Barramundi Quarter Update Newsletter December 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The State of the Deal and Deloitte Queensland Index

The State of the Deal and Deloitte Queensland Index March 2021 – Queensland Index Exceeds $100 billion THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Contents Executive Summary 1 Then & Now – Investment Landscape 3 Then & Now – Deloitte Queensland Index 4 Queensland Economic Update 7 The Deloitte Queensland Index Q1 2021 8 Contacts 11 Sources 12 ii THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Executive Summary Following the significant rebound in the second half of 2020, companies in the Deloitte Queensland Index exceeded $100 billion at 31 March 2021, the highest month end market capitalisation on record for the State. Deloitte Queensland Index S&P/ASX All Ordinaries Companies in the Deloitte return in Q1 2021 return in Q1 2021 Queensland Index 3.5% 2.4% 169 at 31 March 2021 10.6% in Q4 2020 14.0% in Q4 2020 173 at 31 December 2020 90 companies increased Market capitalisation as at Mar-21 market capitalisation (53%) 66 companies decreased market $101.6b capitalisation (39%) 12 no movement (7%) $97.2b as at Dec-20 $18.5b as at Sep-02 5 delistings 1 listing (1%) Announced QLD M&A Disclosed value of announced transactions in Q1 2021 QLD M&A transactions in Q1 2021 64 $1.9b 92 in Q4 2020 $3.3b in Q4 2020 1 THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion The Deloitte Queensland Index increased by 3.5% in Q1 2021 Queensland M&A more broadly remains strong with with total market capitalisation increasing to $101.6b at 64 transactions announced in Q1 2021 including: Mar-21, the highest month end value on record for the State. -

Annual Report for the YEAR 1 JULY 2013 to 30 JUNE 2014

1 JULY 2013 TO 30 JUNE 2014 NEXTDC Limited ABN 35 143 582 521 Annual Report FOR THE YEAR 1 JULY 2013 TO 30 JUNE 2014 2 4 6 16 24 57 58 72 122 124 126 129 FY14 1 JULY 2013 TO 30 JUNE 2014 NEXTDC Limited ABN 35 143 582 521 1 NEXTDC LIMITED ANNUAL REPORT 30 JUNE 2014 Letter from the Chairman Operational performance and cost management are a key focus to ensure the Company is strongly positioned for growth and to deliver the financial performance and shareholder value that investors require. Douglas Flynn, Chairman On behalf of the Board of Directors and NEXTDC Limited, it The completion of our capital recycling program with the I was honoured to take over as Chairman of the Board We believe the Company’s new Board has the strength, is my pleasure to present NEXTDC Limited’s fourth Annual Asia Pacific Data Centre Group raised approximately $140 from Mr Ted Pretty in April 2014. Ted has remained on the independence and breadth of experience required to Report. million across the 2013 and 2014 financial years. The investor Board as a Non-executive Director and I’d like to take this build long term shareholder value. Your Directors and response to NEXTDC’s five-year senior unsecured notes opportunity to thank him for guiding the Company during management team look forward to a period of stability as The past financial year has been transformational with offering in June 2014, which raised $60 million of debt what was a key period of change. -

Monthly NTA and Performance Update

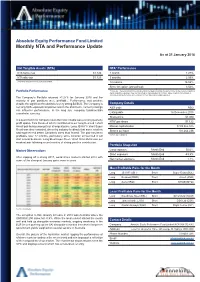

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Australian Investment Strategy

2 November 2016 Asia Pacific/Australia Equity Research Investment Strategy Australian Investment Strategy Research Analysts STRATEGY Hasan Tevfik ,CFA 61 2 8205 4284 [email protected] Aussie darlings Peter Liu 61 2 8205 4071 ■ Aussies love their darlings: Australia currently has the most expensive [email protected] equity market "Darlings" in the world. Our darlings trade on a forward P/E Damien Boey of 38x. The other commodity-focused market, Canada, has the second 61 2 8205 4615 [email protected] most expensive darlings. Darlings in Australia have been more expensive only during the Nasdaq bubble when they touched 45x. ■ Darling derating: Buying Australian darlings at these valuations has been a poor strategy in the past. Also, the current high valuation for Australia's darlings suggest they are especially vulnerable to rising bond yields and the coming end of the Australian profits recession. A rising discount rate and a lower premium for growth suggest investors should focus on stocks that could be future darlings. ■ Hello Daaarling: Future market darlings have shared many similar characteristics over the last 20 years. They are generally well managed, have strong balance sheets and operate on high margins. Our "Hello Daaarling" strategy highlights potential future darlings and they currently trade on just 17x P/E and include Caltex, Eclipx, Mayne Pharma, Nufarm, Star Entertainment and South 32. We add Eclipx to our long Portfolio. Figure 1: Australia has the most expensive darlings in the world Median 12-month forward P/E of "market darlings" around the world* 40 35 30 25 20 15 10 Australia Canada Cont. -

Ethical Trans-Tasman Fund Fact Sheet – August 2021

Ethical Trans-Tasman Fund Fact Sheet – August 2021 Investment Objective Fund Performance (after fees, before tax) Ethical investing in Australasian equities to achieve above average long-term risk adjusted returns. Performance 1 6 1 Inception month months year p.a. The Fund invests directly in Australasian equities, listed property companies and other assets that satisfy Pathfinder’s ethical investment 1 criteria. This is a high-conviction fund of top investment ideas and Fund Return 5.3% 8.9% 18.3% 23.3% targets a portfolio of 10 to 40 holdings. Benchmark 3.1% 9.9% 16.0% 8.1% Investing Ethically Return 2 1. UN Sustainable Development Goals: Aspiring for investment Outperformance 2.2% -1.0% 2.3% 15.2% decisions to contribute to UN Sustainable Development Goals. 2. Environmental, social and governance focus: Focusing investment 1 Performance as of 31 August 2021. Trading started: October 2019. into companies that rate higher on environmental, social and 2 50/50 composite of NZX 50 and ASX 200 Index governance criteria. 3. Climate change awareness: Companies with a lower carbon intensity Actual Investment Mix and a plan for managing the transition to a low carbon economy make better long-term investments. Health Care: 29.7% 4. Aware, Fair, Care: Avoiding investment in companies engaged in industries or activities seen as harmful. Utilities: 13.3% 5. Engagement and shareholder voting: Engaging and voting as a Information Technology: 13.3% shareholder can bring about positive change. Consumer Staples: 12.5% Please refer to our Ethical Investment Policy for more details. Financials: 11.2% Investor Suitability Communication Services: 10.2% Industrials: 5.8% The Ethical Trans-Tasman Fund is suited to an investor with a high tolerance to risk and a minimum investment timeframe of 5+ years. -

NEXTDC FY17 Appendix 4E and Annual Report

NEXTDC Limited Appendix 4E Preliminary Final Report Results for announcement to the market For the year ended 30 June 2017 (Previous corresponding period: to 30 June 2016) Summary of Financial Information 2017 2016 Change Change Note $’000 $’000 $’000 % Revenue from ordinary activities 123,550 92,837 30,713 33% Profit/(loss) from ordinary activities after income tax for the period attributable to 1 22,999 1,756 21,243 NMF1 members Profit/(loss) after income tax attributable to 1 22,999 1,756 21,243 NMF members 1. Included in profit after income tax is an income tax benefit of $10.2 million which is primarily due to the recognition of accumulated tax losses as deferred tax assets. Dividends No dividend has been proposed or declared in respect of the year ended 30 June 2017. Net tangible assets 2017 2016 Basic net tangible asset backing per ordinary share $1.75 $1.36 Refer to the attached audited Financial Report for additional disclosures. 1 NMF = Not meaningful NEXTDC Limited and controlled entities | FY17 Annual Report Page 1 of 100 ANNUAL REPORT FOR THE YEAR 1 JULY 2016 TO 30 JUNE 2017 Letter from the Chairman and CEO 3 About NEXTDC 6 Directors’ Report 12 Remuneration Report 22 Auditor’s Independence Declaration 46 Corporate Governance 47 Financial Report 48 Directors’ Declaration 91 Independent Auditor’s Report to the Members 92 Shareholder Information 98 Corporate Directory 100 NEXTDC Limited and controlled entities | FY17 Annual Report Page 2 of 100 Letter from Chairman and CEO We welcome our shareholders to this year’s Annual Report, which marks the end of the financial year to 30 June 2017 (“FY17”) and another period of significant growth and strategic achievements. -

Is Xero in the BUY Zone?

Monday 15 March 2021 Is Xero in the BUY zone? I don’t think all tech stocks are born equal. What I’m really saying is Apple is very different to Zoom, while Xero is not like Afterpay. They’re lumped in the same tech group and can get sold off when tech loses friends but this sometimes silly sell-off could be creating opportunities. For the last month, tech stocks have been in the twilight zone and Xero has dropped from its highs. Does this mean it’s passed over into the buy zone? Sincerely, Peter Switzer Inside this Issue 02 Is Xero in the buy zone? Is Xero in the buy zone? by Peter Switzer 05 Does environmental, social and corporate governance (ESG) investing stack up? And what’s the best ETF? Does ESG investing stack up? by Paul Rickard 08 5 companies at the forefront of the hydrogen push FMG, HZR, LCK, HXG & PH2 Is Xero in the buy by James Dunn 11 My “HOT” stock: QAN zone? Qantas by Peter Switzer by Maureen Jordan 02 12 Buy, Hold, Sell – What the Brokers Say 12 upgrades, 5 downgrades by Rudi Filapek-Vandyck Important information: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. For this reason, any individual should, before Switzer Super Report is published by Switzer Financial Group Pty Ltd AFSL No. 286 531 acting, consider the appropriateness of the information, having regard to the Level 4, 10 Spring Street, Sydney, NSW, 2000 individual's objectives, financial situation and needs and, if necessary, seek T: 1300 794 893 F: (02) 9222 1456 appropriate professional advice. -

(ASX100) Women on Boards Analysis

Australia/NZ | Australia Thematic Investing (Citi) Equities 18 August 2011 │ 32 pages ESG: ASX100 Women on Board Analysis Increasing Focus on Board Diversity Women on Boards of ASX100 Companies — The ASX Corporate Governance Council’s new principles and recommendations on diversity commenced on 1 January Elaine Prior 2011. This is likely to lead to increasing focus on companies’ approaches to diversity +61-2-8225-4891 issues, including female representation on company boards. This report looks at data [email protected] on women directors on ASX100 company boards. The number of women directors has Felipe Faria increased, particularly in recent months (Figure 5 to Figure 8). Board diversity may [email protected] enhance effectiveness, by providing a wider range of perspectives and knowledge. Women on Boards Data — We collected and analysed data on female board directors of S&P/ASX100 companies from FY08 to 8 August 2011 (Figure 5 to Figure 9). At 8 August 2011 there were 134 women on ASX100 boards, a 46% increase from FY08. ASX100 companies with no female board directors were AQP, CQO, EGP, FMG, IPL, JHX, LEI, LYC, OSH, PDN, PRY, RHC, RMD, SGM and SWM. Companies with three female directors (the highest number identified) are AMP, BEN, CBA, MQG, QAN, QBE and WBC. Seven female directors each currently hold three ASX100 directorships. Business Case for Gender Diversity — Reibey Institute research found that those ASX500 companies with women directors on 30 June 2010 had a 3-year return on equity (ROE) 10.7% higher than those without any women directors. The 5-year ROE was 11.1% higher. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Business Leadership: the Catalyst for Accelerating Change

BUSINESS LEADERSHIP: THE CATALYST FOR ACCELERATING CHANGE Follow us on twitter @30pctAustralia OUR OBJECTIVE is to achieve 30% of ASX 200 seats held by women by end 2018. Gender balance on boards does achieve better outcomes. GREATER DIVERSITY ON BOARDS IS VITAL TO THE GOOD GOVERNANCE OF AUSTRALIAN BUSINESSES. FROM THE PERSPECTIVE OF PERFORMANCE AS WELL AS EQUITY THE CASE IS CLEAR. AUSTRALIA HAS MORE THAN ENOUGH CAPABLE WOMEN TO EXCEED THE 30% TARGET. IF YOUR BOARD IS NOT INVESTING IN THE CAPABILITY THAT DIVERSITY BRINGS, IT’S NOW A MARKED DEPARTURE FROM THE WHAT THE INVESTOR AND BROADER COMMUNITY EXPECT. Angus Armour FAICD, Managing Director & Chief Executive Officer, Australian Institute of Company Directors BY BRINGING TOGETHER INFLUENTIAL COMPANY CHAIRS, DIRECTORS, INVESTORS, HEAD HUNTERS AND CEOs, WE WANT TO DRIVE A BUSINESS-LED APPROACH TO INCREASING GENDER BALANCE THAT CHANGES THE WAY “COMPANIES APPROACH DIVERSITY ISSUES. Patricia Cross, Australian Chair 30% Club WHO WE ARE LEADERS LEADING BY EXAMPLE We are a group of chairs, directors and business leaders taking action to increase gender diversity on Australian boards. The Australian chapter launched in May 2015 with a goal of achieving 30% women on ASX 200 boards by the end of 2018. AUSTRALIAN 30% CLUB MEMBERS Andrew Forrest Fortescue Metals Douglas McTaggart Spark Group Ltd Infrastructure Trust Samuel Weiss Altium Ltd Kenneth MacKenzie BHP Billiton Ltd John Mulcahy Mirvac Ltd Stephen Johns Brambles Ltd Mark Johnson G8 Education Ltd John Shine CSL Ltd Paul Brasher Incitec Pivot