Macroeconomic Forecasts for 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Federal Research Division Country Profile: Tajikistan, January 2007

Library of Congress – Federal Research Division Country Profile: Tajikistan, January 2007 COUNTRY PROFILE: TAJIKISTAN January 2007 COUNTRY Formal Name: Republic of Tajikistan (Jumhurii Tojikiston). Short Form: Tajikistan. Term for Citizen(s): Tajikistani(s). Capital: Dushanbe. Other Major Cities: Istravshan, Khujand, Kulob, and Qurghonteppa. Independence: The official date of independence is September 9, 1991, the date on which Tajikistan withdrew from the Soviet Union. Public Holidays: New Year’s Day (January 1), International Women’s Day (March 8), Navruz (Persian New Year, March 20, 21, or 22), International Labor Day (May 1), Victory Day (May 9), Independence Day (September 9), Constitution Day (November 6), and National Reconciliation Day (November 9). Flag: The flag features three horizontal stripes: a wide middle white stripe with narrower red (top) and green stripes. Centered in the white stripe is a golden crown topped by seven gold, five-pointed stars. The red is taken from the flag of the Soviet Union; the green represents agriculture and the white, cotton. The crown and stars represent the Click to Enlarge Image country’s sovereignty and the friendship of nationalities. HISTORICAL BACKGROUND Early History: Iranian peoples such as the Soghdians and the Bactrians are the ethnic forbears of the modern Tajiks. They have inhabited parts of Central Asia for at least 2,500 years, assimilating with Turkic and Mongol groups. Between the sixth and fourth centuries B.C., present-day Tajikistan was part of the Persian Achaemenian Empire, which was conquered by Alexander the Great in the fourth century B.C. After that conquest, Tajikistan was part of the Greco-Bactrian Kingdom, a successor state to Alexander’s empire. -

Enhancing Access to Finance for Sme Development in Tajikistan

ENHANCING ACCESS TO FINANCE FOR SME DEVELOPMENT IN TAJIKISTAN IN DEVELOPMENT SME FOR FINANCE TO ACCESS ENHANCING ENHANCING ACCESS TO FINANCE РАСШИРЕНИЕ ДОСТУПА FOR SME DEVELOPMENT IN К ФИНАНСИРОВАНИЮ В PRIVATE SECTOR DEVELOPMENT TAJIKISTAN ЦЕЛЯХ РАЗВИТИЯ МСП ТАДЖИКИСТАНА Policy Handbook Small and medium-sized enterprises (SMEs) are the Малые и средние предприятия backbone of Tajikistan’s economy, (МСП) составляют костяк yet they face significant barriers экономики Таджикистана, однако in accessing finance. Accounting for испытывают серьезные трудности 50% of GDP, the large inflow of migrant при получении финансирования. Enhancing access remittances is an opportunity for Tajikistan to Один из способов укрепления финансового strengthen the financial sector. However, a number сектора страны заключается в грамотном to finance for SME of important challenges remain: a large proportion использовании денежных переводов, которые of remittances do not enter the formal banking поступают в большом объеме из-за рубежа development in system, and business creation by return migrants is и составляют 50% ВВП. Тем не менее, ряд limited. This Handbook presents recommendations существенных проблем все же сохраняется: to channel savings from remittances as a means значительная часть денежных переводов Tajikistan to improve access to finance and foster SME не поступает в банковскую систему, а development. вернувшиеся мигранты редко открывают собственные предприятия. В настоящем Расширение доступа This Handbook was peer reviewed on 26 November руководстве содержатся рекомендации о 2014 at the OECD Eurasia Competitiveness том, как способствовать формированию у к финансированию в Roundtable. The Roundtable is a policy network that населения сбережений за счет получаемых gathers OECD members and partner countries from денежных переводов в целях повышения целях развития МСП the Eurasia region for knowledge sharing on the доступности финансирования и развития МСП. -

Country Note: Tajikistan

Country Note: Tajikistan OECD Centre for Private Sector Development Sixth Conference on Financial Sector Development in the Central Asian Countries, Azerbaijan and Mongolia 29-30 April 2004, Istanbul Country note: Republic of Tajikistan The Republic of Tajikistan became an independent state in 1991 following the collapse of the Soviet Union. The country subsequently experienced a period of civil war and internal strife. Basic stability was restored only in 1997 after the Agreement on Peaceful Settlement was signed between the government of Tajikistan and the United Tajik Opposition, and a coalition government was formed. The processes of reconciliation and peacekeeping have since been developing satisfactorily. The government is actively strengthening democracy and is working to establish a functioning market economy. After independence, the economy of Tajikistan was faced with various problems, typical of countries in transition to a market economy: low level of incomes and savings; weak market institutions; an incomplete tax system; and ineffectual economic structures. With the collapse of the Soviet Union, Tajikistan lost its traditional export markets and import sources, and budget transfers from Moscow. The republic's level of economic development deteriorated sharply: over the period 1991-1996, production volumes fell to 33.1% of their 1991 level; in 1997 GDP was down by more than 60% on 1991; and the standard of living fell sharply. Signs of economic recovery appeared only in 1997 and 1998, when official statistics put GDP growth at 1.7% and 5.3% respectively. This modest rise was a consequence of the end of the war and the restoration of basic economic stability. -

Economic and Social Commission for Asia and the Pacific

ECONOMIC AND SOCIAL COMMISSION FOR ASIA AND THE PACIFIC TRADERS’ MANUAL FOR LANDLOCKED COUNTRIES: TAJIKISTAN UNITED NATIONS 2009 Trader’s Manual for Landlocked Countries: Tajikistan United Nations publication Copyright © United Nations 2009 All rights reserved Manufactured in Thailand ST/ESCAP/2545 For further information on this online publication, please contact: Mr. Ravi Ratnayake Director Trade and Investment Division Economic and Social Commission for Asia and the Pacific United Nations Building, Rajadamnern Nok Avenue Bangkok 10200, Thailand E-mail: [email protected] This publication may be reproduced in whole or in part for educational or non-profit purposes without special permission from the copyright holder, provided that the source is acknowledged. The ESCAP Publications Office would appreciate receiving a copy of any publication that uses this publication as a source. No use may be made of this publication for resale or any other commercial purpose whatsoever without prior permission. Applications for such permission, with a statement of the purpose and extent of reproduction, should be addressed to the Secretary of the Publications Board, United Nations, New York. i Symbols of United Nations documents are composed of capital letters combined with figures. Mention of such a symbol indicates a reference to United Nations documents. Reference to dollars ($) are United States dollars, unless otherwise stated. Throughout the report, the abbreviation “..” is used in tables to mean not available. The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city, area or of its authorities, or concerning the delimitation of its frontiers or boundaries. -

Maximum Monthly Stipend Rates For

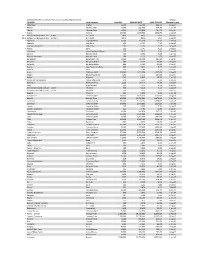

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS Jul 2020 COUNTRY Local Currency Local DSA MAX RES RATE MAX TRV RATE Effective % date * Afghanistan Afghani 12,600 132,300 198,450 1-Aug-07 * Albania Albania Lek(e) 14,000 220,500 330,750 1-Jan-05 Algeria Algerian Dinar 31,600 331,800 497,700 1-Aug-07 * Angola Kwanza 133,000 1,396,500 2,094,750 1-Aug-07 #N/A Antigua and Barbuda (1 Apr. - 30 Nov.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 #N/A Antigua and Barbuda (1 Dec. - 31 Mar.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 * Argentina Argentine Peso 18,600 153,450 230,175 1-Jan-05 Australia AUL Dollar 453 4,757 7,135 1-Aug-07 Australia - Academic AUL Dollar 453 1,200 7,135 1-Aug-07 * Austria Euro 261 2,741 4,111 1-Aug-07 * Azerbaijan (new)Azerbaijan Manat 239 1,613 2,420 1-Jan-05 Bahrain Bahraini Dinar 106 2,226 3,180 1-Jan-05 Bahrain - Academic Bahraini Dinar 106 1,113 1,670 1-Aug-07 Bangladesh Bangladesh Taka 12,400 130,200 195,300 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 * Belarus New Belarusian Ruble 600 5,850 8,775 1-Jan-06 Belgium Euro 338 3,549 5,324 1-Aug-07 Benin CFA Franc(XOF) 123,000 1,291,500 1,937,250 1-Aug-07 Bhutan Bhutan Ngultrum 7,290 76,545 114,818 1-Aug-07 * Bolivia Boliviano 1,200 10,800 16,200 1-Jan-07 * Bosnia and Herzegovina Convertible Mark 279 3,557 5,336 1-Jan-05 Botswana Botswana Pula 2,220 23,310 34,965 1-Aug-07 Brazil Brazilian Real 530 4,373 6,559 1-Jan-05 British Virgin Islands (16 Apr. -

Business Environment in Tajikistan As Seen by Small and Medium Enterprises, 2006

40840 BUSINESS ENVIRONMENT Public Disclosure Authorized IN TAJIKISTAN AS SEEN BY SMALL AND MEDIUM ENTERPRISES, 2006 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The content of this report is under copyright protection. This report may not be reproduced, copied or distributed, in whole or in part, in any form without mandatory citation of “Business En- vironment in Tajikistan as Seen by Small and Medium Enterprises, 2006.” The opinions expressed in this report do not necessarily reflect those of the International Finance Corporation (IFC), the Swiss State Secretariat for Economic Affairs (SECO), or the World Bank Group (WBG). The information in this report is presented in good faith as general informational material and IFC, SECO, and WBG can not be held liable for any loss, expense and/or possible consequences arising from the publication of or the use of information contained in the report. All information and materials used in this report are property of IFC and are preserved in IFC archives. BUSINESS ENVIRONMENT IN TAJIKISTAN AS SEEN BY SMALL AND MEDIUM ENTERPRISES, 2006 CONTENT CONTENT GLOSSARY..............................................................................................................................................vii FOREWORD AND ACKNOWLEDGEMENTS.............................................................................................ix EXECUTIVE SUMMARY.............................................................................................................................xi -

For Tajikistan

Integrated Socioeconomic Response Framework to Covid-19 (ISEF) for Tajikistan UNITED NATIONS IN TAJIKISTAN 2020 Executive Summary The outbreak of Covid-19 pandemic in Tajikistan has amplified its multi-faceted vulnerabilities and precariousness to shocks. After officially announcing the first 15 cases of Covid-19 on April 30, 2020, the number of confirmed cases has continued to rise and by July 9, 2020, the total number of cases had already reached 6,410 including 54 deaths. 1 Tajikistan’s already weak healthcare system makes the task of containing Covid-19 even more challenging. There is limited testing capacity with only a few laboratories certified to conduct polymerase chain reaction (PCR) tests in the country. There is also a limited supply of testing kits and reagents which is affecting the number of tests being carried out. The Covid-19 medical response is already stretching the entire health care system in Tajikistan. As a result, routine clinical services, hospitalization, and immunization programmes are getting affected. Beyond its immediate public health impact, the protracted nature of this pandemic is drastically slowing down the economy, jobs are being lost, and the state faces a tight fiscal space. Tajikistan did not go for a complete lockdown but closed its borders and airport and briefly stopped mass gatherings. However, even these partial measures have significantly impacted this low-income and socio-economically fragile country. According to the latest estimate, Tajikistan’s economy is likely to shrink by 2 percent in 2020. 2 It will be a major setback considering that the economy has recorded a growth rate of around 7 percent in the last five year. -

Education System of Tajikistan During the Civil War

EDUCATION SYSTEM OF TAJIKISTAN DURING THE CIVIL WAR: STUDENTS’ PERSPECTIVES OF HARDSHIPS A Thesis Submitted to the Graduate Faculty of the North Dakota State University of Agriculture and Applied Science By Muhabbat Makhbudovna Yakubova In Partial Fulfillment of the Requirements for the Degree of MASTER OF SCIENCE Major Department: Sociology and Anthropology July 2014 Fargo, North Dakota North Dakota State University Graduate School Title EDUCATION SYSTEM OF TAJIKISTAN DURING THE CIVIL WAR: STUDENT PERSPECTIVES OF HARDSHIPS By MUHABBAT MAKHBUDOVNA YAKUBOVA The Supervisory Committee certifies that this disquisition complies with North Dakota State University’s regulations and meets the accepted standards for the degree of MASTER OF SCIENCE SUPERVISORY COMMITTEE: CHRISTOPHER WHITSEL Chair ANN BURNETT CHRISTINA WEBER GARY GOREHAM Approved: 07/01/2014 JEFFREY T. CLARK Date Department Chair ABSTRACT Civil wars have devastating consequences for people who witness them. Wars collapse states’ economies, ruin infrastructures, and result in death of people. The goal of this study is to examine the multiple perspectives of students about the effects of the civil war in Tajikistan on the education system. The study uses secondary data collected by the “Oral History of Independent Tajikistan Project” of the Organization for Security and Cooperation in Europe (OSCE) Academy. 107 interviews with participants representing all regions of the country, who were in school or university during war in Tajikistan, were selected translated, transcribed and coded. Coding revealed topics and characteristics such as the start of the war, school quality issues, and long-term consequences of the war are the effects of the war on education. The findings also revealed differences in standpoints about the effects of the war on their education based on participants’ gender and region. -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

Maximum Monthly Stipend Rates for Fellows And

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS Sep 2020 COUNTRY Local Currency Local DSA MAX RES RATE MAX TRV RATE Effective % date Afghanistan Afghani 12,500 131,250 196,875 1-Aug-07 * Albania Albania Lek(e) 13,100 206,325 309,488 1-Jan-05 Algeria Algerian Dinar 31,600 331,800 497,700 1-Aug-07 * Angola Kwanza 134,000 1,407,000 2,110,500 1-Aug-07 #N/A Antigua and Barbuda (1 Apr. - 30 Nov.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 #N/A Antigua and Barbuda (1 Dec. - 31 Mar.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 * Argentina Argentine Peso 19,700 162,525 243,788 1-Jan-05 Australia AUL Dollar 453 4,757 7,135 1-Aug-07 Australia - Academic AUL Dollar 453 1,200 7,135 1-Aug-07 Austria Euro 261 2,741 4,111 1-Aug-07 Azerbaijan (new)Azerbaijan Manat 239 1,613 2,420 1-Jan-05 Bahrain Bahraini Dinar 106 2,226 3,180 1-Jan-05 Bahrain - Academic Bahraini Dinar 106 1,113 1,670 1-Aug-07 Bangladesh Bangladesh Taka 12,400 130,200 195,300 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 * Belarus New Belarusian Ruble 680 6,630 9,945 1-Jan-06 Belgium Euro 338 3,549 5,324 1-Aug-07 Benin CFA Franc(XOF) 123,000 1,291,500 1,937,250 1-Aug-07 Bhutan Bhutan Ngultrum 7,290 76,545 114,818 1-Aug-07 Bolivia Boliviano 1,180 10,620 15,930 1-Jan-07 * Bosnia and Herzegovina Convertible Mark 264 3,366 5,049 1-Jan-05 Botswana Botswana Pula 2,220 23,310 34,965 1-Aug-07 Brazil Brazilian Real 530 4,373 6,559 1-Jan-05 British Virgin Islands (16 Apr. -

Migration, Remittances and Climate Resilience in Tajikistan.Indd

Migration, remittances and climate resilience in Tajikistan Working paper Part I Migration, remittances and climate resilience in Tajikistan April 2017 Zhanna Babagaliyeva Abdulkhamid Kayumov Nurullo Mahmadullozoda Nailya Mustaeva This report has been produced by the Regional Environmental Centre for Central Asia (CAREC) in cooperation with the Ministry of Labour, Migration and Employment of Population of the Republic of Tajikistan. The PRISE consortium is comprised of the Overseas Development Institute (lead institution), UK; Grantham Research Institute for Climate Change and the Environment, UK; Innovations Environnement Développement en Afrique, Senegal; and the Sustainable Development Policy Institute, Pakistan; with country research partners the Regional Environmental Centre for Central Asia; Kenya Markets Trust, Kenya; University of Ouagadougou, Burkina Faso and the University of Central Asia, Kyrgyzstan. 2 Migration, remittances and climate resilience in Tajikistan Acknowledgements CAREC would like to express its deepest gratitude to representatives of the PRISE Stakeholder Engagement Platform in Dushanbe, representing the Ministry of Labour, Migration and Employment, Committee for Environmental Protection under the Government of the Republic of Tajikistan, Ministry of Economic Development and Trade, Ministry of Energy and Water Resources, Ministry of Agriculture, academia, civil society organisations and international development partners, who provided valuable contributions to the development of this study. The authors would -

Banking Sector and Economy of CEE Countries: Development Features and Correlation

Centre for Research on Settlements and Urbanism Journal of Settlements and Spatial Planning J o u r n a l h o m e p a g e: http://jssp.reviste.ubbcluj.ro Banking Sector and Economy of CEE Countries: Development Features and Correlation Iurii UMANTSIV 1, Olena ISHCHENKO 1 1 Kyiv National University of Trade and Economics, Faculty of Economics, Management and Psychology, Department of Economic Theory and Competition Policy, Kyiv, UKRAINE E-mail: [email protected], [email protected] DOI: 10.24193/JSSP.2017.1.05 https://doi.org/10.24193/JSSP.2017.1.05 K e y w o r d s: economy of CEE country, banking system, financial sector, role of banks, correlation between GDP and bank investments, EU operational programs, CEE countries, banking sector development A B S T R A C T This research focuses on the analysis of current trends in the banking sector of Central and Eastern Europe (CEE), and on its role in the development of the economy. This region is represented by countries situated at different levels of development and types of economic system. The following countries are analyzed: Bulgaria, Poland, Romania, the Republic of Belarus and Ukraine. The article starts with a general description of the economy of each of the five countries listed above, followed by a discussion of main trends of their development and a comparison of these states based on the status of their socioeconomic development. The study will also examine the banking systems of each of these countries looking at the types of banks that are present on the market, capital ownership, and market share, as well as the main indicators of soundness of the banking system.