A Systems Approach to the Determination of the NAIRU, Inflation and Potential Output in Austria

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Total and Short-Term Unemployment and the Recent Behavior of Prices and Wages

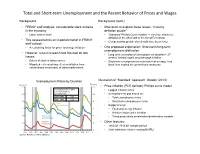

Total and Short-term Unemployment and the Recent Behavior of Prices and Wages Background Background (cont.) • FRBNY staff analysis: considerable slack remains • Motivation to explore these issues: “missing in the economy deflation puzzle” • Labor market flows • “Standard” Phillips Curve models → very low inflation or deflation in the aftermath of the Great Recession • This assessment is an important factor in FRBNY • Compensation growth also should have been lower staff outlook • A restraining factor for price- and wage-inflation • One proposed explanation: Short-term/long-term unemployment distinction • However, recent research has focused on two • Long-term unemployed (unemployment duration > 27 issues: weeks): limited impact on price/wage inflation • Extent of slack in labor market • Short-term unemployment near historical average: less • Magnitude of restraining effect on inflation from slack than implied by conventional measures conventional measure(s) of labor market slack Unemployment Rates by Duration Illustration of “Standard” Approach: Gordon (2013) Percent Percent 12 12 • Price-inflation (PCE deflator) Phillips curve model: Correlation Between Short- • Lagged inflation terms term and Long-term 10 Unemployment 10 • Unemployment gap based on: 1976—2007 0.63 • Total unemployment rate 1976—2013 0.28 8 8 • Short-term unemployment rate Total Unemployment • Supply shocks: 6 6 • Food and energy inflation • Relative import price inflation 4 Short-term 4 • Trend productivity acceleration/deceleration variable Unemployment Long-term • Other features: 2 Unemployment 2 • 1960:Q1-2013:Q1 sample period 0 0 • Joint estimation of time-varying NAIRU 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 4 Source: Bureau of Labor Statistics Total and Short-term Unemployment and the Recent Behavior of Prices and Wages Evaluation of Short-term vs. -

Calculating the Output Gap

ECONOMIC AND MONETARY DEVELOPMENTS AND PROSPECTS Appendix 2 Calculating the output gap The output gap is an important concept in the preparation of inflation forecasts and assessments of the economic outlook. However, the output gap is difficult to measure and subject to great uncertainty in practice. The techniques used by the Central Bank of Iceland and elsewhere to calculate the output gap, which have previously been described in Monetary Bulletin (2000/4 pp. 14-15), will be recapitulated here taking particular account of investments in the aluminium and power sectors, since these have a substantial impact on both the level of production and output potential in the economy, not only during the construction phase but also when the investments 1 have been completed. 2005•1 MONETARY BULLETIN Definition of the output gap The output gap is defined as the difference between actual and potential GDP as a per cent of potential GDP, i.e.: (1) P where GAPt is the output gap, Yt is GDP in real terms and Y t is the potential output of the economy, all during the year t. Potential output is defined as the level of GDP that is consistent with full utilisation of all factors of production under conditions of stable inflation. Thus potential output is determined on the supply side of the economy, i.e. by capital stock, labour use and available technology. Potential output in the long term is determined by how effici- ently the available factors of production can be utilised for a given level of productivity. In the short run, however, aggregate demand can drive the level of production beyond long-term potential output. -

Output Gaps and Robust Monetary Policy Rules

SVERIGES RIKSBANK WORKING PAPER SERIES 260 Output Gaps and Robust Monetary Policy Rules Roberto M. Billi MARCH 2012 WORKING PAPERS ARE OBTAINABLE FROM Sveriges Riksbank • Information Riksbank • SE-103 37 Stockholm Fax international: +46 8 787 05 26 Telephone international: +46 8 787 01 00 E-mail: [email protected] The Working Paper series presents reports on matters in the sphere of activities of the Riksbank that are considered to be of interest to a wider public. The papers are to be regarded as reports on ongoing studies and the authors will be pleased to receive comments. The views expressed in Working Papers are solely the responsibility of the authors and should not to be interpreted as reflecting the views of the Executive Board of Sveriges Riksbank. Output Gaps and Robust Monetary Policy Rules Roberto M. Billiy Sveriges Riksbank Working Paper Series No. 260 March 2012 Abstract Policymakers often use the output gap, a noisy signal of economic activity, as a guide for setting monetary policy. Noise in the data argues for policy caution. At the same time, the zero bound on nominal interest rates constrains the central bank’sability to stimulate the economy during downturns. In such an environment, greater policy stimulus may be needed to stabilize the economy. Thus, noisy data and the zero bound present policymakers with a dilemma in deciding the appropriate stance for monetary policy. I investigate this dilemma in a small New Keynesian model, and show that policymakers should pay more attention to output gaps than suggested by previous research. Keywords: output gap, measurement errors, monetary policy, zero lower bound JEL: E52, E58 I thank Tor Jacobson, Per Jansson, Ulf Söderström, David Vestin, Karl Walentin, and seminar participants at Sveriges Riksbank for helpful comments and discussions. -

Mind the Output Gap: the Disconnect of Growth and Inflation During Recessions and Convex Phillips Curves in the Euro Area

Working Paper Series Marco Gross, Willi Semmler Mind the output gap: the disconnect of growth and inflation during recessions and convex Phillips curves in the euro area Task force on low inflation (LIFT) No 2004 / January 2017 Disclaimer: This paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB. Task force on low inflation (LIFT) This paper presents research conducted within the Task Force on Low Inflation (LIFT). The task force is composed of economists from the European System of Central Banks (ESCB) - i.e. the 29 national central banks of the European Union (EU) and the European Central Bank. The objective of the expert team is to study issues raised by persistently low inflation from both empirical and theoretical modelling perspectives. The research is carried out in three workstreams: 1) Drivers of Low Inflation; 2) Inflation Expectations; 3) Macroeconomic Effects of Low Inflation. LIFT is chaired by Matteo Ciccarelli and Chiara Osbat (ECB). Workstream 1 is headed by Elena Bobeica and Marek Jarocinski (ECB) ; workstream 2 by Catherine Jardet (Banque de France) and Arnoud Stevens (National Bank of Belgium); workstream 3 by Caterina Mendicino (ECB), Sergio Santoro (Banca d’Italia) and Alessandro Notarpietro (Banca d’Italia). The selection and refereeing process for this paper was carried out by the Chairs of the Task Force. Papers were selected based on their quality and on the relevance of the research subject to the aim of the Task Force. The authors of the selected papers were invited to revise their paper to take into consideration feedback received during the preparatory work and the referee’s and Editors’ comments. -

New Keynesian Macroeconomics: Empirically Tested in the Case of Republic of Macedonia

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Josheski, Dushko; Lazarov, Darko Preprint New Keynesian Macroeconomics: Empirically tested in the case of Republic of Macedonia Suggested Citation: Josheski, Dushko; Lazarov, Darko (2012) : New Keynesian Macroeconomics: Empirically tested in the case of Republic of Macedonia, ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften, Leibniz-Informationszentrum Wirtschaft, Kiel und Hamburg This Version is available at: http://hdl.handle.net/10419/64403 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu NEW KEYNESIAN MACROECONOMICS: EMPIRICALLY TESTED IN THE CASE OF REPUBLIC OF MACEDONIA Dushko Josheski 1 Darko Lazarov2 Abstract In this paper we test New Keynesian propositions about inflation and unemployment trade off with the New Keynesian Phillips curve and the proposition of non-neutrality of money. -

The Nairu Concept, Its Phillips Curve Origins and Its Evolution in Terms of the Economic Policy Debate

7+(1$,58&21&(37±0($685(0(17 81&(57$,17,(6+<67(5(6,6$1'(&2120,& 32/,&<52/( 30&$'$0$1'.0&02552: 7$%/(2)&217(176 ,QWURGXFWRU\5HPDUNV &KDSWHUUncertainties concerning model selection : A number of plausible modelling approaches exist for Measuring the NAIRU 1.1 Univariate Methods / Models 1.2 Variants of the Expectations Augmented Phillips Curve Approach &KDSWHUProduction of NAIRU estimates for the US, Japan and EU- 15 using a Conventional Bargaining model approach &KDSWHU Empirical Inadequacies : Uncertainties surrounding the NAIRU Point Estimates 3.1 Confidence Intervals 3.2 Results from US and Canadian NAIRU studies &KDSWHU Theoretical Weaknesses : The Notion of Hysteresis Complicates the Interpretation of Changes in the NAIRU &KDSWHU The Nairu Concept, its Phillips Curve Origins and its Evolution in terms of the Economic Policy Debate &RQFOXGLQJ5HPDUNV 2 7+(1$,58&21&(37±0($685(0(17 81&(57$,17,(6+<67(5(6,6$1' (&2120,&32/,&<52/( ,1752'8&725<5(0$5.6 In 1968 Friedman put forward the notion of a “natural” rate of unemployment to encapsulate the idea that a “normal” level of unemployment, roughly equivalent to the amount of frictional and structural unemployment, persists even when the labour market is in equilibrium. Since there are no direct measures of the natural rate, as it is essentially a theoretical construct, one must be satisfied with proxy estimates derived using various methods including that which draws on Tobin’s concept of the non- accelerating inflation rate of unemployment(i.e. the NAIRU). This latter concept has been used extensively since the 1970s to show that policy makers are not in a position to buy permanent reductions in unemployment by tolerating a higher rate of inflation. -

Measuring Potential Output and Output Gap and Macroeconomic Policy: the Ac Se of Kenya Angelica E

University of Connecticut OpenCommons@UConn Economics Working Papers Department of Economics October 2005 Measuring Potential Output and Output Gap and Macroeconomic Policy: The aC se of Kenya Angelica E. Njuguna Kenyatta University and KIPPRA Stephen N. Karingi United Nations Economic Commission for Africa Mwangi S. Kimenyi University of Connecticut Follow this and additional works at: https://opencommons.uconn.edu/econ_wpapers Recommended Citation Njuguna, Angelica E.; Karingi, Stephen N.; and Kimenyi, Mwangi S., "Measuring Potential Output and Output Gap and Macroeconomic Policy: The asC e of Kenya" (2005). Economics Working Papers. 200545. https://opencommons.uconn.edu/econ_wpapers/200545 Department of Economics Working Paper Series Measuring Potential Output and Output Gap and Macroeco- nomic Policy: The Case of Kenya Angelica E. Njuguna Kenyatta University and KIPPRA Stephen N. Karingi United Nations Economic Commission for Africa Mwangi S. Kimenyi University of Connecticut Working Paper 2005-45 October 2005 341 Mansfield Road, Unit 1063 Storrs, CT 06269–1063 Phone: (860) 486–3022 Fax: (860) 486–4463 http://www.econ.uconn.edu/ This working paper is indexed on RePEc, http://repec.org/ Abstract Measuring the level of an economy.s potential output and output gap are essen- tial in identifying a sustainable non-inflationary growth and assessing appropriate macroeconomic policies. The estimation of potential output helps to determine the pace of sustainable growth while output gap estimates provide a key bench- mark against which to assess inflationary or disinflationary pressures suggesting when to tighten or ease monetary policies. These measures also help to provide a gauge in the determining the structural fiscal position of the government. -

Working Paper No. 563 Whither New Consensus Macroeconomics? the Role of Government and Fiscal Policy in Modern Macroeconomics

Working Paper No. 563 Whither New Consensus Macroeconomics? The Role of Government and Fiscal Policy in Modern Macroeconomics by Giuseppe Fontana* May 2009 * University of Leeds (UK) and Università del Sannio (Benevento, Italy). Correspondence address: Economics, LUBS, University of Leeds, Leeds LS2 9JT, UK. E-mail: [email protected]; tel.: +44 (0) 113 343 4503; fax: +44 (0) 113 343 4465. The Levy Economics Institute Working Paper Collection presents research in progress by Levy Institute scholars and conference participants. The purpose of the series is to disseminate ideas to and elicit comments from academics and professionals. The Levy Economics Institute of Bard College, founded in 1986, is a nonprofit, nonpartisan, independently funded research organization devoted to public service. Through scholarship and economic research it generates viable, effective public policy responses to important economic problems that profoundly affect the quality of life in the United States and abroad. The Levy Economics Institute P.O. Box 5000 Annandale-on-Hudson, NY 12504-5000 http://www.levy.org Copyright © The Levy Economics Institute 2009 All rights reserved. ABSTRACT In the face of the dramatic economic events of recent months and the inability of academics and policymakers to prevent them, the New Consensus Macroeconomics (NCM) model has been the subject of several criticisms. This paper considers one of the main criticisms lodged against the NCM model, namely, the absence of any essential role for the government and fiscal policy. Given the size of the public sector and the increasing role of fiscal policy in modern economies, this simplifying assumption of the NCM model is difficult to defend. -

Deflation: Economic Significance, Current Risk, and Policy Responses

Deflation: Economic Significance, Current Risk, and Policy Responses Craig K. Elwell Specialist in Macroeconomic Policy August 30, 2010 Congressional Research Service 7-5700 www.crs.gov R40512 CRS Report for Congress Prepared for Members and Committees of Congress Deflation: Economic Significance, Current Risk, and Policy Responses Summary Despite the severity of the recent financial crisis and recession, the U.S. economy has so far avoided falling into a deflationary spiral. Since mid-2009, the economy has been on a path of economic recovery. However, the pace of economic growth during the recovery has been relatively slow, and major economic weaknesses persist. In this economic environment, the risk of deflation remains significant and could delay sustained economic recovery. Deflation is a persistent decline in the overall level of prices. It is not unusual for prices to fall in a particular sector because of rising productivity, falling costs, or weak demand relative to the wider economy. In contrast, deflation occurs when price declines are so widespread and sustained that they cause a broad-based price index, such as the Consumer Price Index (CPI), to decline for several quarters. Such a continuous decline in the price level is more troublesome, because in a weak or contracting economy it can lead to a damaging self-reinforcing downward spiral of prices and economic activity. However, there are also examples of relatively benign deflations when economic activity expanded despite a falling price level. For instance, from 1880 through 1896, the U.S. price level fell about 30%, but this coincided with a period of strong economic growth. -

The Labor Market and the Phillips Curve

4 The Labor Market and the Phillips Curve A New Method for Estimating Time Variation in the NAIRU William T. Dickens The non-accelerating inflation rate of unemployment (NAIRU) is fre- quently employed in fiscal and monetary policy deliberations. The U.S. Congressional Budget Office uses estimates of the NAIRU to compute potential GDP, that in turn is used to make budget projections that affect decisions about federal spending and taxation. Central banks consider estimates of the NAIRU to determine the likely course of inflation and what actions they should take to preserve price stability. A problem with the use of the NAIRU in policy formation is that it is thought to change over time (Ball and Mankiw 2002; Cohen, Dickens, and Posen 2001; Stock 2001; Gordon 1997, 1998). But estimates of the NAIRU and its time variation are remarkably imprecise and are far from robust (Staiger, Stock, and Watson 1997, 2001; Stock 2001). NAIRU estimates are obtained from estimates of the Phillips curve— the relationship between the inflation rate, on the one hand, and the unemployment rate, measures of inflationary expectations, and variables representing supply shocks on the other. Typically, inflationary expecta- tions are proxied with several lags of inflation and the unemployment rate is entered with lags as well. The NAIRU is recovered as the constant in the regression divided by the coefficient on unemployment (or the sum of the coefficient on unemployment and its lags). The notion that the NAIRU might vary over time goes back at least to Perry (1970), who suggested that changes in the demographic com- position of the labor force would change the NAIRU. -

Two Approaches for Measuring the NAIRU Considered

TI 2007-017/1 Tinbergen Institute Discussion Paper Derived Measurement in Macroeconomics: Two Approaches for Measuring the NAIRU Considered Peter Rodenburg University of Amsterdam. Tinbergen Institute The Tinbergen Institute is the institute for economic research of the Erasmus Universiteit Rotterdam, Universiteit van Amsterdam, and Vrije Universiteit Amsterdam. Tinbergen Institute Amsterdam Roetersstraat 31 1018 WB Amsterdam The Netherlands Tel.: +31(0)20 551 3500 Fax: +31(0)20 551 3555 Tinbergen Institute Rotterdam Burg. Oudlaan 50 3062 PA Rotterdam The Netherlands Tel.: +31(0)10 408 8900 Fax: +31(0)10 408 9031 Most TI discussion papers can be downloaded at http://www.tinbergen.nl. Derived Measurement in Macroeconomics: Two Approaches for Measuring the NAIRU considered ∗ Peter Rodenburg Faculty of Economics and Econometrics and Faculty of European Studies University of Amsterdam Spuistraat 134 1012 VB Amsterdam The Netherlands Tel: 0031 20-525 4660 E-mail: [email protected] http://home.medewerker.uva.nl/p.rodenburg/ Abstract: This paper investigates two different procedures for the measurement of the NAIRU; one based on structural modeling while the other is a statistical approach using Vector Auto Regression (VAR)-models. Both measurement procedures are assessed by confronting them with the dominant theory of measurement, the Representation Theory of Measurement, which states that for sound measurement a strict isomorphism (strict one-to- one mapping) is needed between variations in the phenomenon (the NAIRU) and numbers. The paper argues that shifts of the Phillips-curve are not a problem for the structural approach to measurement of the NAIRU, as the NAIRU itself is a time-varying concept. -

The New Neoclassical Synthesis and the Role of Monetary Policy

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: NBER Macroeconomics Annual 1997, Volume 12 Volume Author/Editor: Ben S. Bernanke and Julio Rotemberg Volume Publisher: MIT Press Volume ISBN: 0-262-02435-7 Volume URL: http://www.nber.org/books/bern97-1 Publication Date: January 1997 Chapter Title: The New Neoclassical Synthesis and the Role of Monetary Policy Chapter Author: Marvin Goodfriend, Robert King Chapter URL: http://www.nber.org/chapters/c11040 Chapter pages in book: (p. 231 - 296) Marvin Goodfriendand RobertG. King FEDERAL RESERVEBANK OF RICHMOND AND UNIVERSITY OF VIRGINIA; AND UNIVERSITY OF VIRGINIA, NBER, AND FEDERAL RESERVEBANK OF RICHMOND The New Neoclassical Synthesis and the Role of Monetary Policy 1. Introduction It is common for macroeconomics to be portrayed as a field in intellectual disarray, with major and persistent disagreements about methodology and substance between competing camps of researchers. One frequently discussed measure of disarray is the distance between the flexible price models of the new classical macroeconomics and real-business-cycle (RBC) analysis, in which monetary policy is essentially unimportant for real activity, and the sticky-price models of the New Keynesian econom- ics, in which monetary policy is viewed as central to the evolution of real activity. For policymakers and the economists that advise them, this perceived intellectual disarray makes it difficult to employ recent and ongoing developments in macroeconomics. The intellectual currents of the last ten years are, however, subject to a very different interpretation: macroeconomics is moving toward a New NeoclassicalSynthesis. In the 1960s, the original synthesis involved a com- mitment to three-sometimes conflicting-principles: a desire to pro- vide practical macroeconomic policy advice, a belief that short-run price stickiness was at the root of economic fluctuations, and a commitment to modeling macroeconomic behavior using the same optimization ap- proach commonly employed in microeconomics.