Banking & Finance Litigation Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Assigning Responsibilities in the Libor Scandal

1233 The Differential Management of Financial Illegalisms: Assigning Responsibilities in the Libor Scandal Thomas Angeletti How, in a context of growing critiques of financialization, can law contribute to protecting the legitimacy of finance? This paper argues that the assign- ment of responsibilities between individuals and organizations plays a deci- sive role, using the recent Libor scandal as an empirical illustration. To do so, the paper offers a Foucauldian framework, the differential management of financial illegalisms, dedicated to the study of illegalities in financial capi- talism. The comparison of the legal treatment of two manipulations of Libor, this key benchmark in financial markets, reveals how mid-level traders have been the object of criminal prosecution, while law undervalued the role of top managers and organizations. To capture how differential management is performed in practice, I analyze precisely how the conflict-resolution devices (criminal trial vs. settlement) and the social categorizations prevailing in the two manipulations of Libor favor different forms of responsibility, individual or organizational. I conclude by exploring the implications of law’s relation- ship to financial legitimacy. For more than a decade now, the financialization of capitalism (Krippner 2011; Van der Zwan 2014) has been the locus of many critiques. Financialization has been studied sufficiently to under- stand how much finance has invaded our daily lives (Martin 2002), without measuring necessarily fully its ramifications. The clear causality between the rise of wages in the financial sector and the rise in income inequality in the United Kingdom (Bell and Van Reenen 2013), the United States (Volscho and Kelly 2012), and France (Godechot 2012) has put the financial sector on the spot. -

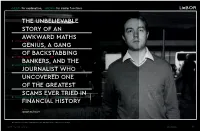

The Unbelievable Story of an Awkward Maths Genius, A

<HELP> for explanation, <MENU> for similar functions LieBOR THE UNBELIEVABLE STORY OF AN AWKWARD MATHS 1) Tom Hayes (Trader) -10.12 GENIUS, A GANG OF BACKSTABBING 2) Tom's Brokers (Cabal) -66.69 BANKERS, AND THE 3) David Enrich (Author) 21.03 JOURNALIST WHO UNCOVERED ONE OF THE GREATEST SCAMS EVER TRIED IN 4) The Libor rigging scandal (Global Crisis) -176.12 FINANCIAL HISTORY Words by Joseph Bullmore The trader at the centre of the scandal: Asperger's sufferer Tom Hayes, currently serving an 11-year term in jail GENTLEMAN’S JOURNAL FEATURES 77 he Libor is the most important number in the world. It’s also probably the they didn’t raise suspicions harems of escorts – and often all five in com- THE How they did it... THE most boring. A single figure that underpins modern capitalism, the Libor (or SCAM among their managers, while EXCESS bination. Some stories were too salacious to T London Interbank Offered Rate) is the theoretical rate at which banks will their managers would invariably Trader 1: make the final edit. ‘This one broker – he lend to each other – the price, essentially, of borrowed money. The magazine you turn a blind eye in the face of ‘What's the call called himself Danny the Animal – was brag- hold in your hands at this very moment is drenched in Libor – it soaks through the ‘The thing about Tom is he’s very literal – no healthy profit spikes. (‘Where on the Libor?’ ‘At a certain point during my in- ging about how he’d stocked a boat in the credit card you used to pay for it, the price of printing ink, the mortgage overheads sense of sarcasm or subtlety,’ Enrich tells me. -

2020 Impact Report

IMPACT REPORT 2020 ABOUT THIS REPORT This report covers United Way’s 2020 fiscal year (July 1, 2019 through June 30, 2020). For the latest information about our work, visit YourUnitedWay.org. CONTENTS INTRODUCTION 4 OUR SERVICE AREA 6 STEPS TO SUCCESS 7 LETTER FROM JAMES L. M. TAYLOR, PRESIDENT & CEO 8 LETTER FROM LORI ELLIOTT JARVIS, BOARD CHAIR 8 2020 BOARD OF DIRECTORS 9 FUNDING 10 2020-22 COMMUNITY INVESTMENTS 12 COMMUNITY VOLUNTEERS 14 UNITED WAY IN THE COMMUNITY 16 KINDERGARTEN COUNTDOWN CAMP 18 VOLUNTEER INCOME TAX ASSISTANCE 20 WORKFORCE PARTNERSHIP TEAM 24 VOLUNTEERING 27 CORPORATE PARTNERSHIPS 32 COVID-19: LEADERSHIP IN A TIME OF CRISIS 34 2020 STEPS TO SUCCESS AWARDS 36 GIVING COMMUNITIES 38 2020 FINANCIALS 48 Impact Report | 3 INTRODUCTION 4 | United Way of Greater Richmond & Petersburg Impact Report | 5 OUR SERVICE AREA We serve the region’s neighborhoods and rural areas alike – 11 localities in all. 6 | United Way of Greater Richmond & Petersburg STEPS TO SUCCESS Our Steps to Success model identifies nine key milestones on the path to prosperity and serves as the framework for everything we do. Impact Report | 7 FROM OUR LEADERSHIP September 2020 September 2020 Thank you for reading United Way of Greater Richmond & Our region is changing rapidly, and the needs of our communities Petersburg’s 2020 Impact Report. I am glad to be able to share this are changing just as quickly. That has never been truer than it is moment of reflection with you. right now in 2020. 2020 has been a challenging and tumultuous year for everyone in Now more than ever, United Way of Greater Richmond & our region. -

The Libor Scandal: a Need for Revised National and International Reforms and Regulations

North East Journal of Legal Studies Volume 32 Fall 2014 Article 4 Fall 2014 The Libor Scandal: A Need For Revised National And International Reforms And Regulations Roy J. Girasa [email protected] Richard J. Kraus [email protected] Follow this and additional works at: https://digitalcommons.fairfield.edu/nealsb Recommended Citation Girasa, Roy J. and Kraus, Richard J. (2014) "The Libor Scandal: A Need For Revised National And International Reforms And Regulations," North East Journal of Legal Studies: Vol. 32 , Article 4. Available at: https://digitalcommons.fairfield.edu/nealsb/vol32/iss1/4 This item has been accepted for inclusion in DigitalCommons@Fairfield by an authorized administrator of DigitalCommons@Fairfield. It is brought to you by DigitalCommons@Fairfield with permission from the rights- holder(s) and is protected by copyright and/or related rights. You are free to use this item in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses, you need to obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/or on the work itself. For more information, please contact [email protected]. 89 / Vol 32 / North East Journal of Legal Studies THE LIBOR SCANDAL: A NEED FOR REVISED NATIONAL AND INTERNATIONAL REFORMS AND REGULATIONS by Roy J. Girasa* Richard J. Kraus** INTRODUCTION Few individuals or even major investors are aware of the London Interbank Offered Rate (LIBOR), a little-known activity that profoundly affects local and world finances. The total value of securities and loans affected by LIBOR is approximately $800 trillion dollars annually. -

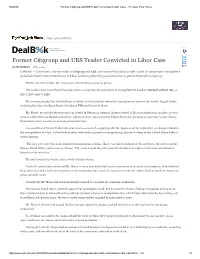

Former Citigroup and UBS Trader Convicted in Libor Case the New York Times

8/6/2015 Former Citigroup and UBS Trader Convicted in Libor Case The New York Times http://nyti.ms/1N4llzh CLOSE X Former Citigroup and UBS Trader Convicted in Libor Case By CHAD BRAY AUG. 3, 2015 LONDON — Tom Hayes, a former trader at Citigroup and UBS, was convicted Monday on eight counts of conspiring to manipulate a global benchmark interest rate known as Libor, bolstering efforts by prosecutors here to pursue financial wrongdoing. Shortly after the verdict, Mr. Hayes was sentenced to 14 years in prison. The verdict came more than three years after a conspiracy among traders to manipulate the London interbank offered rate, or Libor, first came to light. The ensuing scandal has led to billions of dollars in fines and has rocked the reputations of some of the world’s biggest banks, including Barclays, the Royal Bank of Scotland, UBS and Deutsche Bank. Mr. Hayes, 35, was the first person to go to trial in Britain on criminal charges related to Libor manipulation, and his case was seen as a bellwether for British authorities, who have been criticized in the United States for not being as aggressive as the Justice Department when it comes to pursuing financial crime. A second trial of former traders who have been accused of conspiring with Mr. Hayes is set for September on charges related to the manipulation of Libor. A third trial of other individuals accused of manipulating Libor as it relates to the United States dollar is set for January. “The jury were sure that in his admitted manipulation of Libor, Hayes was indeed dishonest,” David Green, the director of the Serious Fraud Office, said in a news release. -

P.R.I.M.E. Finance Panel of Recognized International Market Experts in Finance

P.R.I.M.E. Finance Panel of Recognized International Market Experts in Finance Beyond LIBOR: New Benchmarks And New Issues Affecting Benchmarks Presentation by Thomas Werlen 2017 P.R.I.M.E. Finance Annual Conference 23 & 24 January, Peace Palace, The Hague Agenda 1 Scope of the Panel’s Discussions 2 From the LIBOR Scandal to other Benchmark Manipulations 3 Involvement of Authorities 4 Agenda 2 Beyond LIBOR: New Benchmarks and new Issues affecting Benchmarks Benchmarks causing regulatory issues include but are not limited to LIBOR Alternative systems to determine benchmarks are explored due to regulatory and investigatory pressure but also following industry initiatives Investigations are still ongoing and private enforcement is in full steam Goal of today is to update on current developments on all fronts 3 Agenda 1 Scope of the Panel’s Discussions 2 From the LIBOR Scandal to other Benchmark Manipulations 3 Involvement of Authorities 4 Agenda of Panel 4 From LIBOR… (1/2) Benchmark reference rate for debt instruments, including government and corporate bonds, mortgages, student loans, credit cards; as well as derivatives such as currency and interest swaps, among many other financial products In early 2008, New York Fed learns of false reports “we know that we’re not posting, um, an honest rate” (statement of Barclays employee to a New York Fed official) Provoked a series of regulatory actions, e.g.: Barclays settled a case with U.S. and UK authorities for $435 million in July 2012, and in August 2016 agreed to pay an additional $100 million to forty-four U.S. -

Banking and the Limits of Professionalism I

2017 Thematic: Banking and the Limits of Professionalism 411 17 BANKING AND THE LIMITS OF PROFESSIONALISM DIMITY KINGSFORD SMITH,* THOMAS CLARKE** AND JUSTINE ROGERS*** I INTRODUCTION Few other occupations that aspire to professional status have the influence, both beneficial and destructive, or the raw power to resist regulation and political constraint, that banking has. The global financial crisis (‘GFC’) and revelations of bank manipulation of the benchmark London Inter-bank Offering Rate (‘LIBOR’),1 which followed quickly afterwards, showed devastatingly the worst of this influence and power. These failings have been diagnosed as stemming from a foundational collapse in the values of individuals and in the governance of banking entities.2 The critique has concentrated on demands for better decisions and conduct from individuals, as well as changes in the entities for which they work, to better support those individuals. This post-GFC prescription for banking has turned attention to the professions as a possible framework for promoting individual ethical conduct in banking.3 Indeed, since the LIBOR revelations, even banking itself has expressed a desire to professionalise.4 * Professor and Director of the Centre for Law, Markets and Regulation (‘CLMR’) University of New South Wales (‘UNSW’); LLM (London School of Economics, London) LLB (Sydney) BA (Sydney). Correspondence to Professor Kingsford Smith <[email protected]>. ** Professor of Management and Director of the Key University Research Centre for Corporate Governance, University of Technology Sydney; PhD (Warwick) BSocSc (Birm). *** Lecturer, UNSW Law; DPhil (Oxford) MSc (Oxford). The authors acknowledge the support of the Australian Research Council and the Professional Standards Councils for this work and particularly the comments of the anonymous referees and of fellow researcher, Hugh Breakey, on an earlier version of this paper and the work of Senior Research Fellow, John Chellew. -

World Investment Report 2001: Promoting Linkages

United Nations Conference on Trade and Development World Investment Report 2001 Promoting Linkages United Nations New York and Geneva, 2001 Note UNCTAD serves as the focal point within the United Nations Secretariat for all matters related to foreign direct investment and transnational corporations. In the past, the Programme on Transnational Corporations was carried out by the United Nations Centre on Transnational Corporations (1975-1992) and the Transnational Corporations and Management Division of the United Nations Department of Economic and Social Development (1992-1993). In 1993, the Programme was transferred to the United Nations Conference on Trade and Development. UNCTAD seeks to further the understanding of the nature of transnational corporations and their contribution to development and to create an enabling environment for international investment and enterprise development. UNCTAD's work is carried out through intergovernmental deliberations, technical assistance activities, seminars, workshops and conferences. The term “country” as used in this study also refers, as appropriate, to territories or areas; the designations employed and the presentation of the material do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. In addition, the designations of country groups are intended solely for statistical or analytical convenience and do not necessarily express a judgement about the stage of development reached by a particular country or area in the development process. The reference to a company and its activities should not be construed as an endorsement by UNCTAD of the company or its activities. -

Public Affairs and Lobbying Register

Public Affairs and Lobbying Register 3x1 Offices: 16a Walker Street, Edinburgh EH3 7LP 210 Borough High Street, London SE1 1JX 26-28 Exchange Street, Aberdeen, AB11 6PH OFFICE(S) Address: 3x1 Group, 11 Fitzroy Place, Glasgow, G3 7RW Tel: Fax: Web: CONTACT FOR PUBLIC AFFAIRS [email protected] LIST OF EMPLOYEES THAT HAVE CONDUCTED PUBLIC AFFAIRS SERVICES Ailsa Pender Cameron Grant Katrine Pearson Lindsay McGarvie Patrick Hogan Richard Holligan LIST OF CLIENTS FOR WHOM PUBLIC AFFAIRS SERVICES HAVE BEEN PROVIDED North British Distillery Atos The Scottish Salmon Company SICPA Public Affairs and Lobbying Register Aiken PR OFFICE(S) Address: 418 Lisburn Road, Belfast, BT9 6GN Tel: 028 9066 3000 Fax: 028 9068 3030 Web: www.aikenpr.com CONTACT FOR PUBLIC AFFAIRS [email protected] LIST OF EMPLOYEES THAT HAVE CONDUCTED PUBLIC AFFAIRS SERVICES Claire Aiken Donal O'Neill John McManus Lyn Sheridan Shane Finnegan LIST OF CLIENTS FOR WHOM PUBLIC AFFAIRS SERVICES HAVE BEEN PROVIDED Diageo McDonald’s Public Affairs and Lobbying Register Airport Operators Associaon OFFICE(S) Address: Airport Operators Association, 3 Birdcage Walk, London, SW1H 9JJ Tel: 020 7799 3171 Fax: 020 7340 0999 Web: www.aoa.org.uk CONTACT FOR PUBLIC AFFAIRS [email protected] LIST OF EMPLOYEES THAT HAVE CONDUCTED PUBLIC AFFAIRS SERVICES Ed Anderson Henk van Klaveren Jeff Bevan Karen Dee Michael Burrell - external public affairs Peter O'Broin advisor Roger Koukkoullis LIST OF CLIENTS FOR WHOM PUBLIC AFFAIRS SERVICES HAVE BEEN PROVIDED N/A Public Affairs and Lobbying Register Anchor -

1 'The Fight Against Fraud: a Critical Review and Comparative Analysis Of

‘The fight against fraud: A critical review and comparative analysis of the Labour and Conservative government’s anti-fraud policies in the United Kingdom’ Dr. Umut Turksen (Professor in Law & Business)1 and Dr. Nicholas Ryder (Professor in Financial Crime)2 1 Professor Umut Turksen, Kingston University, London. E-mail: [email protected] 2 Professor Nicholas Ryder, University of the West of England, Bristol. E-mail: [email protected] 1 “There is clear evidence that fraud is becoming the crime of choice for organised crime and terrorist funding. The response from law enforcement world-wide has not been sufficient. We need to bear down on fraud; to make sure that laws, procedures and resources devoted to combating fraud are fit for the modern age”.3 Introduction Initially, international efforts to tackle financial crimes have concentrated mainly on money laundering and terrorist financing. This is largely due to the United States of America (US) led ‘war on drugs’ and the ‘financial war on terrorism’. Fraud on the other hand has been placed lower in the list of public policy priorities and law enforcement efforts.4 Following the turbulent times we have experienced since the global economic downturn first in 1997 (triggered by the Asian crisis) and later in 2008 (triggered by the bursting of the US subprime mortgage bubble), there is evidence that politicians are changing their stance in tackling a number of fraudulent and malfeasant activities particularly in the banking and financial services sectors. Fraud can be defined as “persuading someone to part with something”,5 which includes “deceit or an intention to deceive”,6 or an “act of deception intended for personal gain or to cause a loss to another party” 7 and it “involves the perpetrator making personal gains or avoiding losses through the 3 Wright, R. -

Farewell to LIBOR Steven Criscuolo, CPA, MBA | September 2017

Farewell To LIBOR Steven Criscuolo, CPA, MBA | September 2017 We all know banks are in business to make money. While most of today’s banks are quite sophisticated and have multiple sources of income, the most basic and surest way to make money is to “borrow” from depositors at very low interest rates, and then lend to borrowers at higher rates. The difference between the average rate paid to depositors and the average rate collected from borrowers, referred to as the “spread,” represents a profit to the bank. Money made on the spread is a sure thing, unless the market rate of interest that must be paid to attract and keep depositors increases, while the rate collected from borrowers remains flat. For this reason, banks prefer to lend on a variable rate basis, maintaining their spread no matter how market interest rates move. This, combined with an increase in the trading of sophisticated market instruments such as interest rate swaps, foreign currency options and forward rate agreements, convinced the British Bankers Association to begin work on setting a short-term interest rate standard in 1984. On January 1, 1986, the London Interbank Offering Rate (“LIBOR”) was born. On any given day, 35 LIBOR rates are set – one for each of seven different time periods (ranging from one day to one year) in five different currencies (Dollar, Euro, Yen, Sterling, Franc). On each business day since January 1, 1986, twenty specific banks from around the world submit applicable rates “at which an individual Contributor Panel bank could borrow funds, were it to do so, by asking for and then accepting inter-bank offers in reasonable market size, just before 11:00 London time.”1 Submitted rates are used by The Intercontinental Exchange to calculate the day’s LIBOR rates. -

Note LIBOR: the World's Most Important Headache

Note LIBOR: The World’s Most Important Headache Alec Foote Mitchell* INTRODUCTION Imagine your friend has an appointment, but today she forgot her watch. In return for giving you $50, she wants you to keep an eye on the clock. But in the middle of the day, the clock suddenly vanishes. There might be some alternatives: you could use the sun to estimate the time, look to the traffic to see when rush hour starts, or you could guess. But how do you know whether those alternatives are sufficient? What seemed to be a simple contract was premised on a basic assump- tion: your clock would not disappear. But once it did, it threw the en- tire agreement into question and could result in your friend missing her appointment and you losing the $50. In finance, many contracts are based on a similar premise: the availability of LIBOR. The London Inter-Bank Offered Rate, known as LIBOR, has been dubbed “the world’s most important number.”1 The rate is ubiquitous in global finance, where it underlies almost $350 trillion in financial contracts2 and is meant to measure the estimated * J.D. Candidate 2021, University of Minnesota Law School. For my Mom and Dad, whose patience and guidance taught me that improving writing skills is a never- ending pursuit. To my sisters, whose intelligence and hard work have provided me with a source of continual inspiration. Special thanks to the editors and staff members of the Minnesota Law Review, whose work is often unnoticed but greatly improves legal scholarship, and to Professor Claire Hill for her feedback throughout my authorship of this Note.