News Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Erasmus Student W0RK Placement

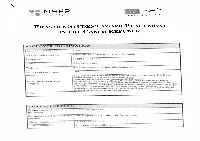

ERAsMus STuDENT W0RK PLAcEMENT IN THE CzEcH REPuBuc EMPLOYER INFORMATION Name of organization Pixmania s.r Address mcl. post cede Trnt 391/5. 60200 Brne, Czech Repuhiic Felephone 00420 543 123 100 mail [email protected] Wehsite \n uaa e; johs pixmania.corn Number cI emplevees 180 Dixons Reta plc s one of ELropes Ieadng electrLcal retaers, The Group trades through L200 stores and online stores, spanning 28 countnes and empIoyng 3650O people. Shert descrption of the Pixmania.com, as a part of Dixons Retail pc., is an European E-taer of company consurner e1ectronc goods. It app{ies innovative market strateges on an nterrational evei, leading te a pan-European presence n 26 countnes and 17 anguages. In order te support ts development in the flagshp markets and increase ts brard-awareness Pixrnanìa would ike to give an opportunty to studentsin vanousf!elds te join our tearn! Other CONTACT DETAILS (rntact persen for this ‘v arernka Modra placei ienl Departmer t and de’enata e i HR Support it Pi\mania [IR D partme ìt h ‘7 Diret tcleohene nun bLr (Ni42( 51 i i 593 E a Idrc \ ned’a i5 pi\ViI e om I)epartrnent I Funetion Transport aceount coordinator Description of activities The Transport Team Is responsible for ensure the quality of tra nsport services ordered by customers. The interna wN be responsibe for foflowing transport issues • Pick Ups (parcels on the way back to Pixmania frorn custorner) • !nvestigations hnquiry of darnaged, Iost parcels or delayed parceR) o Vahdation of Pick Ups with different carriers. -

Dixons Retail Plc a Year of Strong Performance

PR 06/14 7.00am, Thursday, 26 June 2014 DIXONS RETAIL PLC A YEAR OF STRONG PERFORMANCE Dixons Retail plc, one of Europe’s leading specialist multi-channel electrical retail and services companies, today announces preliminary audited results for the financial year ended 30 April 2014. Key highlights Group underlying profit before tax increased by 76% to £166.2 million versus £94.5 million reported last year and up 10% on a restated basis (1), (2). – Further strong progress in the UK & Ireland with underlying operating profits up 24%(1) – Elkjøp delivered another strong year with record sales – Greece delivered an improved performance with some signs of stability returning to the market Another successful year for the Group, delivering on its key objectives: – Firm establishment of a sustainable business in a multi-channel world – Disposals of all non-core operations, leaving the Group with leading positions in all our core markets Proposed merger with Carphone Warehouse announced to develop a leading position across electricals, mobiles and connectivity. – European Commission has confirmed that it has unconditionally cleared the proposed merger Group online sales increased by 16% to £1 billion. Customer service metrics at their highest ever recorded levels in all markets. Return on capital employed of 16.3%, up from 14.9% in the prior year. Group costs reduced by a further £45 million completing the two year £90 million cost reduction initiative. Very strong cash generation with the Group ending the year with net cash increasing to £70.9 million. Financial highlights Total underlying Group sales up 3% at £7.22 billion (2012/13 £7.03 billion) (1). -

Multichannel-Now-Retail-Week.Pdf

Contents Foreword Page 3 Sponsor foreword Page 4 Executive summary Page 5 Chapter 1 Retailers reorganising around the customer Page 8 Structural and operational changes taking place in businesses prove that retailers are using actions, not just words, when it comes to creating genuine cross-channel customer experiences Chapter 2 Property: what lies ahead for stores? Page 14 Changing footfall patterns combined with the cannibalisation of store sales by online channels is polarising the retail property market. But the good news is that retailers realise they must invest in the space they want to keep Chapter 3 Pricing, promotions and marketing in a multichannel world Page 18 In non-food retail in particular, online promotions are creating price differentials between channels. But online marketing channels are allowing retailers to stretch their budgets further Chapter 4 Mobile: the connective tissue between all other channels Page 22 Customers’ desire to use mobiles to support online and offline purchases is evident. Retailers are quickly finding how valuable mobile is as a sales channel and to create seamless journeys between other channels Chapter 5 The last mile for delivery, fulfilment and click and collectPage 27 The fulfilment of web orders is one of the most competitive areas of multichannel retailing. We explain why convenience is winning over pure speed, and how this impacts the premium services being launched Chapter 6 International expansion moves from passive to active Page 31 The first wave of international expansion through ecommerce has caught on. Now retailers are using the data collected from international delivery to further target markets with the most potential Chapter 7 Channel proliferation and the rise of the marketplace Page 35 Complicating matters for retailers is the creation of channels such as mobile, Facebook and international ecommerce. -

Discover Athens, Greece Top 5

Discover Athens, Greece Photo: Anastasios71/Shutterstock.com Of all Europe’s historical capitals, Athens is probably the one that has changed the most in recent years. But even though it has become a modern metropolis, it still retains a good deal of its old small town feel. Here antiquity meets the future, and the ancient monuments mix with a trendier Athens and it is precisely these great contrasts that make the city such a fascinating place to explore.The heart of its historical centre is the Plaka neighbourhood, with narrow streets mingling like a labyrinth where to discover ancient secrets. Anastasios71/Shutterstock.com Top 5 1. Roman Agora During the antiquity, the Agora played a major role as both a marketplace and … 2. National Archaeological Museum The National Archaeological Museum, in Exarchia, is home to 3. The Acropolis and its surround The Parthenon, the temple of Athena, is the major city attraction as well as... Anastasios71/Shutterstock.com 4. Benaki Museum of Greek Culture Benaki is a history museum with Greek art and objects from the 5. Mount Lycabettus Mount Lycabettus (in Greek: Lykavittos, Λυκαβηττός) lies right in the centre... Milan Gonda/Shutterstock.com Athens THE CITY DO & SEE Nick Pavlakis/Shutterstock.com Anastasios71/Shutterstock.com Athens’ heyday was around 400 years BC, that’s Dive in perhaps the most historically rich capital when most of the classical monuments were of Europe and discover its secrets. Athens' past built. During the Byzantine and Turkish eras, the and its landmarks are worldly famous, but the city decayed into just an insignicant little city ofiers much more than the postcards show: village, only to become the capital of it is a vivid city of culture and art, where the newly-liberated Greece in 1833. -

Strategic Retail Management Text and International Cases 3Rd Edition Strategic Retail Management Joachim Zentes • Dirk Morschett • Hanna Schramm-Klein

Joachim Zentes Dirk Morschett Hanna Schramm-Klein Strategic Retail Management Text and International Cases 3rd Edition Strategic Retail Management Joachim Zentes • Dirk Morschett • Hanna Schramm-Klein Strategic Retail Management Text and International Cases 3rd Edition Joachim Zentes Hanna Schramm-Klein FB Wirtschaftswissenschaften, Universität Siegen Universität des Saarlandes Siegen, Germany Saarbrücken, Germany Dirk Morschett Universität Fribourg Fribourg, Switzerland ISBN 978-3-658-10182-4 ISBN 978-3-658-10183-1 (eBook) DOI 10.1007/978-3-658-10183-1 Springer Gabler Library of Congress Control Number: 2016954795 Springer Gabler © Springer Fachmedien Wiesbaden GmbH 2007, 2011, 2017 This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, repro- duction on microfilms or in any other physical way, and transmission or information storage and retrieval, elec- tronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made. -

AUTO RECONCILIATION SERVER • Cost Reduction

Note: This brochure is Customer designed to be Managing critical Dixons Carphone Warehouse Auto printed. You tasks at the entry should test print point is fundamental Region Reconciliation on regular paper to increase Europe to ensure proper productivity and positioning before Challenge – How it started printing on card ensure information stock. • Input of source 100% paper based. Papersoft professional services for Enterprise departments, quality at a lower enterprise shared services – SSC or large BPO providers that • Manage input branches all over the UK and IRL. cost. want to: You may need to • Monthly +1M/documents. • Organize unstructured data. uncheck Scale to • Human based reporting to commissions team and loss Fit Paper in the prevention. • Manage volume peaks. • Register accurate data into ERP´s. Print dialog (in the • Multiple document reconciliation checks such as bank statements, IDs, contract and others. • Meet regulatory target dates. Full Page Slides • External/Internal audit control. dropdown). To speed up implementation • Vendor relation satisfaction. “we took a staged approach. Benefits from initiative • Credibility/Professionalism. Papersoft consulted with us Check your printer • Full process automation. to create a roadmap of the Finance departments that aim to: instructions to • Process standardisation. print double-sided discrete stages and • Approve/Reject internal information. • Compliant and auditable customer info. pages. identified gaps where best • Avoid service cancellation/penalties. Workflow with alerts and action steps on frauds and practices would speed up • • Optimize cash flow. each phase. This approach errors for all branches. To change images allowed us to accelerate on this slide, business transformation and Benefits from Papersoft ecosystem select a picture greatly reduced the About Dixons Carphone Warehouse and delete it. -

Greece Athens University of Economics and Business Fourlis

CFA Institute Research Challenge hosted by CFA Society Greece Athens University of Economics and Business The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and presentation skills of university students. The following report was submitted by a team of university students as part of this annual educational initiative and should not be considered a professional report. Disclosures: Ownership and material conflicts of interest The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report. Receipt of compensation Compensation of the author(s) of this report is not based on investment banking revenue. Position as an officer or a director The author(s), or a member of their household, does not serve as an officer, director, or advisory board member of the subject company. Market making The author(s) does not act as a market maker in the subject company’s securities. Disclaimer The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. -

Appointment of New Group CEO

22 January 2018 Embargoed until 7.00am Appointment of new Group CEO Dixons Carphone plc announces the appointment of Alex Baldock as Group Chief Executive from April 2018, to succeed Sebastian James who has informed the board of his decision to step down around the end of the financial year after six years in the role. Sebastian will be joining Walgreens Boots Alliance later this year. Alex Baldock is currently Group Chief Executive of Shop Direct plc, the UK’s second largest pure-play online retailer, a position which he has held since 2012. Ian Livingston, Chairman of Dixons Carphone plc, said: “Seb has made an outstanding contribution to both the creation and success of Dixons Carphone. It is a much stronger company today than when he became CEO of Dixons Retail in 2012 with revenue, profit and customer satisfaction all substantially higher. The Group is now the market leader in eight countries.” “On behalf of the Board and all our colleagues, I would like to thank Seb for all that he has done over the past six years as CEO of first Dixons Retail and now Dixons Carphone. We wish him every success in his new role.” “The Board and I are delighted to welcome Alex Baldock to the Group. He has an outstanding track record in leading large, complex consumer-facing businesses. He’s led Shop Direct through one of UK Retail’s fastest, most far-reaching and most successful digital transformations, delivering five consecutive years of record financial performance, with strongly rising sales and an almost tenfold increase in profits. -

Continued Strong Online Momentum Despite Covid

20 January 2021 Trading Update for 10 weeks ended 9 January 2021 Continued strong online momentum despite Covid impact • Electricals like-for-like revenue +11% o Highest growth in large screen TVs, smart tech, food preparation, health & beauty and all areas of computing & gaming • UK & Ireland Electricals like-for-like revenue +8% o Online growth +121% o Online market share +6%pts • International like-for-like revenue +14%: Nordics +19%, Greece (13)% o Nordic online sales +97%, Greece online sales +366% o Nordics: Double-digit growth and strong market share gains o Greece: Performance impacted by national lockdown • UK & Ireland Mobile total revenue down (40)% o Sales and cashflow in line with plan given UK standalone Carphone Warehouse store closures last April • Transformation progress: o Omnichannel: Group Electricals online sales +118%. ShopLive 24/7 live video shopping growing strongly o Credit: UK Electricals credit customers grew to 1.4m o Services: Nordic Customer Club grew to over 4.9m members and 50% of Black Friday week sales o Mobile: Restructuring on track, new mobile offer to launch this year Alex Baldock, Group Chief Executive “I’m so grateful to my colleagues. Thanks to their dedication and adaptability in such a testing time, we’ve kept safely providing vital technology to the public, keeping millions of people connected, healthy, productive and entertained. And so we’ve continued to trade strongly, both in the UK and Internationally, while ensuring colleague and customer safety is paramount. We’re winning online, where we’re the biggest and fastest-growing specialist technology retailer in all our markets. -

Dsg International

PROSPECTUS DATED 26 JULY 2010 6JUL201009455162 DSG INTERNATIONAL PLC (to be renamed Dixons Retail plc, subject to shareholder approval) (incorporated in England and Wales under the Companies Act 1985 with registered number 03847921) £150,000,000 8.75 per cent. Guaranteed Notes due 2015 guaranteed by certain subsidiaries of DSG international plc Issue Price: 99.007 per cent. The £150,000,000 8.75 per cent. Guaranteed Notes due 2015 (the ‘‘Notes’’) will be issued by DSG international plc (‘‘DSGi’’ or the ‘‘Issuer’’) (to be renamed Dixons Retail plc, subject to shareholder approval) and will, upon issue, be unconditionally and irrevocably guaranteed (the ‘‘Guarantee’’) on a joint and several basis by DSG International Holdings Limited, DSG Retail Limited, DSG Card Handling Services Limited, Coverplan Insurance Services Limited, DSG International Treasury Management Limited, DSG Overseas Investments Limited, DSG European Investments Limited, DSG Ireland Limited and DSG Retail Ireland Limited (collectively the ‘‘Guarantors’’ and each a ‘‘Guarantor’’). Interest on the Notes is payable on a semi-annual basis in arrear on 1 February and 1 August of each year, beginning on 1 February 2011 save that the last interest payment date will fall on 3 August 2015, as described in ‘‘Terms and Conditions of the Notes—Interest’’. Unless previously redeemed or purchased and cancelled, the Notes will mature on 3 August 2015. The Issuer may purchase all (but not some only) of the Notes at their principal amount outstanding together with interest accrued to (but excluding) the date of such purchase or, as the case may be, redemption, in the event of certain tax changes as described under ‘‘Terms and Conditions of the Notes—Redemption and Purchase—Redemption for Taxation Reasons’’. -

Dixons Retail AR Cover with Spine.Indd

Dixons Retail plc Annual Report and Accounts 2013/14 Annual Report and Accounts 2013/14 www.dixonsretail.com @DixonsRetail Dixons Retail plc Maylands Avenue Hemel Hempstead Hertfordshire HP2 7TG United Kingdom Tel: 0344 800 2030 www.dixonsretail.com “This has been a great year for the Group with some excellent performances across our multi-channel businesses, together with the achievement of a number of important strategic objectives. Our profits are up 76% from those we reported a year ago and up 10% on a restated basis. This not only reflects the fact we have now exited all of our non-core markets, meaning we are now a leader in all our core markets, but is also a testament to the creativity and hard work of our teams. The Group is in robust financial health with further cash generation resulting in a strong net cash position even after the costs incurred in exiting the non-core businesses. Best of all, our customer service metrics have again reached new records. All of this all means that the Group is stronger – both commercially and financially – than it has been for a number of years and we are well positioned to set sail into new waters. I am very excited about the opportunities that the proposed merger with Carphone Warehouse offers for the Group. We will build what I hope will be the first and best truly multi-channel proposition that allows customers not only to buy and experience the explosion of new connected products that are emerging, but to also get the advice, connectivity and services that will allow them to use technology as it should be used – to make their lives better. -

DSG Internationalplc Annualreport and a Ccounts 2006/07 Annual

Annual Report and Accounts 2006/07 Accounts and Report Annual DSG international plc Annual Report and Accounts 2006/07 Financial Highlights Underlying Group sales* Underlying profit before taxation* £million £million 2006/07 7,929.7 2006/07 295.1 Group Overview Group 2005/06 6,984.4 2005/06 311.0 2004/05 6,451.8 2004/05 289.9 2003/04 5,947.3 2003/04 289.8 2002/03 5,294.4 2002/03 251.2 Contents 4 Our Markets 11 Business Performance 19 Customer Service 24 Corporate Responsibility Review 34 Directors’ Report 124 Five Year Record Underlying diluted earnings per share* Dividends per share pence pence 2006/07 10.9 2006/07 8.870 Group Overview Group 2005/06 11.8 2005/06 8.450 2004/05 10.9 2004/05 8.050 2003/04 11.1 2003/04 7.320 2002/03 10.0 2002/03 6.655 *Underlying results exclude the effects of amortisation of acquired intangibles, exceptional asset impairments, net restructuring charges and other one off items, profit on sale of investments, net fair value remeasurements of financial instruments and, where applicable, discontinued operations. Figures for 2006/07, 2005/06 and 2004/05 are presented under International Financial Reporting Standards (IFRS). Figures for 2003/04 and 2002/03 are presented under UK GAAP as previously reported and whilst have been restated to exclude discontinued operations have not been restated for any new UK accounting standards which may now apply. 1 Group Overview 60 Consolidated Financial Statements 1 Financial Highlights 60 Statement of Directors’ Responsibilities 2 Our Brands 61 Independent Auditors’ Report