Profitability Analysis of Mahindra & Mahindra Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Merger of Tech Mahindra and Satyam Computer Services Ltd. with Special Reference to HR Issues

IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X, p-ISSN: 2319-7668 PP 03-06 www.iosrjournals.org Merger of Tech Mahindra and Satyam Computer Services Ltd. with special reference to HR Issues Rangana Maitra1, M. Phil (Management), M.B.A (NMIMS), M.A. (English Literature), P.G. Diploma in Personnel Management & Ms. Mayuri Asamwar 2, 1Associate Professor,IES’ Management College and Research Centre, Mumbai 2MMS, IES’ Management College and Research Centre, Mumbai Abstract: Satyam Computer Services Ltd is an Indian IT services company based in Hyderabad, India. Tech Mahindra which was ranked #5 in India's software services firms and overall #161 in Fortune India 500 list for 2011, is a is a part of Mahindra Group conglomerate with headquartered at Pune, India. Tech Mahindra Limited is a leading global systems integrator and business transformation consulting organization, focused primarily on the telecommunications industry. Satyam unveiled its new brand identity Mahindra Satyam subsequent to its takeover by the Mahindra Group's IT arm on 13 April 2009. On June 24, 2013 Tech Mahindra and Mahindra Satyam merging process completed and the name of the parent company was retained for the merged entity with a new Logo and motto. Merger was delayed due to various disputes both in India and abroad. There were quite many problems in the areas of legal and judicial issues, diverse expertise of the merged entities and also the culture between two companies. All these problems were successfully handled by the companies even while working is virtually integrated companies before the High court clearance for the merger. -

Fundamental Analysis: Tata Consultancy Services Limited (TCS)

Fundamental Analysis: Tata Consultancy Services Limited (TCS) May 15, 2020 ─ Ayan Banerjee Roll No. 16EC8020 Stock Market and Investment Management (MS842) Assignment Part-I Company Background and Product/Services Tata Consultancy Services Limited (TCS) is the largest Indian multinational information technology (IT) service and consulting company, and is headquartered in Mumbai, Maharashtra, India. It is a subsidiary of Tata Group and operates in 149 locations across 46 countries. TCS is the largest Indian company by market capitalization. Tata consultancy services is now placed among the most valuable IT services brands worldwide. It is the world's largest IT services provider. In 2018, it is ranked 11th on the Fortune India 500 list. In April 2018, TCS became the first Indian IT company to reach $100 billion market capitalization (this makes it a large cap company), and second Indian company ever (after Reliance Industries achieved it in 2007) after its market capitalization stood at ₹6,79,332.81 crores ($102.6 billion) on the BSE (formerly Bombay Stock Exchange). Sales Break up Net sales breakdown by activity – IT services (98.7%): consulting and engineering services, solutions and systems integration, management applications development, outsourcing services, etc.; Sale of IT equipment and software licenses (1.3%) Net sales break down by market – Sales Breakdown by Activity Bank-financial services insurance (BFSI) (30.5%) Retail and consumer packaged goods (15.2%) Communication and media (7.0%) Sales of IT Equipme Manufacturing industry (9.9%) nt & Life sciences and healthcare (8.3%) Software Licenses Technology and services (8.6%) and, 1% Others (20.5%). Net sales are distributed geographically as follows – India (5.7%), Americas (52.3%), Europe (30.6%) and, Others (11.4%). -

Mahindra Ei Ileal Lint

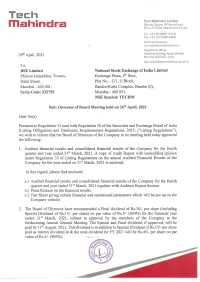

Tech 7 Mahindra ei ilealL i n t Pune 411004, Maharashtra, India Tel. +91 206601 8100 Fax. +91 20 2542 4466 techmahindra.com [email protected] Registered Office: th ¥ Gateway Building, Apoilo Bunder 26% April, 2021 Mumbai 400 001, India CIN L64200MH1 S86PLC041370 To, BSE Limited National Stock Exchange of India Limited Phiroze Jeejeebhoy Towers, Exchange Plaza, 5" floor, Dalal Street, Plot No. - C/1, G Block, Mumbai - 400 001. Bandra-Kurla Complex, Bandra (E), Scrip Code: 532755 Mumbai - 400 051. NSE Symbol: TECHM Sub: Outcome of Board Meeting held on 26" April, 2021 Dear Sir(s) Pursuant to Regulation 33 read with Regulation 30 of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, (“Listing Regulations”), we wish to inform that the Board of Directors of the Company in its meeting held today approved the following: 1. Audited financial results and consolidated financial results of the Company for the fourth quarter and year ended 31% March, 2021. A copy of Audit Report with unmodified opinion under Regulation 33 of Listing Regulations on the annual Audited Financial Results of the Company for the year ended on 31* March, 2021 is enclosed. In this regard, please find enclosed: a.) Audited financial results and consolidated financial results of the Company for the fourth quarter and year ended 31*' March, 2021 together with Auditors Report thereon. b.) Press Release on the financial results. c.) Fact Sheet giving certain financial and operational parameters which will be put up on the Company website. 2. The Board of Directors have recommended a Final dividend of Rs.30/- per share (including Special Dividend of Rs.15/- per share) on par value of Rs.5/- (600%) for the financial year ended 31 March, 2021, subject to approval by the members of the Company at the forthcoming Annual General Meeting. -

Issue XVI – June 2018

Dear Friends, As we enter into the new financial year FY 19, I take this opportunity to acknowledge the support of our Customers & JV Partners as well as appreciate the relentless efforts of each member of UNO MINDA faily. Because of your concerted efforts our overall performance throughout the year has been phenomenal. Overall, it has been a year of spectacular all-round achievements. Corporate News A proud highlight of 2017-18 is that MIL has improved its ranking UNO MINDA rolls out The New Vision in Fortune India 500 listing which The UNO MINDA Management has rolled out a new is testimony to our remarkable Vision along with the Goals FY 2024-25 in December Read More... presence in the Automotive sector and a unique brand proposition for UNO MINDA. We are focused on Innovation Corner further building our brand value Minda Nabtesco a Joint Venture Company between UNO and make UNO MINDA Group MINDA Group and Nabtesco Automotive Corporation, among the best places to work. Japan has developed a Distribution Read More... As we set out to achieve our new vision and realize our near term UNO Minda in Events goals , we are geared up to take new challenges and make most of UNO MINDA participates in ACMA Value Chain the opportunities that come our Summit, Gujarat way. We have established a strong Read More... value system and a well rooted work culture in the welfare of our International News workforce. Ford Visit to Clarton Horn, Spain Juan R. Sendra ( North Africa Purchasing Office Our vision is “To be a Sustainable Supervisor,FORD) has visited Clarton Horn facility Global Organization that enhances Read More.. -

A Critical Study on Business Strategies of TCS Ltd

Advances in Information Technology, Management, Social Sciences and Education December 2018 ISBN No.: 978-81-938040-8-7 Paper 15 A Critical Study on Business Strategies of TCS Ltd. Sheikh Mohammed Arfan I Year MCA, College of Computer & Information Sciences, Srinivas University, Mangalore, Karnataka, India. E-Mail: [email protected] Abstract: TataConsultancyServicesLimited(TCS)isanIndianmulti-nationalInformationTechnology (IT)service,consultingcompanyheadquarteredinMumbai,Maharashtrastate.Itisapartof theTataGroupandoperatesin46countrieswithoverfourlacksemployee.TCSisoneof India‘s largest companies by market capitalization. TCS is now placed among the most valuableITservicesbrandsintheworldwidenation.TCSLimitedwasfoundedororganized in1968bythedivisionofTataSonsLimited.TSChadearlycontractsincludedpunchedcard services to sister‘s company TISCO (now Tata Steel), working on an Inter-Branch reconciliation System for the Central Bank of India and providing bureau services to Unit TrustofIndia.In1975,TCSdeliveredadepositoryelectronicandtradingsystemiscalled SECOMfortheSwisscompanySISSegaInterSettle(Dutch).TCSisalsodevelopedSystem XfortheCanadianDepositorySystemandautomatedtheJohannesburgStockExchange.Itis associated with a Swiss partner, TKS Teknosoft, which it later acquired. In 1980, TCS established India's first dedicated software research and development center, the Tata ResearchDevelopmentandDesignCentre(TRDDC)inPune.In1981,itestablishedIndia's firstclient-dedicatedoffshoredevelopmentcenter,setupforclientsTandem.On25August 2004,TCSbecameaPubliclyListedCompany.In2015,TCSisranked64thoverallinthe -

“An Analysis of Increase in Volume of Payroll Queries and Streamlining the Payroll Process”

“An Analysis of Increase in Volume of Payroll Queries and Streamlining the Payroll Process” INTERNSHIP REPORT Compiled by: Dennis Joseph Koshy (50) ACKNOWLEDGEMENT First and foremost we offer our sincere gratitude to our project manager, Suresh SR, (Associate Vice President & Lead HR Operations (Global Payroll)) who gave us the opportunity to work with his team on this project. He supported us throughout our project with his patience and knowledge whilst giving us the liberty to work in our own way. We are grateful to Saraswathy MS (Senior Manager - Global Payroll and International Transfers), for her constant encouragement, guidance and support throughout our project. We would also like to acknowledge the valuable inputs that she provided which helped us to develop a better understanding of the entire payroll process. We wish to express our deep sense of gratitude to Fanny Florence (Senior Officer - HR Global Payroll), for her timely guidance and useful suggestions, which helped us in carrying out the project work. Sincere thanks to Shalom Thomas (HR Business Partner–Corporate Support) and Julie John (Assistant Manager-PMO) for their timely guidance and valuable assistance in the conduct of our project work. I would like to thank Prof. J. Philip, President, XIME for instituting the Summer Internship Programme (SIP) which has helped us prepare better for corporate life. I also thank Prof. Reji Mathew, Dean, XIME for his support. I extend my warm gratitude to Prof. Binu Modoor, Associate Dean, XIME and my Project guide for his time, encouragement and able guidance. Finally, yet importantly, we would like to express our heartfelt thanks to our beloved parents, friends and the entire payroll team for their help and wishes for the successful completion of this project. -

Chapter 1 a Brief History of Risk and Return

STOCK ANALYSIS OF COMPUTER SOFTWARE COMPANIES OF INDIA TATA CONSULTANCY SERVICES (TCS) Company founded on 1968 by J.R.D. Tata which specializes in IT services and consulting. Natarajan Chandrashekaran is the current CEO and MD of the company. th It is ranked 40 by Forbes in the most innovative companies of the world list. Its is the top company in India by market capitalization with market cap of Rs.489,006.23 crores. TCS is recognized as the leader in independent software testing by Everest Group. TCS has branches in 38 countries including India. th It’s the world’s 10 largest IT service provider. TCS contd. Quarterly results of TCS are as follows (figures in Rs cr) Jun’14 Mar’14 Dec’13 Sep’13 Jun’13 Sales 17,438.43 16,893.91 16,692.65 16,1607.72 13,944.08 Operating 5,488.21 5,565.04 5,779.19 5,748.45 4,169.83 profit Interest 3.73 4.55 4.00 9.83 5.02 Gross profit 6,283.44 6,246.38 6,428.32 7,252.25 4,439.89 EPS(Rs.) 26.02 23.63 24.39 28.63 16.85 Dividend(%) 400 400 July April 2000 4000 Jan Oct Predictions based on past data of TCS INFOSYS Company founded on 1981 by N.R. Narayana Murthy and his friends which provides business consulting, IT, software engineering and outsourcing services. Vishal Sikka is the current CEO and MD of the company. rd It is the 3 largest India based IT services company by 2014 revenues and 5th largest employer in the US. -

Daily News Monitor: 2 December 2020

Daily News Monitor: 2 December 2020 1. Reliance Industries tops Fortune India-500 list second year in a row Source: Business Standard (Link) Mukesh Ambani-led Reliance Industries has topped the Fortune India-500 list for the second straight year, accounting for seven per cent of cumulative revenues and 11 per cent profit of the companies featured. Last year, RIL pipped public sector Indian Oil Corporation to make it to the top slot for the first time. The Fortune India 500 list is based on revenue and the figures this year pertain to fiscal year 2019-2020. This year, ICICI Bank, ranked nine and Larsen & Toubro at 10 made it to the top 10, as Coal India and Tata Steel slipped out; Tata Steel had ranked eighth on the 2019 list and Coal India ninth. The largest companies continued to account for bulk of the cumulative revenues of the 500 companies. The list showed 38 companies clocking revenues of over Rs 50,000 crore each, together accounting for nearly 60 per cent of the total revenues this year, Fortune India said. 2. OECD cuts India's FY21 GDP contraction rate to 9.9% from 10.2% earlier Source: Business Standard (Link) The Organization for Economic Co-operation and Development (OECD) has raised prospects of India’s economy by pegging contraction at 9.9 per cent, against 10.2 per cent it projected in September. It forecast that the economy would rebound to 8 per cent in the next fiscal year and 5 per cent a year later, but gross domestic product (GDP) loss would be substantial. -

Nava Bharat Ventures Featured in Fortune

·······~----- SPECIAL QUARTERLY ISSUE •• Some of the world's most i1 Containers release applications from dependencies & give 11 DEC. 2018·111 MARCH 2020 • FORTUNIINDIA.CDN 8U88CRIBER'S COPY NOT FOR SALE entirely new business mode your developers the agility to build lighter, portable IND IA . applications, faster. Red Hat helps untie constn helping turn IT into a transl Spur your digital transformation with the right co nt ainer platform Red Hat can help you choose. ?1' ,~~ -~ !'f,::_· ' · Create a hybrid cloud architecture . ~.. - Partner with a Red Hat cons For more details, email mar NOlA'S LARGEST CORPORATIONS THE WEALTH CREATORS + CIVETS 100 THE LISTS INDIA'S LARGEST CORPORATIONS From ~38 , 16 , 239 crore in 2010, revenu es of FORTUNE IND IA 500 compan ies have increased at a compound annual growth rate (CAGR] of 9.17% to ~ 91,79,L.tt.t8 crore in 2019- which is nearly 65% of India's gross domestic product. But profits went up by just 3. 25% CAGR, from ~3 .30, 8 2LJ crore in 2010 to ~ t.t . 55 , 293 cro re in 2019. On the other hand, employee co sts ros e at a CAGR of 10.12% to ~ 8.86, 3 83 crore in 2019, from ~3 . 3 8,033 crore in 2010. RANK COMPANY CITY REVENUE NET OPERATING PROFIT ASSETS NET WORTH PROFIT AS % OF EQUITY DIVIDEND EMPLOYEE COST INCOME YoY YoY YoY YoY YoY Net YoY YoY lncorpo- chg( %) ~ crore Rank ch g(%) ~ crore Rank chg(%) ~ cro re 2018 ~ crore ch g( %) ~ crore Rank chg(%) Revenue Assets worth ~ crore Rank chg(%) ~ crore Rank chg (%) rationy ear Industry Own ership Ql.SO 5,6 7,135.00 qq_8o 39,588.00 1 9. -

Indian Companies in Belgium

Indian Companies in Belgium By Gauri Khandekar 1 About the author: Gauri Khandekar is Researcher and Head of EU-Asia Programme at Think Tank FRIDE, based in Brussels. COPYRIGHT C 2014 EICC, ALL RIGHTS RESERVED Disclaimer: Although the Author and EICC have used their best efforts in the preparation of the report, they assume no responsibility for any errors or omissions nor any liability for damages resulting from the use of or reliance on information contained in the report. 2 Indian Companies in Belgium Antwerp Zeebrugge Mechelen Tessenderlo Gent Brussels Liège Lillois-Witterzée Verviers Namur 3 Contents Preface 13. Gemini Corporation NV 14. Avantha – The Global Green Company – Intergaarden NV Foreword 15. Godrej Group – LVD Godrej InfoTech NV India in Belgium – Overview of Bilateral Relations 16. GSC Glass ltd. – GSC Starconstruct 17. Havells India ltd. – Havells Sylvania Belgium BVBA Indian Companies in Belgium 18. ICICI Bank 19. IM Gears Flanders 20. Jasch Industries ltd. –Jasch Europe 1. Aditya Birla Carbon – ACB Belgium BVBA 21. JBF Global Europe BVBA 2. Allcargo Logistics ltd. – ECU Line 22. Jubilant Pharmaceuticals SA 3. Ashapura Group of Industries – Ashapura Midgulf NV 23. Meghmani Organics ltd. – Meghmani Europe BVBA 4. Autotech Industries BVBA 24. MphasiS Unleash the Next 5. Bank of India 25. NIIT Technologies ltd. 6. C&S Electric ltd. – Eta-com B 26. Piramal Glass ltd. 7. CEAT ltd. – Altura 27. Punjab Chemical and Crop Protection ltd. – SD Agchem 8. Cipla ltd. – Cipla Europe (Europe) NV 9. Crompton Greaves ltd. – CG Power Systems Belgium NV 28. Rain Industries ltd. – Rütgers group 10. Dr D Y Patil Educational Enterprises Private ltd. -

NOTICE REGISTRATION & CAMPUS DETAIL- MPHASIS Eligible Students Must Register in the Given Below Link Before 6Th April 2019

NOTICE REGISTRATION & CAMPUS DETAIL- MPHASIS Eligible students must register in the given below link before 6th April 2019: https://tinyurl.com/Mphasis-2019 About the company: Mphasis is an IT services company based in Bangalore, India. The company provides infrastructure technology and applications outsourcing services, as well as architecture guidance, application development and integration, and application management services. It serves financial services, telecom, logistics, and technology industries. Mphasis was ranked #7 in India IT companies and overall #165 by Fortune India 500 in 2011.[2] In April 2016, Hewlett Packard Enterprise sold the majority of its stake in Mphasis to Blackstone Group LP for around $USD 1 billion. Mphasis has been a leading provider of core IT services to global marquee customers for over 25 years; bringing in best-of-class expertise in the foundational services of Application Development and Maintenance, Infrastructure Services, and Business Process Services. To this existing suite of services, Mphasis has been nimble and agile in integrating and building specialization to enable future-proofing of the organization as well as its customers. Mphasis enables customers re-imagine their digital future by applying a unique formula of cloud migration and cognitive technology, to modernize and power the legacy systems to timeless computing. Mphasis’ array of algorithm-based technologies seamlessly combines Robotic Process Automation, Predictive Analytics, Cloud, Artificial Intelligence, and Blockchain, surrounding legacy technologies with domain expertise and modernization. For more details, please login our website https://www.mphasis.com/ Date: 15th April, 2019 Time: 09:00 am Venue: SVCE, Indore Branches: BE- CS, IT, EC, EEE/EX and MCA- 2019 Batch Locations of work: Pune, Bangalore, Chennai, Mumbai, Hyderabad CTC Details: The selected candidate is eligible for monthly salary of INR 21,000 (Rupees Twenty one thousands including CTC @ INR 1.8 Lakhs per annum and Rupees 6000 monthly allowance). -

Q2 FY2013 Earnings Release

Mindtree Limited (NSE: MINDTREE, BSE: 532819) Earnings release Third quarter ended December 31, 2012 (Q3 FY2013) January 18, 2013 Contents 1. Press Release 3 2. Key Financial Metrics 5 3. Key Ratios 5 4. Key Revenue Metrics 6 5. Effort and Utilization 7 6. Key Customer Metrics 7 7. Key Employee Metrics 8 8. Infrastructure 8 9. Statutory Financials 9 Earnings Conference Call for Analysts / Investors January 18, 2013 (6:30 PM IST) Primary Number: +91 22 6629 0040 Secondary Number: +91 22 3065 0182 (The numbers listed above are universally accessible from all networks and all countries) Toll free numbers: Singapore: 800 101 2045 Hong Kong: 800 964 448 UK: 0 808 101 1573 US: 1 866 746 2133 Replay of conference call available until January 25, 2013 +91 22 3065 1212 (Playback id: 230712#) Transcript will be available on www.mindtree.com after January 23, 2013 © Mindtree Limited 2013 Page 2 of 11 Mindtree’s net profit surges 63% y-o-y in rupee terms; better client mining leads to more $5M and $10M customers Bangalore (India), January 18, 2013: Mindtree Limited, a global information technology solutions company, announced its results today for the third quarter ended December 31, 2012, as approved by its Board of Directors. “Our revenue growth has been satisfactory despite a seasonally weak quarter. We are very pleased that our efforts to reposition and strengthen our business continue to yield good results, as can be seen in our strong profitability improvements. Our expertise led positioning is helping us develop deeper customer relationships and deliver transformative changes for existing and new customers ” said Krishnakumar Natarajan, CEO & Managing Director, Mindtree Limited.