London Office Crane Survey Activity Rising

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Spring Retail Report 2014

Spring Retail Report 2014 Continued Confidence Crucial Introduction by Graham Chase Who Turned The Switch? In-Town Agency Evolution not Revolution Out-of-Town Agency Prime & Dominant Secondary Assets On The Up Retail Investment PACT - Better The Devil You Know... or Why The Devil Not? Professional Convenience is King Superstores and Supermarkets Localism or Free For All? Planning Who’s who at C&P Key Contacts 01 Contents “The biggest scandal 03 Continued Confidence Crucial affecting retail Introduction by Graham Chase property has been 07 Who Turned The Switch? the Government’s In-Town Agency decision to delay 13 Evolution not Revolution the rating valuation, Out-of-Town Agency creating significant 19 Prime & Dominant Secondary Assets On The Up inequalities and Retail Investment unfairness on 25 PACT - Better The Devil You retail businesses. Know... or Why The Devil Not? The recession and Professional downturn in trade 29 Convenience is King has ravaged various Superstores and Supermarkets parts of the 35 Localism or Free For All? country, particularly Planning those outside of the 39 Who’s who at C&P South East.” Key Contacts Continued Confidence Crucial Introduction by Graham Chase Spring Retail Report 2014 Introduction by Graham Chase Continued Confidence Crucial Introduction 03 Return to Contents Confidence in any market is a crucial ingredient for a positive approach. The retail property sector craves confidence more than most, for it is the consumers and their expenditure that drives this significant and important component of the UK’s economy forward. Confidence Returns in their share price above the FTSE 100 average. Further, the number of published For the first time since the middle of 2007, requirements by retailers reflects expansion some seven years ago, there are clear signs across the board. -

Investment Market Commentary

INVESTMENT MARKET COMMENTARY For the Period 1 October – 31 December 2020 PRIVATE & CONFIDENTIAL APAM Ltd 3 Barrett Street London W1U 1AY T: 0207 963 8858 | E: | W: www.apamuk.com [email protected] As at 6 January 2021 EXECUTIVE SUMMARY On Christmas Eve 2020, the UK and EU agreed a trade deal, ahead of the end of the transition period in January 2021. The deal has been referred to as a framework, with key issues such as financial services, to continue to be debated in the New Year. Yet, the deal represents a key moment in the UK’s exit from the bloc and assuages any concerns over the damaging effects of crashing out in a no-deal scenario. In certain areas, such as tax and state aid, the UK and EU have agreed high level commonality in rules but have not yet fleshed out the details. In other areas, such as farming, the UK has accepted greater friction in trade with the EU in order to assure the flexibility to strike deals with the rest of the world. With the conclusion of the EU trade deal and a separate deal with Turkey, the UK has now signed 62 trade agreements since it left the European Union. The markets have responded positively to the UK’s progress as it endeavours to redefine itself as a forward-thinking green tech hub in the post-Brexit world. After emerging from a month-long lockdown, the UK successfully approved and administered the world’s first COVID-19 vaccine. Markets rallied on the news with the MSCI All-Country World Index climbing by a record 12.2% in November, followed by a correction on 21 December after the discovery of a variant strain of the virus and the imposition of a strict lockdown which is expected to last until February. -

Smithfield Market but Are Now Largely Vacant

The Planning Inspectorate Report to the Temple Quay House 2 The Square Temple Quay Secretary of State Bristol BS1 6PN for Communities and GTN 1371 8000 Local Government by K D Barton BA(Hons) DipArch DipArb RIBA FCIArb an Inspector appointed by the Secretary of State Date 20 May 2008 for Communities and Local Government TOWN AND COUNTRY PLANNING ACT 1990 PLANNING (LISTED BUILDINGS AND CONSERVATION AREAS) ACT 1990 APPLICATIONS BY THORNFIELD PROPERTIES (LONDON) LIMITED TO THE CITY OF LONDON COUNCIL DEVELOPMENT AT 43 FARRINGDON STREET, 25 SNOW HILL AND 29 SMITHFIELD STREET, LONDON EC1A Inquiry opened on 6 November 2007 File Refs: APP/K5030/V/07/1201433-36 Report APP/K5030/V/07/1201433-36 CONTENTS SECTION TITLE PAGE 1.0 Procedural Matters 3 2.0 The Site and Its Surroundings 3 3.0 Planning History 5 4.0 Planning Policy 6 5.0 The Case for the Thornfield Properties (London) 7 Limited 5.1 Introduction 7 5.2 Character and Appearance of the Surrounding Area 8 including the Settings of Nearby Listed Buildings and Conservation Areas 5.3 Viability 19 5.4 Repair, maintenance and retention of the existing buildings 23 5.5 Sustainability and Accessibility 31 5.6 Retail 31 5.7 Transportation 32 5.8 Other Matters 33 5.9 Section 106 Agreement and Conditions 35 5.10 Conclusion 36 6.0 The Case for the City of London Corporation 36 6.1 Introduction 36 6.2 Character and Appearance of the Surrounding Area 36 including the Settings of Nearby Listed Buildings and Conservation Areas 6.3 Viability 42 6.4 Repair, maintenance and retention of the existing buildings -

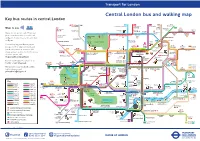

Central London Bus and Walking Map Key Bus Routes in Central London

General A3 Leaflet v2 23/07/2015 10:49 Page 1 Transport for London Central London bus and walking map Key bus routes in central London Stoke West 139 24 C2 390 43 Hampstead to Hampstead Heath to Parliament to Archway to Newington Ways to pay 23 Hill Fields Friern 73 Westbourne Barnet Newington Kentish Green Dalston Clapton Park Abbey Road Camden Lock Pond Market Town York Way Junction The Zoo Agar Grove Caledonian Buses do not accept cash. Please use Road Mildmay Hackney 38 Camden Park Central your contactless debit or credit card Ladbroke Grove ZSL Camden Town Road SainsburyÕs LordÕs Cricket London Ground Zoo Essex Road or Oyster. Contactless is the same fare Lisson Grove Albany Street for The Zoo Mornington 274 Islington Angel as Oyster. Ladbroke Grove Sherlock London Holmes RegentÕs Park Crescent Canal Museum Museum You can top up your Oyster pay as Westbourne Grove Madame St John KingÕs TussaudÕs Street Bethnal 8 to Bow you go credit or buy Travelcards and Euston Cross SadlerÕs Wells Old Street Church 205 Telecom Theatre Green bus & tram passes at around 4,000 Marylebone Tower 14 Charles Dickens Old Ford Paddington Museum shops across London. For the locations Great Warren Street 10 Barbican Shoreditch 453 74 Baker Street and and Euston Square St Pancras Portland International 59 Centre High Street of these, please visit Gloucester Place Street Edgware Road Moorgate 11 PollockÕs 188 TheobaldÕs 23 tfl.gov.uk/ticketstopfinder Toy Museum 159 Russell Road Marble Museum Goodge Street Square For live travel updates, follow us on Arch British -

PRCA Public Affairs Register: Consultancies – September to November 2013

PRCA Public Affairs Register: Consultancies – September to November 2013 Aardvark Communications Office(s) address: 843 Finchley Road London NW11 8NA Tel: 07779 102 758 Email: [email protected] List of employees that have conducted lobbying services: Richard Ellis List of clients for whom lobbying services have been provided: Advantage42 Aiken PR Office(s) address: 418 Lisburn Road, Belfast, BT9 6GN Tel: 028 9066 3000 Fax: 028 9068 3030 Email: [email protected] (office manager) List of employees that have conducted lobbying services: Claire Aiken Lyn Sheridan Shane Finnegan Patrick Finlay List of clients for whom lobbying services have been provided: McDonald’s Diageo APCO WORLDWIDE Office(s) address: 90 Long Acre, London, WC2E 9RA Tel: 020 7526 3620 Fax: 020 7526 3699 Email: [email protected] Website: http://www.apcoworldwide.com/uk List of employees that have conducted lobbying services: Adrian Edwards Alex Clackson Anjali Jingree Alexandra Bigland Alfred von Stauffenberg Ben Steele Bridget Taylor Charlotte Higgo Chris Genasi Christopher Steel Claire Laurence Daniella Lebor Danielle McGuigan David Clark Edward Bird Edward Walsh Elise Martin-Davies Emma Putt Fiona Funke Francis Mote Graham Ackerman James Acheson-Gray Jessica Sullivan Joanne Milroy John Roberts Jolyon Kimble Jenny Runnacles Keir Ferguson Laure Stein Lidia Borisova Lionel Zetter Magdalen Bush Maria Lavrova Martin Sawer Matthew Bostrom Megan Wanee Melis Ogutcu Michael Burrell Phoebe Judd Roger Hayes Rupert Davis Sara Cruz Stephanie Lvovich Thomas Eymond-Laritaz Tom Quayle William Browne William Wallace List of clients for whom lobbying services have been provided: A.I.S.E asbl Arison Investments Ltd Bangko Sentral ng Pilipinas British Association Pharmaceutical Wholesalers (BAPW) BlackBerry Butler Snow PLLC Church of Jesus Christ of the Latter-day Saints Constellium Credit Suisse Cruise Line International Association Danaher UK Industries DEK International DePuy International Dow Corning Dynex S.A. -

Property Investor Profiles AER

Property Investor Profiles AER Aerium Finance Ltd Fund 49 Grosvenor Street, London W1K 3HB AEW UK REIT Plc Tel: 0207 838 7900 Fax: 0207 838 7858 Fund Manager: AEW UK Investment Management LLP Email: [email protected] 33 Jermyn Street, London SW1Y 6DN Web: www.aerium.com Tel: 020 7016 4800 Fax: 020 7016 4700 Contacts Email: [email protected] Franck Ruimy (CEO) Web: www.aeweurope.com Robin Carr (UK Fund Director) Contacts Comment Alex Short (Portfolio Manager) Aerium, which has been established since 1988, currently Comment manages circa €6.1 billion of real estate assets across 12 countries AEW UK REIT Plc was listed on the Official List of the UK Listing and is in the process of raising capital for its seventeenth fund, a Authority and admitted to trading on the Main Market of the London Pan-European Value-Add Fund. (03/15) Stock Exchange on 12 May 2015, raising £100.5m. 02/14 - European real estate fund manager Aerium purchased New 06/15 - AEW UK REIT purchased Eastpoint Business Park, Oxford Uberior House and Princes Exchange in Edinburgh from Invesco for £8.2m, reflecting a net initial yield of 9.4% including rents and for £61.75m. rent guarantees. Eastpoint Business Park, Oxford comprises five self contained office buildings totalling 75,000 sq ft. Tenants 03/15 - Aerium sold a 15% stake in its operating business to include Clarendon Business Centres and Cancer Partners UK. NorthStar Realty Finance Corp Year Ending Dec 2013 Dec 2012 Dec 2011 Fund Turnover £7.92m £8.16m £8.5m Pre-Tax Profit £1.35m £1.35m £0.05m AEW UK South East -

214 Corporate Locations 746 Brands Across the Locations

214 Corporate Locations 746 Brands Across The Locations +39 Offices and Co Working Spaces Jones Lang LaSalle Regents Quarter Cornerstone Research ACCELERATOR LONDON Perception Receptions Palmer Access Financial Services AWS LOFT The Peak Adsatis BATHTUB2BOARDROOM Gatwick Express -Cust Service TL Office Agn International-europe THE BLACK & WHITE BUILDING (TOG) Sky Media - BSKyB Alex Johnson CAMPUS LONDON Perception Receptions Grosvenor Alex Johnson CENTRAL WORKING CITY Perception Receptions Grosvenor Alliance Assurance Company CENTRAL WORKING SHOREDITCH CORP -CBRE St James Allied Irish Bank CENTRAL WORKING WHITECHAPEL Perception Receptions Ryder Alvarez & Marsal CENTRAL WORKING BLOOMSBURY Corp Household Cavalry American Express CENTRAL WORKING DEANSGATE IHG - Reception Office Shop American Express CLUB WORKSPACE BETHNAL GREEN IHG - Starbucks Coffee shop Axis Corporate Capital UK DIGITAL CATAPULT CENTRE Telefonica UK Ltd Banif EAST TUB (BATHTUB2BOARDROOM) Portman Square Bank of America Merril Lynch ENTIQ\COGNICITY Invesco Bank Of China IDEALONDON Portico - York House Bank of Yokohama LAUNCH 22 Sony DADC BC Partners LEVEL39 Perception Receptions New Cavendish Berenberg Bank LIVERPOOL ST (TOG) G4S Integrated Services (UK) Ltd Brewin Dolphin LONDON & PARTNERS GVA Acuity reception rack 1 Brown Brothers Harriman MASS CHALLENGE GVA Acuity reception rack 2 Business Finance Universe RAINMAKING LOFT Aker Solutions Building 6 BVCA ROCKSTAR HUBS Enjoy work Reception Building 1-11 Canaccord Genuity TECH HUB LONDON Enjoy work Reception Building 1-11 Capita Insurance Services TECH HUB SHOREDITCH Enjoy work Reception Building 1-11 Caspar Property Nominee Holdings Ltd THE BAKERY WORLDWIDE Enjoy work Reception Building 1-11 CBPE Capital THE CUBE Enjoy work Reception Building 1-11 CBRE (Gresham Street) THE TRAMPERY Enjoy work Reception Building 1-11 CBRE (Wood Street) WEWORK DEVONSHIRE SQ. -

Aldersgate Street London EC1A 4JQ

124 Aldersgate Street London EC1A 4JQ Charming self-contained Charming self-contained warehouse style office warehouse style office freehold with its own freehold with its own courtyard & rear garden courtyard & rear garden For Sale For Sale The Opportunity • Character Clerkenwell freehold, close to Smithfield, Farringdon and Barbican • Converted warehouse office building comprising a Net Internal Area of 4,981 sq ft (462.7 sq m) and a Gross Internal Area of 6,173 sq ft (573.5 sq m) • B1 officese u throughout • Exclusive private gated courtyard providing secure car parking for up to 3 cars • Secluded rear walled garden of approx. 1,500 sq ft • Attractive 1st floor terrace of approx. 600 sq ft • Potential to extend subject to securing the necessary consents • Sold with vacant possession on completion • Offers are invited for the freehold interest to include the front courtyard & rear garden Garden Lower Ground Floor Ground Floor Ground Floor Front Entrance The Location Connectivity The building sits in a cul-de-sac off Aldersgate Street with Charterhouse Square to the Barbican Station is within a minutes walk giving access to the Circle, west and Carthusian Street to the south. Clerkenwell Road is 300 metres to the north. Hammersmith & City and Metropolitan Lines. Farringdon Station is within 500 metres (7 minute walk) and is served by the same Tube lines, The immediate area benefits from the amenities of Smithfield Market and Clerkenwell Thameslink and Crossrail (from 2018). St Paul’s Station is a 10 minute walk Green, with a plethora of shops, bars and restaurants. The Barbican Centre, London to the south providing access to the Central Line. -

June 2018 Members 2018

Members 2018 Tourism, Retail and Leisure AB Foods Chelsea Football Club Banking & Financial Services D&D London American Express Delfont Mackintosh Aviva Investors Edwardian Hotels London Barclays Fortnum & Mason Barings Global Blue Deutsche Harrods HSBC Hilton Legal & General J Sainsbury Lloyds Bank Kingfisher Macquarie Marks & Spencer MasterCard Mastercard Pool Reinsurance McDonalds Restaurants Prudential Merlin Entertainments Royal Bank of Scotland NBC Universal State Street Phillip Morris Limited Tristan Capital Partners Primark Starbucks Tate Consultants and Advisors Tesco becg The Barbican Centre Blue Mountain Group The O2 Cratus QVC CIS Security Walgreens Boots Alliance Edelman Whitbread Hotels & Restaurants Field Consulting Fire Protection Association Partnerships & Associations Four Communications ASIS FTI Consulting British Hospitality Association Kanda Communications LLP Heart of London London Communications Agency London First PA Consulting Group New West End Company Odgers Berndtson North London Business Royal Brompton & Harefield NHS Trust Construction & Architecture South Bank Employers’ Group Aedas South London Business Assael Architecture The Security Institute BAM Nuttall West London Business Dar Al-Handasah (Shair and Partners) Farrells Gensler Professional Services Grimshaw Allen & Overy HOK Ashurst Interserve Bryan Cave Leighton Paisner LLP Kier Blick Rothenberg Mace Charles Russell Speechlys Make Clyde & Co Mulalley Deloitte Multiplex Dentons PLP Architecture DLA Piper Skanska EY WestonWilliamson+Partners Freshfields -

Cloister Court Cloister Court

22- 26 FARRINGDON LANE CLOISTERCLOISTER COURTCOURT LONDON EC1 PRIME FARRINGDON FREEHOLD FOR SALE 9.80 YEARS SECURE INCOME 2 CLOISTER COURT INVESTMENT SUMMARY Freehold. Situated in prime Farringdon, one of London’s most sought after office districts. Unrivalled connectivity located 250 metres from Farringdon Station’s Turnmill entrance. Highly coveted former Victorian warehouse building. Comprises 9,459 sq ft (878.7 sq m) of office and retail accommodation arranged over ground and four upper floors. The office accommodation was comprehensively refurbished in 2020. The offices are single let to Your Golf Travel on a lease expiring 30/04/2031 at a passing rent of £550,000 per annum. Total passing rent of £565,000 per annum reflecting £59.74 per sq ft. Minimum guaranteed rental uplift to £576,000 per annum in 2026. Prime Farringdon rents are in excess of £85.00 per sq ft. WAULT of 9.8 years to expiry. Offers in excess of £11,500,000, subject to contract. This reflects a capital value of £1,215 per sq ft and a net initial yield of circa 4.61%, allowing for purchasers costs of 6.71%. 100% of the shares in the holding UK SPV are available, reducing the purchasers costs to 2.3%. 4 CLOISTER COURT CANARY WHARF SMITHFIELD ST PAUL’S OLD STREET LIVERPOOL STREET BARBICAN FARRINGDON MARKET CATHEDRAL CITY OF SHOREDITCH MOORGATE LONDON MIDTOWN CLOISTER COURT CHANCERY LANE CLERKENWELL GREEN LEATHER LANE MARKET FARRINGDON (TURNMILL STREET ENTRANCE) 6 CLOISTER COURT FARRINGDON Farringdon is one of Central London’s most exciting and diverse commercial districts. -

Marylebone Lane Area

DRAFT CHAPTER 5 Marylebone Lane Area At the time of its development in the second half of the eighteenth century the area south of the High Street was mostly divided between three relatively small landholdings separating the Portman and Portland estates. Largest was Conduit Field, twenty acres immediately east of the Portman estate and extending east and south to the Tyburn or Ay Brook and Oxford Street. This belonged to Sir Thomas Edward(e)s and later his son-in-law John Thomas Hope. North of that, along the west side of Marylebone Lane, were the four acres of Little Conduit Close, belonging to Jacob Hinde. Smaller still was the Lord Mayor’s Banqueting House Ground, a detached piece of the City of London Corporation’s Conduit Mead estate, bounded by the Tyburn, Oxford Street and Marylebone Lane. The Portland estate took in all the ground on the east side of Marylebone Lane, including the two island sites: one at the south end, where the parish court-house and watch-house stood, the other backing on to what is now Jason Court (John’s Court until 1895). This chapter is mainly concerned with Marylebone Lane, the streets on its east side north of Wigmore Street, and the southern extension of the High Street through the Hinde and part of the Hope–Edwardes estates, in the form of Thayer Street and Mandeville Place – excluding James Street, which is to be described together with the Hope–Edwardes estate generally in a later volume. The other streets east of Marylebone Lane – Henrietta Place and Wigmore Street – are described in Chapters 8 and 9. -

The Flexible Workspace Market Contents

GREEN KINNEAR The Flexible Workspace Market Contents Contents 1. The flexible workspace market – p3 2. Types of flexible workspace – p5 3. Drivers of the flexible workspace market – p6 4. Operator income streams – p8 5. Opportunities for landlords – p9 6. Valuation – p11 7. The future of flexible workspace – p13 8. About GKRE – p16 The Collective Old Oak, NW10 2 The flexible workspace market The flexible The Space High Holborn, WC1 The flexible workspace market t is no exaggeration to say that there has been • Around two thirds of the flexible workspace Ia revolution in the workplace over the past run by the top operators is outside London, few years. Flexible workspace has moved from as shown in our table on page 7. the fringes of the market to centre stage with demand continuing to grow year on year. • The UK flexible workspace sector is UK flexible estimated to be worth £16bn using Britain is at the forefront of this revolution, traditional valuation methods, although workspace sector leading the way in offering a working taking into account additional income from environment that meets the needs of the services supplied by operators it has been estimated worth 21st century occupier. estimated it is worth close to £19bn. This could rise to £62bn by 2025.* Key flexible office market statistics: • With 52% of global office space either £16bn • The flexible workspace market in the UK vacant or unused, the expectation is that accounts for around 36% of the world the flexible workspace market will increase market. significantly– currently, it represents 8% of global office space.**JLL estimates that 30% • There are approximately 3,300 centres of office space will be co-working space by in the UK, with over 5m square feet in 2030.