The Effectiveness of a Credit Financing Model and the Potential of Regional

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download Article (PDF)

Advances in Social Science, Education and Humanities Research, volume 565 Proceedings of the International Conference on Education Universitas PGRI Palembang (INCoEPP 2021) Free School Leadership Meilia Rosani1, Misdalina1*), Tri Widayatsih1 1Universitas PGRI Palembang, Indonesia *Corresponding author. Email: [email protected] ABSTRACT The introduction of free schools needs to be dealt with seriously by the leader. Seriousness is shown by his ability to lead. Leadership is required so that the introduction of free schools can be guided and targets can be accomplished quickly and efficiently. The purpose of this study was to decide how free school leadership is in the Musi Banyuasin Regency (MUBA). This research uses a qualitative approach to the case study process. The data collection technique was conducted by interviewing, analyzing and recording the validity of the data used in the triangulation process. The results show that free school leadership in the MUBA district is focused on coordination, collaboration, productivity in the division of roles, the arrangement of the activities of the management team members in an integrated and sustainable manner between the district management team and the school. Keywords: Leadership, Cohesion, Performance, Sustainability 1. INTRODUCTION Regional Governments, that education and the enhancement of the quality of human resources in the The Free School that is introduced in MUBA regions are also the responsibility of the Regional Regency is a program of the MUBA Regency Government. In addition to this clause, the leaders of the Government that has been implemented since 2003. MUBA District Government, along with stakeholders Until now, the software has been running well. -

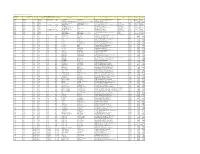

Colgate Palmolive List of Mills As of June 2018 (H1 2018) Direct

Colgate Palmolive List of Mills as of June 2018 (H1 2018) Direct Supplier Second Refiner First Refinery/Aggregator Information Load Port/ Refinery/Aggregator Address Province/ Direct Supplier Supplier Parent Company Refinery/Aggregator Name Mill Company Name Mill Name Country Latitude Longitude Location Location State AgroAmerica Agrocaribe Guatemala Agrocaribe S.A Extractora La Francia Guatemala Extractora Agroaceite Extractora Agroaceite Finca Pensilvania Aldea Los Encuentros, Coatepeque Quetzaltenango. Coatepeque Guatemala 14°33'19.1"N 92°00'20.3"W AgroAmerica Agrocaribe Guatemala Agrocaribe S.A Extractora del Atlantico Guatemala Extractora del Atlantico Extractora del Atlantico km276.5, carretera al Atlantico,Aldea Champona, Morales, izabal Izabal Guatemala 15°35'29.70"N 88°32'40.70"O AgroAmerica Agrocaribe Guatemala Agrocaribe S.A Extractora La Francia Guatemala Extractora La Francia Extractora La Francia km. 243, carretera al Atlantico,Aldea Buena Vista, Morales, izabal Izabal Guatemala 15°28'48.42"N 88°48'6.45" O Oleofinos Oleofinos Mexico Pasternak - - ASOCIACION AGROINDUSTRIAL DE PALMICULTORES DE SABA C.V.Asociacion (ASAPALSA) Agroindustrial de Palmicutores de Saba (ASAPALSA) ALDEA DE ORICA, SABA, COLON Colon HONDURAS 15.54505 -86.180154 Oleofinos Oleofinos Mexico Pasternak - - Cooperativa Agroindustrial de Productores de Palma AceiteraCoopeagropal R.L. (Coopeagropal El Robel R.L.) EL ROBLE, LAUREL, CORREDORES, PUNTARENAS, COSTA RICA Puntarenas Costa Rica 8.4358333 -82.94469444 Oleofinos Oleofinos Mexico Pasternak - - CORPORACIÓN -

Sustainable Agroforestry Models for Proposed Food Production in Post

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by International Journal on Advanced Science, Engineering and Information Technology Vol.6 (2016) No. 2 ISSN: 2088-5334 Sustainable Agroforestry Models for Proposed Food Production in Post-Mined Land Sites of South Sumatera Bandi Hermawan# # Department of Agricultural Cultivation, University of Bengkulu, Bengkulu, 38178, Indonesia E-mail: [email protected] Abstract — The reclamation areas of the opencast coal mining in South Sumatera are predominantly compact and nutrient-poor, marginal sites but have a high potential for cultivation of fast-growing trees and agricultural crops. This paper aims to promote several models of agroforestry in the post-mined land in South Sumatera as a new strategy in reclaiming degraded soil properties for both enviroment and economic purposes. About 5,000 ha of coal mining areas were observed to characterize the landscape and soil properties in the area, then overlaid with the landuse maps of post-mining plans issued by the company. Results showed that about 1,730 ha of the reclamation areas was suitable for agroforestry while the rest was for utilities, camping ground, water pond and grassland. Three models were proposed for the agroforestry areas, including (i) agrisilviculture model (1,190 ha), (ii) silvihorticulture model (203 ha), and (iii) local-species collection model for agrihortisilviculture (337 ha). Prior to the agroforestry establishment, all reclamation sites were subjected to the revegetation with fast-growing trees and other rejuvenation treatments in order to restore favour soil and microclimate conditions. The proposed components for each model were as follows: for agrisilviculture model were cultivation on the alley cropping system of trees and food crops, for silvihorticulture model were the plantation of fruit trees in the bench of water pond, and for local-species collection model for agrihortisilviculture were the cultivation of local forest and food crop species. -

Analisis Sektor Potensial Dan Keterkaitan Antar Wilayah Pada Perekonomian Kabupaten Ogan Komering Ulu (Oku) Tahun 2010-2016

KOLEGIAL – Vol.6, No.1. Juni 2018 P-ISSN 2088-5644; E-ISSN 2614-008X ANALISIS SEKTOR POTENSIAL DAN KETERKAITAN ANTAR WILAYAH PADA PEREKONOMIAN KABUPATEN OGAN KOMERING ULU (OKU) TAHUN 2010-2016 Lisa Hermawati1, Nopita Sari2 1,2Program Studi Ekonomi Pembangunan, Fakultas Ekonomi, Universitas Baturaja [email protected] Abstract The purpose of this study is to find out what potential sectors need to be developed in OKU Regency and find out the relationship between OKU District and the surrounding Regencies/Cities to support its economic growth. The results of this study indicate that in the period 2010-2016, there are 9 potential sectors that need to be developed in OKU Regency, namely the Agriculture, Forestry and Fisheries Sector; Water Supply, Waste Management, Waste and Recycling Sector; Wholesale and Retail Trade Sector, Car and Motorcycle Repair; Sector of Providing Accommodation and Foods and Drinks; Financial Services and Insurance Sector; Real Estate Sector; Education Services Sector; Health Services Sector and Social Activities; Other service sectors. Based on gravity analysis, the Regency with the most interaction with OKU Regency is Muara Enim Regency and the weakest interaction is Ogan Ilir Regency. The connection of Muara Enim Regency and OKU Regency is the biggest because the two regions have a close enough distance so that the interaction of them is the strongest. Keywords: potential sector, inter-region linkage, Location Quotient, Klassen Typologyy, Gravity Analysis Abstrak Tujuan penelitian ini untuk mengetahui sektor -

Food Security and Environmental Sustainability on the South Sumatra Wetlands, Indonesia Syuhada, A.*1, M

Sys Rev Pharm 2020; 11(3): 457 464 A multifaceted review journal in the field of pharmacy E-ISSN 0976-2779 P-ISSN 0975-8453 Food Security and Environmental Sustainability on the South Sumatra Wetlands, Indonesia Syuhada, A.*1, M. Edi Armanto2, A. Siswanto3, M. Yazid4, Elisa Wildayana5 1* Environmental Study Program, Postgraduate Program, Sriwijaya University, Jln Raya Palembang-Prabumulih KM 32, Indralaya Campus, South Sumatra, Indonesia 2.4.5 Faculty of Agriculture, Sriwijaya University, Jln Raya Palembang-Prabumulih KM 32, Indralaya Campus, South Sumatra, Indonesia 3 Faculty of Engineering, Sriwijaya University, Jln Raya Palembang-Prabumulih KM 32, Indralaya Campus, South Sumatra, Indonesia. Article History: Submitted: 25.12.2019 Revised: 22.02.2020 Accepted: 10.03.2020 ABSTRACT The research aimed to analyze food security and environmental continuous rice-based; extensive perennial-based crops; and vegetable- sustainability in the South Sumatra wetlands. This research conducted on based crops. The main typology was dominated by continuous rice-based the wetlands of Banyuasin Regency, By Using the Survey method system taking around 197.961 ha or 58.50% and the lowest level was interview with respondents, guided by a questionnaire through the Focus shown by vegetable-based crops around 20.998 ha or 6.20%. Group Discussion (FGD). All data collected, by analyzed with SPSS Keywords: Food security, environmental sustainability, wetlands program. The results showed that plants planted in wetlands vary widely, Correspondance: such as rice, corn, soy, sweet potatoes, nuts, and cassava. The diversity of Syuhada, A commodities is cultivated on high enough wetlands; they seek food Environmental Study Program, Postgraduate Program, farming in order to meet their own subsistence with little agricultural input, Sriwijaya University, making it relatively difficult for crops to be able to produce optimally. -

The Influence of Leading Commodity, Quality of Labor, Economic Structure, and Productivity of Labor Against Inequality of Income

Journal of Economics and Economic Education Research Volume19, Issue 4, 2018 THE INFLUENCE OF LEADING COMMODITY, QUALITY OF LABOR, ECONOMIC STRUCTURE, AND PRODUCTIVITY OF LABOR AGAINST INEQUALITY OF INCOME AMONG THE REGENCIES IN SOUTH SUMATRA PROVINCE, INDONESIA Syamsurijal Abdul Kadir, Sriwijaya University Azwardi, Sriwijaya University Anna Yulianita, Sriwijaya University Siti Rohima, Sriwijaya University ABSTRACT This research aims to know the influence of leading commodities, quality of labor (life expectancy and education), economic structure, and productivity of labor toward inequality of income among regencies in the Province of South Sumatra. The data used in this research are panel data consist of time series (2010-2016) and cross-section (14 regencies). The method of analysis used in this study is a multiple linear regression analysis technique. The results show that an increase in number of leading commodity of coffee, labor productivity of palm oil and economic structure can reduce the inequality of income among the regencies, while the increase in palm oil as a leading commodity, and labor productivity of coffee can increase income inequality among the regencies in South Sumatra Province. Keywords: Leading Commodity, Quality of Labor, Economic Structure, Labor Productivity, Income Inequality. INTRODUCTION The main objective of economic development in addition to create high growth is also to reduce some levels of poverty and inequality of income between groups either communities or regions. The development policy that prioritizes economic growth has led to increasingly high levels of inequality. A major factor that causes the problem of income inequality is economic growth. High economic growth that is not followed by a proper policy of equitable income distribution would lead to an increasingly widening income inequalityy. -

App 10-CHA V13-16Jan'18.1.1

Environmental and Social Impact Assessment Report (ESIA) – Appendix 10 Project Number: 50330-001 February 2018 INO: Rantau Dedap Geothermal Power Project (Phase 2) Prepared by PT Supreme Energy Rantau Dedap (PT SERD) for Asian Development Bank The environmental and social impact assessment is a document of the project sponsor. The views expressed herein do not necessarily represent those of ADB’s Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “Terms of Use” section of this website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of or any territory or area. Rantau Dedap Geothermal Power Plant, Lahat Regency, Muara Enim Regency, Pagar Alam City, South Sumatra Province Critical Habitat Assessment Version 13 January 2018 The business of sustainability FINAL REPORT Supreme Energy Rantau Dedap Geothermal Power Plant, Lahat Regency, Muara Enim Regency, Pagar Alam City, South Sumatra Province Critical Habitat Assessment January 2018 Reference: 0383026 CH Assessment SERD Environmental Resources Management Siam Co. Ltd 179 Bangkok City Tower 24th Floor, South Sathorn Road Thungmahamek, Sathorn Bangkok 10120 Thailand www.erm.com This page left intentionally blank (Remove after printing to PDF) TABLE OF CONTENTS 1 INTRODUCTION 1 1.1 PURPOSE OF THE REPORT 1 1.2 QUALIFICATIONS -

Download (199Kb)

PROCEEDING, SEMINAR NASIONAL KEBUMIAN KE-11 PERSPEKTIF ILMU KEBUMIAN DALAM KAJIAN BENCANA GEOLOGI DI INDONESIA QUANTITATIVE CHAR5A–C6TSEPRTIESMTBIECRS2O01F8T, GHREHACSLAEBAHTA PARSAAMNANIANDICATOR OF A COAL METHANE GAS IN TAMBANG BANKO, MUARA ENIM, SOUTH SUMATRA Anis Millayanti1* Ratih Purwaningsih2 Yusi Firmansyah3 Reza Mohammad Ganjar Gani4 Faculty of Geological Engineering, Padjdjaran University, Bandung *Corresponding Author: [email protected] ABSTRACT The observed area is one of the coal exploration areas in Indonesia, i.e. Muara Enim Formation in South Sumatra Basin. The purpose of this research is to find out CBM indicator based on cleat quantitative analysis and the value of its permeability. The methods used in the research includes cleat attribute measures, i.e. length, aperture, and cleat spacing in 3 Coal Seam, i.e A1, A2, and B1. The cleat attribute measures use Cubes and Match Sticks formula based on Lucia (1983). Seam A1 has an aperture ranged between 0.0344 – 0.062 cm, cleat spacing ranged between 2.624 – 3.809 cm, and permeability ranged between 2.658 – 31.13 Darcy based on Cubes model and 1.9937 – 23.344 Darcy based on Match Sticks.While Seam A2 has an aperture ranged between 0.0343 – 0.0672 cm, and cleat spacing ranged between 2.484 – 3.724 cm, and permeability ranged between 2.07 – 45.82 Darcy based on Cubes model and 1.5525 – 34.364 Darcy based on Match Sticks model. And Seam B1 has an aperture ranged between 0.0348 – 0.0423 cm, and cleat spacing ranged between 2.673 – 4.577 cm, and permeability ranged between 2.544 – 6.677 Darcy based on Cubes model and 1.9077 – 5.008 Darcy based on Match Sticks model. -

Review Results International Journal of GEOMATE

Review Results International Journal of GEOMATE DAFTAR ISI ➢ Pengantar dari Editor ➢ 2017-12-07 11-02AM - 18652-Dinar.pdf ➢ 2017-12-11 10-42AM - 18652-2.pdf ➢ reviewed 18652-Dinar.pdf 8/25/2020 Yahoo Mail - Fwd: Review Results: Int J of GEOMATE Fwd: Review Results: Int J of GEOMATE Dari: Zakaria ([email protected]) Kepada: [email protected]; [email protected]; [email protected]; [email protected] Tanggal: Senin, 11 Desember 2017 11.52 WIB Dear Authors, Thanks for your kind contribution. We have reviewers' comments on your paper (attached). Please send the revised paper by maximum of 4 days upon receiving this email. Please send response to reviewers by authors in separate file. An example of “response to reviewers by authors” is attached. Please use the following link: http://www.geomatejournal.com/ revised Best regards. -- Dr. Zakaria Hossain (Ph.D. Kyoto Univ.) Professor, Mie University, Japan Editor-in-Chief, Int. J. of GEOMATE Director, Sci. Eng. & Env. Int. Conf. General Secretary, GEOMATE Int. Soc. [email protected] [email protected] [email protected] [email protected] http://www.koku.bio.mie-u.ac.j p/ http://www.geomate.org/ http://www.confsee.com/ http://www.geomatejournal.com/ Example-Response to reviewer by Author.pdf 18.2kB 2017-12-11 10-42AM - 18652-2.pdf 20.1kB 2017-12-07 11-02AM - 18652-Dinar.pdf 24.7kB reviewed 18652-Dinar.pdf 837.4kB 1/1 GEOMATE Journal Review and Evaluation Submission Date 2017-12-07 11:02:11 Paper ID number 18652-Dinar Paper Title INTEGRATION OF SURFACE WATER MANAGEMENT IN URBAN AND REGIONAL SPATIAL PLANNING i. -

The Local Wisdom of Tunggu Tubang Culture in the Challenges of the Times (Study on Ethnical Semende District Muara Enim South Sumatera)

E3S Web of Conferences 68, 02011 (2018) https://doi.org/10.1051/e3sconf /20186802011 1st SRICOENV 2018 The Local Wisdom of Tunggu Tubang Culture in the Challenges of the Times (Study on Ethnical Semende District Muara Enim South Sumatera) Eni Murdiati1, Sriati3,Alfitri4, Muhammad1, and Ridhah Taqwa4 1Department of Environmental Science, Graduate Program-Universitas Sriwijaya, Palembang, Indonesia 2Preaching and Communication Faculty, Islamic State University of Raden Fatah, Palembang,Indonesia 3Department of Agribusiness, Faculty of Agriculture, Universitas Sriwijaya, Palembang, Indonesia 4Department of Sociology, Faculty of Social and Politic, Universitas Sriwijaya, Palembang, Indonesia Abstract. This study discusses the local wisdom of TungguTubang culture that is still embraced by the Semende ethnic community in MuaraEnim district. This study uses a qualitative descriptive approach with more emphasis on TungguTubang study facing the challenges in the era of globalization and modernization. The uniqueness local wisdom of TungguTubang culture which initially harmony with the surrounding natural environment, finally experienced a drastic change. The result of the research shows that the high- value award given by a TungguTubang to Semende society is not the expected reward anymore, because of the internal and external change factor of the social causes a change in the meaning and value of TungguTubangitself. 1 Introduction The issue of environmental crises, both in terms of management and conservation facing humans today, is increasingly very worrying. The loss of localwisdom cultural inherited by the ancestors for the following generations is due to various internal and external factors. The emergence of conflicts between families and communities in a culture area makes the tradition of deep-rooted customs increasingly shifting and extinct. -

Pelaksanaan Pengawasan Notaris Di Kabupaten Muara Enim, Kabupaten Pali, Kabupaten Lahat, Kabupaten Empat Lawang Dan Kota Pagaralam FOREMAN WIJAYA, Dr

Pelaksanaan Pengawasan Notaris di Kabupaten Muara Enim, Kabupaten Pali, Kabupaten Lahat, Kabupaten Empat Lawang dan Kota Pagaralam FOREMAN WIJAYA, Dr. Rimawati, S.H.,M.Hum Universitas Gadjah Mada, 2021 | Diunduh dari http://etd.repository.ugm.ac.id/ PELAKSANAAN PENGAWASAN NOTARIS DI KABUPATEN MUARA ENIM, KABUPATEN PALI, KABUPATEM EMPAT LAWANG, KABUPATEN LAHAT DAN KOTA PAGARALAM INTISARI Oleh : Foreman Wijaya*, Rimawati** Penelitian ini bertujuan untuk : 1) Mengetahui, mengkaji dan menganalisis yang menjadi latar belakang belum terbentuknya Majelis Pengawas Daerah di Kabupaten Muara Enim, Kabupaten Pali, Kabupaten Empat Lawang, Kabupaten Lahat dan Kota Pagaralam; (2) Mengetahui dan menganalisis tentang pelaksanaan pengawasan Notaris yang ada di daerah Kabupaten Muara Enim, Kabupaten Pali, Kabupaten Empat Lawang, Kabupaten Lahat dan Kota Pagaralam yang belum terbentuk Majelis Pengawas Daerah. Jenis penelitian ini adalah yuridis empiris yang bersifat deskriptif. Data yang digunakan terdiri dari data primer dan data sekunder. Data primer diperoleh dari subjek penelitian dengan cara wawancara menggunakan pedoman wawancara. Data sekunder diperoleh dengan studi kepustakaan. Data sekunder dilakukan dengan membaca, menelaah dan mengkritisi bahan hukum yang terdiri dari bahan hukum primer, bahan hukum sekunder dan bahan hukum tersier. Lokasi penelitian dilakukan di Provinsi Sumatea Selatan tepatnya di Kabupaten Muara Enim, Kabupaten Pali, Kabupaten Empat Lawang, Kabupaten Lahat dan Kota Pagaralam. Analisis dilakukan dengan metode kualitatif. Hasil penelitian dan pembahasan dapat ditunjukkan sebagai berikut: (1) Belum dibentuknya Majelis Pengawas Daerah di Kabupaten Muara Enim, Kabupaten Pali, Kabupaten Empat Lawang, Kabupaten Lahat dan Kota Pagaralam karena kurangnya jumlah Notaris di setiap Kabupaten Muara Enim, Kabupaten Pali, Kabupaten Empat Lawang, Kabupaten Lahat dan Kota Pagaralam, kurangnya Majelis Pengawas dari unsur akademisi dan tidak adanya Fakultas Hukum dan sampai saat ini belum dibentuknya Majelis Pengawas Daerah karena kekurangan dana. -

The Effectiveness of Free Education Policy in Indonesia (A Case Study on the District of Musi Banyuasin South Sumatera)

The Effectiveness of Free Education Policy in Indonesia (A Case Study on the district of Musi Banyuasin South Sumatera) Dr. Muhammad Iqbal Department of Psychology, Mercu Buana University Jakarta Consultant of Bappenas Jakarta, 2011 Email : [email protected] Abstract This study aims to determine the effectiveness of the free educational program that has been conducted in Indonesian local government. This study investigates a case study on the implementation of free education in the district of Musi Banyuasin South Sumatera. The research was conducted qualitatively by analyzing secondary data and conduct interviews with stake holders whom are the executive of education from the Department of Education, the Principal and parents. From the research, it was found that the implementation of free education in Indonesia is still a political commodity, free education policy in practice still have problems and weaknesses. The constraints faced by schools is the budget provided by the local government is the cost of education and minimum service standards budget given are not payed monthly, but given every 6months which causes problems and obstacles in school operations, which then affects the school’s ability to thrive and compete with other schools. In the implementation of free education, the school is still collects school tuition fee from the parents through the school committee, this is because it takes a very large budget. Free schools policy also has psychological implications, where students and parents tend to be less concerned about the needs of the school, because they think everything is free, so the students have low interest and motivation, causing them to change schools freely because of the free education policy.