AR 2018 AW Cvr BC IFC IBC.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download Annual Report 2004/05

ETHIOPIAN AIRLINES Annual Report 2004-05 WWW.ETHIOPIANAIRLINES.COM ANNUAL REPORT 2004-05 building CONTENTS on the FUTURE Management Board of Ethiopian Airlines .................................. 2 CEO’s Message............................................................................................. 3 Ethiopian Airlines Management Team ......................................... 4 Embarking on a long-range reform I. Investing for the future Continent .................................... 5 II. Continuous Change .............................................................. 5 III. Operations Review ............................................................... 5 IV. Measures to Enhance Profitability .................................. 7 V. Human Resource Development ....................................... 10 VI. Fleet Planning and Financing .......................................... 11 VII. Information Systems .......................................................... 11 VIII. Tourism Promotion ............................................................ 11 IX. Corporate Social Responsibility (CSR) Measures ....... 12 Finance ............................................................................................................. 13 Auditors Report and Financial Statements ................................ 22 Domestic Route Map .............................................................................. 40 Ethiopian Airlines Offices ...................................................................... 41 International Route Map ...................................................................... -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Silhouette-Jan-Mar-2021

HM Silhouette Cover_Apr2019-Approved.pdf 1 08/03/2019 16:41 Inflight magazine of Air Seychelles • January-March 2021 FINISHED APARTMENTS AVAILABLE TO VIEW • New Waterfront Apartments released • Communal area with mountain views • Gated security village • Secure parking and storage • All bedrooms are en-suite • Furniture packages available • Walking distance to Eden Plaza shops, restaurants and entertainment • Beautifully landscaped gardens • Views across Eden Marina TO BOOK AN APPOINTMENT TO VIEW OR FOR FURTHER INFORMATION CONTACT: JEAN MARKHAM +248 252 7715 / CHRISTOPHER NEL +248 252 7575 Office hours Monday to Friday 08:30 to 17:00 and Saturdays 09:00 to 12:00 [ CEO’S WELCOME ] Dear Guests, Welcome aboard! In 2020 following the sudden drop in travel demand due to the COVID-19 pandemic, flying for a time was at a standstill. For a regional carrier to remain commercially viable, following the closure of borders across our network, we had to quickly shift our strategy to focus on operating cargo, repatriation and charter flights. Amidst the global pandemic, the beautiful colours of the Air Seychelles livery were spotted at more than 30 destinations across the Asian, European and African continents connecting stranded families together in addition to delivering essential COVID-19 medical supplies. This incredible yet challenging journey, requiring intense planning, really tested the capacity of our assets and teams who I must say embraced all obstacles with great determination. Today I am beyond proud to be part of the Air Seychelles family to which I salute and extend my gratitude for always keeping up the positive momentum. Despite the unprecedented event, the tireless efforts of the entire Air Seychelles team were recognised at the 2020 World Travel Awards where the airline collected three prestigious accolades including ‘Indian Ocean’s Leading Airline’, ‘Indian Ocean’s Leading Airline – Business Class 2020’ as well as ‘Indian Ocean’s Leading Cabin Crew 2020’ for the fifth year running. -

Air Seychelles Posts Second Consecutive Year of Net Profitability

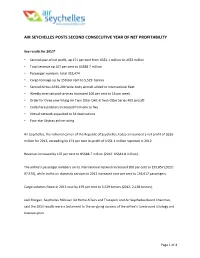

AIR SEYCHELLES POSTS SECOND CONSECUTIVE YEAR OF NET PROFITABILITY Key results for 2013* • Second year of net profit, up 171 per cent from US$1.1 million to US$3 million • Total revenue up 107 per cent to US$88.7 million • Passenger numbers total 352,474 • Cargo tonnage up by 159 per cent to 5,529 tonnes • Second Airbus A330-200 wide-body aircraft added to international fleet • Weekly international services increased 100 per cent to 16 per week • Order for three new Viking Air Twin Otter DHC-6 Twin Otter Series 400 aircraft • Codeshare partners increased from one to five • Virtual network expanded to 34 destinations • Four-star Skytrax airline rating Air Seychelles, the national carrier of the Republic of Seychelles, today announced a net profit of US$3 million for 2013, exceeding by 171 per cent its profit of US$1.1 million reported in 2012. Revenue increased by 107 per cent to US$88.7 million (2012: US$42.8 million). The airline’s passenger numbers on its international network increased 100 per cent to 195,857 (2012: 97,576), while traffic on domestic services in 2013 increased nine per cent to 156,617 passengers. Cargo volumes flown in 2013 rose by 159 per cent to 5,529 tonnes (2012: 2,128 tonnes). Joël Morgan, Seychelles Minister for Home Affairs and Transport and Air Seychelles Board Chairman, said the 2013 results were a testament to the on-going success of the airline’s turnaround strategy and business plan. Page 1 of 4 “To record a second successive year of profitability after the immense challenges of the past is an achievement of which we are all very proud. -

Appendix 25 Box 31/3 Airline Codes

March 2021 APPENDIX 25 BOX 31/3 AIRLINE CODES The information in this document is provided as a guide only and is not professional advice, including legal advice. It should not be assumed that the guidance is comprehensive or that it provides a definitive answer in every case. Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 000 ANTONOV DESIGN BUREAU 001 AMERICAN AIRLINES 005 CONTINENTAL AIRLINES 006 DELTA AIR LINES 012 NORTHWEST AIRLINES 014 AIR CANADA 015 TRANS WORLD AIRLINES 016 UNITED AIRLINES 018 CANADIAN AIRLINES INT 020 LUFTHANSA 023 FEDERAL EXPRESS CORP. (CARGO) 027 ALASKA AIRLINES 029 LINEAS AER DEL CARIBE (CARGO) 034 MILLON AIR (CARGO) 037 USAIR 042 VARIG BRAZILIAN AIRLINES 043 DRAGONAIR 044 AEROLINEAS ARGENTINAS 045 LAN-CHILE 046 LAV LINEA AERO VENEZOLANA 047 TAP AIR PORTUGAL 048 CYPRUS AIRWAYS 049 CRUZEIRO DO SUL 050 OLYMPIC AIRWAYS 051 LLOYD AEREO BOLIVIANO 053 AER LINGUS 055 ALITALIA 056 CYPRUS TURKISH AIRLINES 057 AIR FRANCE 058 INDIAN AIRLINES 060 FLIGHT WEST AIRLINES 061 AIR SEYCHELLES 062 DAN-AIR SERVICES 063 AIR CALEDONIE INTERNATIONAL 064 CSA CZECHOSLOVAK AIRLINES 065 SAUDI ARABIAN 066 NORONTAIR 067 AIR MOOREA 068 LAM-LINHAS AEREAS MOCAMBIQUE Page 2 of 19 Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 069 LAPA 070 SYRIAN ARAB AIRLINES 071 ETHIOPIAN AIRLINES 072 GULF AIR 073 IRAQI AIRWAYS 074 KLM ROYAL DUTCH AIRLINES 075 IBERIA 076 MIDDLE EAST AIRLINES 077 EGYPTAIR 078 AERO CALIFORNIA 079 PHILIPPINE AIRLINES 080 LOT POLISH AIRLINES 081 QANTAS AIRWAYS -

Final AFI RVSM Approvals 05 June 08

Mfr & Type Variant Reg. No. Build Year Operator Acft Op ICAO Serial No Mode S RVSM Date RVSM Operator Yes/No Approval Country Boeing 737 800 7T - VJK 2000 Air Algérie DAH 30203 0A0019 Yes 23/01/02 Algeria Boeing 737 800 7T - VJL 2000 Air Algérie DAH 30204 0A001A Yes 23/01/02 Algeria Boeing 737 800 7T - VJM 2000 Air Algérie DAH 30205 0A001B Yes 23/01/02 Algeria Boeing 737 800 7T - VJN 2000 Air Algérie DAH 30206 0A0020 Yes 23/01/02 Algeria Boeing 737 800 7T - VJQ 2002 Air Algérie DAH 30207 0A0021 Yes 23/01/02 Algeria Boeing 737 800 7T - VJP 2001 Air Algérie DAH 30208 0A0022 Yes 23/01/02 Algeria Boeing 737 600 7T - VJR 2002 Air Algérie DAH 30545 0A0025 Yes 01/06/02 Algeria Boeing 737 600 7T - VJS 2002 Air Algérie DAH 30210 0A0026 Yes 18/06/02 Algeria Boeing 737 600 7T - VJT 2002 Air Algérie DAH 30546 0A0027 Yes 18/06/02 Algeria Boeing 737 600 7T - VJU 2002 Air Algérie DAH 30211 0A0028 Yes 06/07/02 Algeria Airbus 330 202 7T - VJV 2005 Air Algérie DAH 0644 0A0044 Yes 31/01/05 Algeria Airbus 330 202 7T - VJW 2005 Air Algérie DAH 647 0A0045 Yes 05/03/05 Algeria Airbus 330 202 7T - VJY 2005 Air Algérie DAH 653 0A0047 Yes 20/03/05 Algeria Airbus 330 202 7T - VJX 2005 Air Algérie DAH 650 0A0046 Yes 20/03/05 Algeria Boeing 737 800 7T - VKA Air Algérie DAH 34164 0A0049 Yes 23/07/05 Algeria Boeing 737 800 7T - VKB Air Algérie DAH 34165 0A004A Yes 22/08/05 Algeria Boeing 737 800 7T - VKC Air Algérie DAH 34166 0A004B Yes 24/08/05 Algeria Gulfstream Aerospace SP 7T - VPC 2001 Gouv of Algeria IGA 1418 0A4009 Yes 27/07/05 Algeria Gulfstream Aerospace SP -

International Tariff General Rules Applicable to the Transportation Of

1 Egypt Air International Tariff INTERNATIONAL TARIFF GENERAL RULES APPLICABLE TO THE TRANSPORTATION OF PASSENGERS AND BAGGAGE ____________________________________ Issue DEC 15 2019 2 Egypt Air International Tariff TABLE OF CONTENTS: PAGE RULE 1 - DEFINITIONS………………………………………………………………………………………………………………..3 RULE 5 - APPLICATION OF TARIFF………………………………………………………………………………………………17 RULE 10 – RESERVATION AND SEAT SELECTION…………………………………………………………………………20 RULE 15 – CURRENCY OF PAYMENT………………………………………………………………………………………….27 RULE 20 – TAXES, FEES AND OTHER CHARGES…………………………………………………………………………..29 RULE 25 – TICKETS…………………………………………………………………………………………………………………….29 RULE 30 – FARE BRANDS, CLASSES OF SERVICE AND UPGARDES……………………………………………….32 RULE 35 – PERSONAL DATA ………………………………………………………………………………………………………37 RULE 40 – PASSENGER WITH DISABILITY ………………………………………………………………………………….39 RULE 45 – OXYGEN SERVICE AND PERSONAL OXYGEN CONCENTRATORS………………………………….44 RULE 50 - UNACCOMPANIED MINORS AND INFANTS…………………………………………………………………46 RULE 55 – PETS AND ANIMALS………………………………………………………………………………………………….49 RULE 60 – BAGGAGE…………………………………………………………………………………………………………………56 RULE 61 – INTERLINE BAGGAGE ACCECPTANCE…………………………………………………………………………79 RULE 65 – ADMINSTARIVE FORMALIITES………………………………………………………………………………….82 RULE 70 – CHECK-IN AND BOARDING TIME LIMITS……………………………………………………………………84 RULE 75 – REFUSAL TO TRANSPORT………………………………………………………………………………………….85 RULE 80 – SCHEDULE IRREUGLARITIES……………………………………………………………………………………….90 RULE 85 – VOLUNATRY CHANGES AND REROUTING………………………………………………………………….94 RULE -

CHAPTER 11: Civil Aviation Industry

CHAPTER 11: Civil Aviation Industry 11.1 AIR TRANSPORT The main objective of the decision was IN AFRICA the gradual liberalization of scheduled and non-scheduled intra-African air services, The poor state of land transport infrastructure abolishing limits on the capacity and and freight and passenger services in much frequency of international air services within of Africa appears to offer a promising Africa, liberalizing fares and universally opportunity for the further development of air granting traffi c rights up to the ”fi fth freedom transport services throughout the continent. At of the air.”2 Signatory states were obliged to this stage, the key policy issues for Zimbabwe ensure the fair opportunity to compete on a are the ways it can benefi t from the ongoing nondiscriminatory basis. A monitoring body liberalization of civil aviation within the was to supervise and implement the decision, continent called for in the Yamoussoukro and an African air transport executing agency Decision of 1999 and the actions it needs to was to ensure fair competition. Even though take in the decade ahead to ensure that the the decision was a pan-African agreement benefi ts of liberalization are realized. to which most African states are bound, the parties decided that it should be implemented 11.1.1 The Yamoussoukro Decision by separate regional economic organizations. The monitoring body has met only a few Over the past three decades, much of the times. Competition rules and arbitration world has moved from a strictly regulated air procedures are still pending. A recent World transport industry to a more liberalized one. -

UPDATED ON: 18-03-2019 STATION AIRLINE IATA CODE AWB Prefix ON-LINE CARGO HANDLING FREIGHTER RAMP HANDLING RAMP LINEHAUL IMPORT

WFS CARGO - CUSTOMERS LIST DENMARK - CPH SERVICES UPDATED ON: 18-03-2019 IATA AWB CARGO FREIGHTER RAMP RAMP IMPORT STATION AIRLINE ON-LINE GSA TRUCKING TERMINAL CODE Prefix HANDLING HANDLING LINEHAUL EXPORT CPH AMERICAN AIRLINES AA 001 X E NAL WALLENBORN HAL 1 CPH DELTA AIRLINES DL 006 X X I/E PROACTIVE WALLENBORN HAL1 CPH AIR CANADA AC 014 X X X I/E HWF DK WALLENBORN HAL 1 CPH UNITED AIRLINES UA 016 X I/E NORDIC GSA WALLENBORN HAL1 CPH LUFTHANSA LH 020 X X I/E LUFTHANSA CARGO WALLENBORN HAL1 CPH US AIRWAYS US 037 X I/E NORDIC GSA WALLENBORN HAL1 CPH DRAGON AIR XH 043 X I NORDIC GSA WALLENBORN HAL1 CPH AEROLINEAS ARGENTINAS AR 044 X E CARGOCARE WALLENBORN HAL1 CPH LAN CHILE - LINEA AEREA LA 045 X E KALES WALLENBORN HAL1 CPH TAP TP 047 X X x I/E SCANPARTNER WALLENBORN HAL1 CPH AER LINGUS EI 053 X I/E NORDIC GSA N/A HAL1 CPH AIR France AF 057 X X I/E KL/AF KIM JOHANSEN HAL2 CPH AIR SEYCHELLES HM 061 X E NORDIC GSA WALLENBORN HAL1 CPH CZECH AIRLINES OK 064 X X I/E AviationPlus VARIOUS HAL1 CPH SAUDI AIRLINES CARGO SV 065 X I/E AviationPlus VARIOUS HAL1 CPH ETHIOPIAN AIRLINES ET 071 X E KALES WALLENBORN HAL1 CPH GULF AIR GF 072 X E KALES WALLENBORN HAL1 CPH KLM KL 074 X X I/E KL/AF JDR HAL2 CPH IBERIA IB 075 X X I/E UNIVERSAL GSA WALLENBORN HAL1 CPH MIDDLE EAST AIRLINES ME 076 X X E UNIVERSAL GSA WALLENBORN HAL1 CPH EGYPTAIR MS 077 X E HWF DK WALLENBORN HAL1 CPH BRUSSELS AIRLINES SN 020 X X I/E LUFTHANSA CARGO JDR HAL1 CPH SOUTH AFRICAN AIRWAYS SA 083 X E CARGOCARE WALLENBORN HAL1 CPH AIR NEW ZEALAND NZ 086 X E KALES WALLENBORN HAL1 CPH AIR -

Emerging Markets – Unlocking Africa

ACE 2018 - CHINA EMERGING MARKETS – UNLOCKING AFRICA By Sanjeev S. Gadhia CEO – Astral Aviation Who we are – What we do All-Cargo Airline, based at JKIA, Nairobi and operational for 18y. Designated a National Carrier - Cargo by MoT - Kenya Scheduled ‘Regional’ Intra-Africa Cargo Flights from Nairobi – Dar-es- salaam, Mwanza, Zanzibar, Entebbe, Kigali, Juba, Mogadishu, Nampula & Moroni on F27, DC9F & B727F. Scheduled ‘International’ Cargo Flights from Nairobi – London, Stansted and Liege, Belgium with Perishables from Kenya on B747F Interlines with 20 Airlines from Europe, Middle East & Asia. Global GSA Network via NAS (Network Aviation Services) Voted Best African All Cargo Airline in 2017, 2015, 2013 and 2011. NAP Partner. Proud Member of AFRAA, TIACA Our Network Fleet; B747-400F – 115 Tons Fleet & B727-200F – 24 Tons Fleet; DC9-34F – 15 Tons Fleet & Fokker 27- 6 Ton Coming Soon- Singular Aircraft FlyOx-1 – 2 Tons KEY AFRICAN FREIGHTER HUBS TOP CARGO DESTINATIONS INTERNATIONAL CONNECTIVITY -> AFRICA SEA-AIR PORTS -> AFRICA Share of Freight Tonne - Kilometres by region in 2016 22.7% 19.6% 39.2% 14.1% 2.8% 1.6% Source: ICAO 11 Volume of world Value of world international international cargo shipment cargo shipment Aviation Surface modes Aviation One third of the value of world $6.4 trillion trade is shipped by air Surface modes 12 Source: Air Transport Action Group (ATAG), 2014 INTRA AFRICA NETWORK Existing Intra-African Hubs East Africa: Nairobi & Addis Ababa. South Africa: Johannesburg. West Africa: Lagos. North Africa: Casablanca & Cairo. Airlines operating on the Intra African Network East Africa: Astral, Ethiopian Cargo & Kenya Airways Cargo South Africa: SAA Cargo. -

E-First A220 Air Tanzania

Air Tanzania becomes first African-based A220 operator @AirTanzania @Airbus #A220 #FlyAirTanzania Mirabel, Quebec, 21 December 2018 – Air Tanzania as become the first African carrier to take delivery of the Airbus A220 aircraft, the newest addition to the Airbus family of commercial aircraft. Air Tanzania (The Wings of the Kilimanjaro) also becomes the latest member of Airbus aircraft operators. Representatives from the airline as well as officials from the United Republic of Tanzania Government alongside executives from the A220 program celebrated the aircraft handover at the A220 Mirabel assembly line. “The A220 unrivalled passenger comfort combined with its remarkable performance and economics will be an excellent asset to further develop Air Tanzania’s network,” said Tito Kasambala, Acting CEO, Tanzanian Government Flight Agency (TGFA). The A220 will allow Air Tanzania to further develop its domestic and regional market as well as open new routes to India and the Middle East from its home base Dar es Salaam. “With the addition of the A220 in our fleet we are confident that we will expand our footprint in the growing African markets and beyond, as we unlock additional routes and regain our position as a key player in the African air transport market,” added Ladislaus Matindi, Managing Director & CEO, Air Tanzania Company Limited. Air Tanzania becomes the fifth airline globally with an A220 family aircraft. “After Europe, Asia and America, we are proud to see the A220 fly now also on the African continent and in Air Tanzania’s livery. With over 240 Airbus aircraft flying in Africa and a large network of flight service offices in the region, we are ready to contribute to the airline’s success,” said Philippe Balducchi, CEO of the A220 partnership. -

08-06-2021 Airline Ticket Matrix (Doc 141)

Airline Ticket Matrix 1 Supports 1 Supports Supports Supports 1 Supports 1 Supports 2 Accepts IAR IAR IAR ET IAR EMD Airline Name IAR EMD IAR EMD Automated ET ET Cancel Cancel Code Void? Refund? MCOs? Numeric Void? Refund? Refund? Refund? AccesRail 450 9B Y Y N N N N Advanced Air 360 AN N N N N N N Aegean Airlines 390 A3 Y Y Y N N N N Aer Lingus 053 EI Y Y N N N N Aeroflot Russian Airlines 555 SU Y Y Y N N N N Aerolineas Argentinas 044 AR Y Y N N N N N Aeromar 942 VW Y Y N N N N Aeromexico 139 AM Y Y N N N N Africa World Airlines 394 AW N N N N N N Air Algerie 124 AH Y Y N N N N Air Arabia Maroc 452 3O N N N N N N Air Astana 465 KC Y Y Y N N N N Air Austral 760 UU Y Y N N N N Air Baltic 657 BT Y Y Y N N N Air Belgium 142 KF Y Y N N N N Air Botswana Ltd 636 BP Y Y Y N N N Air Burkina 226 2J N N N N N N Air Canada 014 AC Y Y Y Y Y N N Air China Ltd. 999 CA Y Y N N N N Air Choice One 122 3E N N N N N N Air Côte d'Ivoire 483 HF N N N N N N Air Dolomiti 101 EN N N N N N N Air Europa 996 UX Y Y Y N N N Alaska Seaplanes 042 X4 N N N N N N Air France 057 AF Y Y Y N N N Air Greenland 631 GL Y Y Y N N N Air India 098 AI Y Y Y N N N N Air Macau 675 NX Y Y N N N N Air Madagascar 258 MD N N N N N N Air Malta 643 KM Y Y Y N N N Air Mauritius 239 MK Y Y Y N N N Air Moldova 572 9U Y Y Y N N N Air New Zealand 086 NZ Y Y N N N N Air Niugini 656 PX Y Y Y N N N Air North 287 4N Y Y N N N N Air Rarotonga 755 GZ N N N N N N Air Senegal 490 HC N N N N N N Air Serbia 115 JU Y Y Y N N N Air Seychelles 061 HM N N N N N N Air Tahiti 135 VT Y Y N N N N N Air Tahiti Nui 244 TN Y Y Y N N N Air Tanzania 197 TC N N N N N N Air Transat 649 TS Y Y N N N N N Air Vanuatu 218 NF N N N N N N Aircalin 063 SB Y Y N N N N Airlink 749 4Z Y Y Y N N N Alaska Airlines 027 AS Y Y Y N N N Alitalia 055 AZ Y Y Y N N N All Nippon Airways 205 NH Y Y Y N N N N Amaszonas S.A.