FAQ - Nasdaq Stockholm 2017-08-07 09:39

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Execution Venues List

Execution Venues List This list should be read in conjunction with the Best Execution policy for Credit Suisse AG (excluding branches and subsidiaries), Credit Suisse (Switzerland) Ltd, Credit Suisse (Luxembourg) S.A, Credit Suisse (Luxembourg) S.A. Zweigniederlassung Österreichand, Neue Aargauer Bank AG published at www.credit-suisse.com/MiFID and https://www.credit-suisse.com/lu/en/private-banking/best-execution.html The Execution Venues1) shown enable the in scope legal entities to obtain on a consistent basis the best possible result for the execution of client orders. Accordingly, where the in scope legal entities may place significant reliance on these Execution Venues. Equity Cash & Exchange Traded Funds Country/Liquidity Pool Execution Venue1) Name MIC Code2) Regulated Markets & 3rd party exchanges Europe Austria Wiener Börse – Official Market WBAH Austria Wiener Börse – Securities Exchange XVIE Austria Wiener Börse XWBO Austria Wiener Börse Dritter Markt WBDM Belgium Euronext Brussels XBRU Belgium Euronext Growth Brussels ALXB Czech Republic Prague Stock Exchange XPRA Cyprus Cyprus Stock Exchange XCYS Denmark NASDAQ Copenhagen XCSE Estonia NASDAQ Tallinn XTAL Finland NASDAQ Helsinki XHEL France EURONEXT Paris XPAR France EURONEXT Growth Paris ALXP Germany Börse Berlin XBER Germany Börse Berlin – Equiduct Trading XEQT Germany Deutsche Börse XFRA Germany Börse Frankfurt Warrants XSCO Germany Börse Hamburg XHAM Germany Börse Düsseldorf XDUS Germany Börse München XMUN Germany Börse Stuttgart XSTU Germany Hannover Stock Exchange XHAN -

Surveillance Stockholm

Surveillance Stockholm Exchange Notice Stockholm 2020-05-18 News for listed companies 8/20 Information from the Surveillance function at Nasdaq Stockholm with regards to amendments to the Act on Temporary Exemptions Following up on the Surveillance update on March 31, 2020, regarding Corona related topics relevant for issuers on Nasdaq Stockholm and Nasdaq First North Growth Market Stockholm, Nasdaq now informs about amendments to the Act (2020:198) on temporary exemptions to facilitate the implementation of corporate and association meetings (the Act on Temporary Exemptions) that came into force today, May 18, 2020. Summary As of today, Swedish companies are temporarily allowed to hold general meetings without any physical participation. According to amendments to the Act on Temporary Exemptions general meetings can be held either by electronic connection in combination with postal voting, or by the shareholders only participating by postal vote. If the general meeting is held by postal vote only, shareholders must also be able to exercise their other rights by post. To apply these temporary exemptions, it must be stated in the notice to the general meeting, entailing that the option to hold the meeting completely without physical participation can be applied by companies that have not yet convene the general meeting, or companies that decide to postpone the general meeting within the time limits set out in applicable law. You can find the Act on Temporary Exemptions (available in Swedish only) – https://www.riksdagen.se/sv/dokument-lagar/dokument/svensk-forfattningssamling/lag-2020198- om-tillfalliga-undantag-for-att_sfs-2020-198 Please be advised that we are available for discussions regarding regulatory and disclosure-related matters. -

Representation Letter from Nasdaq Stockholm

Katten Paternoster House 65 St Paul's Churchyard London, EC4M SAB +44 (0) 20 7776 7620 tel +44 (0) 20 7776 7621 fax www.katten.co.uk [email protected] +44 (0) 20 7776 7625 direct January 15, 2020 Ref No. 385248 00020 CHJ:sh VIA E-MAIL AND FEDERAL EXPRESS Mr. Brett Redfeam Director U.S. Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-7010 United States of America Re: Intent of Nasdaq Stockholm AB to Rely on No-Action Relief for Foreign Options Markets and Their Members That Engage in Familiarization Activities Dear Mr. Redfeam: At the request of our client, Nasdaq Stockholm AB ("Nasdaq"), we are writing to provide you with a notification of Nasdaq's intent to rely on the class no-action relief issued by the Securities and Exchange Commission's ("SEC" or "Commission") Division of Trading and Markets ("Division") for foreign options markets and their members that engage in familiarization activities with certain U.S.-based persons.1 BACKGROUND In the Class Relief, the Division took a no-action position under which a Foreign Options Market2, its Representatives3 and the Foreign Options Market's members, could engage in 1 See LIFFE A&M and Class Relief, SEC No-Action Letter (Jul. 1, 2013) ("Class Relief'). Capitalized terms used herein and not otherwise defined have the meanings given in the Class Relief. Pursuant to the Class Relief, a Foreign Options Market is not required to apply de novo for similar no-action or other relief; it can file with the Division a notice of intent to rely on the Class Relief. -

Nasdaq Stockholm Welcomes Logistea to First North

Nasdaq Stockholm Welcomes Logistea to First North Stockholm, May 8, 2017 — Nasdaq (Nasdaq: NDAQ) announces that the trading in Logistea AB’s shares (short name: LOG) commenced today on Nasdaq First North in Stockholm. Logistea belongs to the financial sector (sub sector: real estate) and is the 35th company to be admitted to trading on Nasdaq’s Nordic markets* in 2017. Logistea is a real estate company that owns and manages the property Örja 1:20, located along the E6 highway in Landskrona, Sweden. The property consists of a logistics terminal and an office building, with a total, rentable area of 42 000 square meters. Its largest tenant is DSV. For more information, please visit www.logistea.se. “We welcome Logistea to Nasdaq First North,” said Adam Kostyál, SVP and Head of European listings at Nasdaq. “We congratulate the company on its listing, and look forward to supporting them with the investor exposure that comes with a Nasdaq First North listing.” Logistea AB has appointed FNCA Sweden AB as the Certified Adviser. *Main markets and Nasdaq First North at Nasdaq Copenhagen, Nasdaq Helsinki, Nasdaq Iceland and Nasdaq Stockholm. About Nasdaq First North Nasdaq First North is regulated as a multilateral trading facility, operated by the different exchanges within Nasdaq Nordic (Nasdaq First North Denmark is regulated as an alternative marketplace). It does not have the legal status as an EU-regulated market. Companies at Nasdaq First North are subject to the rules of Nasdaq First North and not the legal requirements for admission to trading on a regulated market. The risk in such an investment may be higher than on the main market. -

1 Not for Release, Publication Or Distribution in Whole Or

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN THE UNITED STATES, CANADA, AUSTRALIA, SOUTH AFRICA OR JAPAN. Marel: Final Offer Price set at EUR 3.70 per Offer Share Marel hf. (“Marel”), a leading global provider of advanced food processing equipment, systems, software and services to the poultry, meat and fish industries, has set the final price for the shares (the “Offer Shares”) sold in the offering and listing on Euronext Amsterdam (the “Offering) at EUR 3.70 per Offer Share (the “Offer Price”). Listing of and first trading in Marel’s shares (the “Shares”) on an “as-if-and-when-issued/delivered” basis on Euronext Amsterdam commence on Friday 7 June 2019. The Offer Price has been set at EUR 3.70, implying a market capitalisation for Marel of EUR 2.82 billion. The Offering comprises approximately 90.9 million Shares. In addition, Marel has granted a customary Over-allotment Option (as defined and described below) representing approximately 9.1 million Shares. The Offering represents 15% of Marel’s entire share capital, assuming full exercise of the Over-allotment Option. Total offer size amounts to EUR 336.36 million, and will increase to EUR 370 million assuming full exercise of the Over-allotment Option. The Offering was multiple times oversubscribed at the Offer Price with strong demand from both institutional and retail investors. Free-float following completion of the Offering is expected to be 75.0%, and will increase to 75.3% assuming full exercise of the Over-allotment Option. Listing of the Shares and first day of conditional trading on Euronext Amsterdam on an “as-if- and-when-issued/delivered” basis commence on 7 June 2019 under the symbol “MAREL”. -

Final Report Amending ITS on Main Indices and Recognised Exchanges

Final Report Amendment to Commission Implementing Regulation (EU) 2016/1646 11 December 2019 | ESMA70-156-1535 Table of Contents 1 Executive Summary ....................................................................................................... 4 2 Introduction .................................................................................................................... 5 3 Main indices ................................................................................................................... 6 3.1 General approach ................................................................................................... 6 3.2 Analysis ................................................................................................................... 7 3.3 Conclusions............................................................................................................. 8 4 Recognised exchanges .................................................................................................. 9 4.1 General approach ................................................................................................... 9 4.2 Conclusions............................................................................................................. 9 4.2.1 Treatment of third-country exchanges .............................................................. 9 4.2.2 Impact of Brexit ...............................................................................................10 5 Annexes ........................................................................................................................12 -

Iceland's Implementation of the 2030 Agenda for Sustainable Development

June 2019 Iceland's Implementation of the 2030 Agenda for Sustainable Development Voluntary National Review Government of Iceland Prime Minister’s Office Contents PRESS BOX TO GO TO CHAPTER Message from the Prime Minister very Friday at noon, hundreds of young people gather out- side Althingi, Iceland’s Parliament, insisting on radical action against climate change. They are a part of an international Emovement of young people who rightly point out the fact that today’s decisions determine their future. Climate change is a crisis for humanity as a whole; rendering traditional territorial borders meaningless. International collaboration is the only way forward. The Millennium Development Goals, adopted in 2000, were often referred to as “the world’s biggest promise”. They were a global agreement to reduce poverty and human deprivation. And they did. The MDGs lifted more than one billion people out of extreme poverty. The goals provided access to water and sanitation; drove down child mortality; drastically improved maternal health; cut the number of children out of school; and made huge advances in combatting HIV/AIDS and malaria. The Sustainable Development Goals are a bold commitment to finish what has been started. Coinciding with the historic Paris Agreement on climate change, the SDGs are the promise our young people are calling for, of sustainability, equality and wellbeing for all. The SDGs are also an important reminder that sustainable development is not just an issue for faraway places. Each and every one of us has both rights and obligations in this context. While some of the SDGs might feel distant from our daily lives, they encompass everything that makes life worthwhile, such as education, water, peace and equality, to name just a few. -

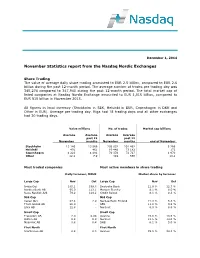

May 2010 Statistics Report from the NASDAQ OMX Nordic Exchanges

December 1, 2014 November Statistics report from the Nasdaq Nordic Exchanges Share Trading The value of average daily share trading amounted to EUR 2.5 billion, compared to EUR 2.6 billion during the past 12-month period. The average number of trades per trading day was 345,274 compared to 347,940 during the past 12-month period. The total market cap of listed companies at Nasdaq Nordic Exchange amounted to EUR 1,015 billion, compared to EUR 915 billion in November 2013. All figures in local currency (Stockholm in SEK, Helsinki in EUR, Copenhagen in DKK and Other in EUR). Average per trading day. Riga had 18 trading days and all other exchanges had 20 trading days. Value millions No. of trades Market cap billions Average Average Average Average past 12 past 12 November months November months end of November Stockholm 13 140 13 566 205 032 201 462 5 266 Helsinki 491 461 69 448 73 182 172 Copenhagen 4 223 4 481 70 376 72 727 1 970 Other 12.1 7.9 419 568 10.1 Most traded companies Most active members in share trading Daily turnover, MEUR Market share by turnover Large Cap Nov Oct Large Cap Nov Oct Nokia Oyj 145.1 189.4 Deutsche Bank 12.9 % 12.7 % Nordea Bank AB 95.0 113.1 Morgan Stanley 8.1 % 8.0 % Novo Nordisk A/S 79.2 129.2 Credit Suisse 8.1 % 8.3 % Mid Cap Mid Cap Vacon Oyj 47.4 2.9 Nordea Bank Finland 21.3 % 5.3 % Thule Group AB 20.0 - SEB 11.8 % 9.8 % Lifco AB 12.8 - Nordnet 6.0 % 8.6 % Small Cap Small Cap Transcom AB 2.0 0.08 Avanza 15.8 % 13.5 % Bulten AB 0.8 0.9 Nordnet 13.5 % 13.0 % Mycronic AB 0.8 0.4 SHB 6.1 % 5.0 % First North -

Doing Data Differently

General Company Overview Doing data differently V.14.9. Company Overview Helping the global financial community make informed decisions through the provision of fast, accurate, timely and affordable reference data services With more than 20 years of experience, we offer comprehensive and complete securities reference and pricing data for equities, fixed income and derivative instruments around the globe. Our customers can rely on our successful track record to efficiently deliver high quality data sets including: § Worldwide Corporate Actions § Worldwide Fixed Income § Security Reference File § Worldwide End-of-Day Prices Exchange Data International has recently expanded its data coverage to include economic data. Currently it has three products: § African Economic Data www.africadata.com § Economic Indicator Service (EIS) § Global Economic Data Our professional sales, support and data/research teams deliver the lowest cost of ownership whilst at the same time being the most responsive to client requests. As a result of our on-going commitment to providing cost effective and innovative data solutions, whilst at the same time ensuring the highest standards, we have been awarded the internationally recognized symbol of quality ISO 9001. Headquartered in United Kingdom, we have staff in Canada, India, Morocco, South Africa and United States. www.exchange-data.com 2 Company Overview Contents Reference Data ............................................................................................................................................ -

Arise Ab (Publ)

ARISE AB (PUBL) Prospectus for the admission to trading on Nasdaq Stockholm of SEK 650,000,000 SENIOR SECURED GREEN FLOATING RATE NOTES 2018/2021 ISIN: SE0010920900 Lead Manager SW37716777/13 Page 2 of 81 IMPORTANT INFORMATION In this prospectus, “Arise”, the “Company” or the “Group”, depending on the context, refers to Arise AB (publ), the group in which Arise AB (publ) is the parent company, a subsidiary of the group in which Arise AB (publ) is the parent company or including the associ- ated company Sirocco Wind Holding AB as relevant. The “Issuer” means Arise AB (publ). The “Sole Manager” means DNB Markets, DNB Bank ASA, Sverige filial. “Euroclear” refers to Euroclear Sweden AB and “Nasdaq Stockholm” refers to Nasdaq Stockholm AB. “SEK” refers to Swedish kronor. Words and expressions defined in the terms and conditions of the Notes (as defined below) (the “Terms and Conditions”) beginning on page 39 have the same meaning when used in this Prospectus, unless expressly stated or the context requires otherwise. Notice to investors On 16 March 2018 (the “Issue Date”) the Issuer issued a note loan in the amount of SEK 650,000,000. The initial nominal amount of each note is SEK 2,000,000 (the “Nominal Amount”) (the “Notes”). The maximum nominal amount of the Notes may not exceed SEK 650,000,000 unless a consent from the Noteholders is obtained pursuant to the Terms and Conditions. This prospectus (the “Pro- spectus”) has been prepared for the listing of the loan constituted by the Notes on a Regulated Market. This Prospectus does not con- tain and does not constitute an offer or a solicitation to buy or sell Notes. -

Over 100 Exchanges Worldwide 'Ring the Bell for Gender Equality in 2021' with Women in Etfs and Five Partner Organizations

OVER 100 EXCHANGES WORLDWIDE 'RING THE BELL FOR GENDER EQUALITY IN 2021’ WITH WOMEN IN ETFS AND FIVE PARTNER ORGANIZATIONS Wednesday March 3, 2021, London – For the seventh consecutive year, a global collaboration across over 100 exchanges around the world plan to hold a bell ringing event to celebrate International Women’s Day 2021 (8 March 2020). The events - which start on Monday 1 March, and will last for two weeks - are a partnership between IFC, Sustainable Stock Exchanges (SSE) Initiative, UN Global Compact, UN Women, the World Federation of Exchanges and Women in ETFs, The UN Women’s theme for International Women’s Day 2021 - “Women in leadership: Achieving an equal future in a COVID-19 world ” celebrates the tremendous efforts by women and girls around the world in shaping a more equal future and recovery from the COVID-19 pandemic. Women leaders and women’s organizations have demonstrated their skills, knowledge and networks to effectively lead in COVID-19 response and recovery efforts. Today there is more recognition than ever before that women bring different experiences, perspectives and skills to the table, and make irreplaceable contributions to decisions, policies and laws that work better for all. Women in ETFs leadership globally are united in the view that “There is a natural synergy for Women in ETFs to celebrate International Women’s Day with bell ringings. Gender equality is central to driving the global economy and the private sector has an important role to play. Our mission is to create opportunities for professional development and advancement of women by expanding connections among women and men in the financial industry.” The list of exchanges and organisations that have registered to hold an in person or virtual bell ringing event are shown on the following pages. -

Attachment (.Pdf)

November 7th, 2018 Press release on the earnings of Sýn hf. for the Third quarter of 2018: The merger starting to generate positive results with EBITDA increase of 21% The interim financial report for Sýn hf. for the third quarter of 2018, was approved by the company’s Board of Directors and CEO at a board meeting on November 7th 2018. In December 2017 the company purchased certain assets and operations of 365 Miðlar hf., and this influences the comparison between periods. • Revenue in the third quarter of 2018 amounted to ISK 5,449 million, an increase of 59% from the previous year. Income in the first nine months of the year increased by ISK 6,233 million, or 63%. • The quarter’s EBITDA amounted to ISK 1,032 million, an increase by ISK 178 million from previous year. EBITDA for the first nine months amounted to ISK 2,468 million, a 6% increase from previous year. • EBITDA adjusted for one off items in relation to the acquisition amounted to ISK 1,038 million, a 21% increase from the previous year. • Profit in the period amounted to ISK 226 million, a decrease of 22% from the previous year. Profit for the first nine months of the year amounted to ISK 278 million, a 62% decrease from previous year. • Profit per share was ISK 0.76 in Q3 and was ISK 0.94 for the first nine months of the year. • The quarter‘s investment activities amounted to ISK 516 million, an increase of 40% from the previous year due to integration projects.