News Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Towards-Sustauinable-Mining-Report

2018 2018 Progress Report Table of Contents Introduction About Towards Sustainable Mining® (TSM®) 3 TSM Guiding Principles 4 Message from the Chair of the TSM Governance Team and MAC’s President and CEO 5 2017 Statement from the Community of Interest Advisory Panel 7 How TSM Works 11 Industry Performance Understanding the Results 15 Communities and People 16 Aboriginal and Community Outreach 16 Crisis Management and Communications Planning 17 Safety and Health 19 Preventing Child and Forced Labour 21 Environmental Stewardship 25 Tailings Management 25 Biodiversity Conservation Management 27 Energy Efficiency 32 Energy Use and GHG Emissions Management 32 International Application of TSM 35 TSM Awards TSM Excellence Awards 47 TSM Leadership Awards 50 TSM Performance by Company 51 © 2018 The Mining Association of Canada. Trademarks, including but not limited to Towards Sustainable Mining®, TSM®, and the diamond shaped figure arcs and quadrilaterals designs, are either registered trademarks or trademarks of The Mining Association of Canada in Canada and/or other countries. TSM Progress Report 2 2018 Introduction About Towards Sustainable Mining Towards Sustainable Mining ® (TSM®) is an award-winning performance system that helps mining companies evaluate and manage their environmental and social responsibilities. It is a set of tools and indicators to drive performance and ensure that key mining risks are managed responsibly at participating mining and metallurgical facilities. Mining companies that participate in the TSM initiative demonstrate their strong commitment to responsible mining. By adhering to the TSM Guiding Principles, mining companies exhibit leadership by: Committing to the Engaging Driving world-leading safety and health of with communities. -

News Release

NEWS RELEASE Release Time IMMEDIATE Date 17 April 2013 Number 05/13 BHP BILLITON PRODUCTION REPORT FOR THE NINE MONTHS ENDED 31 MARCH 2013 . Full year production guidance is retained for our major businesses following another quarter of robust operating performance. Western Australia Iron Ore achieved record production for the nine month period ended March 2013. Production guidance of 183 million tonnes (100% basis) for the 2013 financial year remains unchanged, despite cyclone related downtime during the period. An annualised production rate approaching 200 million tonnes (100% basis) is anticipated for the June 2013 quarter. Onshore US produced more than five million barrels of liquids during the March 2013 quarter and the Eagle Ford is now our single largest liquids producing field. Petroleum production guidance for the 2013 financial year remains unchanged at approximately 240 million barrels of oil equivalent. Copper in concentrate production at Escondida increased by 61% during the nine month period ended March 2013. Total Escondida copper production remains on track to increase by at least 20% in the 2013 financial year. Queensland Coal production was affected by adverse weather conditions during the March 2013 quarter. However, recently installed flood mitigation infrastructure enabled a rapid recovery in performance and the business was operating at full supply chain capacity at the end of the period. Petroleum MAR MAR MAR YTD13 MAR Q13 MAR Q13 2013 2013 vs vs vs YTD QTR MAR YTD12 MAR Q12 DEC Q12 Crude oil, condensate and natural gas liquids (‘000 boe) 66,610 20,871 1% -4% -10% Natural gas (bcf) 659.78 207.27 10% -1% -6% Total petroleum products (million boe) 176.57 55.42 6% -2% -7% Total petroleum production – An average production rate of 644 thousand barrels of oil equivalent per day was achieved during the nine month period ended March 2013. -

Our Company Annual Report 2011 a Disciplined Approach a Proven Strategy We Are BHP Billiton, a Leading Global Resources Company

For personal use only Our Company Annual Report 2011 A disciplined approach A proven strategy We are BHP Billiton, a leading global resources company. Our purpose is to create long-term shareholder value through the discovery, acquisition, development and marketing of natural resources. For personal use only BHP Billiton Limited. ABN 49 004 028 077. Registered in Australia. Registered office: 180 Lonsdale Street, Melbourne, Victoria 3000, Australia. BHP Billiton Plc. Registration number 3196209. Registered in England and Wales. Registered office: Neathouse Place, London SW1V 1BH, UK. Each of BHP Billiton Limited and BHP Billiton Plc are members of the BHP Billiton Group, which is headquartered in Australia. Contents 1 Key information 3 4 Board of Directors and information Key 1 1.1 Our business 3 Group Management Committee 104 1.2 Chairman’s Review 4 4.1 Board of Directors 104 1.3 Chief Executive Offi cer’s Report 5 4.2 Group Management Committee 107 1.4 Selected key measures 6 5 Corporate Governance Statement 108 1.5 Risk factors 7 5.1 Governance at BHP Billiton 108 1.6 Forward looking statements 11 5.2 Shareholder engagement 109 2 Information on the Company 12 5.3 Board of Directors 109 2.1 BHP Billiton locations 12 5.4 Board of Directors – Review, Information on the Company 2 2.2 Business overview 14 re-election and renewal 115 2.2.1 History and development 14 5.5 Board Committees 117 2.2.2 Petroleum Customer Sector Group 14 5.6 Risk management 124 2.2.3 Aluminium Customer Sector Group 21 5.7 Management 125 2.2.4 Base Metals Customer -

Ekati Diamond Mine Environmental Agreement and Water Licence Annual Report Summary 2018 May 24, 2019

Ekati Diamond Mine Environmental Agreement and Water Licence Annual Report Summary 2018 May 24, 2019 Loretta Ransom Manager – Environmental Assessment and Monitoring Environmental Stewardship and Climate Change Environment and Natural Resources Government of the Northwest Territories P.O. Box 1320 Yellowknife, NT X1A 2L9 Jaida Ohokannoak Chair - Independent Environmental Monitoring Agency PO Box 1192 Yellowknife, NT X1A 2N8 Michael Roesch Senior Implementation Negotiator/Senior Policy and Program Analyst NWT Region Crown-Indigenous Relations and Northern Affairs Canada 4923 52nd Street Gallery Building Box 1500 Yellowknife, NT X1A 2R3 Chair - Joseph Mackenzie Wek’èezhìi Land and Water Board #1, 4905-48th Street Yellowknife, NT X1A 2P6 Re: Ekati Diamond Mine – Environmental Agreement and Water Licence Annual Report Summary 2018 Dominion Diamond Mines ULC (Dominion) is pleased to submit the attached Environmental Agreement and Water Licence Annual Report Summary 2018. This report was prepared in accordance with the annual reporting requirements of Part B Condition 10 and Schedule 1 Condition 1 of Water Licence W2012L2-0001 and Article 5 of the Environmental Agreement. Dominion trusts that you will find this report to be clear and informative. Please contact Claudine Lee, Head of Environment at [email protected] or 403-910-1933 x 2401 should you have any questions. Sincerely, Claudine Lee, M.Sc., P.Geol. Head of Environment Table of Contents Introduction 1 The Ekati Diamond Mine Story 1 The Ekati Diamond Mine Location 2 The Ekati Diamond -

Ekati Diamond Mine

2019 EKATI DIAMOND MINE SOCIO-ECONOMICEKATI DIAMOND MINE 2019 AGREEMENT Socio-Economic Agreement REPORT Report 1 2 CONTENTS 5 COO’s Message 6 Community Development 9 Health & Safety 10 Environment 15 Employment 24 Business Spend 29 Appendix A: Position Listings 35 Appendix B: Interpretations & Definitions EKATI DIAMOND MINE 2019 Socio-Economic Agreement Report 3 4 COO’S MESSAGE Dominion Diamond Mines ULC (“Dominion” or “the company”) is pleased to present the 2019 Socio-Economic Agreement Report (SEA Report) for the Ekati Diamond Mine, in which we describe the results of our commitments to the Government of the Northwest Territories (GNWT) as set out in the SEA. Dominion is continuing to make a positive difference in the North through support for education, training, community development, employment and business opportunities. ABOUT THE COMPANY 2019 was a challenging, but exciting year for Dominion. By the Dominion is a Canadian mining end of the year we had updated our current Life of Mine company and one of the world’s plan, which now includes the Point Lake project with the largest producers and suppliers of intention to follow with the Jay pipe development. As well, premium rough diamonds to the Dominion has applied to continue its exploration of the Lac global market. de Gras and Glowworn Lake regions. These projects will continue to keep the Ekati mine operating while providing The company operates the Ekati ongoing opportunities for the North. As we move into 2020, Diamond Mine, in which it owns we continue to work diligently towards the future of the a controlling interest, and owns Ekati mine. -

For Announcement to the Market

20 February 2013 For Announcement to the Market Name of Companies: BHP Billiton Limited (ABN 49 004 028 077) and BHP Billiton Plc (Registration No. 3196209) Report for the half year ended 31 December 2012 This statement includes the consolidated results of the BHP Billiton Group, comprising BHP Billiton Limited and BHP Billiton Plc, for the half year ended 31 December 2012 compared with the half year ended 31 December 2011. The results are prepared in accordance with IFRS and are presented in US dollars. US$ Million Revenue down 14.1% to 32,204 Profit attributable to the members of the BHP Billiton Group down 57.8% to 4,238 Net Tangible Asset Backing: Net tangible assets per fully paid share were US$11.77 as at 31 December 2012, compared with US$11.59 at 30 June 2012. Dividends per share: Interim dividend for current period US 57 cents fully franked (record date 8 March 2013; payment date 28 March 2013) Interim dividend for previous corresponding period US 55 cents fully franked This statement was approved by the Board of Directors. Jane McAloon Group Company Secretary BHP Billiton Limited and BHP Billiton Plc WorldReginfo - 48e7f989-b053-4af9-872f-13baefa08e8a NEWS RELEASE Release Time IMMEDIATE Date 20 February 2013 Number 04/13 BHP BILLITON RESULTS FOR THE HALF YEAR ENDED 31 DECEMBER 2012 . The December 2012 half year was more challenging for the global resources industry. Against this backdrop, BHP Billiton’s solid financial results were built on the foundations of strong operating performance, our continued focus on costs and the benefits of our differentiated strategy. -

Feature Feature Major Wa Mining Projects

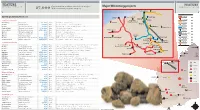

FEATURE FEATURE MINING OUTLOOK Construction workers needed for major Major WA mining projects MINING OUTLOOK 27,000 WA resources projects 2014-15 Source: Pitcrew Port Hedland Pardoo Rio Tinto rail MAJOR WA MINING PROJECTS Dampier Cape Lambert Iron Bridge Mt Dove Rio Tinto mine Completed in past year Balla Balla Abydos (Forge Resources) BHP rail Karara Mining Karara project $2.6bn Mid West Production ramp-up proceeding Sino Iron Wodgina Rio Tinto Hope Downs 4 mine $2.1bn Pilbara First production in H1 2013, ramping up to 15mtpa BHP mine Rio Tinto Marandoo mine expansion $1.1bn Pilbara Production will be sustained at 15mtpa for 16 further years Mt Webber McPhee Creek FMG rail Fortescue Metals Christmas Creek 2 expansion $US1.0bn Pilbara Completed in June 2013 quarter Fortescue Metals Port Hedland port expansion $US2.4bn Pilbara Fourth berth and support infrastructure opened in Aug 2013 Pannawonica FMG mine Atlas Iron Mt Dove mine development n/a Pilbara Production commenced in Dec 2012 Hancock proposed rail Atlas Iron Abydos mine development n/a Pilbara First haulage in Aug 2013, ramping up to 2-3mtpa Solomon Atlas Iron Utah Point 2 stockyard n/a Pilbara Largely complete and now ready to receive ore Hancock mine Hub Christmas Creek Rio Tinto Argyle Diamonds underground mine $US2.2bn Kimberley Production commenced in H1 2013 and is ramping up Buckland (Iron Ore Holdings) Cloudbreak Mineral Resources Sandfire Resources DeGrussa copper mine $US384m Mid West Ramp-up to nameplate production nearing completion Koodaideri Roy Hill Atlas Iron Construction -

South32 Roadshow Presentation

TAO2013\Comms\2015.03.16 - South32 Global Roadshow Pres\150305 South32 Global Roadshow Pres POST BAC Submission_v14.pptx MAKING A DIFFERENCE FROM THE GROUND UP ROADSHOW PRESENTATION MARCH 2015 TAO2013\Comms\2015.03.16 - South32 Global Roadshow Pres\150305 South32 Global Roadshow Pres POST BAC Submission_v14.pptx IMPORTANT INFORMATION AND DISCLAIMER Nature of this presentation The information contained in this presentation does not constitute a prospectus or other listing document in relation to BHP Billiton or the new company proposed to be demerged from BHP Billiton (‘South32’) in any jurisdiction and is summary information provided for information purposes only. Any investment decision in relation to South32 should be made only on the basis of the information contained in the Listing Document for the relevant jurisdiction. The “Listing Documents”, which are available, subject to applicable securities laws, on the BHP Billiton website at www.bhpbilliton.com/demerger, comprise a prospectus which has been approved by the UK Listing Authority in connection with the proposed admission of South32’s ordinary shares to the standard listing segment of the Official List of the UK Financial Conduct Authority and to trading on the Main Market for listed securities of London Stock Exchange plc, an information memorandum in connection with South32’s application for the admission of its ordinary shares to listing on the Australian Securities Exchange and a pre-listing statement in connection with South32’s application for the admission of its ordinary shares to listing on the Johannesburg Stock Exchange. This presentation should not be relied upon in connection with voting on the proposed demerger. -

TROUBLED WATERS How Mine Waste Dumping Is Poisoning Our Oceans, Rivers, and Lakes

TROUBLED WATERS HOW MINE WASTE DUMPING IS POISONING OUR OCEANS, RIVERS, AND LAKES Earthworks and MiningWatch Canada, February 2012 TABLE OF CONTENTS EXECUTIVE SUMMARY .......................................................................................................1 TABLE 1. WATER BODIES IMPERILED BY CURRENT OR PROPOSED TAILINGS DUMPING ................................. 2 TABLE 2. MINING CORPORATIONS THAT DUMP TAILINGS INTO NATURAL WATER BODIES .......................... 4 TAILINGS DUMPING 101....................................................................................................5 OCEAN DUMPING ....................................................................................................................................... 7 RIVER DUMPING........................................................................................................................................... 8 TABLE 3. TAILINGS AND WASTE ROCK DUMPED BY EXISTING MINES EVERY YEAR ......................................... 8 LAKE DUMPING ......................................................................................................................................... 10 CAN WASTES DUMPED IN BODIES OF WATER BE CLEANED UP? ................................................................ 10 CASE STUDIES: BODIES OF WATER MOST THREATENED BY DUMPING .................................11 LOWER SLATE LAKE, FRYING PAN LAKE ALASKA, USA .................................................................................. 12 NORWEGIAN FJORDS ............................................................................................................................... -

Mining Tenement Summary Report

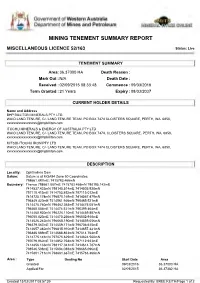

Government of Western Australia Department of Mines and Petroleum MINING TENEMENT SUMMARY REPORT MISCELLANEOUS LICENCE 52/163 Status: Live TENEMENT SUMMARY Area: 36.37000 HA Death Reason : Mark Out : N/A Death Date : Received : 02/09/2015 08:33:48 Commence : 09/03/2016 Term Granted : 21 Years Expiry : 08/03/2037 CURRENT HOLDER DETAILS Name and Address BHP BILLITON MINERALS PTY LTD WAIO LAND TENURE, C/- LAND TENURE TEAM, PO BOX 7474 CLOISTERS SQUARE, PERTH, WA, 6850, [email protected] ITOCHU MINERALS & ENERGY OF AUSTRALIA PTY LTD WAIO LAND TENURE, C/- LAND TENURE TEAM, PO BOX 7474, CLOISTERS SQUARE, PERTH, WA, 6850, [email protected] MITSUI-ITOCHU IRON PTY LTD WAIO LAND TENURE, C/- LAND TENURE TEAM, PO BOX 7474 CLOISTERS SQUARE, PERTH, WA, 6850, [email protected] DESCRIPTION Locality: Ophthalmia Dam Datum: Datum is at MGA94 Zone 50 Coordinates. 798661.887mE; 7415783.466mN Boundary: Thence 798661.887mE 7415783.466mN 798195.142mE 7414537.433mN 798145.514mE 7414505.938mN 797110.415mE 7414753.892mN 797115.012mE 7414725.174mN 796870.169mE 7414567.479mN 796849.420mE 7414561.946mN 796465.521mE 7414475.760mN 796462.363mE 7414475.051mN 796460.004mE 7414474.521mN 796399.464mE 7414460.930mN 796226.110mE 7414459.887mN 796050.820mE 7414470.256mN 796032.918mE 7414526.242mN 796068.190mE 7414559.056mN 796379.567mE 7414559.171mN 796736.615mE 7414657.382mN 796815.910mE 7414657.431mN 796886.689mE 7414688.863mN 797014.764mE 7414775.141mN 797075.629mE 7414824.500mN 797079.962mE 7414852.758mN 797112.933mE 7414856.133mN -

Iron Ore Briefing and Western Australia Iron Ore Site Tour

BHP Billiton Limited BHP Billiton Plc 171 Collins Street Neathouse Place Melbourne Victoria 3000 Australia London SW1V 1LH UK GPO BOX 86 Tel +44 20 7802 4000 Melbourne Victoria 3001 Australia Fax + 44 20 7802 4111 Tel +61 1300 55 47 57 Fax +61 3 9609 3015 bhpbilliton.com bhpbilliton.com 6 October 2014 To: Australian Securities Exchange cc: London Stock Exchange New York Stock Exchange JSE Limited IRON ORE BRIEFING AND WESTERN AUSTRALIA IRON ORE SITE TOUR Jimmy Wilson, President, Iron Ore will host an Iron Ore briefing and a Western Australia Iron Ore (WAIO) site tour on Monday 6 October 2014, Tuesday 7 October 2014 and Wednesday 8 October 2014. A copy of the materials to be presented is attached. Further information on BHP Billiton can be found at: www.bhpbilliton.com. Nicole Duncan Company Secretary For personal use only NEWS RELEASE Release Time IMMEDIATE Date 6 October 2014 Number 17/14 COST REDUCTIONS AND CAPITAL EFFICIENT GROWTH AT WAIO BHP Billiton President Iron Ore, Jimmy Wilson, today announced plans to cut unit costs at Western Australia Iron Ore (WAIO) by at least 25 per cent and the potential to increase capacity there by 65 million tonnes per year at a very low capital cost. Mr Wilson outlined BHP Billiton’s view of the long-term supply and demand trends in the iron ore market. “We continue to see healthy demand growth for iron ore in the mid-term as Chinese steel production is expected to increase by approximately 25 per cent to between 1.0 and 1.1 billion tonnes in the early to mid-2020s,” he said. -

Initial Public Offering (“IPO”) of Ordinary Shares in Mcaleese

McAleese Group Prospectus For personal use only Prospectus JOINT LEAD MANAGERS McAleese Limited ACN 156 354 068 Important Notices Offer and unknown risks, including the risks set out in The Shares have not been, and will not be, The Offer contained in this Prospectus is an Section 5, many of which are beyond the control registered under the US Securities Act or the invitation to acquire fully paid ordinary shares in of McAleese Group and the Directors. McAleese securities laws of any state or other jurisdiction in McAleese Limited (ACN 156 354 068) (“McAleese Group and the Directors cannot and do not give the United States and may not be offered or sold, Group”) (“Shares”). any assurance that the results, performance or directly or indirectly, in the United States unless the achievements expressed or implied by the forward Shares are registered under the US Securities Act, Lodgement and Listing looking statements contained in this Prospectus or an exemption from the registration requirements This Prospectus is dated 12 November 2013 and will actually occur and investors are cautioned of the US Securities Act and any other applicable was lodged with the Australian Securities and not to place undue reliance on these forward securities laws is available. Investment Commission (“ASIC”) on that date. looking statements. Except where required by law, See Section 7.7 for more detail on selling Neither ASIC nor the Australian Securities Exchange McAleese Group has no intention of updating or (“ASX”) takes any responsibility for the contents restrictions that apply to the offer and sale revising forward looking statements, or publishing of Shares in jurisdictions outside of Australia.