AECO Gas Storage Partnership Ag Energy Co-Operative Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cenovus Reports Second-Quarter 2020 Results Company Captures Value by Leveraging Flexibility of Its Operations Calgary, Alberta (July 23, 2020) – Cenovus Energy Inc

Cenovus reports second-quarter 2020 results Company captures value by leveraging flexibility of its operations Calgary, Alberta (July 23, 2020) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) remained focused on financial resilience in the second quarter of 2020 and used the flexibility of its assets and marketing strategy to adapt quickly to the changing external environment. This positioned the company to weather the sharp decline in benchmark crude oil prices in April by reducing volumes at its oil sands operations and storing the mobilized oil in its reservoirs for production in an improved price environment. While Cenovus’s financial results were impacted by the weak prices early in the quarter, the company captured value by quickly ramping up production when Western Canadian Select (WCS) prices increased almost tenfold from April to an average of C$46.03 per barrel (bbl) in June. As a result of this decision, Cenovus reached record volumes at its Christina Lake oil sands project in June and achieved free funds flow for the month of more than $290 million. “We view the second quarter as a period of transition, with April as the low point of the downturn and the first signs of recovery taking hold in May and June,” said Alex Pourbaix, Cenovus President & Chief Executive Officer. “That said, we expect the commodity price environment to remain volatile for some time. We believe the flexibility of our assets and our low cost structure position us to withstand a continued period of low prices if necessary. And we’re ready to play a significant -

Middle East Oil Pricing Systems in Flux Introduction

May 2021: ISSUE 128 MIDDLE EAST OIL PRICING SYSTEMS IN FLUX INTRODUCTION ........................................................................................................................................................................ 2 THE GULF/ASIA BENCHMARKS: SETTING THE SCENE...................................................................................................... 5 Adi Imsirovic THE SHIFT IN CRUDE AND PRODUCT FLOWS ..................................................................................................................... 8 Reid l'Anson and Kevin Wright THE DUBAI BENCHMARK: EVOLUTION AND RESILIENCE ............................................................................................... 12 Dave Ernsberger MIDDLE EAST AND ASIA OIL PRICING—BENCHMARKS AND TRADING OPPORTUNITIES......................................... 15 Paul Young THE PROSPECTS OF MURBAN AS A BENCHMARK .......................................................................................................... 18 Michael Wittner IFAD: A LURCHING START IN A SANDY ROAD .................................................................................................................. 22 Jorge Montepeque THE SECOND SPLIT: BASRAH MEDIUM AND THE CHALLENGE OF IRAQI CRUDE QUALITY...................................... 29 Ahmed Mehdi CHINA’S SHANGHAI INE CRUDE FUTURES: HAPPY ACCIDENT VERSUS OVERDESIGN ............................................. 33 Tom Reed FUJAIRAH’S RISE TO PROMINENCE .................................................................................................................................. -

Pipeline Authority Annual Report 2018

North Dakota Pipeline Authority Annual Report July 1, 2017 – June 30, 2018 Industrial Commission of North Dakota Governor Doug Burgum, Chairman Attorney General Wayne Stenehjem Agriculture Commissioner Doug Goehring North Dakota Pipeline Authority Annual Report July 1, 2017 – June 30, 2018 Overview At the request of the North Dakota Industrial Commission, the Sixtieth Legislature passed House Bill 1128 authorizing the North Dakota Pipeline Authority. It was signed into law on April 11, 2007. The statutory mission of the Pipeline Authority is “to diversify and expand the North Dakota economy by facilitating development of pipeline facilities to support the production, transportation, and utilization of North Dakota energy-related commodities, thereby increasing employment, stimulating economic activity, augmenting sources of tax revenue, fostering economic stability and improving the State’s economy”. As established by the Legislature, the Pipeline Authority is a builder of last resort, meaning private business would have the first opportunity to invest in and/or build additional needed pipeline infrastructure. By law, the Pipeline Authority membership is comprised of the members of the North Dakota Industrial Commission. Upon the recommendation of the Oil and Gas Research Council, the Industrial Commission authorized the expenditure of up to $325,000 during the 2017-2019 biennium for the Pipeline Authority with funding being made available from the Oil and Gas Research Fund. On August 1, 2008 the Industrial Commission named Justin J. Kringstad, an engineering consultant, to serve as Director of the North Dakota Pipeline Authority. The North Dakota Pipeline Authority Director works closely with Lynn Helms, Department of Mineral Resources Director, Ron Ness, North Dakota Petroleum Council President and Karlene Fine, Industrial Commission Executive Director. -

ABOUT PIPELINES OUR ENERGY CONNECTIONS the Facts About Pipelines

ABOUT PIPELINES OUR ENERGY CONNECTIONS THE facts ABOUT PIPELINES This fact book is designed to provide easy access to information about the transmission pipeline industry in Canada. The facts are developed using CEPA member data or sourced from third parties. For more information about pipelines visit aboutpipelines.com. An electronic version of this fact book is available at aboutpipelines.com, and printed copies can be obtained by contacting [email protected]. The Canadian Energy Pipeline Association (CEPA) CEPA’s members represents Canada’s transmission pipeline companies transport around who operate more than 115,000 kilometres of 97 per cent of pipeline in Canada. CEPA’s mission is to enhance Canada’s daily the operating excellence, business environment and natural gas and recognized responsibility of the Canadian energy transmission pipeline industry through leadership and onshore crude credible engagement between member companies, oil production. governments, the public and stakeholders. TABLE OF CONTENTS 1. Canada’s Pipeline Network .................................1 2. Pipeline Design and Standards .........................6 3. Safety and the Environment ..............................7 4. The Regulatory Landscape ...............................11 5. Fuelling Strong Economic ................................13 and Community Growth 6. The Future of Canada’s Pipelines ................13 Unless otherwise indicated, all photos used in this fact book are courtesy of CEPA member companies. CANADA’S PIPELINE % of the energy used for NETWORK transportation in Canada comes 94 from petroleum products. The Importance of • More than half the homes in Canada are Canada’s Pipelines heated by furnaces that burn natural gas. • Many pharmaceuticals, chemicals, oils, Oil and gas products are an important part lubricants and plastics incorporate of our daily lives. -

Cenovus Energy Inc. (CVE) – Quality and Growth for the Patient Investor

Portfolio Advisory Group Cenovus Energy Inc. (CVE) – Quality and Growth For The Patient Investor Cenovus was created through the split of Calgary-based Primer on the Oil Sands and energy company EnCana into two separate organizations in late 2009. As a result of this split, many Canadian Steam-Assisted-Gravity-Drainage investors found themselves holding two very different (SAGD) investments: a pure-play natural gas company (EnCana) Including the oil sands, Canada’s oil reserves are the and an integrated oil & gas company (Cenovus). This second largest in the world. Oil sands are composed document aims to provide some insight into the nature primarily of sand, clay, bitumen and water. Bitumen and long-term potential of Cenovus. is the product of oil sands production – a thick oil Cenovus owns oil sands projects that have a tremendous embedded in sand. growth profile over the next decade and are widely Recovery of bitumen is typically achieved by one of viewed as some of the highest-quality assets in the two methods: mining in open pits or drilling. Bitumen industry. However, since inception, the shares of extraction using drilling is referred to as in situ recovery, Cenovus have largely traded within a range. One reason and is generally used for reservoirs that are too deep for is that the company has made a trade-off between near- surface mining techniques to work economically. It is term and future production by drawing cash flows from estimated that approximately 80% of the total bitumen its natural gas business to fund growth in its oil sands recoverable in Alberta can only be produced with in business. -

Vitol-Brochure-2019 FINAL-1.Pdf

02 VITOL | Contents Vitol 04 VLC Renewables 14 Vitol at a glance 05 Our investments 16 Operating Globally 08 VTTI 17 Trading portfolio 10 Vitol Aviation 17 Crude oil 10 Viva Energy 18 Middle distillates 10 Vivo Energy 18 Gasoline 10 Petrol Ofisi 19 Biofuel 11 OVH Energy 19 Fuel oil 11 VARO 20 Naphtha 12 Rodoil 20 Bitumen 12 Hascol 20 Coal 13 Cockett Marine Oil 20 Liquid petroleum gas (LPG) 13 VPI Immingham 21 Liquefied natural gas (LNG) 13 VLC Renewables 21 Natural gas 13 Exploration and production 24 Power 14 Vitol Foundation 25 Renewables 14 Our worldwide capabilities 26 Shipping 14 VITOL VITOL | 03 Vitol Vitol is at the For over 50 years Vitol has served the Responsibility heart of the world’s world’s energy markets, trading over We are mindful of the risks associated seven million barrels of crude oil and with handling energy. Our assets energy flows. Every products a day and delivering energy operate to international HSE standards day we use our products to countries worldwide. and we expect the same of our partners expertise and throughout the energy chain. We seek logistical networks Our customers include national oil to conduct our business in line with to distribute energy companies, multinationals, leading the ten principles of the UN Global industrial and chemical companies and Compact and to work with partners around the world, the world’s largest airlines. We deliver who share our commitment to high efficiently and the products they need on time and to standards of operation. responsibly. specification by sourcing and managing the movement of energy through the relevant infrastructures. -

Global Energy 2012 Conference & Exhibition

GLOBAL 12 ENERGY 20 29/30/31 OCTOBER 2012 HOTEL PRESIDENT WILSON Global Energy Geneva 2012 Where the oil & gas trade meets...with key participation of Cargill, Gunvor, Lundin, Lukoil, Mercuria, Socar, Trafigura To register: www.globalenergygeneva.com GLOBAL 12 ENERGY 20 GLOBAL ENERGY 2012 CONFERENCE & EXHIBITION 29/30/31 October 2012, Hotel President Wilson, Geneva T: +41 (0) 22 321 74 80 | F: +41 (0) 22 321 74 82 | E: [email protected] | www.globalenergygeneva.com About Global Energy 2012 The oil and gas trade is critical to the global economy and the effect of energy prices and trade is more profound than for any other traded commodity. Global Energy is a trade show, conference and exhibition unique to Geneva. Global Energy 2012 is being held on October 29/30/31 at the prestigious Hotel President Wilson in the heart of Geneva. The event brings together energy traders, banks, policymakers, delivering important keynote speeches and panel debates. Global Energy 2012 takes place during an important week in the Geneva commodities trade calendar. It will be attended by a “who’s who” in oil and gas in Switzerland and abroad. Who will attend Global Energy 2012? Major international oil & gas trading firms Traders from small and medium-sized firms throughout the globe Leaders in the Swiss energy trade community Upstream oil and gas majors – interested in the global S&D of oil and gas Oil and gas investors, including family offices and private banks Trade financiers specialising in oil and gas Professional firms: lawyers, advisory/management -

Climate and Energy Benchmark in Oil and Gas Insights Report

Climate and Energy Benchmark in Oil and Gas Insights Report Partners XxxxContents Introduction 3 Five key findings 5 Key finding 1: Staying within 1.5°C means companies must 6 keep oil and gas in the ground Key finding 2: Smoke and mirrors: companies are deflecting 8 attention from their inaction and ineffective climate strategies Key finding 3: Greatest contributors to climate change show 11 limited recognition of emissions responsibility through targets and planning Key finding 4: Empty promises: companies’ capital 12 expenditure in low-carbon technologies not nearly enough Key finding 5:National oil companies: big emissions, 16 little transparency, virtually no accountability Ranking 19 Module Summaries 25 Module 1: Targets 25 Module 2: Material Investment 28 Module 3: Intangible Investment 31 Module 4: Sold Products 32 Module 5: Management 34 Module 6: Supplier Engagement 37 Module 7: Client Engagement 39 Module 8: Policy Engagement 41 Module 9: Business Model 43 CLIMATE AND ENERGY BENCHMARK IN OIL AND GAS - INSIGHTS REPORT 2 Introduction Our world needs a major decarbonisation and energy transformation to WBA’s Climate and Energy Benchmark measures and ranks the world’s prevent the climate crisis we’re facing and meet the Paris Agreement goal 100 most influential oil and gas companies on their low-carbon transition. of limiting global warming to 1.5°C. Without urgent climate action, we will The Oil and Gas Benchmark is the first comprehensive assessment experience more extreme weather events, rising sea levels and immense of companies in the oil and gas sector using the International Energy negative impacts on ecosystems. -

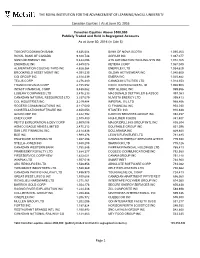

THE ROYAL INSTITUTION for the ADVANCEMENT of LEARNING/Mcgill UNIVERSITY

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Canadian Equities │ As at June 30, 2016 Canadian Equities Above $500,000 Publicly Traded and Held in Segregated Accounts As at June 30, 2016 (in Cdn $) TORONTO DOMINION BANK 9,836,604 BANK OF NOVA SCOTIA 1,095,263 ROYAL BANK OF CANADA 9,328,748 AGRIUM INC 1,087,077 SUNCOR ENERGY INC 5,444,096 ATS AUTOMATION TOOLING SYS INC 1,072,165 ENBRIDGE INC 4,849,078 KEYERA CORP 1,067,040 ALIMENTATION COUCHE-TARD INC 4,628,364 ENERFLEX LTD 1,054,629 BROOKFIELD ASSET MGMT INC 4,391,535 GILDAN ACTIVEWEAR INC 1,040,600 CGI GROUP INC 4,310,339 EMERA INC 1,025,882 TELUS CORP 4,276,480 CANADIAN UTILITIES LTD 1,014,353 FRANCO-NEVADA CORP 4,155,552 EXCO TECHNOLOGIES LTD 1,008,903 INTACT FINANCIAL CORP 3,488,562 WSP GLOBAL INC 999,856 LOBLAW COMPANIES LTD 3,476,233 MACDONALD DETTWILER & ASSOC 997,083 CANADIAN NATURAL RESOURCES LTD 3,337,079 NUVISTA ENERGY LTD 995,413 CCL INDUSTRIES INC 3,219,484 IMPERIAL OIL LTD 968,856 ROGERS COMMUNICATIONS INC 3,117,080 CI FINANCIAL INC 954,030 CONSTELLATION SOFTWARE INC 2,650,053 STANTEC INC 910,638 GOLDCORP INC 2,622,792 CANYON SERVICES GROUP INC 892,457 ONEX CORP 2,575,400 HIGH LINER FOODS 841,407 PEYTO EXPLORATION & DEV CORP 2,509,098 MAJOR DRILLING GROUP INTL INC 838,304 AGNICO EAGLE MINES LIMITED 2,475,212 EQUITABLE GROUP INC 831,396 SUN LIFE FINANCIAL INC 2,414,836 DOLLARAMA INC 829,840 BCE INC 1,999,278 LEON'S FURNITURE LTD 781,495 ENGHOUSE SYSTEMS LTD 1,867,298 CANADIAN ENERGY SERVICES &TECH 779,690 STELLA-JONES INC 1,840,208 SHAWCOR LTD 775,126 -

Cenovus Completes Acquisition of Assets in Western Canada from Conocophillips

Cenovus completes acquisition of assets in Western Canada from ConocoPhillips Calgary, Alberta (May 17, 2017) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) has closed its previously announced purchase of assets in Western Canada from ConocoPhillips after receiving all necessary regulatory approvals for the transaction. The acquired assets include ConocoPhillips’ 50% interest in the FCCL Partnership, the oil sands venture which was jointly owned with and operated by Cenovus, as well as the majority of ConocoPhillips’ Deep Basin conventional assets in Alberta and British Columbia. “With the completion of this transformational deal, we now have full control of our best-in- class oil sands projects and an exciting new growth platform in the Deep Basin that provides us with significant short-cycle development opportunities to complement our long-term oil sands growth portfolio,” said Brian Ferguson, Cenovus President & Chief Executive Officer. “As a result of this transaction, we’ve now doubled our production and reserves base.” In the coming months, Cenovus will remain firmly focused on: • Continuing to safely and reliably operate all of its assets • Efficiently integrating the Deep Basin assets and staff into the company • Deleveraging its balance sheet, including using the proceeds of planned divestitures, such as the sale of the company’s Pelican Lake and Suffield assets, which are currently being marketed. Cenovus intends to provide an update on its investment plans for its consolidated oil sands business and newly acquired Deep Basin -

Integrating Into Our Strategy

INTEGRATING CLIMATE INTO OUR STRATEGY • 03 MAY 2017 Integrating Climate Into Our Strategy INTEGRATING CLIMATE INTO OUR STRATEGY • 03 CONTENTS Foreword by Patrick Pouyanné, Chairman and Chief Executive Officer, Total 05 Three Questions for Patricia Barbizet, Lead Independent Director of Total 09 _____________ SHAPING TOMORROW’S ENERGY Interview with Fatih Birol, Executive Director of the International Energy Agency 11 The 2°C Objective: Challenges Ahead for Every Form of Energy 12 Carbon Pricing, the Key to Achieving the 2°C Scenario 14 Interview with Erik Solheim, Executive Director of UN Environment 15 Oil and Gas Companies Join Forces 16 Interview with Bill Gates, Breakthrough Energy Ventures 18 _____________ TAKING ACTION TODAY Integrating Climate into Our Strategy 20 An Ambition Consistent with the 2°C Scenario 22 Greenhouse Gas Emissions Down 23% Since 2010 23 Natural Gas, the Key Energy Resource for Fast Climate Action 24 Switching to Natural Gas from Coal for Power Generation 26 Investigating and Strictly Limiting Methane Emissions 27 Providing Affordable Natural Gas 28 CCUS, Critical to Carbon Neutrality 29 A Resilient Portfolio 30 Low-Carbon Businesses to Become the Responsible Energy Major 32 Acquisitions That Exemplify Our Low-Carbon Strategy 33 Accelerating the Solar Energy Transition 34 Affordable, Reliable and Clean Energy 35 Saft, Offering Industrial Solutions to the Climate Change Challenge 36 The La Mède Biorefinery, a Responsible Transformation 37 Energy Efficiency: Optimizing Energy Consumption 38 _____________ FOCUS ON TRANSPORTATION Offering a Balanced Response to New Challenges 40 Our Initiatives 42 ______________ OUR FIGURES 45 04 • INTEGRATING CLIMATE INTO OUR STRATEGY Total at a Glance More than 98,109 4 million employees customers served in our at January 31, 2017 service stations each day after the sale of Atotech A Global Energy Leader No. -

Recent Crude Oil Price Dynamics, PETRONAS and Malaysia

Recent crude oil price dynamics, PETRONAS and Malaysia Lim Kim-Hwa [email protected] Tim Niklas Schoepp [email protected] 23 January 2015 Executive Summary Since PETRONAS contributed RM73.4 billion (30% of the Malaysian government’s expenditure) in 2013, the recent crude oil price fall has profound implications. The commodity effect will mean lower revenue and profits. However, this effect is cushioned by the depreciating USDMYR. This report aims to evaluate the likely price range of crude oil in 2015 and shows the possible impact on PETRONAS under different circumstances. With contained geo-political risks, global crude oil oversupply, slower global economic growth and cost factors that favour continuous production rather than cuts, crude oil is likely to trade between USD40 – 70 per barrel. Using the Annual Reports of PETRONAS, we estimated that: • If USDMYR depreciates slightly to 3.75 and crude oil trades at USD55 per barrel in 2015, PETRONAS’ profitability (as measured EBITDA) might fall to RM72 billion; and dividends might fall to RM19 billion (vs. RM123 billion and RM27 billion respectively in 2013); • In a rosy case (where crude oil trades at USD70 per barrel and USDMYR trades at 4), PETRONAS’ EBITDA would fall to RM98 billion but RM26 billion dividends payment might be possible; • In a bad case (where crude oil trades at USD40 per barrel and USDMYR trades at 3.5), PETRONAS’ EBITDA would fall to RM49 billion and dividends might fall by half to RM13 billion. • Some PETRONAS assets might be impaired, in particular those that were purchased when crude oil price was trading at over USD100 per barrel.