Moneris Merchant Resource Center User Manual 46

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GSR Service Repair Guide

paypoint Implementation Guide 4.77 Implementation Guide paypoint version 5.08.xx, 5.11.xx, 5.15.xx, 5.16.xx 1 Introduction This PA-DSS Implementation Guide contains information for proper use of the paypoint application. Verifone Norway AS does not possess the authority to state that a merchant may be deemed “PCI Compliant” if information contained within this document is followed. Each merchant is responsible for creating a PCI-compliant environment. The purpose of this guide is to provide the information needed during installation and operation of the paypoint application in a manner that will support a merchant’s PCI DSS compliance efforts. 1.1 Audience The PA-DSS implementation guide must be read and understood by terminal operators including resellers, ECR integrators, support organizations and the merchant controlling the terminal. The guide should be used by assessors conducting onsite reviews and for merchants who must validate their compliance with the PCI DSS requirements. This implementation guide is reviewed annually and updated if needed due to changes in paypoint or the PCI requirements. Latest version is always made available on www.verifone.no and information about updates are sent in the release notes. 1.2 Payment Card Industry (PCI) Security Standard Council The PCI Security Standards Council is an open global forum, that is responsible for the development, management, education, and awareness of the PCI Security Standards, including the Data Security Standard (PCI DSS), Payment Application Data Security Standard (PA-DSS), and PIN Transaction Security (PTS) requirements. 1.3 PCI DSS Secure payment applications such as paypoint must be run in a secure environment. -

Navigating the Emv Implementation Process

PARTNERING FOR SUCCESS: NAVIGATING THE EMV IMPLEMENTATION PROCESS A Mercator Advisory Group Research Brief Sponsored by Moneris Solutions November 2014 Partnering for Success: Navigating the EMV ImplementationProcess A Mercator Advisory Group Research Brief Sponsored by Moneris Solutions Contents The EMV Standard .............................................................................................................................3 Reducing Counterfeit Card Fraud .......................................................................................................... 3 Reducing Card Theft Fraud .................................................................................................................... 3 Chip and PIN vs. Chip and Signature ...................................................................................................... 3 Card Network EMV Road Maps ............................................................................................................. 4 Outlook: EMV Adoption in the United States ......................................................................................5 Credit Card Issuance .............................................................................................................................. 5 Debit Card Issuance ............................................................................................................................... 6 Acceptance ........................................................................................................................................... -

To Consult DPQ/Moneris Preferred Pricing

Preferred Rates For Your Business Les Dentistes propriétaires du Québec (DPQ) and Moneris® are pleased to introduce preferred card payment processing rates for your business.† Moneris Transaction 1 Interac Per Transaction Rate Card Type * Assessment Fee Interchange Fee Fee Debit Card $0.040 VISA 0.10% 0.09% Foreign Assessment Fee (VISA) of 0.40% will apply to all gross foreign sales dollar volume processed. Card Brand Fee (Interac) of $0.0085 will apply to each Interac transaction. An Interac fee of $0.035 Mastercard 0.10% 0.08% per transaction will apply to each Interac Flash® (contactless) transaction. Foreign Assessment Fee (Mastercard) of 0.60% will apply to all gross foreign sales dollar volume processed. For more information about the applicable Discover 0.10% 0.063% Interchange rates, Foreign Assessment Fee (Discover) of 0.40% will apply to all gross foreign sales dollar volume processed. please visit moneris.com/interchange POS Solution(s) Rates Union Pay 0.10% 0.1% Standalone $22.00/month Foreign Assessment Fee (UnionPay) of 0.10% will apply to all gross foreign sales dollar volume processed. PIN Pad $16.00/month Visa Debit 0.10% Short Range Wireless $45.00/month Debit MasterCard 0.10% $50.00/month * You agree that you are responsible for the fulfillment of any increase imposed by the Long Range Wireless (plus $75.00 one time activation fee) Card Brand and any fees, fines, penalties, or assessments levied by the Card Brands on us or our parent banks, RBC and BMO, in connection with the processing of your transactions. -

PCI PIN Transaction Security (PTS) Point of Interaction (POI)

Payment Card Industry (PCI) PIN Transaction Security (PTS) Point of Interaction (POI) Modular Security Requirements Version 4.0 June 2013 Document Changes Date Version Description February 2010 3.x RFC version April 2010 3.0 Public release October 2011 3.1 Clarifications and errata, updates for non-PIN POIs, encrypting card readers February 2013 4.x RFC version June 2013 4.0 Public release Payment Card Industry PTS POI Security Requirements v4.0 June 2013 Copyright 2013 PCI Security Standards Council LLC Page 1 Table of Contents Document Changes ................................................................................................................. 1 About This Document .............................................................................................................. 4 Purpose .................................................................................................................................. 4 Scope of the Document .......................................................................................................... 4 Main Differences from Previous Version ................................................................................. 5 PTS Approval Modules Selection ........................................................................................... 6 Foreword .................................................................................................................................. 7 Evaluation Domains ............................................................................................................... -

2008 Annual Report to Shareholders

191ST ANNUAL REPORT 2008 Defining great customer experience I value a clear plan for the retirement I want. I appreciate a bank that can help my company in good times and bad. Who will explain all my mortgage options so that I actually understand? Thanks for giving me the advice that makes sense for me. Defining great customer experience begins with making sense of it all. BMO’s vision – to be the bank that defines great customer experience – galvanizes our organization and encourages every one of our 37,000 employees to help us succeed. In everything we do, we define great customer experience. We do so by helping our customers make sense of their financial lives, and by bringing clarity to the complexities of money. BMO gratefully acknowledges our customers who so generously gave their time and portraits to this annual report. Adolphe A. Tinling Linda Knight Scott Saxberg Maria Monreal-Cameron President and Principal Designer CEO, President and CEO, President and CEO, Adolphe Anthony T. Design CarePartners Crescent Point Energy Trust Hispanic Chamber of Commerce International and Associates Waterloo, Ontario Calgary, Alberta of Wisconsin Montreal, Quebec Milwaukee, Wisconsin Who We Are A Canadian-based North American bank, established in 1817, BMO® Financial Group is highly diversified. We work with millions of personal, commercial, corporate and institutional customers through our operating groups: Personal and Commercial Banking Canada, Personal and Commercial Banking U.S., Private Client Group and BMO Capital Markets. Our 37,000 employees are dedicated to making BMO the bank that defines great customer experience. Our approach is relationship-driven. -

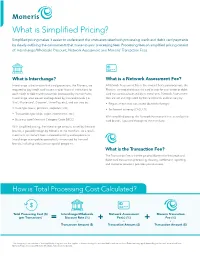

What Is Simplified Pricing?

What is Simplified Pricing? Simplified pricing makes it easier to understand the costs associated with processing credit and debit card payments by clearly outlining the components that make up your processing fees. Processing fees on simplified pricing consist of: Interchange/Wholesale Discount, Network Assessment and Moneris® Transaction Fees. What is Interchange? What is a Network Assessment Fee? Interchange is the amount that card processors, like Moneris, are A Network Assessment Fee is the amount that card processors, like required to pay credit card issuers and/or financial institutions for Moneris, are required to pay the card brands for each credit or debit each credit or debit card transaction processed by its merchants. card transaction processed by its merchants. Network Assessment Interchange rates are set and regulated by the card brands (i.e. fees are set and regulated by the card brands and can vary by: ® ® ® Visa , Mastercard , Discover , UnionPay, etc.), and can vary by: • Region where card was issued (domestic/foreign) • Card type (basic, premium, corporate, etc.) • Settlement currency (CAD, US) • Transaction type (chip, swipe, ecommerce, etc.) With simplified pricing, the Network Assessment Fee, as set by the • Business type/Merchant Category Code (MCC) card brands, is passed through to the merchant. With simplified pricing, the interchange amount, as set by the card brands, is passed through by Moneris to the merchant. As a result, merchants will benefit from increased visibility and exposure to interchange rate updates periodically announced by the card brands, including reductions or special programs. What is the Transaction Fee? The Transaction Fee is the fee paid to Moneris for the credit and debit card transaction processing, clearing, settlement, reporting and customer service it provides your business. -

For Apple® Ipad®, Iphone® and Ipod Touch®

For Apple® iPad®, iPhone® and iPod touch® (11/17) For more information and assistance: Web: getpayd.com/paydpro/support Email: [email protected] Toll-free: 1-855-423-PAYD (7293) Record your Moneris® merchant ID here: __________________________________________ Contents Introduction ................................................................................................ 6 Before you get started .............................................................................. 7 Activating your PAYD Pro store .............................................................. 8 Setting up the PAYD App on your mobile device .............................. 9 Downloading and installing the PAYD App from the App Store SM 10 Setting up the PAYD PIN Pad ................................................................. 11 Pairing a new PAYD PIN Pad with your mobile device 12 Pairing an initialized PAYD PIN Pad with a different mobile device 19 Pairing a replacement PAYD PIN Pad with your mobile device 22 Other PAYD PIN Pad settings 24 Changing an initialized PAYD PIN Pad's default language 24 Bluetooth pairing in Legacy mode 26 Ready to use the PAYD App? 30 Optional features ..................................................................................... 31 Setting the transaction details level 31 Setting a default payment device 32 1 Enabling Pre-Authorizations 32 Enabling tip prompting 33 Setting a tax rate 34 Location-mapping transactions 35 Viewing a location map 35 Setting a quick PIN for sign-in 36 Pre-filling the employee ID/store ID at -

View PIN Pad Security Best Practices

PIN Pad Security Best Practices v2 PIN Pad Security Best Practices © Copyright, VeriFone, 2008 PIN Pad Security Best Practices v2 Introduction The payment industry and card associations adopted PED and PCI PED requirements because of concerns that sophisticated criminal organizations may have the resources to tamper with PED terminals to install a bug and collect private card data. In Pre PED devices, security features were left to each vendor to determine. The more recently adopted Visa PED and PCI PED requirements provide standardized security features that make tampering progressively more difficult. We are seeing an increase in criminal organizations targeting the less secure pre PED terminals by installing bugs to collect private credit card and debit information. In these cases, the criminal organizations are inserting a bug into an in-place device or obtaining the same terminal model that a retailer uses, installing a bug, and then substituting the tampered device for the retailer's terminals. They then either come back to retrieve these terminals to obtain the stolen information, or in some cases, the tampered terminals send the information to another computer via wireless communications. Due to repeated targeting of pre PED PIN pads and payment terminals, VeriFone has developed the following PIN Pad Security Best Practices. These best practices first enable a retailer to determine if any existing terminals have been tampered with, and second make tampering much more difficult by implementing a comprehensive set of security controls to prevent tampering and more quickly become aware if tampering has occurred. This document details the PIN Pad Security Best Practices from a sound security perspective to minimize fraud through education, routine inspection, vendor management, and prompt action. -

BMO Financial Group Reports Third Quarter 2018 Results

BMO Financial Group Reports Third Quarter 2018 Results REPORT TO SHAREHOLDERS Financial Results Highlights Third Quarter 2018 Compared With Third Quarter 2017: • Net income of $1,536 million, up 11%; adjusted net income1 of $1,565 million, up 14% • EPS2 of $2.31, up 13%; adjusted EPS1,2 of $2.36, up 16% • ROE of 14.7%, up from 13.4%; adjusted ROE1 of 15.0%, up from 13.3% • Provision for credit losses3 (PCL) of $186 million compared with $202 million on an adjusted basis in the prior year and $126 million on a reported basis; prior year reported provision for credit losses includes a decrease in the collective allowance of $76 million pre-tax • Common Equity Tier 1 Ratio of 11.4% Year-to-Date 2018 Compared With Year-to-Date 2017: • Net income of $3,755 million, down 9%, reflecting the revaluation of our U.S. net deferred tax asset4 and a restructuring charge in the current year5 and a net gain6 in the prior year; adjusted net income1 of $4,450 million, up 6% • EPS2,4,5 of $5.59, down 8%; adjusted EPS1,2 of $6.67, up 7% • ROE of 12.3%, compared with 13.7%; adjusted ROE1 of 14.6%, up from 13.9% • Provision for credit losses of $487 million3 compared with $620 million on an adjusted basis and $544 million on a reported basis Toronto, August 28, 2018 – For the third quarter ended July 31, 2018, BMO Financial Group recorded net income of $1,536 million or $2.31 per share on a reported basis, and net income of $1,565 million or $2.36 per share on an adjusted basis. -

Quick Reference Booklet 11 August 2020

Quick Reference Booklet 11 August 2020 QR Summary of Changes, 11 August 2020 Summary of Changes, 11 August 2020 This document reflects updates effective since the 15 October 2019 version. Table 1: Descriptions of Changes Description of Change Where to Look Chapter 3—Card Acceptor Business Codes Card Acceptor Business (CAB) Programs and (MCCs) Descriptions Updated country-specific CAB program to include Throughout AUS4, Australia transit 4. Added Macedonia to MCC 9406. MCC 9406—Government-owned Lottery (Specific Countries) Added MCC 9406 Government-owned Lottery Card Acceptor Business Codes (MCCs)— (Specific Countries) to All Transaction Category Transaction Category Codes Codes. Removed vending machines from MCC 5499. MCC 5499—Miscellaneous Food Stores— Convenience Stores, Markets, Specialty Stores Added P for MCC 9399 and MCC 7800. Removed Card Acceptor Business Codes (MCCs)— note in MCC Description. Abbreviated Removed sentence: “This MCC may also be used MCC 9399—Government Services—not to identify U.S. state lottery ticket sales by elsewhere classified merchants properly registered with Mastercard as set forth in section 9.4.5 of the Security Rules and Proceduresmanual.” Added MCC—Electric Vehicle Charging. MCC 5552—Electric Vehicle Charging Added Card Acceptor Business Segment codes for Card Acceptor Business (CAB) Programs and Uruguay. Descriptions Added Card Acceptor Business program, MON2, Throughout to MCC 4829 and MCC 6540. Added 2021 holiday schedule Holiday Processing Schedule ©1990–©2020 Mastercard. Proprietary. All rights reserved. Quick Reference Booklet • 11 August 2020 2 Contents Contents Summary of Changes, 11 August 2020.............................................................2 Chapter 1: Holiday Processing Schedule........................................................ 12 Overview Settlement U.S. Dollar Holiday Schedule............................................................13 Settlement Holidays........................................................................................................ -

A Guide to EMV Chip Technology November 2014

EMVCo, LLC Version 2.0 A Guide to EMV Chip Technology November 2014 A Guide to EMV Chip Technology Version 2.0 November 2014 - 1 - Copyright © 2014 EMVCo, LLC. All rights reserved. EMVCo, LLC Version 2.0 A Guide to EMV Chip Technology November 2014 Table of Contents TABLE OF CONTENTS .................................................................................................................. 2 LIST OF FIGURES .......................................................................................................................... 3 1 INTRODUCTION ................................................................................................................ 4 1.1 Purpose .......................................................................................................................... 4 1.2 References ..................................................................................................................... 4 2 BACKGROUND ................................................................................................................. 5 2.1 What are the EMV Chip Specifications? ........................................................................ 5 2.2 Why EMV Chip Technology? ......................................................................................... 6 3 THE HISTORY OF THE EMV CHIP SPECIFICATIONS ................................................... 8 3.1 Timeline .......................................................................................................................... 8 3.1.1 The Need -

What Is Simplified Pricing?

What is Simplified Pricing? Simplified pricing makes it easier to understand the costs associated with processing credit and debit card payments by clearly outlining the components that make up your processing fees. Processing fees on simplified pricing consist of: Interchange/Wholesale Discount, Network Assessment and Moneris® Transaction Fees. What is Interchange? What is a Network Assessment Fee? Interchange is the amount that card processors, like Moneris, are A Network Assessment Fee is the amount that card processors, required to pay credit card issuers and/or financial institutions for like Moneris, are required to pay the card brands for each credit or each credit or debit card transaction processed by its merchants. debit card transaction processed by its merchants. Network Interchange rates are set and regulated by the card brands (i.e. Assessment fees are set and regulated by the card brands and can Visa®, Mastercard®, Discover®, UnionPay, etc.), and can vary by: vary by: • Card type (basic, premium, corporate, etc.) • Region where card was issued (domestic/foreign) • Transaction type (chip, swipe, ecommerce, etc.) • Settlement currency (CAD, US) • Business type/Merchant Category Code (MCC) With simplified pricing, the Network Assessment Fee, as set by With simplified pricing, the interchange amount, as set by the the card brands, is passed through to the merchant. card brands, is passed through by Moneris to the merchant. As a result, merchants will benefit from increased visibility and exposure to interchange rate updates periodically announced by the card brands, including reductions or special programs. What is the Transaction Fee? The Transaction Fee is the fee paid to Moneris for the credit and debit card transaction processing, clearing, settlement, reporting and customer service it provides your business.