Milk Cluster Report.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Electrochemical Biosensor Based on Furosemide-Gold Nanoparticles for the Determination of Dopamine for Practical Applications

ISSN: 2578-7365 Research Article Journal of Chemistry: Education Research and Practice Electrochemical Biosensor Based on Furosemide-Gold Nanoparticles for The Determination of Dopamine for Practical Applications Maqsood Ahmed Abro1, Farman Ali Mangi1, Deedar Ali Jamro1, Naimatullah Channa4, Ihsan Ali Mallah, Sikander Ali Larik1, Sajid Hussain Metlo5, Mansib Ali Jakhrani1, Dost Mohammad Kalhoro3, Aijaz Ali Otho3 & Abdul Qayoom Mugheri2* 1Department of Physics and Electronics Shah Abdul Latif University *Corresponding author Khairpur Sindh, Pakistan Abdul Qayoom Mugheri, Dr. M.A Kazi Institute of Chemistry University of Sindh Jamshoro, 76080, Sindh Pakistan 2Dr. M.A Kazi Institute of Chemistry University of Sindh Jamshoro, 76080, Sindh Pakistan Submitted: 11 Jan 2021; Accepted: 18 Jan 2021; Published: 01 Feb 2021 3Institute of plant sciences University of Sindh, Jamshoro, 76080 Sindh Pakistan 4Beijing university of Engineering of chemical technology, Beijing china 5College of nuclear science and technology Harbin engineering university of china Citation: Maqsood Ahmed Abro, Farman Ali Mangi, Deedar Ali Jamro, Naimatullah Channa, Ashan Ali Mallah, Sikander Ali Larik, Sajid Ali Metlo, Mansib Ali Jakhrani, Sajid Hussain, Dost Mohammad Kalhoro, Aijaz Ali Otho & Abdul Qayoom Mugheri (2021) Electrochemical Biosensor Based on Furosemide-Gold Nanoparticles for The Determination of Dopamine for Practical Applications. J Chem Edu Res Prac 5: 36-41. Abstract In this study, by taking the advantage of the facile & controlled synthesis of furosemide derived gold nanoparticles (Fr-AuNps) for rapid and sensitive amperometric determination of dopamine (DP). The one-step synthesis of Fr- AuNps was carried out at room temperature without the use of strong reducing agents. The synthesized Fr-AuNps were studied by UV-Vis spectroscopy, and a strong absorption band for gold nanoparticles was observed at 520 nm. -

Review Current Livestock Marketing and Its Future Prospects for the Economic Development of Balochistan–Pakistan

INTERNATIONAL JOURNAL OF AGRICULTURE & BIOLOGY 1560–8530/2006/08–6–885–895 http://www.fspublishers.org Review Current Livestock Marketing and its Future Prospects for the Economic Development of Balochistan–Pakistan MUHAMMAD SHAFIQ1 AND MUHAMMAD AZAM KAKAR† Department of Commerce, University of Balochistan Quetta, Pakistan †Livestock and Dairy Development Department Balochistan Quetta, Pakistan 1Corresponding author’s e-mail: [email protected] ABSTRACT In Pakistan, marketing of livestock and its products is dominated by the private sector. Information regarding the marketing of livestock and its products is necessary for knowing the current status and re-organizing these markets for increasing their efficiency. Secondly, it is the stated policy of the government to increase the export of agricultural products to lessen the net trade deficit. In the past, relatively more emphasis is placed on enhancing the production and productivity of livestock and its products ignoring the marketing aspects. Any lopsided production augmentation strategy could not be fruitful unless the marketing aspects are adequately addressed. Livestock marketing is the most important segment of livestock business. Hence, for ensuring reasonable returns to the producers as well as protecting consumers’ interests, an efficient marketing system is necessary. Efficient marketing systems promote production and efficient production systems attract marketing agents. In Balochistan livestock are generally marketed either at village level by personal contact between buyer and seller at special places called livestock markets organized for animal trade. These livestock markets are organized at different levels such as; sub-tehsil, tehsil and district levels on daily, weekly, fortnightly, monthly and sometimes yearly bases. These markets are traditional; therefore both buyers and sellers are mostly well informed about these market days or dates, as they are remained un-changed since ages. -

Honour Killing in Sindh Men's and Women's Divergent Accounts

Honour Killing in Sindh Men's and Women's Divergent Accounts Shahnaz Begum Laghari PhD University of York Women’s Studies March 2016 Abstract The aim of this project is to investigate the phenomenon of honour-related violence, the most extreme form of which is honour killing. The research was conducted in Sindh (one of the four provinces of Pakistan). The main research question is, ‘Are these killings for honour?’ This study was inspired by a need to investigate whether the practice of honour killing in Sindh is still guided by the norm of honour or whether other elements have come to the fore. It is comprised of the experiences of those involved in honour killings through informal, semi- structured, open-ended, in-depth interviews, conducted under the framework of the qualitative method. The aim of my thesis is to apply a feminist perspective in interpreting the data to explore the tradition of honour killing and to let the versions of the affected people be heard. In my research, the women who are accused as karis, having very little redress, are uncertain about their lives; they speak and reveal the motives behind the allegations and killings in the name of honour. The male killers, whom I met inside and outside the jails, justify their act of killing in the name of honour, culture, tradition and religion. Drawing upon interviews with thirteen women and thirteen men, I explore and interpret the data to reveal their childhood, educational, financial and social conditions and the impacts of these on their lives, thoughts and actions. -

Physio-Chemical Assessment of Water Sources for Drinking Purpose in Badin City, Sindh Province, Pakistan, (Water Supply Schemes and Hand Pumps)

Advance Research Journal of Multi-Disciplinary Discoveries I Vol. 29.0 I Issue – I ISSN NO : 2456-1045 Physio-Chemical assessment of water sources for drinking purpose in Badin City, Sindh Province, Pakistan, (Water Supply Schemes and Hand Pumps) Original Research Article ABSTRACT ISSN : 2456-1045 (Online) ecently, water bodies contain several types of chemicals (ICV-ENV/Impact Value): 63.78 R and the quantity is more than there were couples of years ago. (GIF) Impact Factor: 4.126 Clean and safe drinking water is one of the basic needs of life Publishing Copyright @ International Journal Foundation and society. Pakistan is the country will all types of water Journal Code: ARJMD/ENV/V-29.0/I-1/C-7/SEP-2018 resources, around the country, water quality is crossing the Category : ENVIRONMENTAL SCIENCE limit above WHO level standard for the drinking water of different big regions. Study area of this study is Badin city, Volume : 29.0 / Chapter-VII/ Issue-1(SEPTEMBER-2018) Sindh province, Pakistan. Present study focused on ―Physio- Journal Website: www.journalresearchijf.com Chemical assessment of water sources for drinking purpose in Paper Received: 23.09.2018 Badin City, Sindh Province, Pakistan‖. Ten sites from Badin Paper Accepted: 02.10.2018 city were decided for sampling to assess the drinking water from different water bodies, the areas names are: Canal Water Date of Publication: 10-10-2018 (Jamali Village), Hand Pump (Jamali Village), WSS Pond By Pass, Hand Pump (Laghari Village), Tap Water (Chandia Page: 38-44 Nangar), WSS Pond (Ward No-04), Filter Plant (Bilawal Park), Civil Hospital Badin, Iqra School Badin, Akram Canal etc. -

First Interviews Call, 19 Batch

QUAID-E-AWAM UNIVERSITY OF ENGINEERING, SCIENCE & TECHNOLOGY, NAWABSHAH AND DATED 20-09-2019 QUAID-E-AWAM UNIVERSITY CAMPUS, LARKANO District wise First Interview call list of All Districts, for Admission in B.E Programme for 19-Batch. The Candidates are Required to Bring All Original Documents Alongwith Admission Fee of Rs.45000/- (Rupees Forty Five Thousands only), and One Set of Attested Photostat Copies of all documents as per Schedule Already Announced on 24.09.2019 to 26.09.2019 FIRST LIST FOR INTERVIEW / ADMISSION DISTT. SUKKUR (A-1) URBAN QUEST = 17 ECL = 05 TOTAL = 22 DISTT. SUKKUR (A-1) RURAL QUEST = 18 ECL = 05 TOTAL = 23 S # Seat # Form # Name Father's Name DOM U/R SSC % HSC% T.S MW IW TW CMP Category GRP M/F 01 0727 72 ABDUL RAFIUE SHAIKH ABDUL QADEER Sukkur U 80 84.727 84 8 33.89 42 83.891 [A-1] PE M 02 1077 58 MANSOOR NAWAZ SOOMRO ALI NAWAZ Sukkur R 81.18 81.364 76 8.118 32.55 38 78.663 [A-1] PE M SAYED NAQUISH HUSSAIN RIZVI 03 3239 5538 ALI MUHAMMAD SHAH Sukkur U 87.06 85.636 71 8.706 34.25 35.5 78.460 [A-1] PE M SAYED 04 0455 3395 HAMZA ASAD MALIK MUHAMMAD ASAD Sukkur R 88.35 88.091 68 8.835 35.24 34 78.072 [A-1] PE M 05 1634 3327 NAVEED BAIG KALHORO BAIG MUHAMMAD Sukkur R 81.29 77.818 77 8.129 31.13 38.5 77.757 [A-1] PE M 06 7547 3319 AIMAN SHAIKH MANZOOR AHMED Sukkur R 84.35 85.818 69 8.435 34.33 34.5 77.263 [A-1][B-upper] PE F 07 7866 3371 BISMA KANWAL JATOI ABDUL RAHIM Sukkur U 82.71 79 73 8.271 31.6 36.5 76.371 [B-lower][A-1] PE F 08 1078 57 SHER KHAN SOOMRO DIL SHER Sukkur R 70 88.091 68 7 35.24 34 76.236 [A-1] PE M 09 1515 148 AFAQUE ALI INDHER HAFIZ ALI MURTAZA Sukkur R 79.18 85.182 66 7.918 34.07 33 74.990 [A-1] PE M 10 0635 163 JUNAID ALI SOOMRO GHULAM MURTAZA Sukkur U 88.59 84.909 64 8.859 33.96 32 74.822 [A-1] PE M NOTE: Any mistake if detected will be rectified lateron. -

Essays on the History of Sindh.Pdf

Essays On The History of Sindh Mubarak Ali Reproduced by Sani H. Panhwar (2019) CONTENTS Introduction .. .. .. .. .. .. .. .. .. 1 Historiography of Sindh .. .. .. .. .. .. .. .. 6 Nasir Al-Din Qubachah (1206-1228) .. .. .. .. .. .. 12 Lahribandar: A Historical Port of Sindh .. .. .. .. .. 22 The Portuguese in Sindh .. .. .. .. .. .. .. .. 29 Sayyid Ahmad Shahid In Sindh .. .. .. .. .. .. 35 Umarkot: A Historic City of Sindh .. .. .. .. .. .. 39 APPENDIX .. .. .. .. .. .. .. .. 49 Relations of Sindh with Central Asia .. .. .. .. .. .. 70 Reinterpretation of Arab Conquest of Sindh .. .. .. .. .. 79 Looters are 'great men' in History! .. .. .. .. .. .. 81 Index .. .. .. .. .. .. .. .. .. .. 85 INTRODUCTION The new history creates an image of the vanquished from its own angle and the defeated nation does not provide any opportunity to defend or to correct historical narrative that is not in its favour. As a result, the construction of the history made by the conquerors becomes valid without challenge. A change comes when nations fight wars of liberation and become independent after a long and arduous struggle. During this process, leaders of liberation movements are required to use history in order to fulfil their political ends. Therefore, attempts are made to glorify the past to counter the causes of their subjugation. A comprehensive plan is made to retrieve their lost past and reconstruct history to rediscover their traditions and values and strengthen their national identity. However, in some cases, subject nations are so much integrated to the culture of their conquerors that they lose their national identity and align themselves with foreign culture. They accept their version of history and recognize the aggressors as their heroes who had liberated them from their inefficient rulers and, after elimination of their out- dated traditions, introduced them to modern values and new ideas. -

PAKISTAN: Health Facilities in Sanghar- Sindh Province

PAKISTAN: Health facilities in Sanghar- Sindh province Health facility Total Type of health facilities DHQ 1 "D District headquarter (DHQ) "T THQ 4 Tehsil headquarter (THQ) "H Civil hospital (CH) CH 1 "R Rural health center (RHC) RHC 6 "B Basic health unit (BHU) "D Civil dispensary (CD) BHU 58 "C District council dispensary (DCD) DCD 2 "S Sub health center (SHC) Khairpur CD 14 Road Shaheed NIAZ SHC 1 MUHAMMAD Primary Benazirabad RAJPAR Total 87 Secondary "B Tertiary International Boundary JAM "B Province Boundary Sinjhoro CHAK AWADH District Boundary PRITAMABAD NO 57 "D "B "B Teshil Boundary JAINDO GUJRI RIND "B Water Bodies "B SHAHPUR KHADRO "R CHAKAR "B "B River SHAHPUR 22-JAMRAOO MULLA CHAK CHAKKAR "B NO 8 HURMAT RAWTIYANI Sindh SARHARI "B "R "B SABIR BARHOON DEH-30 "D "DWASSAN "B JAMRO "B Sanghar CHOTIARI KHAN Shahdadpur "B SANGHAR "B India SANJRANI LANDHI "B JIA ABAD D CHUTIARYOON LUNDO KARIM " B ALI MURDAN "B " SOOMAR "B JAMALI DINO Map Doc Name: PAK843_Sanghar_hfs_L_A3 FAKIR DHANI "B WASAN GHUNDAN TANDO _v1_20190315 JAFFAR KHAN MEHAR PARTO MEHAR ALI "B MEHRAB MITHA Creation Date: 15 March 2019 KILO LAGHARI SINJHORO "D "D RAJPAR "B TALPUR "T JHOL KHAN Projection/Datum: RAJAR "R MUHAMMAD KHAN GCS/WGS84 "B "B KURKALI "B "B LEGHARI RUKKUN "R "D USMAN NIZAMANI Nominal Scale at A3 paper size: 1:610,000 SHAHDADPUR "B "S MUHIB "D HAJI HASSAN GOLO PIR BURRIRO MUHAMMAD "T ALI "D NASIR KHAN HINGORO Khipro KARAM KHAN "B BHIT "B "B KHAN RIND JUNEJO JALALANI "B BAQAR KHAIRO KOLAI "B CHAMAN KAZI WALI NIZAMANI BHAITI "B "B RAHIMABAD PERUMAL QAZI WALI NIZAMANI BAGO KAMIL DAS MUHAMMAD MUHAMMAD Sanghar 0 8.5 17 25.5 "B B "B "D WADADANI AMUL "B HINGORO " "B RAJAR RAJAR "D PIRO "B ALI RANA RAJPUT WASSAN ABDULLA"D MOHEB "B "C kms "C "B FAQIR "B KHIPRO ± MUHAMMAD GIDDER NAGAR SHAH ALI JUNEJO LOON THAIM "B SHORO NAUABAD "T Map data source(s): APPON KUMBHDARHOON "B "H KHAN ABDULLAH "B NAUBAD KANDIARI GAUL, PCO, Logistic Cluster, OCHA. -

The Musalman Races Found in Sindh

A SHORT SKETCH, HISTORICAL AND TRADITIONAL, OF THE MUSALMAN RACES FOUND IN SINDH, BALUCHISTAN AND AFGHANISTAN, THEIR GENEALOGICAL SUB-DIVISIONS AND SEPTS, TOGETHER WITH AN ETHNOLOGICAL AND ETHNOGRAPHICAL ACCOUNT, BY SHEIKH SADIK ALÍ SHER ALÍ, ANSÀRI, DEPUTY COLLECTOR IN SINDH. PRINTED AT THE COMMISSIONER’S PRESS. 1901. Reproduced By SANI HUSSAIN PANHWAR September 2010; The Musalman Races; Copyright © www.panhwar.com 1 DEDICATION. To ROBERT GILES, Esquire, MA., OLE., Commissioner in Sindh, This Volume is dedicated, As a humble token of the most sincere feelings of esteem for his private worth and public services, And his most kind and liberal treatment OF THE MUSALMAN LANDHOLDERS IN THE PROVINCE OF SINDH, ВY HIS OLD SUBORDINATE, THE COMPILER. The Musalman Races; Copyright © www.panhwar.com 2 PREFACE. In 1889, while I was Deputy Collector in the Frontier District of Upper Sindh, I was desired by B. Giles, Esquire, then Deputy Commissioner of that district, to prepare a Note on the Baloch and Birahoi tribes, showing their tribal connections and the feuds existing between their various branches, and other details. Accordingly, I prepared a Note on these two tribes and submitted it to him in May 1890. The Note was revised by me at the direction of C. E. S. Steele, Esquire, when he became Deputy Commissioner of the above district, and a copy of it was furnished to him. It was revised a third time in August 1895, and a copy was submitted to H. C. Mules, Esquire, after he took charge of the district, and at my request the revised Note was printed at the Commissioner-in-Sindh’s Press in 1896, and copies of it were supplied to all the District and Divisional officers. -

Gulawar KHAN 2014.Pdf

WestminsterResearch http://www.westminster.ac.uk/research/westminsterresearch Politics of nationalism, federalism, and separatism: The case of Balochistan in Pakistan Gulawar Khan Faculty of Social Sciences and Humanities This is an electronic version of a PhD thesis awarded by the University of Westminster. © The Author, 2014. This is an exact reproduction of the paper copy held by the University of Westminster library. The WestminsterResearch online digital archive at the University of Westminster aims to make the research output of the University available to a wider audience. Copyright and Moral Rights remain with the authors and/or copyright owners. Users are permitted to download and/or print one copy for non-commercial private study or research. Further distribution and any use of material from within this archive for profit-making enterprises or for commercial gain is strictly forbidden. Whilst further distribution of specific materials from within this archive is forbidden, you may freely distribute the URL of WestminsterResearch: (http://westminsterresearch.wmin.ac.uk/). In case of abuse or copyright appearing without permission e-mail [email protected] POLITICS OF NATIONALISM, FEDERALISM, AND SEPARATISM: THE CASE OF BALOCHISTAN IN PAKISTAN GULAWAR KHAN A thesis submitted in partial fulfilment of the requirements of the University of Westminster for the degree of Doctor of Philosophy September 2014 Author’s declaration This thesis is carried out as per the guidelines and regulations of the University of Westminster. I hereby declare that the materials contained in this thesis have not been previously submitted for a degree in any other university, including the University of Westminster. -

List of Dehs in Sindh

List of Dehs in Sindh S.No District Taluka Deh's 1 Badin Badin 1 Abri 2 Badin Badin 2 Achh 3 Badin Badin 3 Achhro 4 Badin Badin 4 Akro 5 Badin Badin 5 Aminariro 6 Badin Badin 6 Andhalo 7 Badin Badin 7 Angri 8 Badin Badin 8 Babralo-under sea 9 Badin Badin 9 Badin 10 Badin Badin 10 Baghar 11 Badin Badin 11 Bagreji 12 Badin Badin 12 Bakho Khudi 13 Badin Badin 13 Bandho 14 Badin Badin 14 Bano 15 Badin Badin 15 Behdmi 16 Badin Badin 16 Bhambhki 17 Badin Badin 17 Bhaneri 18 Badin Badin 18 Bidhadi 19 Badin Badin 19 Bijoriro 20 Badin Badin 20 Bokhi 21 Badin Badin 21 Booharki 22 Badin Badin 22 Borandi 23 Badin Badin 23 Buxa 24 Badin Badin 24 Chandhadi 25 Badin Badin 25 Chanesri 26 Badin Badin 26 Charo 27 Badin Badin 27 Cheerandi 28 Badin Badin 28 Chhel 29 Badin Badin 29 Chobandi 30 Badin Badin 30 Chorhadi 31 Badin Badin 31 Chorhalo 32 Badin Badin 32 Daleji 33 Badin Badin 33 Dandhi 34 Badin Badin 34 Daphri 35 Badin Badin 35 Dasti 36 Badin Badin 36 Dhandh 37 Badin Badin 37 Dharan 38 Badin Badin 38 Dheenghar 39 Badin Badin 39 Doonghadi 40 Badin Badin 40 Gabarlo 41 Badin Badin 41 Gad 42 Badin Badin 42 Gagro 43 Badin Badin 43 Ghurbi Page 1 of 142 List of Dehs in Sindh S.No District Taluka Deh's 44 Badin Badin 44 Githo 45 Badin Badin 45 Gujjo 46 Badin Badin 46 Gurho 47 Badin Badin 47 Jakhralo 48 Badin Badin 48 Jakhri 49 Badin Badin 49 janath 50 Badin Badin 50 Janjhli 51 Badin Badin 51 Janki 52 Badin Badin 52 Jhagri 53 Badin Badin 53 Jhalar 54 Badin Badin 54 Jhol khasi 55 Badin Badin 55 Jhurkandi 56 Badin Badin 56 Kadhan 57 Badin Badin 57 Kadi kazia -

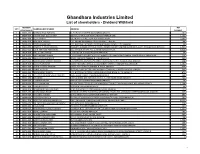

List of Shareholder-Dividend Withheld

Ghandhara Industries Limited List of shareholders - Dividend Withheld MEMBER NET SR # SHAREHOLDER'S NAME ADDRESS FOLIO PAR ID PAYABLE 1 00002-000 MISBAHUDDIN FAROOQI D-151 BLOCK-B NORTH NAZIMABADKARACHI. 461 2 00004-000 FARHAT AFZA BEGUM MST. 166 ABU BAKR BLOCK NEW GARDEN TOWN,LAHORE 1,302 3 00005-000 ALLAH RAKHA 135-MUMTAZ STREETGARHI SHAHOO,LAHORE. 3,293 4 00006-000 AKHTAR A. PERVEZ C/O. AMERICAN EXPRESS CO.87 THE MALL, LAHORE. 180 5 00008-000 DOST MUHAMMAD C/O. NATIONAL MOTORS LIMITEDHUB CHAUKI ROAD, S.I.T.E.KARACHI. 46 6 00010-000 JOSEPH F.P. MASCARENHAS MISQUITA GARDEN CATHOLIC COOP.HOUSING SOCIETY LIMITED BLOCK NO.A-3,OFF: RANDLE ROAD KARACHI. 1,544 7 00013-000 JOHN ANTHONY FERNANDES A-6, ANTHONIAN APT. NO. 1,ADAM ROAD,KARACHI. 5,004 8 00014-000 RIAZ UL HAQ HAMID C-103, BLOCK-XI, FEDERAL.B.AREAKARACHI. 69 9 00015-000 SAIED AHMAD SHAIKH C/O.COMMODORE (RETD) M. RAZI AHMED71/II, KHAYABAN-E-BAHRIA, PHASE-VD.H.A. KARACHI-46. 214 10 00016-000 GHULAM QAMAR KURD 292/8, AZIZABAD FEDERAL B. AREA,KARACHI. 129 11 00017-000 MUHAMMAD QAMAR HUSSAIN C/O.NATIONAL MOTORS LTD.HUB CHAUKI ROAD, S.I.T.E.,P.O.BOX-2706, KARACHI. 218 12 00018-000 AZMAT NAWAZISH AZMAT MOTORS LIMITED, SC-43,CHANDNI CHOWK, STADIUM ROAD,KARACHI. 1,585 13 00021-000 MIRZA HUSSAIN KASHANI HOUSE NO.R-1083/16,FEDERAL B. AREA, KARACHI 434 14 00023-000 RAHAT HUSSAIN PLOT NO.R-483, SECTOR 14-B,SHADMAN TOWN NO.2, NORTH KARACHI,KARACHI. -

Enforced Disappearances by Pakistan Security Forces in Balochistan

Pakistan “We Can Torture, Kill, HUMAN RIGHTS or Keep You for Years” WATCH Enforced Disappearances by Pakistan Security Forces in Balochistan “We Can Torture, Kill, or Keep You for Years” Enforced Disappearances by Pakistan Security Forces in Balochistan Copyright © 2011 Human Rights Watch All rights reserved. Printed in the United States of America ISBN: 156432-786-8 Cover design by Rafael Jimenez Human Rights Watch 350 Fifth Avenue, 34th floor New York, NY 10118-3299 USA Tel: +1 212 290 4700, Fax: +1 212 736 1300 [email protected] Poststraße 4-5 10178 Berlin, Germany Tel: +49 30 2593 06-10, Fax: +49 30 2593 0629 [email protected] Avenue des Gaulois, 7 1040 Brussels, Belgium Tel: + 32 (2) 732 2009, Fax: + 32 (2) 732 0471 [email protected] 51, Avenue Blanc 1202 Geneva, Switzerland Tel: +41 22 738 0481, Fax: +41 22 738 1791 [email protected] 2-12 Pentonville Road, 2nd Floor London N1 9HF, UK Tel: +44 20 7713 1995, Fax: +44 20 7713 1800 [email protected] 27 Rue de Lisbonne 75008 Paris, France Tel: +33 (1)43 59 55 35, Fax: +33 (1) 43 59 55 22 [email protected] 1630 Connecticut Avenue, N.W., Suite 500 Washington, DC 20009 USA Tel: +1 202 612 4321, Fax: +1 202 612 4333 [email protected] Web Site Address: http://www.hrw.org JULY 2011 1-56432-786-8 “We Can Torture, Kill, or Keep You for Years” Enforced Disappearances by Pakistan Security Forces in Balochistan Map of Balochistan .......................................................................................................................... i Summary ......................................................................................................................................... 1 Key Recommendations ......................................................................................................................... 6 Methodology .................................................................................................................................. 9 I.