Banking and the Limits of Professionalism I

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Assigning Responsibilities in the Libor Scandal

1233 The Differential Management of Financial Illegalisms: Assigning Responsibilities in the Libor Scandal Thomas Angeletti How, in a context of growing critiques of financialization, can law contribute to protecting the legitimacy of finance? This paper argues that the assign- ment of responsibilities between individuals and organizations plays a deci- sive role, using the recent Libor scandal as an empirical illustration. To do so, the paper offers a Foucauldian framework, the differential management of financial illegalisms, dedicated to the study of illegalities in financial capi- talism. The comparison of the legal treatment of two manipulations of Libor, this key benchmark in financial markets, reveals how mid-level traders have been the object of criminal prosecution, while law undervalued the role of top managers and organizations. To capture how differential management is performed in practice, I analyze precisely how the conflict-resolution devices (criminal trial vs. settlement) and the social categorizations prevailing in the two manipulations of Libor favor different forms of responsibility, individual or organizational. I conclude by exploring the implications of law’s relation- ship to financial legitimacy. For more than a decade now, the financialization of capitalism (Krippner 2011; Van der Zwan 2014) has been the locus of many critiques. Financialization has been studied sufficiently to under- stand how much finance has invaded our daily lives (Martin 2002), without measuring necessarily fully its ramifications. The clear causality between the rise of wages in the financial sector and the rise in income inequality in the United Kingdom (Bell and Van Reenen 2013), the United States (Volscho and Kelly 2012), and France (Godechot 2012) has put the financial sector on the spot. -

The Unbelievable Story of an Awkward Maths Genius, A

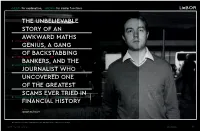

<HELP> for explanation, <MENU> for similar functions LieBOR THE UNBELIEVABLE STORY OF AN AWKWARD MATHS 1) Tom Hayes (Trader) -10.12 GENIUS, A GANG OF BACKSTABBING 2) Tom's Brokers (Cabal) -66.69 BANKERS, AND THE 3) David Enrich (Author) 21.03 JOURNALIST WHO UNCOVERED ONE OF THE GREATEST SCAMS EVER TRIED IN 4) The Libor rigging scandal (Global Crisis) -176.12 FINANCIAL HISTORY Words by Joseph Bullmore The trader at the centre of the scandal: Asperger's sufferer Tom Hayes, currently serving an 11-year term in jail GENTLEMAN’S JOURNAL FEATURES 77 he Libor is the most important number in the world. It’s also probably the they didn’t raise suspicions harems of escorts – and often all five in com- THE How they did it... THE most boring. A single figure that underpins modern capitalism, the Libor (or SCAM among their managers, while EXCESS bination. Some stories were too salacious to T London Interbank Offered Rate) is the theoretical rate at which banks will their managers would invariably Trader 1: make the final edit. ‘This one broker – he lend to each other – the price, essentially, of borrowed money. The magazine you turn a blind eye in the face of ‘What's the call called himself Danny the Animal – was brag- hold in your hands at this very moment is drenched in Libor – it soaks through the ‘The thing about Tom is he’s very literal – no healthy profit spikes. (‘Where on the Libor?’ ‘At a certain point during my in- ging about how he’d stocked a boat in the credit card you used to pay for it, the price of printing ink, the mortgage overheads sense of sarcasm or subtlety,’ Enrich tells me. -

2020 Impact Report

IMPACT REPORT 2020 ABOUT THIS REPORT This report covers United Way’s 2020 fiscal year (July 1, 2019 through June 30, 2020). For the latest information about our work, visit YourUnitedWay.org. CONTENTS INTRODUCTION 4 OUR SERVICE AREA 6 STEPS TO SUCCESS 7 LETTER FROM JAMES L. M. TAYLOR, PRESIDENT & CEO 8 LETTER FROM LORI ELLIOTT JARVIS, BOARD CHAIR 8 2020 BOARD OF DIRECTORS 9 FUNDING 10 2020-22 COMMUNITY INVESTMENTS 12 COMMUNITY VOLUNTEERS 14 UNITED WAY IN THE COMMUNITY 16 KINDERGARTEN COUNTDOWN CAMP 18 VOLUNTEER INCOME TAX ASSISTANCE 20 WORKFORCE PARTNERSHIP TEAM 24 VOLUNTEERING 27 CORPORATE PARTNERSHIPS 32 COVID-19: LEADERSHIP IN A TIME OF CRISIS 34 2020 STEPS TO SUCCESS AWARDS 36 GIVING COMMUNITIES 38 2020 FINANCIALS 48 Impact Report | 3 INTRODUCTION 4 | United Way of Greater Richmond & Petersburg Impact Report | 5 OUR SERVICE AREA We serve the region’s neighborhoods and rural areas alike – 11 localities in all. 6 | United Way of Greater Richmond & Petersburg STEPS TO SUCCESS Our Steps to Success model identifies nine key milestones on the path to prosperity and serves as the framework for everything we do. Impact Report | 7 FROM OUR LEADERSHIP September 2020 September 2020 Thank you for reading United Way of Greater Richmond & Our region is changing rapidly, and the needs of our communities Petersburg’s 2020 Impact Report. I am glad to be able to share this are changing just as quickly. That has never been truer than it is moment of reflection with you. right now in 2020. 2020 has been a challenging and tumultuous year for everyone in Now more than ever, United Way of Greater Richmond & our region. -

Form 20F (SEC Filing) 2012

Lloyds Banking Group plc 2012 Annual Report on Form 20-F As filed with the Securities and Exchange Commission on 25 March 2013 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR X ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended 31 December 2012 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 001-15246 LLOYDS BANKING GROUP plc (previously Lloyds TSB Group plc) (Exact name of Registrant as Specified in Its Charter) Scotland (Jurisdiction of Incorporation or Organization) 25 Gresham Street London EC2V 7HN United Kingdom (Address of Principal Executive Offices) Claire Davies, Group Secretary Tel +44 (0) 20 7356 1043, Fax +44 (0) 20 7356 3506 25 Gresham Street London EC2V 7HN United Kingdom (Name, telephone, e-mail and/or facsimile number and address of Company contact person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Ordinary shares of nominal value 10 pence each, represented by American Depositary Shares ................................The New York Stock Exchange 7.75% Public Income Notes due 2050 ...................................................................................................................................The -

Building the 'Go-To' Bank

Building the ‘Go-To’ bank Citizenship Report 2013 About this report CitizenshipC Report 2013 AnnualA Report 2013 BarclaysB Citizenship Report BarclaysB Annual Report providesp a comprehensive includesi the Strategic viewv of performance against report,r the Governance ouro 2015 Citizenship Plan. report,r Risk review and thet Financial report – WeW also release supporting Building the ‘Go-To’ bank Building the ‘Go-To’ bank includingi our audited information,i including our fi nancial statements. reportingr protocol, full independanti assurance statements and GRI index. Citizenship Report Annual Report 2013 2013 Visit: barclays.com/citizenshipreport Visit: barclays.com/annualreport Guide to navigation buttons Go to main contents page Go to next page Where you see this icon it refers you to more information online: barclays.com/citizenshipreport This icon indicates a cross-reference within this document, please Return to last page visited Go to preceding page follow the page number for more information Basis of preparation business strategy, capital, leverage and other regulatory ratios, payment of The Citizenship Report (the Report) gives a comprehensive account of dividends (including dividend pay-out ratios), projected levels of growth in Barclays’ performance in 2013 across a range of social, ethical and thebanking and fi nancial markets, projected costs, original and revised environmental areas. It outlines progress on the priorities and targets commitments and targets in connection with the Transform Programme, identifi ed in our 2015 Citizenship Plan, and how we are addressing issues deleveraging actions, estimates of capital expenditures and plans and identifi ed as important to both our business and stakeholders. objectives for future operations and other statements that are not historical fact. -

Blinded by Volcker, Vickers, Liikanen, Glass Steagall and Narrow Banking

Randall D. Guynn and Patrick S. Kenadjian Structural Solutions: Blinded by Volcker, Vickers, Liikanen, Glass Steagall and Narrow Banking The phrase “structural solution” is a polite term for breaking up the banks. These “solutions” are presented as the key to solving the problem of “too big to fail” (TBTF).¹ They come in three main varieties, one in the United States (the Volcker Rule), one in the United Kingdom (the Vickers Report) and one in the European Union (the Liikanen Report). The problem they seek to address is real. It is the dilemma faced by public authorities when confronted with the potential failure of a financial institution that could result in destabilizing the financial system in a country or region under conditions of uncertainty and in the absence of appro- priate tools to contain the adverse consequences of failure on the financial sys- tem and the broader economy. Enormous amounts of public resources were de- voted to supporting the financial system in 2008/2009. In some cases this support resulted in increasing public sector debt to levels that make a repeat of public support on a similar level hard to conceive of even if public opinion would tolerate it. Thus, solving TBTF is crucial both to the financial sector and to the common good. But the “structural solutions” proposed are illusory, at best are complementary to other more targeted measures being actively pur- sued, and at worst divert valuable attention and resources away from more tar- geted solutions.² They are perhaps best understood as threats of what could hap- pen to financial institutions if these other measures are not implemented in a timely and credible manner, rather than as real solutions to the TBTF problem. -

The Libor Scandal: a Need for Revised National and International Reforms and Regulations

North East Journal of Legal Studies Volume 32 Fall 2014 Article 4 Fall 2014 The Libor Scandal: A Need For Revised National And International Reforms And Regulations Roy J. Girasa [email protected] Richard J. Kraus [email protected] Follow this and additional works at: https://digitalcommons.fairfield.edu/nealsb Recommended Citation Girasa, Roy J. and Kraus, Richard J. (2014) "The Libor Scandal: A Need For Revised National And International Reforms And Regulations," North East Journal of Legal Studies: Vol. 32 , Article 4. Available at: https://digitalcommons.fairfield.edu/nealsb/vol32/iss1/4 This item has been accepted for inclusion in DigitalCommons@Fairfield by an authorized administrator of DigitalCommons@Fairfield. It is brought to you by DigitalCommons@Fairfield with permission from the rights- holder(s) and is protected by copyright and/or related rights. You are free to use this item in any way that is permitted by the copyright and related rights legislation that applies to your use. For other uses, you need to obtain permission from the rights-holder(s) directly, unless additional rights are indicated by a Creative Commons license in the record and/or on the work itself. For more information, please contact [email protected]. 89 / Vol 32 / North East Journal of Legal Studies THE LIBOR SCANDAL: A NEED FOR REVISED NATIONAL AND INTERNATIONAL REFORMS AND REGULATIONS by Roy J. Girasa* Richard J. Kraus** INTRODUCTION Few individuals or even major investors are aware of the London Interbank Offered Rate (LIBOR), a little-known activity that profoundly affects local and world finances. The total value of securities and loans affected by LIBOR is approximately $800 trillion dollars annually. -

Implementing Volcker, Vickers and Liikanen Comparative Analysis of Bank Structure Reforms

Faculteit Rechtsgeleerdheid Academiejaar 2015-2016 IMPLEMENTING VOLCKER, VICKERS AND LIIKANEN COMPARATIVE ANALYSIS OF BANK STRUCTURE REFORMS Masterproef van de opleiding ‘Master in de rechten’ Ingediend door Robin De Vogelaere (Studentennummer 01102334) Promotor: Prof. Dr. Michel Tison Commissaris: Dhr. Maarten Cleppe 2 Acknowledgement I would like to thank the following people for their contribution to this work. First of all, I would like to thank my promoter, prof. Michel Tison, for providing me with an interesting topic for my master's dissertation and for his help during the writing process. Secondly, I would like to thank my father for proofreading the entire text and my girlfriend, Wiebke, for her help with the lay-out. Finally, I would like to thank my friends and family for their support; and in particular Karel, Vincent and Bertrand who were always available to run ideas by and to provide feedback. Table of Content INTRODUCTION......................................................................................................................1 PART I PURPOSE......................................................................................................................5 I. Purpose of the Volcker rule......................................................................................................7 II. Purpose of retail ring-fencing in the UK................................................................................8 III. Purpose of the separation in the Liikanen Report and its application in continental Europe -

Ring Fencing Volcker's Rule? : the Liikanen Report and Justifications

Munich Personal RePEc Archive Ring fencing Volcker’s Rule? : The Liikanen Report and justifications for ring fencing and separate legal entities revisited Marianne, Ojo North-West University, South Africa 22 January 2016 Online at https://mpra.ub.uni-muenchen.de/70894/ MPRA Paper No. 70894, posted 28 Apr 2016 13:42 UTC 1 ABSTRACT The predecessor paper to this publication, “Volcker/Vickers Hybrid”: The Liikanen Report and Justifications For Ring Fencing and Separate Legal Entities, considered the merits, objectives and cost-benefit attributes of respective models associated with the Vickers Report, Liikanen Report and Volckers Rule – by way of reference to the degree of separation of legal entities or banking activities involved, as well as whether an outright ban or prohibition on proprietary trading is involved. This paper is aimed at highlighting why ring fencing not only presents a more feasible and cost effective option to other models, but also why its degree of flexibility provides the more appropriate balance in a financial environment whose trend is increasingly inclined towards conglomeration. Key Words: Vickers Report, Volcker’s Rule, Liikanen Report, ring fencing, cross-sector services’ risks, liquidity risks, systemic risks, capital requirements, leverage ratios 2 Ring Fencing Volcker’s Rule? : The Liikanen Report and Justifications for Ring Fencing and Separate Legal Entities Revisited Marianne Ojo Professor, North-West University, Faculty of Commerce and Administration, School of Economic and Decision Sciences, Private Bag -

Seven Deadly Sins 359

2017-2018 THE SEVEN DEADLY SINS 359 THE SEVEN DEADLY SINS OF THE CONTEMPORARY FINANCIAL SYSTEM CHENG-YUN TSANG* Abstract This paper identifies and analyzes the fundamental deficiencies, or “Seven Deadly Sins” of the contemporary financial system. The “Sins” are: dominance of an excessive risk-taking culture and behavior, over-reliance on short-term funding, inevitable deficiencies in hedging tools, ignorance of the sources and feedback loops of shadow banking activities, failure to address cognitive bias, over- emphasis on the use of complex regulations, and failure to promote moral restraint and professional standards. An understanding of these sins, together with a brief review of post-crisis reforms, enables policymakers to identify areas where more regulatory effort is needed, or to channel greater market power into the remediation of these fundamental deficiencies. * Assistant Professor, College of Law, National Chengchi University; former Research Fellow, Faculty of Law, UNSW Sydney. This paper draws from a chapter of my doctoral dissertation and therefore special thanks goes to my doctoral supervisor, Professor Lawrence Baxter and other committee members. I would like to express my thanks to the Australian Research Council for their support of the preparation of this paper by the Linkage Grant Project entitled “Regulating a Revolution: A New Regulatory Model for Digital Finance,” to Professor Ross Buckley of UNSW for his mentorship throughout the preparation and submission of this paper, and to Cliff Gadd and Jessica Chapman for exceptional editing assistance. I am also very grateful for the editorial support of this journal. All responsibility is mine. 360 REVIEW OF BANKING & FINANCIAL LAW VOL. -

Former Citigroup and UBS Trader Convicted in Libor Case the New York Times

8/6/2015 Former Citigroup and UBS Trader Convicted in Libor Case The New York Times http://nyti.ms/1N4llzh CLOSE X Former Citigroup and UBS Trader Convicted in Libor Case By CHAD BRAY AUG. 3, 2015 LONDON — Tom Hayes, a former trader at Citigroup and UBS, was convicted Monday on eight counts of conspiring to manipulate a global benchmark interest rate known as Libor, bolstering efforts by prosecutors here to pursue financial wrongdoing. Shortly after the verdict, Mr. Hayes was sentenced to 14 years in prison. The verdict came more than three years after a conspiracy among traders to manipulate the London interbank offered rate, or Libor, first came to light. The ensuing scandal has led to billions of dollars in fines and has rocked the reputations of some of the world’s biggest banks, including Barclays, the Royal Bank of Scotland, UBS and Deutsche Bank. Mr. Hayes, 35, was the first person to go to trial in Britain on criminal charges related to Libor manipulation, and his case was seen as a bellwether for British authorities, who have been criticized in the United States for not being as aggressive as the Justice Department when it comes to pursuing financial crime. A second trial of former traders who have been accused of conspiring with Mr. Hayes is set for September on charges related to the manipulation of Libor. A third trial of other individuals accused of manipulating Libor as it relates to the United States dollar is set for January. “The jury were sure that in his admitted manipulation of Libor, Hayes was indeed dishonest,” David Green, the director of the Serious Fraud Office, said in a news release. -

P.R.I.M.E. Finance Panel of Recognized International Market Experts in Finance

P.R.I.M.E. Finance Panel of Recognized International Market Experts in Finance Beyond LIBOR: New Benchmarks And New Issues Affecting Benchmarks Presentation by Thomas Werlen 2017 P.R.I.M.E. Finance Annual Conference 23 & 24 January, Peace Palace, The Hague Agenda 1 Scope of the Panel’s Discussions 2 From the LIBOR Scandal to other Benchmark Manipulations 3 Involvement of Authorities 4 Agenda 2 Beyond LIBOR: New Benchmarks and new Issues affecting Benchmarks Benchmarks causing regulatory issues include but are not limited to LIBOR Alternative systems to determine benchmarks are explored due to regulatory and investigatory pressure but also following industry initiatives Investigations are still ongoing and private enforcement is in full steam Goal of today is to update on current developments on all fronts 3 Agenda 1 Scope of the Panel’s Discussions 2 From the LIBOR Scandal to other Benchmark Manipulations 3 Involvement of Authorities 4 Agenda of Panel 4 From LIBOR… (1/2) Benchmark reference rate for debt instruments, including government and corporate bonds, mortgages, student loans, credit cards; as well as derivatives such as currency and interest swaps, among many other financial products In early 2008, New York Fed learns of false reports “we know that we’re not posting, um, an honest rate” (statement of Barclays employee to a New York Fed official) Provoked a series of regulatory actions, e.g.: Barclays settled a case with U.S. and UK authorities for $435 million in July 2012, and in August 2016 agreed to pay an additional $100 million to forty-four U.S.