung Cancer than Breast Cancer *2007 70,880 women died from Lung Cancer, while 40,460 women died from Breast Cancer. *Estimated by American Cancer Society 5 Smoking Rate vs. Cancer Rate About 24yrs #1 7th 6 7 8 Success trends cause Markeng Change Internal Medicine News 11/1/06 Cigaree Nicone Levels Increase 10% in 6 Years . Reports Commissioner Paul J. Cote Jr., of Massachuses Dept. of Public Health one of only 3 states that require tobacco co. to report yearly nicone yields 9 9 ‘07 Camel Ads • Pink Camels for Girls? 10 10 And the latest… VIRGINIA SLIMS “PURSE PACKS” 11 Camel Exoc Blends A few years ago, R.J. Reynolds introduced Camel Exotic Blends in a range of flavors, featuring unusual packaging that was bright and alluring. In 2006, RJR pulled this line of flavored cigarettes after signing a settlement with 39 state AG’s to stop marketing flavored cigarettes. -

Songs by Title Karaoke Night with the Patman

Songs By Title Karaoke Night with the Patman Title Versions Title Versions 10 Years 3 Libras Wasteland SC Perfect Circle SI 10,000 Maniacs 3 Of Hearts Because The Night SC Love Is Enough SC Candy Everybody Wants DK 30 Seconds To Mars More Than This SC Kill SC These Are The Days SC 311 Trouble Me SC All Mixed Up SC 100 Proof Aged In Soul Don't Tread On Me SC Somebody's Been Sleeping SC Down SC 10CC Love Song SC I'm Not In Love DK You Wouldn't Believe SC Things We Do For Love SC 38 Special 112 Back Where You Belong SI Come See Me SC Caught Up In You SC Dance With Me SC Hold On Loosely AH It's Over Now SC If I'd Been The One SC Only You SC Rockin' Onto The Night SC Peaches And Cream SC Second Chance SC U Already Know SC Teacher, Teacher SC 12 Gauge Wild Eyed Southern Boys SC Dunkie Butt SC 3LW 1910 Fruitgum Co. No More (Baby I'm A Do Right) SC 1, 2, 3 Redlight SC 3T Simon Says DK Anything SC 1975 Tease Me SC The Sound SI 4 Non Blondes 2 Live Crew What's Up DK Doo Wah Diddy SC 4 P.M. Me So Horny SC Lay Down Your Love SC We Want Some Pussy SC Sukiyaki DK 2 Pac 4 Runner California Love (Original Version) SC Ripples SC Changes SC That Was Him SC Thugz Mansion SC 42nd Street 20 Fingers 42nd Street Song SC Short Dick Man SC We're In The Money SC 3 Doors Down 5 Seconds Of Summer Away From The Sun SC Amnesia SI Be Like That SC She Looks So Perfect SI Behind Those Eyes SC 5 Stairsteps Duck & Run SC Ooh Child SC Here By Me CB 50 Cent Here Without You CB Disco Inferno SC Kryptonite SC If I Can't SC Let Me Go SC In Da Club HT Live For Today SC P.I.M.P. -

Union Officials Pleased Over New Contract

Eastern Illinois University The Keep September 2003 9-16-2003 Daily Eastern News: September 16, 2003 Eastern Illinois University Follow this and additional works at: http://thekeep.eiu.edu/den_2003_sep Recommended Citation Eastern Illinois University, "Daily Eastern News: September 16, 2003" (2003). September. 11. http://thekeep.eiu.edu/den_2003_sep/11 This Article is brought to you for free and open access by the 2003 at The Keep. It has been accepted for inclusion in September by an authorized administrator of The Keep. For more information, please contact [email protected]. N “Tell the truth September 16, 2003 TUESDAY and don’t be afraid.” VOLUME 87, NUMBER 17 THEDAILYEASTERNNEWS.COM Trustees decisions For more on what happened at the Board of Trustees meeting take a look at our in-depth coverage. Page 3 NEWS Union officials pleased over new contract NA new contract agreement between the administra- tion and faculty was unanimously approved by the Board of Trustees By Avian Carrasquillo MANAGING EDITOR streamline procedures and save a lot of time and energy,” Radavich The Board of Trustees unani- said. mously passed the contract agree- Among them was a new per- ment between the administration formance-based increase for and faculty union Monday after annually contracted faculty, he the two sides negotiated for more said. than six months. “These new provisions will ben- Charles Delman, president of efit the administration, the faculty the University Professionals of and the students,” Radavich said. Illinois, said he was happy the con- The contract renegotiations, tract was finalized. which began in April 2002, took “This is an agreement that both long to settle because of all the sides should be pleased with; it has additions. -

Sugar-Sweetened Beverage Marketing Unveiled

SUGAR-SWEETENED BEVERAGE MARKETING UNVEILED VOLUME 1 VOLUME 2 VOLUME 3 VOLUME 4 THE PRODUCT: A VARIED OFFERING TO RESPOND TO A SEGMENTED MARKET A Multidimensional Approach to Reduce the Appeal of Sugar-Sweetened Beverages This report is a central component of the project entitled “A Multidimensional Approach to Reducing the Appeal of Sugar-Sweetened Beverages (SSBs)” launched by the Association pour la santé publique du Québec (ASPQ) and the Quebec Coalition on Weight-Related Problems (Weight Coalition) as part of the 2010 Innovation Strategy of the Public Health Agency of Canada on the theme of “Achieving Healthier Weights in Canada’s Communities”. This project is based on a major pan-Canadian partnership involving: • the Réseau du sport étudiant du Québec (RSEQ) • the Fédération du sport francophone de l’Alberta (FSFA) • the Social Research and Demonstration Corporation (SRDC) • the Université Laval • the Public Health Association of BC (PHABC) • the Ontario Public Health Association (OPHA) The general aim of the project is to reduce the consumption of sugar-sweetened beverages by changing attitudes toward their use and improving the food environment by making healthy choices easier. To do so, the project takes a three-pronged approach: • The preparation of this report, which offers an analysis of the Canadian sugar-sweetened beverage market and the associated marketing strategies aimed at young people (Weight Coalition/Université Laval); • The dissemination of tools, research, knowledge and campaigns on marketing sugar-sweetened beverages (PHABC/OPHA/Weight Coalition); • The adaptation in Francophone Alberta (FSFA/RSEQ) of the Quebec project Gobes-tu ça?, encouraging young people to develop a more critical view of advertising in this industry. -

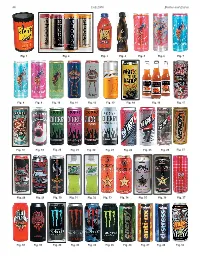

Bottles and Extras Fall 2006 44

44 Fall 2006 Bottles and Extras Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6 Fig. 7 Fig. 8 Fig. 9 Fig. 10 Fig. 11 Fig. 12 Fig. 13 Fig. 14 Fig. 16 Fig. 17 Fig. 18 Fig. 19 Fig. 20 Fig. 21 Fig. 22 Fig. 23 Fig. 24 Fig. 25 Fig. 26 Fig. 27 Fig. 28 Fig. 29 Fig. 30 Fig. 31 Fig. 32 Fig. 33 Fig. 34 Fig. 35 Fig. 36 Fig. 37 Fig. 38 Fig. 39 Fig. 40 Fig. 42 Fig. 43 Fig. 45 Fig. 46 Fig. 47 Fig. 48 Fig. 52 Bottles and Extras March-April 2007 45 nationwide distributor of convenience– and dollar-store merchandise. Rosen couldn’t More Energy Drink Containers figure out why Price Master was not selling coffee. “I realized coffee is too much of a & “Extreme Coffee” competitive market,” Rosen said. “I knew we needed a niche.” Rosen said he found Part Two that niche using his past experience of Continued from the Summer 2006 issue selling YJ Stinger (an energy drink) for By Cecil Munsey Price Master. Rosen discovered a company named Copyright © 2006 “Extreme Coffee.” He arranged for Price Master to make an offer and it bought out INTRODUCTION: According to Gary Hemphill, senior vice president of Extreme Coffee. The product was renamed Beverage Marketing Corp., which analyzes the beverage industry, “The Shock and eventually Rosen bought the energy drink category has been growing fairly consistently for a number of brand from Price Master. years. Sales rose 50 percent at the wholesale level, from $653 million in Rosen confidently believes, “We are 2003 to $980 million in 2004 and is still growing.” Collecting the cans and positioned to be the next Red Bull of bottles used to contain these products is paralleling that 50 percent growth coffee!” in sales at the wholesale level. -

Science, Manufacture, and Marketing of Red Bull and Other Energy Drinks Zeno Yeates, ‘10

No Bull: Science, Manufacture, and Marketing of Red Bull and Other Energy Drinks Zeno Yeates, ‘10 (Photo by Yohan Moon) Yohan by (Photo Zeno smells bad. bad. smells Zeno he increasing prevalence of energy drinks over the The ingredients were explicitly listed on the can itself, and neither Tpast decade is a phenomenon that cannot simply be trademark nor patent existed to protect its formula; hence, Red dismissed as a passing obsession. What began with the advent of Bull was born [3]. Red Bull in 1984 has evolved into a colossus of different brands Careful observation of any university library will reveal the claiming anything from sharpened mental acuity to enhanced undeniable popularity of iPods and Red Bulls – the arsenal for athletic performance. Austrian-born Red Bull founder and CEO the true titan of academic endeavor confronting a full night of Dietrich Mateschitz relies on the younger generation for his sales intellectual tribulation. Nevertheless, some conjecture whether base, exploiting the teenage drive for risk-taking and adventure Red Bull’s buzz serves only to distract the active mind in the using dramatic product names, draconian logos, and sponsorship same way that prolonged auditory stimulation seems to. The of extreme sporting events [1]. Predictably, a multitude of most immediate answer is given on the container itself, which competitors have followed suit, introducing similar concoctions specifically claims to improve performance in times of elevated with dicey names such as Cocaine, Dare Devil, Pimp Juice, stress or strain, increase endurance, increase reaction speed, and Venom, and Monster. However, none of the claims of enhanced stimulate metabolism [4]. -

Sharpton Urges for Defense of Civil Liberties

An Associated Collegiate Press Pacemaker Award Winner • THE • DJ Ken Galvin Hens squish Spiders, celebrates 'Zeptember,' 44-14, - Bl Cl 250 University Center University of Delaware Newark, DE 19716 Tuesday & Friday • • FREE Volume 130, Issue 4 www.review.udel.edu September 16, 2003 Sharpton urges for defense of civil liberties BY CHRIST I~ A HER_:\i A~DEZ half of the audience was compri-,ed of mg forces that "ant to maintain ci' il President Ronald Reagan "s faulty trick Black Student Cnion. said Sharpton \e11.\ F.:awrcs Edttor students. liberties 111 th1s countr:." he said. le-down economics theor:. gave a good peech. The Rev. AI Sharpton stressed the Sharpton stressed that \Ollng for a The current administration is chal "-\mericans lost almost 3 million .. 1 think it \\ill get the young com importance of maintaining ci\ it liberties presidential candidate ,hould rdlect lenging the" ill of the American people. jobs under Bush ... he said. "and they munity im oh cd and make people more and voter registration to approximately onc·s beliefs. not who the likeh ''inner Sharpton said. especial!) the righb of "ill not be compensated by tax cuts.·· a\\ are... she said. 50 people at the Visitor's Center Annex ''ill be. "·omen. gays. lesbians and minorities. Job creation for the middle class Hill said she feels Sharpton ha a Sunday as part of his Democratic presi " If you want to bet on "mners you He said he feeb the Democratic will remedy the unemplojrnent dilem long way to go on the road to the presi dential primary campaign. -

AUSTRALIAN OFFICIAL JOURNAL of TRADE MARKS 22 July 2010

Vol: 24 , No. 29 22 July 2010 AUSTRALIAN OFFICIAL JOURNAL OF TRADE MARKS Did you know a searchable version of this journal is now available online? It's FREE and EASY to SEARCH. Find it at http://pericles.ipaustralia.gov.au/ols/epublish/content/olsEpublications.jsp or using the "Online Journals" link on the IP Australia home page. The Australian Official Journal of Designs is part of the Official Journal issued by the Commissioner of Patents for the purposes of the Patents Act 1990, the Trade Marks Act 1995 and Designs Act 2003. This Page Left Intentionally Blank (ISSN 0819-1808) AUSTRALIAN OFFICIAL JOURNAL OF TRADE MARKS 22 July 2010 Contents General Information & Notices IR means "International Registration" Amendments and Changes Application/IRs Amended and Changes ...................... 8697 Registrations/Protected IRs Amended and Changed ................ 8698 Applications for Extension of Time ...................... 8696 Applications for Amendment .......................... 8696 Applications/IRs Accepted for Registration/Protection .......... 8322 Applications/IRs Filed Nos 1369180 to 1370933 ............................. 8299 Applications/IRs Lapsed, Withdrawn and Refused Lapsed ...................................... 8700 Withdrawn..................................... 8700 Refused ...................................... 8700 Assignments,TransmittalsandTransfers.................. 8700 Cancellations of Entries in Register ...................... 8702 Corrigenda...................................... 8705 Notices....................................... -

ENERGY DRINK CONTAINERS - Bottles & Cans by Cecil Munsey Copyright © 2006

52 Summer 2006 Bottles and Extras Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6 Fig. 7 Fig. 8 Fig. 9 Fig. 10 Fig. 11 Fig. 12 Fig. 13 Fig. 14 Fig. 15 Fig. 16 Fig. 17 Fig. 18 Fig. 19 Fig. 20 Fig. 21 Fig. 22 Fig. 23 Fig. 24 Fig. 25 Fig. 30 Fig. 31 Fig. 26 Fig. 27 Fig. 28 Fig. 29 Fig. 32 > < Fig. 33 Fig. 36 < Fig. 37 Fig. 35 Fig. 38 Fig. 34 > Bottles and Extras Summer 2006 53 ENERGY DRINK CONTAINERS - Bottles & Cans By Cecil Munsey Copyright © 2006 AUTHOR’S NOTE: This article can save you from making a mistake similar to one I made 35+ years ago. I look back now with melancholy at the time while completing the manuscript of my popular study of the Coca-Cola Company’s merchandising history – “The Illustrated Guide to the Collectibles of Cola” (Hawthorn Books, NY). – I consciously did not include a chapter on Coca- Cola cans. Why? I didn’t think that collectors would be interested in “rusty, old tin cans.” I overlooked the entire category except for a few of the early cone-top models and didn’t take into account the successful introduction of aluminum cans and bottles as attractive and long-lasting beverage containers. This article doesn’t make any such mistake; it glorifies a whole, relatively new, category of collectible containers, thus giving collectors the head-start information needed to begin a collection of energy drink cans and bottles. Thanks to eBay and other sources, the current beverages and even those products that didn’t make it in the fast- paced energy drink market, are still available. -

Daily Routine Tributes

November 3, 2010 HANSARD 7127 Yukon Legislative Assembly provide 70 awards to apprentices who have achieved a mark of Whitehorse, Yukon 85 percent or higher on a level or interprovincial exams. Atten- Wednesday, November 3, 2010 — 1:00 p.m. dees to the banquet include apprentices who are being hon- oured and their employers, as well as Skills Canada Yukon, Speaker: I will now call the House to order. We will Yukon Women in Trades and Technology, Yukon College, and proceed at this time with prayers. others who support apprenticeship in Yukon. The next territorial skills competition is being held at Prayers Yukon College on April 29, 2010. This event is now in the school calendar, and I urge all who are listening to attend and DAILY ROUTINE to show support. I know that there will certainly be members of Speaker: We will proceed at this time with the Order the Assembly there, as they have been there in past years. Paper. Finally, I would also like to recognize the Yukoners who Tributes. participate in the many trades- and technology-related boards, working groups, and committees for their contribution toward TRIBUTES the success of trades and technology in Yukon. Together we’re In recognition of Skilled Trades and Technology Week building a skilled workforce that will meet the current and fu- Hon. Mr. Rouble: Mr. Speaker, I rise in the House ture needs of Yukon. today in honour of Skilled Trades and Technology Week, At this time, I would like to ask members of the Assembly which this year will be held from November 1 to 7. -

Songs by Artist

Songs by Artist Title Versions Title Versions Title Versions 10 Years 3 Doors Down 50 Cent Through The Iris TH Kryptonite 9 Just A Lil Bit SF PH TH Wasteland PH Sc TH Let Me Go 4 PIMP SC PH 10,000 Maniacs Live For Today SC PH TH PIMP (Remix) TH Because The Night SC MM Loser 6 Straight To The Bank PH Candy Everybody Wants DK Road I'm On, The 5 Wanksta SC Like The Weather MM Rt Train CB What Up Gangsta PH More Than This SC MM PH When I'm Gone 8 Window Shopper PH TH These Are The Days SC PI 3 Doors Down & Bob Seger 50 Cent & Eminem Trouble Me SC Rt Landing In London CB PH TH Patiently Waiting SC 100 Proof Aged In Soul 3 Of Hearts 50 Cent & Justin Timberlake Somebody's Been Sleeping SC Arizona Rain 4 Ayo Technology PH 10cc Christmas Shoes TU 50 Cent & Mobb Deep Donna SF Love Is Enough 4 Outta Control PH TH Dreadlock Holiday SF 30 Seconds To Mars Outta Control (Remix Version) SC I'm Mandy SF Kill, The SC TH 50 Cent & Nate Dogg I'm Not In Love 5 311 21 Questions 4 Rubber Bullets SF ZM All Mixed Up SC PH RS 50 Cent & Olivia Things We Do For Love, The SC SF ZM Amber PH TH Best Friend PH TH Wall Street Shuffle SF Beyond The Gray Sky PH TH 5th Dimension, The 112 Creatures (For A While) PH TH Aquarius (Let The Sun Shine In) 6 Come See Me SC Don't Tread On Me SC PH Last Night I Didn't Get To Sleep At All SC DG Cupid SC Down SC One Less Bell To Answer SC MM Dance With Me SC CB TH First Straw PH Stoned Soul Picnic 5 It's Over Now SC I'll Be Here Awhile TH Up, Up & Away DK SF Cb Only You SC Love Song SC PH TH Wedding Bell Blues SC DK Cb Peaches & Cream -

Songbook Preview Artist 1014.Pdf

Margarita Mary's Karaoke Artist Title Artist Title ________________________________________________________________________________ _________________________________________________________________________________ 10 SEC COUNTDOW _________________________________________________________NHAPPY NEW YEAR 38 SPECIAL _________________________________________________________CAUGHT UP IN YOU ________________________________________________________________________________MERRY XMAS _________________________________________________________HOLD ON LOOSELY _10_______________________________________________________________________________ YEARS BEAUTIFUL _________________________________________________________________________________IF I'D BEEN THE ONE 10,000 MANIACS _________________________________________________________BECAUSE THE NIGHT 3LW I DO (WANNA GET CLOSE _________________________________________________________CANDY EVERYBODY WANTS _________________________________________________________ TO YOU) _________________________________________________________LIKE THE WEATHER NO MORE (BABY I'M A DO ________________________________________________________________________________MORE THAN THIS _________________________________________________________ RIGHT) 10CC _________________________________________________________DREADLOCK HOLIDAY _________________________________________________________________________________PLAYAS GON' PLAY _________________________________________________________I'M MANDY FLY ME_ 3RD________________________________________________________________________________