Us Supreme Court Holds That Structured Dismissals Cannot Deviate from the Bankruptcy Code's Priority Scheme

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Thomas Hardiman Trump’S Supreme Court Shortlist: Thomas Hardiman

ALLIANCE FOR JUSTICE SNAPSHOT Trump’s Supreme Court Shortlist: Thomas Hardiman Trump’s Supreme Court Shortlist: Thomas Hardiman Thomas Hardiman, currently a judge on the U.S. Court of Appeals for the Third Circuit, is on President Trump’s shortlist for the U.S. Supreme Court. Protections for the Wealthy and Powerful Over the Rights of All Hardiman consistently sides with the wealthy and powerful at the expense of everyday people. He has taken the position that it should be more difficult for everyday Americans –– workers, consumers, middle-class Americans, and small business owners –– to hold corporations and bad actors accountable. In 2018, Hardiman announced to a Federalist Society Convention: “If I were able to do something unilaterally, I would probably institute a new federal rule that said that all cases worth less than $500,000 will be tried without any discovery.” Such a rule would enable corporations and those who commit wrongdoing to hide critical evidence and deprive those with modest-dollar cases of their ability to argue their case in court, including individuals whose cases involve important rights. Hardiman has repeatedly ruled against the rights of workers. In 2015, Hardiman sided against nearly 1,800 truck drivers who were laid off and not paid approximately $8 million they were owed due to the short notice. Under Hardiman’s decision about the company’s bankruptcy, which the Supreme Court later reversed, banks and other lenders were paid first. One person from the company who had terminal cancer was unable to find replacement health insurance and passed away. In another case, Hardiman ruled for Allstate after it fired 6,200 sales agents, offering to bring them back as independent contractors on the condition that they sign away their rights to existing claims against the company, including discrimination claims. -

Notre Dame Lawyer—2018 Notre Dame Law School

Notre Dame Law School NDLScholarship Notre Dame Lawyer Law School Publications 2018 Notre Dame Lawyer—2018 Notre Dame Law School Follow this and additional works at: https://scholarship.law.nd.edu/nd_lawyer Part of the Law Commons Recommended Citation Notre Dame Law School, "Notre Dame Lawyer—2018" (2018). Notre Dame Lawyer. 39. https://scholarship.law.nd.edu/nd_lawyer/39 This Book is brought to you for free and open access by the Law School Publications at NDLScholarship. It has been accepted for inclusion in Notre Dame Lawyer by an authorized administrator of NDLScholarship. For more information, please contact [email protected]. Q&A with Dean Newton Pg. 2 Big Ideas The expansion of ND Law’s intellectual property program is bearing fruit Pg. 20 20 18 A DIFFERENT KIND of LAWYER PHOTOGRAPHY Alicia Sachau and University Marketing Communications EDITOR Kevin Allen Notre Dame Lawyer 1337 Biolchini Hall Notre Dame, IN 46556 574-631-5962 [email protected] Inside 2 Dean Newton 4 Briefs & News 10 Profiles: A Different Kind of Lawyer 16 London Law at 50 20 Intellectual Property 26 Father Mike 30 Faculty News 36 Alumni Notes 44 In Memoriam 46 The Couples of ’81 48 Interrogatory Briefs Dean Newton Steps Down Joseph A. Matson Dean and Professor of Law Nell Jessup Newton will conclude her tenure as dean of Notre Dame Law School on June 30, 2019, after 10 years of service. What was your rela- ÅZ[\\QUMIVLM^MVUMM\QVO sion that leads to follow-up tionship with Notre Dame Fr. Ted. These memories MUIQT[)_ITSIZW]VL\PM before you became the Law are even more tender TISM[WZ\W\PM/ZW\\WKIV School’s dean? because Rob died in 1995 provide a moment to be My brother Rob Mier of lymphoma caused by his grateful for all the ways that attended ND on a Navy exposure to Agent Orange the Notre Dame community ROTC scholarship. -

Worry Over Mistreating Clots Drove Push to Pause J&J Shot

P2JW109000-6-A00100-17FFFF5178F ****** MONDAY,APRIL 19,2021~VOL. CCLXXVII NO.90 WSJ.com HHHH $4.00 Last week: DJIA 34200.67 À 400.07 1.2% NASDAQ 14052.34 À 1.1% STOXX 600 442.49 À 1.2% 10-YR. TREASURY À 27/32 , yield 1.571% OIL $63.13 À $3.81 EURO $1.1982 YEN 108.81 Bull Run What’s News In Stocks Widens, Business&Finance Signaling More stocks have been propelling the U.S. market higher lately,asignal that fur- Strength ther gains could be ahead, but howsmooth the climb might be remains up fordebate. A1 Technical indicators WeWork’s plan to list suggestmoregains, stock by merging with a but some question how blank-check company has echoes of its approach in smooth theywill be 2019,when the shared-office provider’s IPO imploded. A1 BY CAITLIN MCCABE Citigroup plans to scale up its services to wealthy GES Agreater number of stocks entrepreneurs and their IMA have been propelling the U.S. businesses in Asia as the market higher lately,asignal bank refocuses its opera- GETTY that—if historyisany indica- tions in the region. B1 SE/ tor—moregains could be ahead. What remains up forde- A Maryland hotel mag- bate, however, is how smooth natebehind an 11th-hour bid ANCE-PRES FR the climb will be. to acquireTribune Publish- Indicatorsthat point to a ing is working to find new ENCE stronger and moreresilient financing and partnership AG stock market have been hitting options after his partner ON/ LL rare milestones recently as the withdrew from the deal. -

Trump Judges: Even More Extreme Than Reagan and Bush Judges

Trump Judges: Even More Extreme Than Reagan and Bush Judges September 3, 2020 Executive Summary In June, President Donald Trump pledged to release a new short list of potential Supreme Court nominees by September 1, 2020, for his consideration should he be reelected in November. While Trump has not yet released such a list, it likely would include several people he has already picked for powerful lifetime seats on the federal courts of appeals. Trump appointees' records raise alarms about the extremism they would bring to the highest court in the United States – and the people he would put on the appellate bench if he is reelected to a second term. According to People For the American Way’s ongoing research, these judges (including those likely to be on Trump’s short list), have written or joined more than 100 opinions or dissents as of August 31 that are so far to the right that in nearly one out of every four cases we have reviewed, other Republican-appointed judges, including those on Trump’s previous Supreme Court short lists, have disagreed with them.1 Considering that every Republican president since Ronald Reagan has made a considerable effort to pick very conservative judges, the likelihood that Trump could elevate even more of his extreme judicial picks raises serious concerns. On issues including reproductive rights, voting rights, police violence, gun safety, consumer rights against corporations, and the environment, Trump judges have consistently sided with right-wing special interests over the American people – even measured against other Republican-appointed judges. Many of these cases concern majority rulings issued or joined by Trump judges. -

Georgetown Law's Federalist Society Student Chapter Will Host the 37Th

Georgetown Law’s Federalist Society Student Chapter will host the 37th National Student Symposium on March 9-10, 2018. The topic of the Symposium is "First Principles of the Constitution." FRIDAY, MARCH 9, 2018 Debate: The Judicial Power: The Judicial Duty to Follow the Law or a Discretionary Power of Judicial Review? 6:00 p.m. - 7:30 p.m. Hart Auditorium, Georgetown University Law Center Hamilton referred to the federal judiciary as the “least dangerous” branch of the new federal government. But the Court has clearly done more than he envisioned. What is its proper role? How much should judges interpret the exact text and how much should they look to the core principles the text seeks to protect? ● Justice Clint Bolick, Arizona Supreme Court ● Ed Whelan, President, Ethics & Public Policy Center, former Law Clerk to Justice Scalia, and Co-Editor, Scalia Speaks: Reflections on Law, Faith and Life Well Lived ● Moderator: Judge Kevin C. Newsom, United States Court of Appeals, Eleventh Circuit Presentation of the 2017 Article I Initiative Writing Contest Award by Mr. Christopher DeMuth, Co-Chairman, Board of Visitors, The Federalist Society 7:30 p.m. – 7:45 p.m. Hart Auditorium, Georgetown University Law Center Cocktail Reception 8:00 p.m. - 10:00 p.m. Supreme Court of the United States 1 First St., N.E., Washington, DC (NOTE: Due to space constraints, the reception is only open to the first 300 law student registrants.) SATURDAY, MARCH 10, 2018 Ending Government-by-Litigation: An Address by Attorney General Jeff Sessions (Conference Registration & ID REQUIRED) 8:30 a.m. -

Federalist Paper Template

THE Federalist PAPER THE MAGAZINE OF THE FEDERALIST SOCIETY • FEDSOC.ORG Summer 2018 THE FEATURES Federalist PAPER THE MAGAZINE OF THE FEDERALIST SOCIETY • FEDSOC.ORG BOARD OF DIRECTORS BOARD OF VISITORS Prof. Steven G. Calabresi, Chairman Mr. Christopher DeMuth, Co-Chairman Hon. David M. McIntosh, Vice Chairman Hon. Orrin G. Hatch, Co-Chairman Prof. Gary Lawson, Secretary Prof. Lillian BeVier Mr. Brent O. Hatch, Treasurer Mr. George T. Conway 4 National Student Hon. T. Kenneth Cribb Ms. Kimberly O. Dennis Hon. C. Boyden Gray Mr. Michael W. Gleba Symposium Mr. Leonard A. Leo, Executive VP Hon. Lois Haight Herrington Hon. Edwin Meese, III Hon. Donald Paul Hodel 6 Student Division Mr. Eugene B. Meyer, President Hon. Frank Keating, II Hon. Michael B. Mukasey Hon. Gale Norton 8 Lawyers Chapters Hon. Lee Liberman Otis, Senior VP Hon. Theodore B. Olson Prof. Nicholas Quinn Rosenkranz Mr. Andrew J. Redleaf Hon. William Bradford Reynolds 10 Faculty Division Ms. Diana Davis Spencer Mr. Theodore W. Ullyot 12 Practice Groups STAFF 14 Article I President Executive Vice President Senior Vice President Eugene B. Meyer Leonard A. Leo Lee Liberman Otis 16 State Courts & AGs Student Division Lawyers Chapters Peter Redpath, VP & Director Lisa Budzynski Ezell, VP & Director 17 Regulatory Kamron Kompani, Deputy Director Sarah Landeene, Deputy Director Transparency Kate Alcantara, Deputy Director Katherine Fugate, Associate Director Faculty Division Practice Groups 18 Membership Lee Liberman Otis, Director Dean Reuter, VP & General Counsel Laura Flint, Deputy Director Anthony Deardurff, Deputy Director Wesley G. Hodges, Associate Director 19 Resources Jennifer Weinberg, Associate Director Micah Wallen, Assistant Director Brigid Flaherty, Assistant Director Regulatory Transparency Project External Relations Devon Westhill, Director Jonathan Bunch, VP & Director Colton Graub, Project Assistant Peter Bisbee, Director, State Courts Elizabeth Cirri, Assistant Director Article I Initiative Nathan Kaczmarek, Director International Affairs James P. -

Senate Section (PDF929KB)

E PL UR UM IB N U U S Congressional Record United States th of America PROCEEDINGS AND DEBATES OF THE 109 CONGRESS, FIRST SESSION Vol. 151 WASHINGTON, THURSDAY, MAY 19, 2005 No. 67 Senate The Senate met at 9:30 a.m. and was ceed to executive session for the con- Yesterday, 21 Senators—evenly di- called to order by the President pro sideration of calendar No. 71, which the vided, I believe 11 Republicans and 10 tempore (Mr. STEVENS). clerk will report. Democrats—debated for over 10 hours The legislative clerk read the nomi- on the nomination of Priscilla Owen. PRAYER nation of Priscilla Richman Owen, of We will continue that debate—10 hours The Chaplain, Dr. Barry C. Black, of- Texas, to be United States Circuit yesterday—maybe 20 hours, maybe 30 fered the following prayer: Judge for the Fifth Circuit. hours, and we will take as long as it Let us pray. RECOGNITION OF THE MAJORITY LEADER takes for Senators to express their God of grace and glory, open our eyes The PRESIDENT pro tempore. The views on this qualified nominee. to the power You provide for all of our majority leader is recognized. But at some point that debate should challenges. Give us a glimpse of Your SCHEDULE end and there should be a vote. It ability to do what seems impossible, to Mr. FRIST. Mr. President, today we makes sense: up or down, ‘‘yes’’ or exceed what we can request or imagine. will resume executive session to con- ‘‘no,’’ confirm or reject; and then we Encourage us again with Your promise sider Priscilla Owen to be a U.S. -

Measures Highlight Campaign Plan

On the ballot Why should you care whether the U.S. Senate confirms a Measures highlight campaign plan Supreme Court nominee now? There are two very important ini- osition 227 of 1998 and would pro- sembly and Senate, Congress and It may seem like little more than tiatives on the November ballot, the vide services for ALL students in the Presidential campaigns. The CTA noise out of Washington, D.C. , but Children’s Education and Health state of California that would put Board approved a Campaign Plan at the current battle to get the U.S. Sen- Care Protection Act (CEHCP), which them on the path to becoming bilin- their May 17 meeting. Information ate to do its job by considering a new is the extension of the Prop 30 tax on gual. on the Campaign Plan will be shared high court nominee has important im- high wage earners, and the Education CTA members will be asked to at State Council, Service Center plications for every student, every ed- for a Global Economy (EdGE), work in support of these initiatives as Councils and in local rep meetings. ucator, every school, and every union which would repeal and amend prop- well as targeted races in the State As- member in our nation. In the years ahead, the U.S. Su- preme Court may rule on issues in- cluding the rights of teachers to due Field work surprises process and a fair hearing when charges are leveled. It could rule on CSO staff Ed Sibby got a welcome surprise when covering an the rights of schools to be fully fund- Alliance To Reclaim Our Schools walk-in event in Lake Elsinore ed in order to provide a high quality in early May. -

Confirming Supreme Court Justices in a Presidential Election Year

Washington University Law Review Volume 94 Issue 4 2017 Confirming Supreme Court Justices in a Presidential Election Year Carl Tobias University of Richmond Follow this and additional works at: https://openscholarship.wustl.edu/law_lawreview Part of the Judges Commons, and the Law and Politics Commons Recommended Citation Carl Tobias, Confirming Supreme Court Justices in a Presidential Election Year, 94 WASH. U. L. REV. 1089 (2017). Available at: https://openscholarship.wustl.edu/law_lawreview/vol94/iss4/11 This Commentary is brought to you for free and open access by the Law School at Washington University Open Scholarship. It has been accepted for inclusion in Washington University Law Review by an authorized administrator of Washington University Open Scholarship. For more information, please contact [email protected]. CONFIRMING SUPREME COURT JUSTICES IN A PRESIDENTIAL ELECTION YEAR CARL TOBIAS Justice Antonin Scalia’s death prompted United States Senate Majority Leader Mitch McConnell (R-Ky.) and Judiciary Committee Chair Chuck Grassley (R-Iowa) to argue that the President to be inaugurated on January 20, 2017—not Barack Obama—must fill the empty Scalia post.1 Obama in turn expressed sympathy for the Justice’s family and friends, lauded his consummate public service, and pledged to nominate a replacement “in due time,” contending that eleven months remained in his administration for confirming a worthy successor.2 Obama admonished that the President had a constitutional duty to nominate a superlative aspirant to the vacancy, which must not have persisted for more than one year, while the Senate had a constitutional responsibility to advise and consent on the nominee proffered.3 Because this dynamic affected efficacious Supreme Court operations and precipitated a constitutional standoff, the issue merits analysis. -

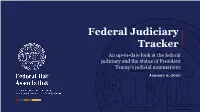

Federal Judiciary Tracker

Federal Judiciary Tracker An up-to-date look at the federal judiciary and the status of President Trump’s judicial nominations January 9, 2020 Trump has had 184 federal judges confirmed while 65 seats remain vacant without a nominee Status of key positions President Trump inherited 108 requiring Senate federal judge vacancies confirmation !" As of January 9, 2020: No nominee Awaiting confirmation 157 judiciary positions have opened up Confirmed during Trump’s presidency and either #! remain vacant or have been filled Source: National Journal as of January 9, 2020 Total: #$$ 265 potential Trump nominations Trump has had more circuit judges confirmed than the average of recent presidents at this point Number of Federal Judges Nominated and Confirmed *+,-. #%% ") ( >739+7?9=?:,+9=@,ABC==== 57+?,79=?:,+9=@,ABC==== D,.+C-C=5:,+9=@,ABC /01-1 &$ (" ( Source: Federal Judicial Center 2,34 #%' %) 56789:8 #"( %) ( ;<=2,34 &" %# ( In three years, Trump has confirmed a higher number of circuit judges as prior presidents in four years Number of Federal Judges Nominated and Confirmed *+,-. !"" '( ) >739+7?9=?:,+9=@,ABC==== 57+?,79=?:,+9=@,ABC==== D,.+C-C=5:,+9=@,ABC /01-1 !#! "( ) Source: Federal Judicial Center 2,34 !$% "' 56789:8 !$& "( ) ;<=2,34 !#% #) ) An overview of the Article III courts US District Courts US Court of Appeals Supreme Court Organization: Organization: Organization: ! The nation is split into 94 ! Federal judicial districts ! The Supreme Court is the federal judicial districts are organized into 12 highest court in the US ! The District of Columbia circuits, which each have a ! There are nine justices on and four US territories court of appeals. -

No Institution Exemplifies Georgetown Law's Ties to the Supreme Court

FALL/WINTER 2018 No institution exemplifies Georgetown Law’s ties to the Supreme Court better than our celebrated Supreme Court Institute GEORGETOWN LAW Fall/Winter 2018 ANN W. PARKS, Esq. (G’14, LL.M.’16) Editor BRENT FUTRELL Director of Design INES HILDE Associate Director of Design MIMI KOUMANELIS Executive Director of Communications TANYA WEINBERG Director of Media Relations and Deputy Director of Communications RICHARD SIMON Director of Web Communications JACLYN DIAZ Communications and Social Media Manager BEN PURSE Senior Video Producer JERRY COOPER Communications Associate CONTRIBUTORS Julie Bourbon, Barbara Grzincic, Melanie D.G. Kaplan, Greg Langlois, Sara Piccini, Abby Reecer, Mark Smith, Anna Louie Sussman MATTHEW F. CALISE Director of Alumni Affairs GENE FINN Assistant Dean of Development and Alumni Relations WILLIAM M. TREANOR Dean of the Law Center Executive Vice President, Law Center Affairs Front and back cover photos: Brent Futrell Contact: Editor, Georgetown Law Georgetown University Law Center 600 New Jersey Avenue, N.W. Washington, D.C. 20001 [email protected] Address changes/additions/deletions: 202-687-1994 or e-mail [email protected] Georgetown Law magazine is on the Law Center’s website at www.law.georgetown.edu Copyright © 2018, Georgetown University Law Center. All rights reserved. Orientation 2018 Michelle Wadolowski (L’21) contemplates the Smithsonian National Museum of African American History and Culture. Photo Credit: Brent Futrell 2018 Fall/Winter 1 INSIDENEWS / CONVINCING EVIDENCE / 10 / 14 Four Cases, Three Circuits, Three Weeks A Civil, Civic Conversation Georgetown Law’s Appellate Litigation Clinic is often compared to a Parkland student, Georgetown Law student speak at an O’Neill boutique appellate firm. -

Presidential Voter Guide

2016 NHLA Presidential Candidate Voter Guide On February 24, 2016, NHLA issued a questionnaire to each of the presidential candidates from both major political parties with questions that were based on its 2016 Hispanic Public Policy Agenda. Each of the candidates was invited to provide their responses to these questions by March 25, 2016. As of September 27, 2016, no responses have been received from candidate Donald Trump. In lieu of his responses, information on the candidate’s positions are included based on publicly available sources. This voter guide will be updated when or if the candidate’s responses are received. NHLA does not endorse or oppose any candidate for public office. This document is based on the responses that were provided to us by the presidential candidates or their public statements. It is not intended to interpret, examine, or opine on any of the responses or the lack thereof. While we encourage the public to read these responses, any candidate’s fitness for office should be judged on a variety of qualifications that go beyond their responses to the questions that follow. National Hispanic Leadership Agenda • 815 16th St. NW, 3rd Floor • Washington, DC 20006 • 202‐508‐6919 • nationalhispanicleadership.org • @NHLAgenda TOPIC BACKGROUND QUESTION CANDIDATE RESPONSE FEDERAL Since 2011, federal efforts to reduce the deficit In your investment agenda As president, I would prioritize investments that drive job creation, productivity, and higher wages have relied more on cuts to domestic — including infrastructure that will put Americans back to work, education from early childhood BUDGET for the federal budget, what discretionary programs rather than on raising to college to unlock the potential of every American, basic research, clean energy, job training and revenue.