The Black Country and Telford

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Inspection Report Saint Stephen's

INSPECTION REPORT SAINT STEPHEN'S CHURCH OF ENGLAND PRIMARY SCHOOL Heath Town, Wolverhampton LEA area: Wolverhampton Unique reference number: 104361 Headteacher: Mr. W Downing Lead inspector: Mrs. V Davies Dates of inspection: 7th - 9th February 2005 Inspection number: 267944 Inspection carried out under section 10 of the School Inspections Act 1996 © Crown copyright 2005 This report may be reproduced in whole or in part for non-commercial educational purposes, provided that all extracts quoted are reproduced verbatim without adaptation and on condition that the source and date thereof are stated. Further copies of this report are obtainable from the school. Under the School Inspections Act 1996, the school must provide a copy of this report and/or its summary free of charge to certain categories of people. A charge not exceeding the full cost of reproduction may be made for any other copies supplied. St Stephen’s CE Primary School - 2 INFORMATION ABOUT THE SCHOOL Type of school: Primary School category: Voluntary controlled Age range of pupils: 3-11 Gender of pupils: Boys and girls Number on roll: 191.5 School address: Woden Road Heath Town Wolverhampton West Midlands Postcode: WV10 0BB Telephone number: 01902 558840 Fax number: 01902 558843 Appropriate authority: Governing body Name of chair of Mr. R.J. Allen governors: Date of previous March 2003 inspection: CHARACTERISTICS OF THE SCHOOL This is an average size Church of England aided primary school for 191 boys and girls between the ages of 3 and 11, including 43 pupils who attend daily half day sessions in the nursery. The school is situated in Heath Town and is close to the centre of Wolverhampton. -

9 Bus Time Schedule & Line Route

9 bus time schedule & line map 9 Walsall - Wolverhampton via Bloxwich, Wednesƒeld View In Website Mode The 9 bus line (Walsall - Wolverhampton via Bloxwich, Wednesƒeld) has 4 routes. For regular weekdays, their operation hours are: (1) Bloxwich: 7:41 PM - 11:11 PM (2) Bloxwich: 11:10 PM (3) Walsall: 5:43 AM - 10:11 PM (4) Wolverhampton: 5:38 AM - 10:10 PM Use the Moovit App to ƒnd the closest 9 bus station near you and ƒnd out when is the next 9 bus arriving. Direction: Bloxwich 9 bus Time Schedule 30 stops Bloxwich Route Timetable: VIEW LINE SCHEDULE Sunday 11:11 PM Monday 7:41 PM - 11:11 PM Wolverhampton Bus Station Tuesday 7:41 PM - 11:11 PM Culwell St, Wolverhampton Wednesƒeld Road, Birmingham/Wolverhampton/Walsall/Dudley Wednesday 7:41 PM - 11:11 PM Burton Rd, Wolverhampton Thursday 7:41 PM - 11:11 PM Friday 7:41 PM - 11:11 PM Inkerman St, Heath Town Saturday 7:41 PM - 11:11 PM Woden Rd, Heath Town Grove St, Heath Town Deans Rd, Heath Town 9 bus Info Wolverhampton Road, Birmingham/Wolverhampton/Walsall/DudleyDirection: Bloxwich Stops: 30 Coronation Rd, Heath Town Trip Duration: 27 min Line Summary: Wolverhampton Bus Station, Culwell Bentley Bridge Retail Park, Wednesƒeld St, Wolverhampton, Burton Rd, Wolverhampton, Inkerman St, Heath Town, Woden Rd, Heath Town, Bentley Bridge Way, Birmingham/Wolverhampton/Walsall/Dudley Grove St, Heath Town, Deans Rd, Heath Town, Rookery St, Wednesƒeld Coronation Rd, Heath Town, Bentley Bridge Retail Park, Wednesƒeld, Rookery St, Wednesƒeld, Church Well Lane, Birmingham/Wolverhampton/Walsall/Dudley -

West Midlands European Regional Development Fund Operational Programme

Regional Competitiveness and Employment Objective 2007 – 2013 West Midlands European Regional Development Fund Operational Programme Version 3 July 2012 CONTENTS 1 EXECUTIVE SUMMARY 1 – 5 2a SOCIO-ECONOMIC ANALYSIS - ORIGINAL 2.1 Summary of Eligible Area - Strengths and Challenges 6 – 14 2.2 Employment 15 – 19 2.3 Competition 20 – 27 2.4 Enterprise 28 – 32 2.5 Innovation 33 – 37 2.6 Investment 38 – 42 2.7 Skills 43 – 47 2.8 Environment and Attractiveness 48 – 50 2.9 Rural 51 – 54 2.10 Urban 55 – 58 2.11 Lessons Learnt 59 – 64 2.12 SWOT Analysis 65 – 70 2b SOCIO-ECONOMIC ANALYSIS – UPDATED 2010 2.1 Summary of Eligible Area - Strengths and Challenges 71 – 83 2.2 Employment 83 – 87 2.3 Competition 88 – 95 2.4 Enterprise 96 – 100 2.5 Innovation 101 – 105 2.6 Investment 106 – 111 2.7 Skills 112 – 119 2.8 Environment and Attractiveness 120 – 122 2.9 Rural 123 – 126 2.10 Urban 127 – 130 2.11 Lessons Learnt 131 – 136 2.12 SWOT Analysis 137 - 142 3 STRATEGY 3.1 Challenges 143 - 145 3.2 Policy Context 145 - 149 3.3 Priorities for Action 150 - 164 3.4 Process for Chosen Strategy 165 3.5 Alignment with the Main Strategies of the West 165 - 166 Midlands 3.6 Development of the West Midlands Economic 166 Strategy 3.7 Strategic Environmental Assessment 166 - 167 3.8 Lisbon Earmarking 167 3.9 Lisbon Agenda and the Lisbon National Reform 167 Programme 3.10 Partnership Involvement 167 3.11 Additionality 167 - 168 4 PRIORITY AXES Priority 1 – Promoting Innovation and Research and Development 4.1 Rationale and Objective 169 - 170 4.2 Description of Activities -

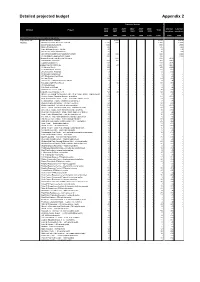

Detailed Projected Budget Appendix 2

Detailed projected budget Appendix 2 Projected budget 2019- 2020- 2021- 2022- 2023- 2024- Internal External Division Project Total 2020 2021 2022 2023 2024 2025 resources resources £000 £000 £000 £000 £000 £000 £000 £000 £000 General Revenue Account capital programme City Assets and Disabled Facilities Grants - 2,215 - - - - 2,215 - (2,215) Housing Mandatory Disabled Facilities Grants 1,500 800 - - - - 2,300 - (2,300) Small Adaptations Grants 800 - - - - - 800 - (800) Stair Lift Maintenance 25 - - - - - 25 - (25) Care & Repair Fees re: DFG's 70 - - - - - 70 - (70) Social Care Minor Adaptations 30 - - - - - 30 - (30) Discretionary Bathrooms Adaptations Grant 50 450 - - - - 500 - (500) Rehabilitation Equipment 2019-2020 165 - - - - - 165 - (165) Housing General Fund General Schemes - 215 - - - - 215 (215) - Small Works Assistance 160 182 - - - - 342 (342) - Capitalised Salaries 118 - - - - - 118 (118) - Empty Properties Strategy 69 178 - - - - 247 (247) - 19 Chester Street 100 - - - - - 100 (100) - 14 Selwyn Road, Bilston 60 - - - - - 60 (60) - 29 Lime Street, Penfields 13 - - - - - 13 (13) - 99 Milfields Road Bilston 5 - - - - - 5 (5) - 473 Birmingham New Road 3 - - - - - 3 (3) - 14 Lane Road 69 - - - - - 69 (69) - Land between 44 and 48 Showell Road 4 - - - - - 4 (4) - Two and a half Clifford Street - 80 - - - - 80 (80) - 30 Victoria Road 2 - - - - - 2 (2) - 182 Castlecroft Road 4 - - - - - 4 (4) - All Saints Development Fees 35 - - - - - 35 (35) - Corporate Asset Management 62 20 - - - - 82 (82) - Graiseley Learning Technology Centre -

Directory of Mental Health Services in Wolverhampton

Directory of Mental Health Services In Wolverhampton 2019 - 2024 Contents Title Page Introduction 1 Emergency Contacts 2 Services for 18 years and over Section 1: Self-referral, referral, and support groups 4 Section 2: Community support services, self-referral and professional 14 referrals Section 3: Services that can be accessed through the Referral and 22 Assessment Service (RAS) Section 4: Services for carers 27 Section 5: Specialist housing services 29 Section 6: Contacts and useful websites 33 Services for 65 years and over Section 1: Community support services – self-referral and 37 professional referrals Section 2: Referral from a General Practitioner (GP) and other 40 agencies Section 3: Contact and useful websites 44 Services for Children and Young People Emergency Contacts 45 Section 1: Referral, self-referral / support groups 47 Section 2: Community support services, self - referral referrals and 50 professional referrals Section 3: Social Care /Local Authority Services 52 Section 4: Services that need a referral from a General Practitioner 54 (GP) and Professional Section 5: Useful websites and contacts 58 0 Introduction Good mental health plays a vital impact upon our quality of life and has an effect upon our ability to attain and maintain good physical health and develop positive relationships with family and friends. Positive mental health also plays a part in our ability to achieve success educationally and achieve other life goals and ambitions including those related to work, hobbies, our home life and sporting and leisure activities. As many as 1 in 4 adults and 1 in 10 children experience mental ill health during their life time. -

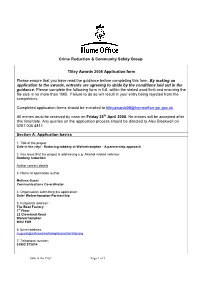

Crime Reduction & Community Safety Group Tilley Awards 2008 Application Form Please Ensure That You Have Read the Guidance B

Crime Reduction & Community Safety Group Tilley Awards 2008 Application form Please ensure that you have read the guidance before completing this form. By making an application to the awards, entrants are agreeing to abide by the conditions laid out in the guidance. Please complete the following form in full, within the stated word limit and ensuring the file size is no more than 1MB. Failure to do so will result in your entry being rejected from the competition. Completed application forms should be e-mailed to [email protected]. All entries must be received by noon on Friday 25th April 2008. No entries will be accepted after this time/date. Any queries on the application process should be directed to Alex Blackwell on 0207 035 4811. Section A: Application basics 1. Title of the project: Safe in the city! - Reducing robbery in Wolverhampton - A partnership approach 2. Key issue that the project is addressing e.g. Alcohol related violence: Robbery reduction Author contact details 3. Name of application author: Melissa Guest Communications Co-ordinator 4. Organisation submitting the application: Safer Wolverhampton Partnership 5. Full postal address: The Boot Factory 1st Floor 22 Cleveland Road Wolverhampton WV2 1BH 6. Email address: [email protected] 7. Telephone number: 01902 572014 Safe in the City! Page 1 of 3 Secondary project contact details 8. Name of secondary contact involved in the project: Billy Corrigan Communications & Reassurance Officer West Midlands Police Chloe Shrubb Communications & Reassurance Officer West Midlands Police 9. Secondary contact email address: [email protected] [email protected] 10. -

STAFFORDSHIRE. (KELLY's & Miss Ina L

- 560 WOLVERHAMPTON. STAFFORDSHIRE. (KELLY's & Miss Ina L. McNeill M.B., Ch.B.Glas. anresthe CbiPf Assistant Clerk, Albert G. Aldridge tists; J. A. Deeley esq. sec.; Miss Elsie Barnett, dis Assistant Clerk for Settlement Work, Horace J. A_ penser; Miss J essie Henderson, matron Starkey, Stafford street, Wolverhampton Wolverhampton & Midland Counties Eye Infirmary, Treasurer, Jesse Millington, United Counties Bank, Wol Compton road, Henry Malet B.A., M.D., B.Ch.Dub. verhampton hon. consulting physician; Arthur Edwin Chesshire Relieving Officers & Collectors to the Guardians Supt. ~LR.C.S.Eng. & Arthur Bernard Cridland Dipl.Ophthl. A. E. Jackson, Stafford street; No. I district, J. G. Oxon., F.R.C.S.Edin., L.R.O.P.Lond. hon. surgeons; Tunley, Stafford street, Wolverhampton; No. 2 dis Henry Carter Mactier B.A., M.B., B.Ch.Dub. hon. trict, George Thompson, 139 Park st. south, Blaken assistant surgeon; Guy Fleet-wood Haycraft M.R.C.S. hall, Wolverhampton; No. 3 district, Edmund Dunton Eng., L.R.C.P.Lond. house surgeon; Major W. Blake Marston, 1g6 Staveley road, Wolverhampton; No. 4 Burke V.D. sec. ; Capt. Eustace Lees, assistant sec. ; district, William Sturmey Wolverson, Regent street. ~iiss M. Connell, matron Bilston; No. 5 district, John N eal, Harper street, Th~ Wolverhampton Society for the Out-Door Blind, 17 Manor, Willenhall; No. 6 district, Ernest J. Block Victoria street, Cecil Tildesley, hon. sec. ; William sidge, Tudor road, Heath To-wn; No. 7 district, Jame~ Johnson, hon. treasurer Stevenson, 3 r St. Mark's road, Wolverhampton Vaccination Offi.cers-W. Rowe, Waterloo road, Wolver TERRITORIAL FORCE. -

The Case for a New Hertfordshire Village WELWYN HATFIELD BOROUGH COUNCIL LOCAL PLAN CONSULTATION 23 JANUARY- 19 MARCH 2015 CONTENTS

The Case for a new Hertfordshire Village WELWYN HATFIELD BOROUGH COUNCIL LOCAL PLAN CONSULTATION 23 JANUARY- 19 MARCH 2015 CONTENTS INTRODUCTION: THE ENGLISH VILLAGE 4 SECTION 1: THE HISTORY AND EVOLUTION OF THE ENGLISH VILLAGE 6 SECTION 2: THE IDEALISATION OF THE ENGLISH VILLAGE 13 SECTION 3: PLANNING POLICY AND THE ENGLISH VILLAGE 17 APPENDIX 1: HERTFORDSHIRE VILLAGES TODAY 28 APPENDIX 2: ENGLISH MODEL VILLAGES 35 APPENDIX 3: SCOTTISH MODEL VILLAGE 54 INTRODUCTION Although close to London, Hertfordshire still enjoys significant and types of village and how they have provided a variety of Hertfordshire has a rich tradition of creative town and country they have developed. A village will typically fall into one of the areas of predominantly rural landscape character. The landscape different responses to these fundamental aims and objectives. planning including two of the most important garden cities. following three categories: the organic village characterised of Hertfordshire is naturally friendly, green and gently rolling. Hertfordshire also can also draw upon its experiences of the by incremental growth; the estate village laid out by private These rural areas are not just characterised by the natural The 21st Century has brought new pressures on housing New Towns – Stevenage, Hatfield and Hemel Hempstead are landowners and; the industrial village planned and executed landscape but also a whole series of villages. In many cases numbers, a fresh debate about green belt and how best to now all mature settlements. In all cases there were lessons to for a new elite, the wealthy entrepreneur. Current planning these are typical of archetypal English villages. -

FREE EMERGENCY CONTRACEPTION the Following Pharmacies Provide Free Emergency Contraception and Free Chlamydia / Gonorrhoea Tests

FREE EMERGENCY CONTRACEPTION The following pharmacies provide free emergency contraception and free chlamydia / gonorrhoea tests. PLEASE CALL THE PHARMACY BEFORE VISITING, TO CHECK THAT THE FREE SERVICE IS AVAILABLE City Centre Superdrug Pharmacy (Mander Centre) Central Arcade, Unit 12, Mander Centre, Wolverhampton WV1 3NN 01902 313654 Jhoots Pharmacy (Thornley Street) 34-35 Thornley Street, Wolverhampton WV1 1JP 01902 424380 Boots UK Ltd (Dudley Street) 40-41 Dudley Street, Wolverhampton WV1 3ER 01902 427145 Asda Pharmacy (Waterloo Rd) Only available on Weds, Thurs, Sunday Asda Supermarket, Molineux Way, Wolverhampton WV1 4DE 01902 778106 Tettenhall, Whitmore Reans Millstream Pharmacy (Tettenhall Road) Halfway House, 151 Tettenhall Road, Wolverhampton, WV3 9NJ 01902 423743 Upper Green Pharmacy (Tettenhall) 5 Upper Green, Tettenhall, Wolverhampton WV6 8QQ 01902 751353 Lloyds Pharmacy (Tettenhall) Lower Street Health Centre, Tettenhall, Wolverhampton WV6 9LL 01902 444565 Tettenhall Wood Pharmacy (Tettenhall Wood) 12 School Road, Tettenhall Wood, Wolverhampton WV6 8EJ 01902 747647 Whitmore Reans Pharmacy 6 Bargate Drive, Avion Centre, Whitmore Reans, Wolverhampton WV6 0QW 01902 420600 Staveley Chemist (Whitmore Reans) 212 Staveley Road, Whitmore Reans, Wolverhampton WV1 4RS 01902 421789 Penn, Pennfields, Merry Hill, Compton, Bradmore, Warstones, Castlecroft Pennfields Pharmacy (Pennfields) 248 Jeffcock Road, Penn Fields, Wolverhampton WV3 7AH 01902 341300 Boots Pharmacy Waitrose (Pennfields) PENDING. PLEASE CHECK Waitrose Store, Penn Road, -

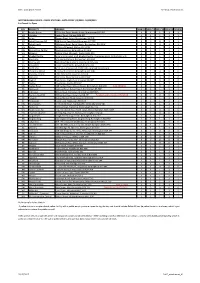

POLICE STATIONS - DATA from 1/4/2010 - 31/03/2015 0 = Closed 1 = Open

WEST MIDLANDS POLICE Freedom of Information WEST MIDLANDS POLICE - POLICE STATIONS - DATA FROM 1/4/2010 - 31/03/2015 0 = Closed 1 = Open LPU PROPERTY ADDRESS 2010/11 2011/12 2012/13 2013/14 2014/15 BE Acocks Green 27 Yardley Road, Acocks Green, Birmingham B27 6LZ 1 1 1 1 1 WS Aldridge Anchor Road, Aldridge WS9 8PT 1 1 1 1 1 BW Aston Queens Road, Aston, Birmingham B6 7ND 1 1 1 1 1 SH Balsall Common BO 208 Station Road, Balsall Common CV7 7EE 0 0 0 1 1 BE Balsall Heath 48 Edward Road, Balsall Heath, Birmingham B12 9EW 0 0 0 1 1 WV Bilston 15 Mount Pleasant, Bilston WV14 7LJ 1 1 1 1 1 BW Birmingham Central Steelhouse Lane, Birmingham B4 6NW 1 1 1 1 1 WS Bloxwich Station Street, Bloxwich, Walsall WS3 2PD 1 1 1 1 1 SH Bluebell Centre Ground Floor West Mall, Bluebell Centre, Chelmsley Wood, Solihull B37 5TN 0 0 1 1 1 BS Bournville 341 Bournville Lane, Birmingham B30 1QX 1 1 1 1 1 DY Brierley Hill High Street/Bank Street, Brierley Hill DY5 3AU 1 1 1 1 1 WS Brownhills Chester Road North, Brownhills WS8 7JW 1 1 0 0 0 BN Castle Vale Reed Sq, Turnhouse Rd, Castle Vale, Birmingham B35 6PR 1 1 1 1 1 SH Chelmsley Wood Ceolmund Crescent, Birmingham B37 5UB 1 1 0 0 0 CV Coventry Central Little Park Street, Coventry CV1 2JX 1 1 1 1 1 WS Darlaston 1 Crescent Road, Darlaston WS10 8AE 0 0 0 0 0 BW Digbeth High Street, Digbeth, Birmingham B5 6DT 1 1 0 0 0 DY Dudley New Street, Dudley DY1 1LP 1 1 1 1 1 BW Dudley Road 238 Dudley Road, Winson Green, Birmingham B18 4NY Sold 28/10/11 0 0 0 0 0 BS Edgbaston Belgrave Road, Balsall Heath, Birmingham B5 7BP 1 1 1 1 -

Celebrating Our Cultures: Guidelines for Mental Health Promotion with Black and Minority Communities

Celebrating our Cultures: Guidelines for Mental Health Promotion with Black and Minority Communities Celebrating our Cultures: Guidelines for Mental Health Promotion with Black and Minority Communities December 2004 Policy Estates HR/Workforce Performance Management IM & T Planning Finance Clinical Partnership Working Document Purpose Procedure – change ROCR Ref: Gateway Reference: 2560 Title Celebrating our Cultures: Guidelines for Mental Health Promotion with Black and Minority Ethnic Communities Author National Institute for Mental Health in England Publication Date December 2004 Target Audience GPs, Black and minority ethnic voluntary sector workers, community development workers, public health and health promotion specialists, primary care workers, mental health workers, local authority workers, community and self help groups, community leaders, prison staff, faith communities Circulation List PCT CEs, NHS Trusts CEs, SHA CEs. Care Trusts CEs, Directors of PH, Ds of Social Services, Voluntary Organisations, NIMHE Racial Equality Leads Description This resource makes the case for mental promotion with black and minority ethnic communities in England. It sets out a framework for delivering local interventions and addressing the needs of black and minority ethnic communities within mental health promotion strategies being implemented in response to Standard 1 of the National Service Framework for Mental Health Cross Ref Making It Happen: A guide to delivering mental health promotion. Inside Outside: Improving Mental Health Services for Black and Minority Ethnic Communities in England Superseded Docs Action Required For information Timing None Contact Details John Scott National Institute for Mental Health in England Room 8E40 Quarry House Quarry Hill Leeds LS2 7UE 0113 254 6892 [email protected] For Recipient’s Use Celebrating our Cultures: Guidelines for Mental Health Promotion with Black and Minority Ethnic Communities Foreword Britain is recognised as a multiethnic and multicultural society. -

WMCA Wellbeing Board

WMCA Wellbeing Board Date 24 January 2020 Report title West Midlands on the Move Portfolio Lead Cllr Izzi Seccombe – Wellbeing Accountable Chief Deborah Cadman OBE, West Midlands Executive Combined Authority email: [email protected] Tel: (0121) 214 7800 Accountable Simon Hall Physical Activity Policy & Delivery Employee Lead Email: [email protected] Tel: 0121 214 7093 Report has been Sean Russell, Wellbeing Director, WMCA considered by Recommendation(s) for action or decision: The WMCA Wellbeing Board is recommended to: 1. To note the progress in the delivery of current priorities. 2. To approve the strategy refresh by Summer 2020. 1. Purpose 1.1 This paper outlines the progress and next steps in the delivery of the WMCA’s West Midlands on the Move Strategic Framework and seeks the Wellbeing’s support for this work. 2. Background 2.1 In delivering its strategic framework, the WMCA’s focus has been on convening the collaborative space for physical activity and working with stakeholders to influence and address some of the barriers preventing people being active. 1 3. Progress Headlines Collaborative Engagement and Evaluating Impact. 3.1. On 9 January 2020, 25 physical activity stakeholders launched the West Midlands physical activity sector collaborative engagement programme, a yearlong programme to strengthen how we work together to make the West Midlands the best it can be in getting more people active. 3.2. This programme is being led by the University of Birmingham’s Institute of Leadership and the Leadership Centre working with Local Authorities, Active Partnerships and regional and national organisations such as Transport for the West Midlands and the Public Health England, will develop shared principles and values, explore shared accountability, priorities as well as applying learning from different practice.