Tualatin Valley Fire and Rescue, a Rural Fire Protection District

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BUSINESS and LIFESTYLE PUBLISHED by the Bendchamber

FREE 2016 BENDBUSINESS AND LIFESTYLE PUBLISHED BY THE BENDChamber TECH BIOSCIENCE BREWING DISTILLING FOOD Brian Fratzke CHAIRMAN OF THE BEND CHAMBER OF COMMERCE Owner of Fratzke Commercial Real Estate Advisors MAKE Works on Saturdays in his sweatpants, a t-shirt and fl ip fl ops. LEARN MORE ABOUT BRIAN - PAGE 52 the move Relocation resources - page 65 LOOK IN THE RED PAGES FOR BEND’S PREFERRED BUSINESSES - PAGE 76 OUR GRATITUDE GOES OUT TO ALL WHO HAVE SUPPORTED THIS ENDEAVOR, ESPECIALLY THE BEND CHAMBER MEMBERS WHO MAKE IT ALL POSSIBLE. PRODUCTION TEAM PHOTO BY: CHRISTIAN HEEB CASCADE CENTER OF PHOTOGRAPHY DESIGN & LAYOUT STEPHANIE SHAVER [email protected] resource (541) 382-3221 Guides Bend Chamber Staff ..........................4 EDITOR Bend Chamber Board of Directors ...5 RACHAEL REES VAN DEN BERG Community Resources ......................6 [email protected] (541) 382-3221 Business Resources ...........................8 Transportation...................................16 ADVERTISING Relocation .......................................64 PATTY DAVIS Preferred Business Listings [email protected] Red pages.. ......................................76 (541) 382-3221 PUbLIcaTIon credITS : MEMBERSHIP PUbLISher: bend chamber, PrInTIng bY: The bULLeTIn coVer PhoTo bY: The hIdden ToUch PhoTograPhY coVer deSIgn bY STePhanIe ShaVer ©2015 bend chamber. SHELLEY JUNKER no PorTIon of ThIS PUbLIcaTIon maY be reProdUced In anY form WIThoUT WrITTen conSenT from The bend chamber. The InformaTIon In ThIS dIrecTorY IS gaThered In [email protected] SUch a WaY aS To enSUre maXImUm accUracY. (541) 382-3221 COVER PHOTO BY THE HIDDEN TOUCH PHOTOGRPAHY 2 | bend chamber of commerce inside LifestyleArticles Business Articles History of the chamber ................... 18 Don’t lose your marbles ................................... 9 Once upon a time in Bend .............. 20 Entrepreneurial ecosystem ............................ -

Apple Inc. K-12 and Higher Education Institution Third-Party Products

Apple Inc. K-12 and Higher Education Institution Third-Party Products: Software Licensing and Hardware Price List June 15, 2010 Table Of Contents Page • How to Order 1 • Revisions to the Price List 1-7 SECTION A: THIRD-PARTY HARDWARE 7-35 • Cables 7-8 • Cameras 8 • Carts, Security & More 8-9 • Displays and Accessories 9 • Input Devices 9-10 • iPad Accessories 10 ˆ • iPod/iPhone Accessories 10-12 • iPod/iPhone Cases 12-17 • Music Creation 17 • Networking 18 • Portable Gear 18-22 • Printers 22 • Printer Supplies 22-28 28-29 • Projectors & Presentation 28-29 • Scanners 29 • Server Accessories 29-30 • Speakers & Audio 30-33 • Storage 33-34 • Storage Media 34 • Video Accessories 34 34-35 • Video Cameras 34-35 • Video Devices 35 SECTION B: THIRD-PARTY SOFTWARE LICENSING 35-39 • Creativity & Productivity Tools 35-39 • IT Infrastructure & Learning Services 39 SECTION C: FOR MORE INFORMATION 39 • Apple Store for Education 39 • Third-Party Websites 39 • Third-Party Sales Policies 40 • Third-Party Products and Ship-Complete Orders 40 HOW TO ORDER Many of the products on this price list are available to order online from the Apple Store for Education: www.apple.com/education/store or 800-800-2775 Purchase orders for all products may be submitted to: Apple Inc. Attn: Apple Education Sales Support 12545 Riata Vista Circle Mail Stop: 198-3ED Austin, TX 78727-6524 Phone: 1-800-800-2775 Fax: (800) 590-0063 IMPORTANT INFORMATION REGARDING ORDERING THIRD PARTY SOFTWARE LICENSING Contact Information: End-user (or, tech coordinator) contact information is required in order to fulfill orders for third party software licensing. -

Insight MFR By

Manufacturers, Publishers and Suppliers by Product Category 11/6/2017 10/100 Hubs & Switches ASCEND COMMUNICATIONS CIS SECURE COMPUTING INC DIGIUM GEAR HEAD 1 TRIPPLITE ASUS Cisco Press D‐LINK SYSTEMS GEFEN 1VISION SOFTWARE ATEN TECHNOLOGY CISCO SYSTEMS DUALCOMM TECHNOLOGY, INC. GEIST 3COM ATLAS SOUND CLEAR CUBE DYCONN GEOVISION INC. 4XEM CORP. ATLONA CLEARSOUNDS DYNEX PRODUCTS GIGAFAST 8E6 TECHNOLOGIES ATTO TECHNOLOGY CNET TECHNOLOGY EATON GIGAMON SYSTEMS LLC AAXEON TECHNOLOGIES LLC. AUDIOCODES, INC. CODE GREEN NETWORKS E‐CORPORATEGIFTS.COM, INC. GLOBAL MARKETING ACCELL AUDIOVOX CODI INC EDGECORE GOLDENRAM ACCELLION AVAYA COMMAND COMMUNICATIONS EDITSHARE LLC GREAT BAY SOFTWARE INC. ACER AMERICA AVENVIEW CORP COMMUNICATION DEVICES INC. EMC GRIFFIN TECHNOLOGY ACTI CORPORATION AVOCENT COMNET ENDACE USA H3C Technology ADAPTEC AVOCENT‐EMERSON COMPELLENT ENGENIUS HALL RESEARCH ADC KENTROX AVTECH CORPORATION COMPREHENSIVE CABLE ENTERASYS NETWORKS HAVIS SHIELD ADC TELECOMMUNICATIONS AXIOM MEMORY COMPU‐CALL, INC EPIPHAN SYSTEMS HAWKING TECHNOLOGY ADDERTECHNOLOGY AXIS COMMUNICATIONS COMPUTER LAB EQUINOX SYSTEMS HERITAGE TRAVELWARE ADD‐ON COMPUTER PERIPHERALS AZIO CORPORATION COMPUTERLINKS ETHERNET DIRECT HEWLETT PACKARD ENTERPRISE ADDON STORE B & B ELECTRONICS COMTROL ETHERWAN HIKVISION DIGITAL TECHNOLOGY CO. LT ADESSO BELDEN CONNECTGEAR EVANS CONSOLES HITACHI ADTRAN BELKIN COMPONENTS CONNECTPRO EVGA.COM HITACHI DATA SYSTEMS ADVANTECH AUTOMATION CORP. BIDUL & CO CONSTANT TECHNOLOGIES INC Exablaze HOO TOO INC AEROHIVE NETWORKS BLACK BOX COOL GEAR EXACQ TECHNOLOGIES INC HP AJA VIDEO SYSTEMS BLACKMAGIC DESIGN USA CP TECHNOLOGIES EXFO INC HP INC ALCATEL BLADE NETWORK TECHNOLOGIES CPS EXTREME NETWORKS HUAWEI ALCATEL LUCENT BLONDER TONGUE LABORATORIES CREATIVE LABS EXTRON HUAWEI SYMANTEC TECHNOLOGIES ALLIED TELESIS BLUE COAT SYSTEMS CRESTRON ELECTRONICS F5 NETWORKS IBM ALLOY COMPUTER PRODUCTS LLC BOSCH SECURITY CTC UNION TECHNOLOGIES CO FELLOWES ICOMTECH INC ALTINEX, INC. -

Comprehensive Annual Financial Report for the Year Ended June 30, 2016

Tualatin Valley Fire and Rescue A Rural Fi re Protection District, Tigard, Oregon Comprehensive Annual Financial Report For the Year Ended June 30, 2016 Tualatin Valley Fire and Rescue 11945 S.W. 70th Avenue Tigard, Oregon 97223 Phone: (503) 649-8577 www.tvfr.com Cover photo courtesy of Claire Cooper Prepared by the Finance Department Table of Contents INTRODUCTORY SECTION Letter of Transmittal 3 Certificate of Achievement for Excellence in Financial Reporting 10 Organization Chart 11 Elected and Appointed Officials 12 FINANCIAL SECTION Independent Auditor’s Report 15 Management’s Discussion and Analysis 21 Basic Financial Statements: 35 Government-wide Financial Statements: Balance Sheet – Governmental Funds/Statement of Net Position 37 Statement of Governmental Fund Revenues, Expenditures, Other Financing Sources (Uses), and Changes in Fund Balances/Statement of Activities 39 Fund Financial Statements: Statement of Revenues, Expenditures, Other Financing Sources (Uses), and Changes in Fund Balances – Budget and Actual – General Fund 40 Statement of Net Position – Proprietary Fund 42 Statement of Revenues, Expenses, and Changes in Net Position – Proprietary Fund 43 Statement of Cash Flows – Proprietary Fund 44 Notes to the Basic Financial Statements 45 Required Supplementary Information: 81 Schedule of Funding Progress – Health Benefit Retiree Program 83 Schedule of the District’s Proportionate Share of the Net Pension (Asset)/Liability 84 Schedule of the District’s Pension Plan Contributions 85 Schedules of Single-Employer Defined Benefit -

Housing Opportunity Program

NEW ISSUE RATINGS: 2005 Series C − Moody’s Aa2 BOOK-ENTRY ONLY 2005 Series D − Moody’s Aaa (Ambac-Insured) In the opinion of Preston Gates & Ellis LLP, Bond Counsel, interest on the 2005 Series C Bonds is included in gross income subject to federal income taxation. Interest on the 2005 Series C Bonds is exempt from Oregon personal income tax and is also exempt from personal income taxation by Multnomah County, Oregon. See “TAX MATTERS” herein. In the opinion of Preston Gates & Ellis LLP, Bond Counsel, assuming compliance with certain covenants of the City, interest on the 2005 Series D Bonds is excluded from the gross income of the owners of the 2005 Series D Bonds for federal income tax purposes under existing law. Interest on the 2005 Series D Bonds is not an item of tax preference for purposes of either individual or corporate alternative minimum tax. Interest on the 2005 Series D Bonds may be indirectly subject to corporate alternative minimum tax and certain other taxes imposed on certain corporations. Interest on the 2005 Series D Bonds is exempt from Oregon personal income tax and is also exempt from personal income taxation by Multnomah County, Oregon See “TAX MATTERS” and “OTHER FEDERAL TAX MATTERS” herein. City of Portland, Oregon $3,170,000 $6,975,000 Limited Tax Housing Limited Tax Housing Revenue Bonds Revenue Bonds 2005 Series C 2005 Series D (Federally Taxable) (Tax-Exempt) (Housing Opportunity Program) (Housing Opportunity Program) BASE CUSIP: 736704 DATED: Date of Delivery DUE: June 1, as shown on inside cover The City of Portland, Oregon, Limited Tax Housing Revenue Bonds, 2005 Series C (Federally Taxable) (Housing Opportunity Program) (the “2005 Series C Bonds”) and Limited Tax Housing Revenue Bonds, 2005 Series D (Tax Exempt) (Housing Opportunity Program) (the “2005 Series D Bonds” and, collectively with the 2005 Bonds, the “2005 Bonds”) will be issued in registered book-entry form only without coupons in denominations of $5,000 or integral multiples thereof. -

Vanport Society

DONOR HONOR ROLL 2014-2015 | Recognizes gifts received between July 1, 2014 through June 30, 2015. Earle Chiles William Michael Foster Family Phil Bogue VANPORT Sue Cooley Friends from Indonesia Duncan and Cindy Campbell Jeannine Cowles Gerding Edlen Development Norm and Rickie Daniels SOCIETY Michael DeShane ◊ and Keren Brown Wilson ◊ John and Betty Gray Geography Fund of the Laura and Doug Eyer Mark and Ann Edlen Oregon Community Foundation Les and Nancy Fahey Diana Gerding Conrad N. Hilton Foundation Tom and Marilyn Fink The Vanport Society recognizes Terry Harrington Howard Hughes Medical Institute Bill and Jane Furman donors whose lifetime giving to Al and Nancy Jubitz Intel Corporation/Intel Foundation Jack and Deane Garrison Robert Wood Johnson Foundation Portland State University is Irving Levin and Stephanie Fowler Bob Gleason ◊ • W.M. Keck Foundation $100,000 or more. With deep Lawrence Levy and Pamela Lindholm- Levy Dan and Karen Halloran W. K. Kellogg Foundation gratitude, we honor all members Jack and Lynn Loacker Debra C. Harris ◊ The Lemelson Foundation of the Vanport Society. Lorry Lokey Art and Sandy James Bob and Sharon Miller LTX-Credence Phil and Penny Knight Rick and Erika Miller Maybelle Clark Macdonald Fund Davis and Judy Moriuchi Gordon and Betty Moore Mentor Graphics Corporation/Mentor Graphics Bob Rawson Foundation FREMONT MEMBERS Robert and Jane Morrow Julie and William Reiersgaard Meyer Memorial Trust $10 MILLION AND ABOVE Martha and John O’Malley Dick Solomon and Alyce Flitcraft M. J. Murdock Charitable Trust Jim and Shirley Rippey Spike Wadsworth and Sherry Sheng INDIVIDUALS Oracle America, Inc. John Salmon and Marcia Schulmerich Fariborz and Azam Maseeh The Oregon Community Foundation CORPORATIONS, FOUNDATIONS, Allen Ray Sandstrom ORGANIZATIONS The Pew Charitable Trusts CORPORATIONS, FOUNDATIONS, Arlene Schnitzer Anonymous ORGANIZATIONS Portland General Electric Company/PGE Jordan Schnitzer Foundation The Autzen Foundation Massiah Foundation, Inc. -

Infocus In120sta Series Datasheet (US English)

in120STa Short throw. High brightness. Unbeatable value. High-value short throw projection with wireless and interactive options www.infocus.com in120STa Tremendous value and flexibility without shadow interference The InFocus IN120STa Series projectors combine short throw, high brightness, networking and low cost – making them perfect for classrooms, offices or tight spaces like trade show booths. These value-packed projectors are easy to buy and built to perform with multiple ways to connect, beautiful image quality, in124STa in126STa and option to convert to an interactive projector. Plus, the short XGA WXGA (1024 x 768) (1280 x 800) throw lens reduces shadows, prevents light from shining in the 3300 lumens 3300 lumens 0.63 throw ratio 0.52 throw ratio presenter’s face, and saves space. Why choose the IN120STa Series? High Brightness and High Contrast ¡ Ultra-low purchase price The image quality of these projectors will not disappoint. ¡ High brightness and high contrast ratio 3300 lumens will give you bright, clear images with the ¡ Short throw for big images in tight spaces lights on and the high 15000:1 contrast ratio adds ¡ Convert to be an interactive projector with sharpness with darker blacks and whiter whites. optional LiteBoard adapter ¡ Wireless connectivity with optional USB adapter You can also instantly dim the projector with the remote ¡ PC-less display from USB drive or 2GB of control to divert your audience’s attention onto you and internal memory extend lamp life. ¡ Display over HDMI or USB The short throw lens gives you big images in tight spaces ¡ Present Office docs, video, audio, photos and and prevents light from shining in the presenter’s face. -

2021 [email protected] Via Santissima 20, Borgosatollo, Brescia - Italia

2021 [email protected] http://www.partelli.it Via Santissima 20, Borgosatollo, Brescia - Italia CATALOGO DI RICAMBI E COMPONENTI 3AAA 3D connexion 3M 3M Company 3Wave 4D Technology 555 Motors FLEXIBLE AUTOMATION AMiT, spol. s r.o. Aaeon AAF Aag Aalborg Instruments Aa Tech ABAC Abanaki Oil Skimmer Abax Abaxis Abbey ABB Jokab ABB SAGE AB C.A. ÖSTBERG ABC diesel ABCO Ab Connectors ABEL ABEL Piston pump ABEM Abex (Parker) Abicor Binzel Hetronic Ab Kihlstroms Manometerfabrik ABLE SYSTEMS abloy Abl Sursum Abm bvba pomac-lub-services sprl ABP INDUCTION Abracon A.B.S. Silo Absolute Process Instruments AB TRASMISSIONI Abus ACC Accel Accele Acco Acco Rexel ACCRETECH ACCU CODER ACCUCUTTER Accuenergy Accu-Lube Accumax ACCU-SORT AccuStandard Accustar Accu Tools Accuway ACDC Dynamics Acd Cryo Ac-Delco Ace Ace Controls Ace Laboratory Ace-mec Ace Pneumatic Ace Tool ACHENBACH Achilli s.r.l. ACI Ackrutat Acksys Acla Aclafrance Acm Acme Acme Electric ACMI AC Motoren ACOEM Acomel Acopian ACOPOS Acr Electronics Acrolon Acroprint Acs Control-System ACS CONTSYS Acson International Actaris [Itron] ACT ELECTRIC Actia Action Instruments (Eurotherm) ACT PRESSURE SWITCH Actreg Act Test Panels Acuangle Acuvim МAC Valves A&D Adalit Vendiamo solo prodotti nuovi e originali! La nostra società non è un rivenditore ufficiale né un costruttore dei prodotti delle marche indicate sul sito. Le marche indicate su questo sito ed i loro loghi sono in possesso dei rispettivi proprietari.  [email protected] http://www.partelli.it Via Santissima 20, Borgosatollo, Brescia - Italia Adam Adamczewski Adams Armaturen Adams Lube Adams Rite Adani ADAN LTD Adaptall Adaptec Adc Adca Adda Adda Antriebstechnik Adder Technology ADDONICS. -

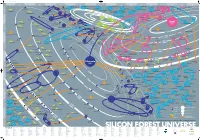

Silicon Forest Universe

15239 Poster 9/16/02 1:03 PM Page 1 AB CDE FGH I JKL M N O P Q R S Pearlsoft COMSAT General Integrated Systems Ashwood Group '85 Qualis Design fka CPU International Nel-Tech Development '98 Qsent '01 Briefsmart.com '00 Relyent TrueDisk Trivium Systems '80 '74 '99 '90 Gearbeat '81 Relational Systems Galois 3DLand Teradyne in 2001 '85 '00 '98 Solution Logic SwiftView Imagenation '89 Metro One IronSpire '84 Smart Mediary Systems Connections 13 Telecommunications WireX GenRad in 1996 '00 CyberOptics E-Core Salu Logiplex '79 MyHealthBank Semiconductor Cotelligent Technologies Fujitsu America Barco Metheus '77 '99 Group Knowledge fka United Data Biotronik Timlick & Associates in 1999 Gadget Labs Adaptive Solutions Wave International Processing Cascade Laser '98 Webridge Axis Clinical Software Mitron Basicon '91 GemStone fka Servio Logic Source Services '83 Integra Telecom Accredo FaxBack Polyserve Metheus Intersolv Babcock & Jenkins Electro '79 Informedics Scientific Sliceware Graphic Software Systems Industries IBM 12 in 1999 Atlas Telecom 1944 Sequent Computer ProSight Credence in 2001 19 ADC Kentrox '78 Oracle '69 Merant Datricon 60s Informix Systems FEI Sage Software fka Polytron MKTX 197 Mikros Nike 0s Etec Systems '63 19 Sentrol in 1995 Intel 80s SEH America Teseda Oregon Graduate Institute Flight Dynamics 1976 '97 1990 Purchasing Solutions Fluence ~ Relcom Vidco Mushroom Resources Cunningham & Cunningham '99 Myteam.com Praegitzer Industries Integrated Measurement Systems Zicon Digital World Lucy.Com Nonbox in 2001 ATEQ 11 Software Access -

Last Updated 10/02/12 Brand Association List Below Is the List Of

Last updated 10/02/12 Brand Association List Below is the list of brands used in the 2013 Final Tier Assignment Schedule for Washington’s Electronic Product Recycling Program. Brands are associated with the responsible manufacturer. The manufacturers listed are those Ecology has identified as the brand owners of electronic products covered by this program (computers, monitors, laptops, televisions, tablets, and e-Readers). Is Your Registration Up to Date? • Manufacturers who own additional brands of covered electronic products not currently registered must add those brands to their registration. • Brand owners of covered electronic products that are not on this list must register as a new participant. If you have questions, please contact Christine Haun at 360-407-6107 or [email protected]. Brand Manufacturer 2go PC Computer Technology Link 3D Corporation 3D Corporation 3M Dynapro 3M Touch Systems 4th Dimension Computer 4th Dimension Computer A1 Best Computer, Inc computer-fix Abacus Abacus Office Machines ACC Tech ACC Tech Access HD GXi International Accu Scan J.C. Penney Corporation, Inc. Accurian RadioShack Corp Acer Acer America Corp ACI Micro ACI Micro ACS Associated Computer Specialists ACTION America Action Inc ACW Computer Warehouse of Central Florida, Inc ADEK ADEK Industrial Computers ADP ADP ADT ADT, Ltd ADVENT Audiovox Electronics Corp. Advueu ProMedia Technologies Inc Affinity Kith Consumer Product Inc. Afunta Afunta, LLC AG Neovo AG Neovo Technology Corp Agasio Amcrest Technologies LLC AGPTEK Mambate USA, Inc. Aiwa Sony Electronics Inc Alden 3MD Inc. Alienware Dell Computer Corp Allegra Electronics Calypso Electronics ALR Acer America Corp Last updated 10/02/12 Aluratek Aluratek, Inc. -

City of Bend Active Business Registrations Print Date: 10/1/2019

City of Bend Active Business Registrations Print Date: 10/1/2019 Business Name License # Street Address Suite Zip Code NAICS Code NAICS Description "A WOMAN'S TOUCH" 20-9796 63112 TURRET CT 97701 561720 JANITORIAL SERVICES *PICKLE 19-17257 61170 FOREST MEADOW PL 97702 541921PHOTOGRAPHY STUDIOS, PORTRAIT 1 DEGREE ADVENTURES 20-18483 19979 POWERS RD 97702 541611 ADMIN MGT & GEN MGT CONSULTING SVC 10 BARREL BREWING COMPANY 21-15897 1135 NW GALVESTON AVE BLDG A 97703 312120BREWERIES 1031 CORP 20-15698 233 SW WILSON AVE STE 204 97702 531390 OTHER ACTIVITIES RELATED TO REAL ESTATE 1130 NW KINGSTON AVE STR 20-14094 1130 NW KINGSTON AVE 97703 531190LESSORS OF OTHER REAL ESTATE PROPERTY 11TH ST SALON 20-5726 1537 NW 11TH ST 97703 812112BEAUTY SALONS 1567 NW ELGIN AVENUE VACATION 20-9932 1567 NW ELGIN AVE 97703 721199ALL OTHR TRAVELER ACCOMMODATION 18-20 SE 24TH AVENUE LLC 20-13484 328 NW RIVERFRONT ST 97703 531190LESSORS OF OTHER REAL ESTATE PROPERTY 1905 PROPERTIES 20-18574 2766 NW CHAMPION CIR 97703 531210 OFFICES OF REAL ESTATE AGENTS & BROKERS 1905 REAL ESTATE 20-13264 150 NE BEND RIVER MALL AVE STE 300 97703 531210 OFFICES OF REAL ESTATE AGENTS & BROKERS 1943 BEND, LLC 20-12782 19551 MEADOWBROOK DR 97702 531190 LESSORS OF OTHER REAL ESTATE PROPERTY 1ST CHOICE ASSISTED CARE, LLC 20-12271 2570 NE TWIN KNOLLS DR STE 120 97701 624120 SVCS FOR THE ELDERLY & PERSONS W/DISABIL 1ST IMPRESSIONS CLEANING 20-6280 61547 SE LINCOLN LN 97702 561720 JANITORIAL SERVICES 2 SISTERS CLEANING SERVICE LLC 20-18108 20065 BADGER RD 97702 561720JANITORIAL SERVICES -

Tualatin Valley Fire and Rescue a Rural Fire Protection District, Tigard, Oregon

Tualatin Valley Fire and Rescue A Rural Fire Protection District, Tigard, Oregon Comprehensive Annual Financial Report for the year ended June 30, 2017 Proudly Serving the Cities of: Beaverton • Durham • King City • Newberg North Plains • Rivergrove • Sherwood • Tigard Tualatin • West Linn • Wilsonville and portions of: Washington • Clackamas • Multnomah Yamhill Counties Tualatin Valley Fire and Rescue A Rural Fire Protection District, Tigard, Oregon Comprehensive Annual Financial Report for the year ended June 30, 2017 11945 SW 70th Avenue Tigard, Oregon 97223 Phone: (503) 649‐8577 www.tvfr.com Prepared by the Finance Department Table of Contents _____________________________________________________________________ Introductory Section Letter of Transmittal ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 3 Certificate of Achievement for Excellence in Financial Reporting ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 10 Organizational Chart ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 11 Elected and Appointed Officials ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 12 Financial Section Independent Auditor’s Report ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 15 Management’s Discussion and Analysis ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐