Court of Appeal Judgment Template

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Assigning Responsibilities in the Libor Scandal

1233 The Differential Management of Financial Illegalisms: Assigning Responsibilities in the Libor Scandal Thomas Angeletti How, in a context of growing critiques of financialization, can law contribute to protecting the legitimacy of finance? This paper argues that the assign- ment of responsibilities between individuals and organizations plays a deci- sive role, using the recent Libor scandal as an empirical illustration. To do so, the paper offers a Foucauldian framework, the differential management of financial illegalisms, dedicated to the study of illegalities in financial capi- talism. The comparison of the legal treatment of two manipulations of Libor, this key benchmark in financial markets, reveals how mid-level traders have been the object of criminal prosecution, while law undervalued the role of top managers and organizations. To capture how differential management is performed in practice, I analyze precisely how the conflict-resolution devices (criminal trial vs. settlement) and the social categorizations prevailing in the two manipulations of Libor favor different forms of responsibility, individual or organizational. I conclude by exploring the implications of law’s relation- ship to financial legitimacy. For more than a decade now, the financialization of capitalism (Krippner 2011; Van der Zwan 2014) has been the locus of many critiques. Financialization has been studied sufficiently to under- stand how much finance has invaded our daily lives (Martin 2002), without measuring necessarily fully its ramifications. The clear causality between the rise of wages in the financial sector and the rise in income inequality in the United Kingdom (Bell and Van Reenen 2013), the United States (Volscho and Kelly 2012), and France (Godechot 2012) has put the financial sector on the spot. -

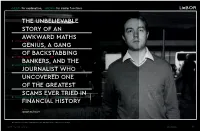

The Unbelievable Story of an Awkward Maths Genius, A

<HELP> for explanation, <MENU> for similar functions LieBOR THE UNBELIEVABLE STORY OF AN AWKWARD MATHS 1) Tom Hayes (Trader) -10.12 GENIUS, A GANG OF BACKSTABBING 2) Tom's Brokers (Cabal) -66.69 BANKERS, AND THE 3) David Enrich (Author) 21.03 JOURNALIST WHO UNCOVERED ONE OF THE GREATEST SCAMS EVER TRIED IN 4) The Libor rigging scandal (Global Crisis) -176.12 FINANCIAL HISTORY Words by Joseph Bullmore The trader at the centre of the scandal: Asperger's sufferer Tom Hayes, currently serving an 11-year term in jail GENTLEMAN’S JOURNAL FEATURES 77 he Libor is the most important number in the world. It’s also probably the they didn’t raise suspicions harems of escorts – and often all five in com- THE How they did it... THE most boring. A single figure that underpins modern capitalism, the Libor (or SCAM among their managers, while EXCESS bination. Some stories were too salacious to T London Interbank Offered Rate) is the theoretical rate at which banks will their managers would invariably Trader 1: make the final edit. ‘This one broker – he lend to each other – the price, essentially, of borrowed money. The magazine you turn a blind eye in the face of ‘What's the call called himself Danny the Animal – was brag- hold in your hands at this very moment is drenched in Libor – it soaks through the ‘The thing about Tom is he’s very literal – no healthy profit spikes. (‘Where on the Libor?’ ‘At a certain point during my in- ging about how he’d stocked a boat in the credit card you used to pay for it, the price of printing ink, the mortgage overheads sense of sarcasm or subtlety,’ Enrich tells me. -

2020 Impact Report

IMPACT REPORT 2020 ABOUT THIS REPORT This report covers United Way’s 2020 fiscal year (July 1, 2019 through June 30, 2020). For the latest information about our work, visit YourUnitedWay.org. CONTENTS INTRODUCTION 4 OUR SERVICE AREA 6 STEPS TO SUCCESS 7 LETTER FROM JAMES L. M. TAYLOR, PRESIDENT & CEO 8 LETTER FROM LORI ELLIOTT JARVIS, BOARD CHAIR 8 2020 BOARD OF DIRECTORS 9 FUNDING 10 2020-22 COMMUNITY INVESTMENTS 12 COMMUNITY VOLUNTEERS 14 UNITED WAY IN THE COMMUNITY 16 KINDERGARTEN COUNTDOWN CAMP 18 VOLUNTEER INCOME TAX ASSISTANCE 20 WORKFORCE PARTNERSHIP TEAM 24 VOLUNTEERING 27 CORPORATE PARTNERSHIPS 32 COVID-19: LEADERSHIP IN A TIME OF CRISIS 34 2020 STEPS TO SUCCESS AWARDS 36 GIVING COMMUNITIES 38 2020 FINANCIALS 48 Impact Report | 3 INTRODUCTION 4 | United Way of Greater Richmond & Petersburg Impact Report | 5 OUR SERVICE AREA We serve the region’s neighborhoods and rural areas alike – 11 localities in all. 6 | United Way of Greater Richmond & Petersburg STEPS TO SUCCESS Our Steps to Success model identifies nine key milestones on the path to prosperity and serves as the framework for everything we do. Impact Report | 7 FROM OUR LEADERSHIP September 2020 September 2020 Thank you for reading United Way of Greater Richmond & Our region is changing rapidly, and the needs of our communities Petersburg’s 2020 Impact Report. I am glad to be able to share this are changing just as quickly. That has never been truer than it is moment of reflection with you. right now in 2020. 2020 has been a challenging and tumultuous year for everyone in Now more than ever, United Way of Greater Richmond & our region. -

A Timely History of Cheating and Fraud Following Ivey V Genting Casinos (UK)

The honest cheat: a timely history of cheating and fraud following Ivey v Genting Casinos (UK) Ltd t/a Crockfords [2017] UKSC 67 Cerian Griffiths Lecturer in Criminal Law and Criminal Justice, Lancaster University Law School1 Author email: [email protected] Abstract: The UK Supreme Court took the opportunity in Ivey v Genting Casinos (UK) Ltd t/a Crockfords [2017] UKSC 67 to reverse the long-standing, but unpopular, test for dishonesty in R v Ghosh. It reduced the relevance of subjectivity in the test of dishonesty, and brought the civil and the criminal law approaches to dishonesty into line by adopting the test as laid down in Royal Brunei Airlines Sdn Bhd v Tan. This article employs extensive legal historical research to demonstrate that the Supreme Court in Ivey was too quick to dismiss the significance of the historical roots of dishonesty. Through an innovative and comprehensive historical framework of fraud, this article demonstrates that dishonesty has long been a central pillar of the actus reus of deceptive offences. The recognition of such significance permits us to situate the role of dishonesty in contemporary criminal property offences. This historical analysis further demonstrates that the Justices erroneously overlooked centuries of jurisprudence in their haste to unite civil and criminal law tests for dishonesty. 1 I would like to thank Lindsay Farmer, Dave Campbell, and Dave Ellis for giving very helpful feedback on earlier drafts of this article. I would also like to thank Angus MacCulloch, Phil Lawton, and the Lancaster Law School Peer Review College for their guidance in developing this paper. -

The Libor Scandal: a Need for Revised National and International Reforms and Regulations

North East Journal of Legal Studies Volume 32 Fall 2014 Article 4 Fall 2014 The Libor Scandal: A Need For Revised National And International Reforms And Regulations Roy J. Girasa [email protected] Richard J. Kraus [email protected] Follow this and additional works at: https://digitalcommons.fairfield.edu/nealsb Recommended Citation Girasa, Roy J. and Kraus, Richard J. (2014) "The Libor Scandal: A Need For Revised National And International Reforms And Regulations," North East Journal of Legal Studies: Vol. 32 , Article 4. Available at: https://digitalcommons.fairfield.edu/nealsb/vol32/iss1/4 This item has been accepted for inclusion in DigitalCommons@Fairfield by an authorized administrator of DigitalCommons@Fairfield. It is brought to you by DigitalCommons@Fairfield with permission from the rights- holder(s) and is protected by copyright and/or related rights. You are free to use this item in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses, you need to obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/or on the work itself. For more information, please contact [email protected]. 89 / Vol 32 / North East Journal of Legal Studies THE LIBOR SCANDAL: A NEED FOR REVISED NATIONAL AND INTERNATIONAL REFORMS AND REGULATIONS by Roy J. Girasa* Richard J. Kraus** INTRODUCTION Few individuals or even major investors are aware of the London Interbank Offered Rate (LIBOR), a little-known activity that profoundly affects local and world finances. The total value of securities and loans affected by LIBOR is approximately $800 trillion dollars annually. -

Court of Appeal Confirms Ivey Test for Dishonesty Is Correct and Clarifies the English Court’S Approach to Rules of Precedent

Court of Appeal confirms Ivey test for Dishonesty is correct and clarifies the English Court’s approach to rules of precedent Published 27 May 2020 An important decision for the determination of offences involving dishonesty and of note for international parties involved in litigation in England. Introduction On 29 April 2020, the Court of Appeal heard what can fairly be regarded as an optimistic appeal made by David Barton and Rosemary Booth against their convictions for multiple counts of conspiracy to defraud, fraud, theft and false accounting. The allegations relate to the extraction of millions of pounds from wealthy individuals by the owners and operators of a luxury care home facility over a number of years. In the Liverpool Crown Court, Mr Barton was convicted 10 counts and sentenced to 21 years imprisonment and Mrs Booth convicted on 3 counts and sentenced to 6 years’ imprisonment. The Appeal Of the multiple grounds of appeal raised, the primary ground related to the law of dishonesty and whether the decision in Ivey v Genting Casinos (UK) (trading as Cockfords Club) [2017] UKSC 67 was the correct approach to dishonesty and if so, was it to be followed in preference to the test described in R v Ghosh [1982] QB 1053. At first instance, the Judge had directed the jury on the issue of dishonesty by reference to Ivey rather than Ghosh. In doing so, he did what the Supreme Court in Ivey indicated he should. The Appellants argued that the Judge should have followed Ghosh because the observations of the Supreme Court in Ivey were made Obiter whilst Ghosh remained binding authority. -

Fakers and Forgers, Deception and Dishonesty: an Exploration of the Murky World of Art Fraud†

Fakers and Forgers, Deception and Dishonesty: An Exploration of the Murky World of Art Fraud† Duncan Chappell and Kenneth Polk Abstract This article examines the problem of fraud in the contemporary art market. It addresses two major cases where persons have been convicted of art fraud in recent years in Australia, examining the legal context within which the prosecutions took place. It then examines problems in common terms such as ‘forgery’ and ‘fakery’. The final sections review the different ways that issues of authenticity in art are addressed in possible cases of art fraud, and examines the question of why so little art fraud comes to the attention of the criminal justice system. Introduction Art fraud, especially allegations of the circulation of spurious works of art, seems a common topic for contemporary mass media. Certainly, the present writers, as criminologists, have encountered numerous allegations of false works in the art market in our many interviews and contacts with leading figures in the Australian context over the past decade. At the same time, as we shall see, almost no cases of art fraud work their way through the court system, either in this country or overseas. This suggests that there may be significant barriers within the criminal justice system that make it difficult to prosecute successfully this form of fraud. The purpose of the present discussion is to examine the crime of art fraud in terms of the major elements that have to be established for a prosecution of the crime, based in large part upon two recent Australian prosecutions of this type which have been successful, and then go on to examine some of the reasons why such prosecutions are so rare. -

FRAUD ACT 2006 - “Making Off” , “ Refusing to Pay” , Doing a Runner”: ( by R.J

FRAUD ACT 2006 - “making off” , “ refusing to pay” , doing a runner”: ( by R.J. April 2009) Making off without payment, or bilking, is now caught by the Fraud Act 2006 Sections 2 and 11 are relevant, however, charges are most easily laid under section 11- ' Obtaining services dishonestly ': The elements of the offence are that the Defendant: • obtains for himself or another • services • dishonestly 1 • knowing the services are made available on the basis that payment has been, is being or will be made for or in respect of them or that they might be and • avoids or intends to avoid payment in full or in part. 2 This offence replaces obtaining services by deception in the Theft Act 1978 which is partly repealed by the Fraud Act. In many cases, the Defendant will also have committed an offence under Section 2 of the Act (Fraud by making a false representation - that payment will be made or made in full). Prosecutors must decide which offence better reflects the criminality involved. The maximum sentence for the Section 11 offence is five years imprisonment; but a fixed penalty may be given. The services must be provided on the basis that they will be paid for; “ they are made available on the basis that payment has been , is being, or will be made, for or in respect of them. The Defendant must intend to avoid payment for the service provided (in full or in part). Actions a driver could take: Phone the police. You can take the offender to the police station, but you must be aware that you are making a citizen's arrest. -

An Overview of the Law of Conspiracy in Selected Jurisdictions

American International Journal of Contemporary Research Vol. 8, No. 2, June 2018 doi:10.30845/aijcr.v8n2p6 An Overview of the Law of Conspiracy in Selected Jurisdictions Dr. A. O. filani Senior Lecturer Department of Jurisprudence and International Law Ekiti State University Nigeria Abstract The paper examines the law of conspiracy in Nigeria, Australia, India, Uganda and England. It examines the applicable laws in these jurisdictions and the position of the judiciary. The paper equally examines defences available to persons charged with conspiracy. The idea of punishing conspirators as if they had committed the offence they conspired to commit as shown in various enactments in Nigeria is a welcome development. Keywords: Conspiracy, Agreement, Over Act, Jurisdiction, Punishment. Introduction The offence of conspiracy in Nigeria is governed primarily by the Penal Code 1 and the Criminal Code. 2 In India, the offence is governed by the Indian Penal Code.3 In the Australian State of Queensland, the primary legislation is the Criminal Code of 18994 from which the Nigerian Criminal Code and the Ugandan Penal Code are derived.5 In England, the offence is both a common law offence and a statutory offence under the Criminal Law Act, 1977. The offence of conspiracy has no definition under the Penal Code and the Criminal Code of Nigeria. But since the common law is in force in Nigeria, it must bear the same meaning as in England as an agreement of two or more persons to do an act which is an offence to agree to do so.6 In Eyo v State,7 defining conspiracy, the court had this to say to wit: Conspiracy is an offence in the agreement of two or more persons to do or cause to be done an illegal act or legal act by illegal means. -

The Impact of the Criminal Law and Money Laundering Measures Upon the Illicit Trade in Art and Antiquities, 16 Art Antiquity & L

+(,121/,1( Citation: Janet Ulph, The Impact of the Criminal Law and Money Laundering Measures upon the Illicit Trade in Art and Antiquities, 16 Art Antiquity & L. 39 (2011) Provided by: Arthur W. Diamond Law Library, Columbia University Content downloaded/printed from HeinOnline Wed May 29 15:10:28 2019 -- Your use of this HeinOnline PDF indicates your acceptance of HeinOnline's Terms and Conditions of the license agreement available at https://heinonline.org/HOL/License -- The search text of this PDF is generated from uncorrected OCR text. -- To obtain permission to use this article beyond the scope of your HeinOnline license, please use: Copyright Information Use QR Code reader to send PDF to your smartphone or tablet device THE IMPACT OF THE CRIMINAL LAW AND MONEY LAUNDERING MEASURES UPON THE ILLICIT TRADE IN ART AND ANTIQUITIES Janet Ulph* INTRODUCTION A cursory glance at the pages of any daily newspaper will reveal that the theft of works of art and antiquities from private museums and collections is a serious problem. It is estimated that the international trade in looted stolen or smuggled cultural property is worth several billion US dollars per year. ' One needs to look no further than the theft in 2010 of five irreplaceable paintings by Picasso, Matisse, Braque, Modigliani and Leger from the Muse d'Art Moderne in Paris in May 2010.2 The disappearance of these prized objects is a source of distress, not only because those who visit the museum are now deprived of the pleasure of viewing them, but also because of fears that the objects might be damaged in the process of theft, as where a painting is cut from its frame, or that it may subsequently be stored in poor conditions. -

Q&A Criminal Law 2E © Mischa Allen, 2018

Allen: Q&A Criminal Law 2e Chapter 9: Mixed Questions Question 1 Robin met Louise one night at a disco. After the dancing had finished, Louise invited him back to her flat for a drink. Robin accepted and escorted Louise home where she drank several whiskies and became very drunk. Robin proposed sexual intercourse but Louise resisted and eventually fell asleep. Robin then had sexual intercourse with her both vaginally and anally. The next week, Robin invited Sandra out for a meal and afterwards they returned to her flat. Robin told Sandra that he was David Beckham’s brother and that if she had sexual intercourse with him he would arrange a meeting with the famous football player. This was untrue. Sandra agreed to the request. Six months later, both Louise and Sandra discovered that they were infected with HIV. Discuss any criminal liability arising from these facts. Answer guidance Firstly, the offence of rape under the Sexual Offences Act 2003. should be considered. The offence takes place where the defendant intentionally penetrates the victim without a reasonable belief in consent (s1 Sexual Offences Act 2003). S74, working along side s1 defines consent in the following terms: a person consents when she agrees by choice, and has the freedom and capacity to make that choice. That capacity is limited if the victim is drunk. The Act also allows the jury to presume lack of consent in certain circumstances, including a situation in which the victim is asleep or otherwise unconscious (s75(2)(d). It is unlikely that the jury will accept that Robin had a reasonable belief in Louise’s consent. -

Former Citigroup and UBS Trader Convicted in Libor Case the New York Times

8/6/2015 Former Citigroup and UBS Trader Convicted in Libor Case The New York Times http://nyti.ms/1N4llzh CLOSE X Former Citigroup and UBS Trader Convicted in Libor Case By CHAD BRAY AUG. 3, 2015 LONDON — Tom Hayes, a former trader at Citigroup and UBS, was convicted Monday on eight counts of conspiring to manipulate a global benchmark interest rate known as Libor, bolstering efforts by prosecutors here to pursue financial wrongdoing. Shortly after the verdict, Mr. Hayes was sentenced to 14 years in prison. The verdict came more than three years after a conspiracy among traders to manipulate the London interbank offered rate, or Libor, first came to light. The ensuing scandal has led to billions of dollars in fines and has rocked the reputations of some of the world’s biggest banks, including Barclays, the Royal Bank of Scotland, UBS and Deutsche Bank. Mr. Hayes, 35, was the first person to go to trial in Britain on criminal charges related to Libor manipulation, and his case was seen as a bellwether for British authorities, who have been criticized in the United States for not being as aggressive as the Justice Department when it comes to pursuing financial crime. A second trial of former traders who have been accused of conspiring with Mr. Hayes is set for September on charges related to the manipulation of Libor. A third trial of other individuals accused of manipulating Libor as it relates to the United States dollar is set for January. “The jury were sure that in his admitted manipulation of Libor, Hayes was indeed dishonest,” David Green, the director of the Serious Fraud Office, said in a news release.