Keeping the Lights on and the Traffic Moving: Sustaining the Benefits of Rail Freight For

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Framework Capacity Statement 2021

OFFICIAL Framework Capacity Statement 2021 Including consultation on alternative approaches to presenting capacity information Network Rail April 2021 Network Rail Framework Capacity Statement April 2021 1 OFFICIAL Contents Framework Capacity Statement Annex: Consultation on alternative approaches 1. Purpose 4. Background to the 2021 consultation 1.1 Purpose 4 4.1 Developments since 2016 17 4.2 Timing and purpose 17 2. Framework capacity on Network Rail’s network 2.1 Infrastructure covered by this statement 7 5. Granularity of analysis – examples and issues 2.2 Framework agreements in Great Britain 9 5.1 Dividing the railway geographically 19 2.3 Capacity allocation 11 5.2 Analysis at Strategic Route level 20 5.3 Analysis at SRS level 23 3. How to identify framework capacity 5.4 Constant Traffic Sections 25 3.1 Capacity of the network 13 3.2 Capacity allocated in framework agreements 13 6. The requirement 3.3 Capacity available for framework agreements 14 6.1 Areas open for interpretation in application 28 3.4 Using the timetable as a proxy 14 6.2 Potential solutions 29 3.5 Conclusion 15 6.3 Questions for stakeholders 30 Network Rail Framework Capacity Statement April 2021 2 OFFICIAL 1. Purpose Network Rail Framework Capacity Statement April 2021 3 OFFICIAL 1.1 Purpose This statement is published alongside Network Rail’s Network current transformation programme, to make the company work Statement in order to meet the requirements of European better with train operators to serve passengers and freight users. Commission Implementing Regulation (EU) 2016/545 of 7 April 2016 on procedures and criteria concerning framework Due to the nature of framework capacity, which legally must not agreements for the allocation of rail infrastructure capacity. -

Implications for the Rail Freight Sector of Stricter European Union Locomotive Emission Limits: a UK Perspective

Implications for the rail freight sector of stricter European Union locomotive emission limits: a UK perspective Article Accepted Version Wilde, M. L. (2016) Implications for the rail freight sector of stricter European Union locomotive emission limits: a UK perspective. Business Law Review, 37 (4). pp. 118-123. ISSN 0143-6295 Available at http://centaur.reading.ac.uk/66749/ It is advisable to refer to the publisher’s version if you intend to cite from the work. See Guidance on citing . Published version at: http://www.kluwerlawonline.com/abstract.php?area=Journals&id=BULA2016024 Publisher: Kluwer Law International All outputs in CentAUR are protected by Intellectual Property Rights law, including copyright law. Copyright and IPR is retained by the creators or other copyright holders. Terms and conditions for use of this material are defined in the End User Agreement . www.reading.ac.uk/centaur CentAUR Central Archive at the University of Reading Reading’s research outputs online Implications for the Rail-freight Sector of Stricter EU Locomotive Emission Limits: a UK perspective INTRODUCTION The European rail freight sector has grown exponentially over the past twenty to thirty years as the limitations of road transport have become increasingly apparent.1 Moreover, moving more freight by rail is seen as a greener alternative.2 Thus, in some respects it is a case of ‘back to the future’ and the halcyon days when the majority of freight was moved by rail; although it must be acknowledged that in the twenty-first century the bulk of freight is still moved by road and this is likely to be the case for the foreseeable future. -

Annex A: Organisations Consulted

Annex A: Organisations consulted This section lists the organisations who have been directly invited to respond to this consultation: Administrative Justice and Tribunals Service Advanced Transport Systems AEA Technology Plc Aggregate Industries Alcan Primary Metal Europe Alcan Smelting & Power UK Alstom Transport Ltd Amey Plc Angel Trains Arriva Trains Wales ASLEF Association of Chief Police Officers in Scotland Association of Community Rail Partnerships Association of London Government Association of Railway Industry Occupational Physicians Association of Train Operating Companies Atkins Rail Avon Valley Rail Axiom Rail BAA Rail Babcock Rail Bala Lake Railways Balfour Beatty plc Bluebell Railway PLC Bombardier Transportation BP Oil UK Ltd Brett Aggregates Ltd British Chambers of Commerce British Gypsum British International Freight Association British Nuclear Fuels Ltd British Nuclear Group Sellafield Ltd British Ports Association British Transport Police BUPA Buxton Lime Industries Ltd c2c Rail Ltd Cabinet Office Campaign for Better Transport Carillion Rail Cawoods of Northern Ireland Cemex UK Cement Ltd Channel Tunnel Safety Authority Chartered Institute of Logistics & Transport Chiltern Railways Company Ltd City of Edinburgh Council Civil Aviation Authority Colas Rail Ltd Commission for Integrated Transport Confederation of British Industry Confederation of Passenger Transport UK Consumer Focus Convention of Scottish Local Authorities Correl Rail Ltd Corus Construction & Industrial CrossCountry Crossrail Croydon Tramlink Dartmoor -

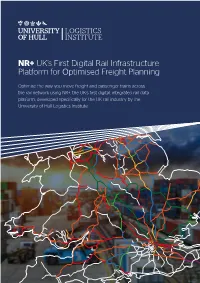

NR+ UK's First Digital Rail Infrastructure Platform for Optimised Freight Planning

LOGISTICS INSTITUTE NR+ UK’s First Digital Rail Infrastructure Platform for Optimised Freight Planning Optimise the way you move freight and passenger trains across the rail network using NR+, the UK’s first digital, integrated rail data platform, developed specifically for the UK rail industry by the University of Hull Logistics Institute. and functionalities for passengerplanning. and functionalities for data willincludeallrelevant ofNR+ conflicts. versions possession Later (RA),electrification engineering availability andpotential gauge, weight, length,route suchasloading criteria basedonkey routes, analyserail to you The applications allow planning. route freight for includesalldatarequired of NR+ version The first theirsolutiondevelopment. thedatafor party tapinto to third any with openAPIsfor database, asingle,integrated into movements planningandschedulingrail for required NR+ University ofHull University Data Sources Database APIs Applications Suite brings together, for the first time, the multiple and diverse information sources sources information the first time,themultipleanddiverse for bringstogether, Suite Tiplocks Infrastrucutre Manager Infrastructure and Schedule Visualisation NESA Implementation Infrastructure Asset API Train Route Planning Initial Possessions BPlan and Conflicts Workflow Load Books Reporting and Analytics Geospatial Data Train Timetabling Development Scheduling API Incident and Delays Future Schedules Management Possessions (EAS) Alerts and Notifications QJ Paths Simulation Development 3rd Party3rd 3rd -

Rail Freight and Business

Value and Importance of Rail Freight July 2010 Contents Contents EXECUTIVE SUMMARY 4 STRATEGIC CONTEXT 7 1 RAIL FREIGHT’S ROLE IN A PROSPEROUS BRITAIN 11 Rail freight’s role 11 Re-emergence of rail freight 12 The changing role 13 The freight market 13 Container business on rail 14 The complementary role of road freight 16 2 RAIL FREIGHT AND BUSINESS 17 Service to business 17 Ensuring reliability 17 Competition 18 Growing use of rail freight 18 Fuel efficiency 19 Buying the benefits of rail freight 20 3 RAIL FREIGHT AND THE CONSUMER 21 Supporting our everyday lives 21 Rail freight and the passenger rail network 21 4 RAIL FREIGHT AND THE ENVIRONMENT 22 The journey of a tin of beans 23 Other pollutants 24 5 RAIL FREIGHT AND COMMUNITIES 25 Making Britain’s roads safer 25 Easing congestion 25 Connecting communities 26 Reducing air pollution 26 6 VALUING RAIL FREIGHT 28 Valuing the contribution of rail freight 28 Other economic impacts 29 7 RAIL FREIGHT’S SUPPORT TO THE REST OF RAIL INDUSTRY 31 8 RAIL FREIGHT AND THE FUTURE 33 The continued growth of rail freight 33 Ensuring a successful future 34 Vision for the future 35 Working in collaboration 36 2 Contents Figures Figure 1.1 Rail freight in Britain (1988-2008) 12 Figure 2.1 Freight train performance over time 15 Figure 2.2 A Tesco branded train 19 Figure 2.3 Distance a tonne of goods can travel on a gallon of diesel 19 Figure 4.1 UK greenhouse gas emissions by cause - 2007 22 Figure 4.2 Road and rail freight – grammes of CO 2 per tonne km 23 Figure 4.3 The journey of a tin of beans 23 Figure 8.1 Network RUS economic scenarios 34 Figure 8.2 Potential growth in rail freight tonne km carried between 2006/07 and 2031 under different scenarios 34 3 Executive Summary Executive Summary An effective way of transporting goods across the country, rail freight is vital to Britain’s economy. -

Near Miss Involving a Freight Train and Two Passenger Trains, Carstairs

Chris O’Doherty RAIB Relationship & Recommendations Handling Manager Telephone 0845 301 3356 E-mail chris.o’[email protected] 28 September 2011 Ms Carolyn Griffiths Chief Inspector of Rail Accidents Rail Accident Investigation Branch Block A 2nd Floor Dukes Court Dukes Street Woking GU21 5BH Dear Carolyn Near miss involving a freight train and two passenger trains, Carstairs I write to report1 and update on the consideration given and the action taken in respect of the recommendations addressed to ORR in the above report published on 19 March 2010. The annex to this letter provides full details of the consideration given/action taken in respect of recommendations 1, 2 and 3 where: • recommendations 1 and 3 have been implemented2 and; • recommendation 2 has been implemented by Colas Rail, DB Schenker, GB Railfreight and Freightliner and is in the process of being implemented3 by DRS. We do not propose to take any further action in respect of recommendations 1 and 3 unless we become aware that any of the information is inaccurate in which case we will write to you again4. We expect to provide an update to recommendation 2 in November 2011. We expect to publish this report on the ORR website on 14 October 2011. Yours Sincerely Chris O’Doherty 1 In accordance with Regulation 12(2)(b) of the Railways (Accident Investigation and Reporting) Regulations 2005 2 In accordance with Regulation 12(2)(b)(i) 3 In accordance with Regulation 12(2)(b)(ii) 4 In accordance with Regulation 12((2)(c) Doc # 427619.01 Head Office: One Kemble Street, London WC2B 4AN T: 020 7282 2000 F: 020 7282 2040 www.rail-reg.gov.uk Annex A Initial Consideration by ORR All 3 recommendations contained in the report were addressed to ORR when RAIB published its report on 31 January 2011. -

S17 GB Railfreight Decision Letter

Katherine Goulding Executive, Access and Licensing [email protected] 29 February 2016 Ian Kapur Nick Coles National Access Manager Customer Relationship Executive GB Railfreight Ltd Network Rail Infrastructure Ltd 3rd Floor One Eversholt Street 55 Old Broad Street London NW1 2DN London EC2M 1RX Dear Ian and Nick, Directions in respect of a track access contract between Network Rail Infrastructure Limited and GB Railfreight Limited PART ONE: OVERVIEW Introduction 1. On 29 February 2016 the Office of Rail and Road (ORR) issued directions under section 17 of the Railways Act 1993 (the Act) to Network Rail Infrastructure Limited (Network Rail) to enter into a track access contract (TAC) with GB Railfreight Limited (GBRf) as formally requested by GBRf on 1 September 2015. The TAC we have directed contains some amendments to that originally submitted by GBRf. This letter is to explain our directions and the reasons for them. 2. We also received similar applications (the Applications) for contracts under section 17 of the Act from other freight operating companies (FOCs). There were issues that were common to all of the Applications and where they had not been able to reach agreement with Network Rail. This enabled us to adopt a broad perspective and to try to achieve consistency between the FOCs making these applications (the Applicants). Summary 3. GBRf and the other Applicants were unable to agree terms for new TACs with Network Rail. We are today issuing directions and decision letters in respect of all of the Applications. ORR has directed Network Rail to enter into TACs that include the following terms: All Level One Access Rights in existing contracts to be carried over as one hour windows. -

Annual Report and Audited Financial Statements 2013 RAIL JOURNEYS 2013 of the WORLD

RAIL JOURNEYS 2013 OF THE WORLD Annual Report and Audited Financial Statements 2013 RAIL JOURNEYS 2013 OF THE WORLD The theme for this year’s annual report and accounts is rail journeys of the world. Find out more about each journey at the back of this booklet. Contents Trustee Company’s responsibilities in respect of Statement of contributions Trustee Company The Railways and summary responsibilities Pension of contributions in relation to The Trustee’s Scheme Audited payable in the year audited financial Investment Financial statements Report Appendices Statements 04 07 10 11 20 21 22 23 24 35 38 39 Actuary’s Key Statistics Report Chairman’s Independent The Trustee introduction Auditor’s Company report Independent Annual Report Auditor’s Statement about contributions to the Trustee of the RPS On behalf of your Trustee Board I introduce the Annual Report and Audited Financial Statements of the Railways Pension Scheme (‘the Scheme’) for the year ended 31 December 2013. Investment returns in 2013 were reasonably strong. The Growth (Pooled) Fund, in which well over half the Scheme’s assets are now invested, performed well both in absolute terms (8.6%) and against benchmark (3.5%), propelled by another “double digit” year for the equities in which more than 40% of that fund is invested. The Growth Fund will not, however, match the performance of equities; rather, it is designed to balance out the risks and volatile returns associated with single-asset strategies by investing in a wide range of assets, targeting a long-term return of 5% per annum above UK RPI inflation. -

Rail Freight: Delivering for Britain

Executive SummaryExecutive Rail Freight: Delivering for Britain 1 Contents Executive SummaryExecutive Executive Summary 4 Introduction 6 The story of rail freight 7 Framework for a successful freight sector 10 Government policy should be aligned across modes 12 A set of consistent legal, commercial and regulatory mechanisms is needed to underpin continued business confidence and private sector investment 13 A network and timetable that is co-ordinated on a GB-wide basis is essential 14 Modelling capabilities should be enhanced which better capture the value of rail freight, to help make choices about network use 16 The GB-wide charging regime that provides long-term clarity and is affordable should be retained 16 An industry structure that provides strong incentives to all parties to encourage freight growth should be prioritised 17 Industry processes that provide flexibility for freight to respond to changing industrial and logistics demands must be retained 18 Case studies 19-23 1. Rail freight building a strong and balanced economy 19 2. Freight supporting Network Rail and the delivery of passenger services 20 3. Delivering benefits to businesses 20 4. Supporting the delivery of major infrastructure projects 22 5. Investment in environmental benefits 23 6. Discover the UK’s biggest mover of metals 23 This document is produced and distributed by Rail Delivery Group. All material is property of Rail Delivery Group Ltd. 2 Rail Freight: Delivering for Britain Contents 3 Executive Executive SummaryExecutive Summary SummaryExecutive This document is a submission to the Williams Government policy should be aligned Review on behalf of the RDG Freight Board. across modes The rail freight industry is vital to the A set of consistent legal, commercial economic success of Great Britain, delivering and regulatory mechanisms is needed to around £1.7bn of economic benefits and underpin continued business confidence supplying £30bn of goods to customers and private sector investment across Britain each year1. -

Railway Upgrade Plan

Railway Upgrade Plan 2017/18 02 Rail in Britain Contents 03 Rail in Britain Contents Safe Affordable Our Railway Upgrade Plan at a glance 04 About us 05 2015-16 was the ninth year in a row with Network Rail operating Message from our Chief Executive 06 no passenger or costs have fallen by 6 Our routes at a glance 08 workforce fatalities in 46% since 2003-04 train accidents1 Anglia 10 The UK has the best safety £10.1bn added value London North Eastern and East Midlands 16 rail contributes to UK record of the ten largest London North Western 22 European railways2 economy every year7 South East 28 Wales 34 Wessex 40 Reliable Growing Western 46 Passenger numbers have Scotland 52 In 2015-16, 89.1% doubled since 1997-988, of train services Freight and National Passenger Operators 58 and they are expected arrived on time3 to double again by 20409 Property 62 Regional Maps 64 The number of delays There were an average of fell by 40% between 4.7m passenger journeys 2006-07 and 2014-154 per day in 2015-1610 In a European comparison, Britain comes second in terms Over 3,800 extra trains 5 of passenger satisfaction per day ran in 2015-16, 11 (after Finland but ahead of France, compared to 1997-98 Germany and other European countries) 1Annual Safety Performance Report, RSSB (2016) 7Our customers, our people, Rail Delivery Group (2016) 2Annual Safety Performance Report, RSSB (2016) 8ORR data portal 3Rail Statistics Compendium 2015-16 Annual, Office of Rail and Road (2016) 9Our customers, our people, Rail Delivery Group (2016) 4Rail’s transformation in numbers, Rail Delivery Group (2016) 10ORR data portal 5What makes Britain’s railways great, Rail Delivery Group (2017) 11Rail’s transformation in numbers, Rail Delivery Group (2016) 6Rail’s transformation in numbers, Rail Delivery Group (2016) 404 Our Railway Upgrade Plan at a glance About us 055 Our Railway Upgrade Plan at a glance About us 2014 Network Rail owns and maintains We are a public sector, arms-length body of the Department – Reopening of the line at Dawlish, after the track was destroyed in winter storms. -

HS2 Must Deliver Its Promises on Rail Freight Vital Capacity Potential Must Not Get Overlooked by ‘Speed’ Debate

140 March 2020 NEWS www.rfg.org.uk Helping ensure a sustainable future for UK rail freight HS2 must deliver its promises on rail freight Vital capacity potential must not get overlooked by ‘speed’ debate. P.3 RFG welcomes On 11 February, Rail Freight Group (RFG) network where HS2 trains will operate. This is Joe O’Donnell as its strongly welcomed the Government essential to allow freight operators and custom- announcement that HS2 is to be delivered ers to develop their future plans, and to ensure new Head of Policy in full, with work on Phases 1 and 2A that the benefits of HS2 can now be delivered given the green light to commence immedi- in practice.” ately and Phase 2B to be developed towards implementation. Views from the sector: HS2 has the potential to deliver significant ben- DB Cargo CEO Hans-Georg Werner said HS2 efits for rail freight by releasing capacity for new represented a “once in a generation” opportu- services on the existing network. With each nity to massively bolster rail capacity, providing freight train producing 76% less CO2 than the significant economic and environmental bene- equivalent road journey, HS2 can also help fits for freight operators. decarbonise freight transport by allowing new P.4 services to operate, taking more HGVs off the “This is fantastic news for the rail freight in- East Midlands congested road network. However, to date, dustry and its customers. We are pleased the Gateway opens for the Government has not confirmed how much Government has recognised the strength of the business capacity will be made available for freight once many arguments the industry made for build- the new line is open. -

Network Licence Condition 7 (Land Disposal): Redhill Sidings, Surrey

30 September 2016 Network licence condition 7 (land disposal): Redhill Sidings, Surrey Decision 1. On 8 August 2016, Network Rail gave notice of its intention to dispose of land at Redhill Sidings (the land), in accordance with paragraph 7.2 of condition 7 of its network licence. The land is described in more detail in the notice (copy attached). Network Rail subsequently provided additional plans included at Annex B. 2. We have considered the information supplied by Network Rail including the responses received from third parties you have consulted. For the purposes of condition 7 of Network Rail’s network licence, ORR consents to the disposal of the land in accordance with the particulars set out in its notice. Reasons for decision 3. We note Network Rail has consulted all relevant stakeholders with current information and no other reasonably foreseeable railway use for the land was identified. 4. In considering the proposed disposal we also note: • there is no evidence that railway operations would be affected adversely; • the scheme will facilitate the new platform 0 project at Redhill station; a requirement relating to the Brighton mainline upgrade and in accordance with the December 2018 programmed timetable; and • Network Rail’s subsequent clarification to us that it had overstated in its submission the amount of land proposed for disposal. Network Rail provided a new plan showing a larger area of land to be acquired for the introduction of services at platform 0. The correction is shown at Annex B. 5. Based on all the evidence we have received and taking into account all the material facts and views relevant to our consideration under condition 7, we are satisfied that there are no further issues for us to address.