Download Financial Report and Accounts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

“Have You Been Offended?” Holocaust Memory in the Channel Islands at HMD 70

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Apollo “Have you been offended?” Holocaust Memory in the Channel Islands at HMD 70 Dr Gilly Carr, Senior Lecturer in Archaeology, Trumpington Street, St Catharine’s College, Cambridge, CB2 1RL. Email: [email protected] Tel: 07790528424 Affiliation: (University of Cambridge Institute of Continuing Education) Dr Gilly Carr is a Senior Lecturer in Archaeology at the University of Cambridge Institute of Continuing Education. She is also a Fellow and Director of Studies at St Catharine’s College. Gilly works in the field of Heritage Studies and Conflict Archaeology and regularly speaks at international conferences. Her recent publications include Heritage and Memory of War: Responses from small islands (co-edited, Routledge 2015); Legacies of Occupation: Heritage, Memory and Archaeology in the Channel Islands (Springer 2014); and Protest, Defiance and Resistance in the Channel Islands: German Occupation 1940-1945 (co- authored, Bloomsbury Academic 2014). Acknowledgements The author would like to thank Freddie Cohen, Elis Bebb, Sir de Vic Carey and Sir Philip Bailhache for interviews collected during my fieldwork. I would also like to thank the Holocaust Memorial Day committee in Jersey for inviting me to the island to speak at the HMD 70. MS length: 10,573, including endnotes. Revision submitted 27 September 2015: 11,001 words, including endnotes. Disclosure statement: I have no financial interest and will receive no financial benefit arising from this research. “Have you been offended?” Holocaust Memory in the Channel Islands at HMD 70 Abstract The Channel Islands have experienced great difficulty in coming to terms with the Holocaust given the implication of the local authorities in the registration of the islands’ Jewish population during the German occupation. -

Annual Report 2020 21

Parish of St Helier 2020/21 Annual Report 1. Foreword by the Constable of St Helier I am delighted to offer Parishioners as well as interested Islanders the Parish's first Annual Report. In previous years the Accounts and Budget Report has been provided to ratepayers in July each year and this has covered some of the ground that readers would expect to find in an Annual Report. However, it seems entirely appropriate that an organisation of the size and complexity of our parish should provide a fuller overview of its activities during the past year, and I am grateful to our Chief Executive for taking up this challenge and producing this significant document. The past financial year has been an enormous challenge with the Coronavirus pandemic requiring huge changes in how the Parish delivers its services; this reports shows the tremendous effort that has been made by every member of staff to adapt and in some cases to change their working practices in order to comply with the public health restrictions. I want to express my heartfelt thanks to all of our staff for their flexibility and commitment to getting their jobs done in what have been extremely trying circumstances. Our honorary and voluntary teams have also been invaluable during the past year in supporting parishioners and ensuring the smooth running of parochial life. I should highlight the work carried out by our Honorary Police force, in particular the significant amount of extra work and responsibility taken on by our Centeniers, four of whom managed the responsibility for charging on behalf of the eleven other parishes as well as our own workload. -

States of Jersey Financial Report and Accounts 2010 States of Jersey Treasury and Resources Department

States of Jersey Financial Report and Accounts 2010 States of Jersey Treasury and Resources Department FINANCIAL REPORT AND ACCOUNTS 2010 Treasury and Resources Department P.F.C. Ozouf Senator Minister J. Refault Connétable Assistant Minister E. Noel Deputy Assistant Minister L. Rowley, MBA, CPFA Treasurer of the States CONTENTS Contents 1. Minister’s Report . .3 9. Notes to the Accounts. .66 2. The Annual Report . .5 9.1. Note 1: Statement of Accounting Policies . 66 2.1. Treasurer’s Introduction . .5 9.2. Note 2. Segmental Analysis . 80 2.2. Financial Performance 2010 . .6 9.3. Note 3: Revenue . 82 2.3. Explanation of the Structure of the States of Jersey .7 9.4. Note 4: Expenditure . 83 2.4. The States of Jersey Business and Financial 9.5. Note 5: Employees and States Members . 84 Planning Cycle . .12 9.6. Note 6: Non-Cash Items and other Significant 2.5. Comparison of Results against Approvals . 13 Items included in the (Deficit)/Surplus . 85 2.6. Detailed Financial Analysis . 19 9.7. Note 7: Finance Costs . 85 2.7. Summary of Current Position . 28 9.8. Note 8: Tangible Fixed Assets . .86 2.8. Outline of Key Objectives and Strategies . 33 9.9. Note 9: Advances . 88 2.9. Key Challenges and Opportunities . 33 9.10. Note 10: Strategic Investments . 89 2.10. Governance Structures . 34 9.11. Note 11: Other Investments . 90 2.11. Corporate Social Responsibility . .40 9.12. Note 12: Stock and Work in Progress . 91 9.13. Note 13: Debtors . .92 3. Statement of Responsibilities for the Financial 9.14. -

Town Crier the Official Parish of St Helier Magazine

TheSt Helier TOWN CRIER THE OFFICIAL PARISH OF ST HELIER MAGAZINE Jersey Hospice Care’s main entrance at Clarkson House Image courtesy of Karl Taylor Jersey Architecture Week 2013 • St Helier House Bicentenary Celebrations Constable’s Comment • Parish Matters • Jersey Heritage • Historic St Helier Parish Notice Board • Dates for your Diary • St Helier Gazette Delivered by Jersey Post to 19,000 homes and businesses every month. Designed and printed in Jersey by MailMate Publishing working in partnership with the Parish of St Helier. A09454 emagazine.pdf 1 05/06/2013 21:23 CELEBRATING OUR 30TH ANNIVERSARY Not many of you may realise but Hi-Speed Freight Services Limited have been the DHL Jersey Agent since April 1985. We are a locally owned company employing 30 locally qualified staff. We have always tried to maintain a family style of atmosphere with a policy of ‘don’t work for us but with us’ that will hopefully see us through the next 30 years. You may have noticed that our staff proudly wear the DHL uniform and our vehicles are in DHL colours along with livery. To all purposes we are DHL and have the same global procedures to adhere to along with strict processes and time scales. We are the only courier company on the island that has a dedicated aircraft that links via Guernsey and directly into the European DHL network, making overnight connections globally. Not only can we offer door to door import and export courier services to over 220 countries globally but we also cover inter island and local Jersey deliveries. -

Valuing the Heritage of the Channel Islands

Valuing the Heritage of the Channel Islands Kate Clark Kate Clark Associates Heritage policy, practice & planning Elizabeth Castle, Jersey Valuing the Heritage of the Channel Islands An initial assessment against World Heritage Site criteria and Public Value criteria Kate Clark Kate Clark Associates For Jersey Heritage August 2008. List of Contents Acknowledgements 6 Introduction 7 Summary Recommendations 8 Recommendation One: Do more to capture the value of Jersey’s Heritage Recommendation Two: Explore a World Heritage bid for the Channel Islands Chapter One - Valuing heritage 11 1.1 Gathering data about heritage 1.2 Research into the value of heritage 1.3 Public value Chapter Two – Initial assessment of the heritage of the Channel Islands 19 2.1 Introduction 2.2 Geography and politics 2.3 Brief history 2.4 Historic environment 2.5 Intangible heritage 2.6 Heritage management in the Channel Islands 2.7 Issues Chapter Three – capturing the value of heritage in the Channel Islands 33 3.1 Introduction 3.2 Intrinsic value 3.3 Instrumental benefits 3.4 Institutional values 3.5 Recommendations Chapter Four – A world heritage site bid for the Channel Islands 37 .0 Introduction .1 World heritage designation .2 The UK tentative list .3 The UK policy review .4 A CI nomination? .5 Assessment against World Heritage Criteria .6 Management criteria .7 Recommendations Conclusions 51 Appendix One – Jersey’s fortifications 53 A 1.1 Historic fortifications A 1.2 A brief history of fortification in Jersey A 1.3 Fortification sites A 1.4 Brief for further work Appendix Two – the UK Tentative List 67 Appendix Three – World Heritage Sites that are fortifications 71 Appendix Four – assessment of La Cotte de St Brelade 73 Appendix Five – brief for this project 75 Bibliography 77 5 Acknowledgements This report would not have been possible without the very kind support, enthusiasm, time and hospitality of John Mesch and his colleagues of the Société Jersiase, including Dr John Renouf and John Stratford. -

Occupation of the Channel Islands from Wikipedia, the Free Encyclopedia

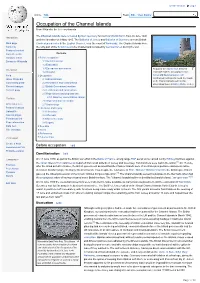

Create account Log in Article Talk Read Edit View history Occupation of the Channel Islands From Wikipedia, the free encyclopedia The Channel Islands were occupied by Nazi Germany for much of World War II, from 30 June 1940 Navigation until the liberation on 9 May 1945. The Bailiwick of Jersey and Bailiwick of Guernsey are two British Main page Crown dependencies in the English Channel, near the coast of Normandy. The Channel Islands were Contents the only part of the British Isles to be invaded and occupied by German forces during the war. Featured content Current events Contents Random article 1 Before occupation Donate to Wikipedia 1.1 Demilitarisation 1.2 Evacuation 1.3 Emergency government Interaction As part of the Atlantic Wall, between 1.4 Invasion 1940 and 1945 the occupying German Help 2 Occupation forces and the Organisation Todt About Wikipedia 2.1 Administration constructed fortifications round the coasts of the Channel Islands such as this Community portal 2.2 Resistance and collaboration observation tower at Battery Moltke, Jersey. Recent changes 2.3 British Government reaction Contact page 2.4 Fortification and construction 2.5 Repressions and deportations 2.5.1 Alderney concentration camps Toolbox 2.6 Representation in London What links here 2.7 Under siege Related changes 3 Liberation and legacy Upload file 3.1 Liberation Special pages 3.2 Aftermath Permanent link 3.3 War crime trials Page information 3.4 Legacy Data item 4 See also Cite this page 5 Notes 6 References Print/export 7 External links Create a book Before occupation [edit] Download as PDF Printable version Demilitarisation [edit] Languages On 11 June 1940, as part of the British war effort in the Battle of France, a long range RAF aerial sortie carried out by Whitley bombers against the Italian cities of Turin and Genoa departed from small airfields in Jersey and Guernsey.