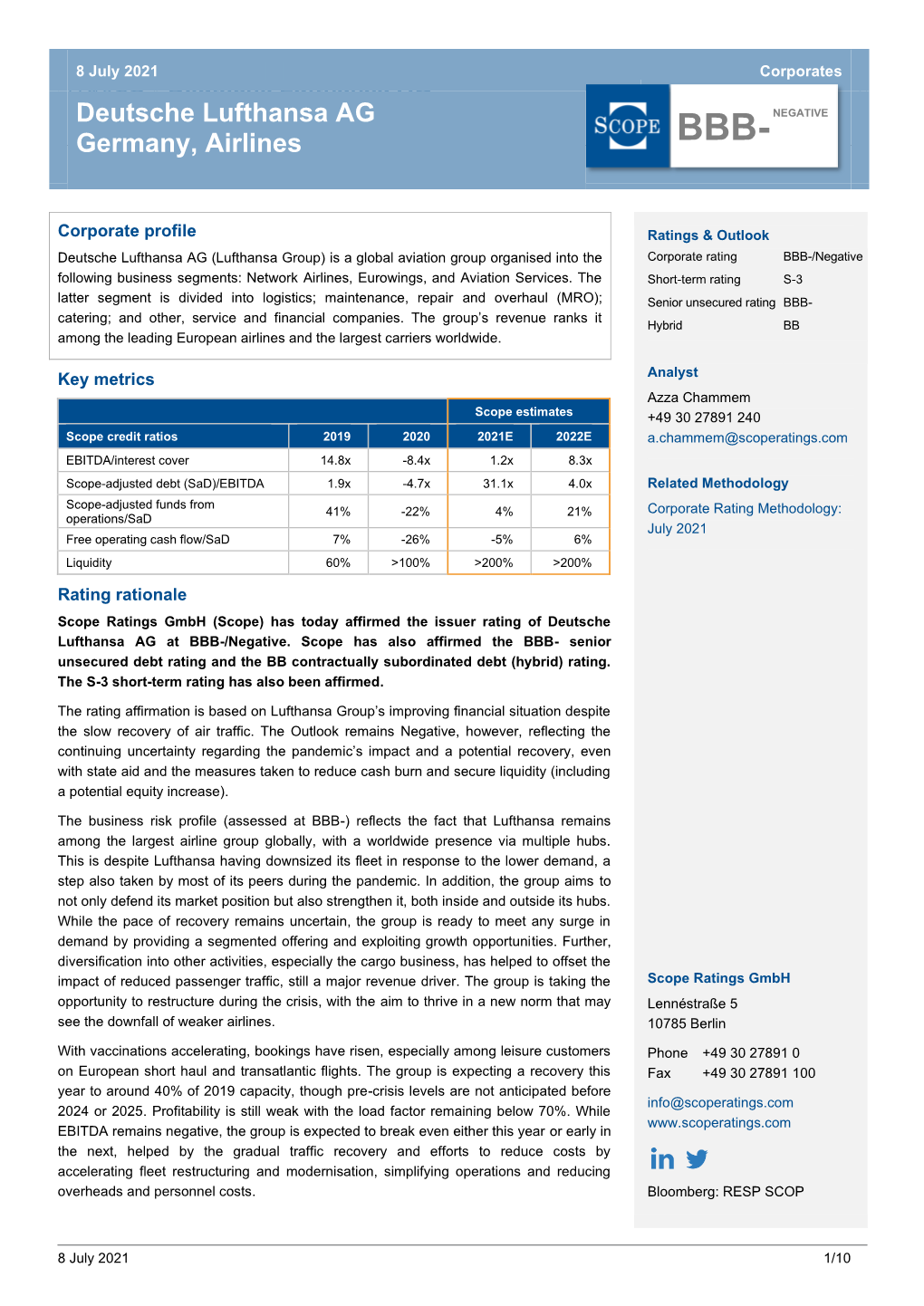

Deutsche Lufthansa AG

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Risk & Reward in Aircraft Backed Finance

Modeling Aircraft Loan & Lease Portfolios 3rd revision Discussion Notes October 2017 Modeling Aircraft Loans & Leases Discussion notes December 2013 2 PK AirFinance is a sub-business of GE Capital Aviation Services (GECAS). The company provides and arranges debt to airlines and investors secured by commercial aircraft. Cover picture by Serge Michels, Luxembourg. 3 Preface These discussion notes are a further update to notes that I prepared in 2010 and revised in 2013. The issues discussed here are ones that we have pondered over the last 25 years, trying to model aircraft loans and leases quantitatively. In 1993, Jan Melgaard (then at PK) and I worked with Bo Persson in Sweden to develop an analytic model of aircraft loans that we called SAFE. This model evolved into a Monte Carlo simulation tool, Lending EDGE, that was taken into operation at PK in 2012 and validated under ISRS 4400 by Deloitte in 2013. I have now made some corrections and amendments to the previous version, based on helpful feed-back from industry practitioners and academics. I have added a section on Prepayment Risk in loans and expanded on Jurisdiction Risk. My work at PK AirFinance has taught me a lot about risks and rewards in aircraft finance, not least from the deep experience and insight of many valued customers and my co-workers here at PK and at GECAS, our parent company, but the views and opinions expressed herein are my own, and do not necessarily represent those of the General Electric Company or its subsidiaries. In preparing these notes, I have been helped by several people with whom I have had many inspiring discussions. -

Onboard Retail LSG Sky Chefs – Catering And

LETTER FROM THE EXECUTIVE BOARD AN INDUSTRY-LEADING NETWORK THE LSG GROUP - POSITIONING04 A GLANCE AT THE OPERATIONS 30 MARKET ENVIRONMENT06 CULINARY EXCELLENCE 32 PRODUCT PORTFOLIO08 ENVIRONMENTAL MANAGEMENT 34 STRATEGIC TRANSFORMATION10 PROVEN EXCELLENCE 38 COURSE OF BUSINESS18 OUTLOOK 40 FINANCIAL PERFORMANCE20 CONSOLIDATED INCOME STATEMENT 42 WORLDWIDE PRESENCE24 44KEY FIGURES 25 45 We look forward LETTER FROM THE EXECUTIVE BOARD to exploring with Dear reader, Once again, we gratefully look back at another year of growth Significant steps have been taken in the transformation of the for our industry. Despite looming turbulence over the world‘s LSG Group. Today, we are able to offer a complete portfolio of you. economy, developments in our key areas of activities – air and products and services for a variety of industries. In the backend, rail travel, as well as convenience retail – were positive around we are changing our operational landscape to become even more the globe. This has certainly laid a solid foundation for the flexible through a market-oriented mix of production modules continued good performance achieved by our company. and tailored logistics. And, most importantly, the processes throughout our value chain are progressively growing in The relative stability of our environment has allowed us to focus consistency, leading to higher efficiency. on the improvement of our processes in terms of standardization, sharing of best practices and learning from each other. Thus, Moving forward, we will concentrate on taking advantage of in addition to a satisfying financial result, we have also attained the multiple opportunities offered by digitalization in creating a remarkable operational standard underlined by quality and new products and applications, facilitating our workflows and sustainability. -

2019 Embraer Aircraft Finance Outlook

2019 EMBRAER AIRCRAFT FINANCE OUTLOOK 1 FORWARD LOOKING STATEMENT This presentation includes forward- looking statements or statements about events or circumstances which have not occurred. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting our business and our future financial performance. These forward-looking statements are subject to risks, uncertainties and assumptions, including, among other things: general economic, political and business conditions, both in Brazil and in our market. The words “believes”, “may”, “will”, “estimates”, “continues”, “anticipates”, “intends”, “expects” and similar words are intended to identify forward-looking statements. We undertake no obligations to update publicly or revise any forward- looking statements because of new information, future events or other factors. In light of these risks and uncertainties, the forward-looking events and circumstances discussed in this presentation might not occur. Our actual results could differ substantially from those anticipated in our forward- looking statements. New York INTRODUCTION The aircraft financing market constitutes one of the are likely to benefit from one of the lowest funding most important pillars of the aviation industry. costs levels in history. There is now a broader range Commercial airplanes are large capital investments that of qualified options available to airlines and lessors. may surpass double digit percentages of aviation total The robust global aircraft financing environment, is operating costs. The aircraft financing market is crucial also seen in the up to 150 seat aircraft category, which for airlines, lessors and OEMs to efficiently manage forecasts financing demand of approximately US$ 7.2 such invesments and maximize their profitability. -

Aspects of Insurance in Aviation Finance Rod D

Journal of Air Law and Commerce Volume 62 | Issue 2 Article 4 1996 Aspects of Insurance in Aviation Finance Rod D. Margo Follow this and additional works at: https://scholar.smu.edu/jalc Recommended Citation Rod D. Margo, Aspects of Insurance in Aviation Finance, 62 J. Air L. & Com. 423 (1996) https://scholar.smu.edu/jalc/vol62/iss2/4 This Article is brought to you for free and open access by the Law Journals at SMU Scholar. It has been accepted for inclusion in Journal of Air Law and Commerce by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu. ASPECTS OF INSURANCE IN AVIATION FINANCE ROD D. MARGO* TABLE OF CONTENTS I. INTRODUCTION .................................. 424 II. THE NATURE OF INSURANCE ................... 428 A. INSURABLE INTEREST ............................ 430 B. THE DUTY OF DISCLOSURE ...................... 430 1. Good Faith .................................. 430 2. Nondisclosure and Misrepresentation.......... 431 III. THE INTERNATIONAL AVIATION INSURANCE M A RKET ........................................... 433 IV. THE ROLE OF THE INSURANCE BROKER ...... 435 V. CERTIFICATES OF INSURANCE AND LETTERS OF UNDERTAKING ............................... 437 VI. TYPES OF COVERAGE ............................ 439 A. HULL INSURANCE ............................... 439 B. LIABILITY INSURANCE ............................ 442 1. PassengerLiability Insurance ................. 443 2. Third Party Liability Insurance ............... 444 C. WAR AND ALLIED PERILS INSURANCE ............ 445 VII. PROTECTING THE INTERESTS OF FINAN CIERS ....................................... 449 A. PROTECTING THE INTERESTS OF FINANCIERS UNDER A HULL POLICY ......................... 449 1. Additional Insured Endorsement .............. 450 2. Loss Payable Clause.......................... 450 * Member of the California and District of Columbia bars; Partner, Condon & Forsyth, Los Angeles; Lecturer in law, UCLA School of Law, Los Angeles. I have received helpful advice and comments from individuals too numerous to men- tion. -

Global Transportation Finance Newsletter August 2021 in This Issue the ABC to AFIC and Balthazar: Overview of Aircraft Non-Payment Insurance Products

Global Transportation Finance Newsletter August 2021 In This Issue The ABC to AFIC and Balthazar: Overview of Aircraft Non-Payment Insurance Products....................................1 Put Option Agreements in Aviation Financing...................5 Biden Administration Economic Sanctions Developments Delineate Allies and Enemies.............................................8 The ABC to AFIC and Balthazar: Team News Overview of Aircraft Non-Payment Insurance Products A number of years have now passed since the terms “AFIC” and “Balthazar” first appeared in the aviation finance market. Since their inception, the Aircraft Non-Payment Insurance (“ANPI”) product has been used by many airlines, leasing companies and other market participants as an alternative source of finance for new aircraft beyond the traditional sources of aviation finance, including financings supported by the European Export Credit Agencies and the Export-Import Bank of the United States. However, despite becoming more prevalent and even with the recent notable closings of aircraft financings supported by the ANPI product, many aviation market participants still seem unsure what these ANPI products are or how they work. The ANPI product is a similar concept to export credit support that provides an insurance policy (rather than a guarantee) to lenders, who rely on the credit of the insurers underlying the ANPI product. At its core, the ANPI product protects investors from payment defaults by obligors (namely, customers Vedder Price Is Recognized in predominantly made up of airlines and leasing companies, who for the purposes of this note, shall be Multiple Top Deal Awards at Airline referred to as the “Customer”). The insurers underlying the ANPI product assume the Customer’s credit Economics “Aviation 100 Deals of risk as well as the residual value, jurisdictional and structural risks of the financing transaction. -

Aviation Industry Leaders Report 2021: Route to Recovery

The Aviation Industry Leaders Report 2021: Route to Recovery www.aviationnews-online.com www.kpmg.ie/aviation KPMG REPORT COVERS 2021.indd 1 20/01/2021 14:19 For what’s next in Aviation. Navigating Change. Together. Your Partner For What’s Next KPMG6840_Aviation_Industry_Leaders_Report REPORT COVERS 2021.indd 2021 2 Ads x 4_Jan_2021.indd 4 19/01/202120/01/2021 15:37:29 14:19 CONTENTS 2 List of 10 Regional Review 24 Airline Survivorship 36 Return of the MAX 54 Chapter Four: The Contributors and Post-Covid World Acknowledgements Chapter One Assessing which Boeing’s 737 MAX incorporates a regional airlines will survive the aircraft was cleared for The recovery from 4 Foreword from Joe review of the aviation immediate health crisis return to service after the devastation the O’Mara, Head of market. and the subsequent the US Federal Aviation coronavirus pandemic Aviation, KPMG recovery period has Administration officially has wrought on the 18 Government rescinded the grounding world is expected to be Ireland become an essential Lifelines skill for lessors, lenders order. Industry experts slow but how will the 6 Chapter One: and suppliers. discuss the prospects new world environment This section takes a for the aircraft type and impact demand for air Surviving the Crisis deep dive into the levels 28 Chapter Two: Fleet how it will be financed. travel. This chapter also of government support considers the impact This chapter considers Focus for the aviation industry 44 Chapter Three: The of climate change the macroeconomic and around the world and Airlines are likely to Credit Challenge concerns on the aviation geopolitical shock of the considers its impact emerge from the crisis coronavirus pandemic industry. -

Valuation Of

Valuation of and the Changing Market Environment Following the Insolvency of Airberlin Program: MSc Applied Economics and Finance Authors: Karen Patricia Steffe (Student number: 106981) Maria Frederiksen (Student number: 57417) Supervisor: Bo Danø Date of submission: 15th of May, 2018 Master Thesis Copenhagen Business School 2018 Number of pages: 114 Executive Summary This master thesis is a valuation of Lufthansa Group as of December 31st, 2017 in light of the changing market environment driven by the insolvency of airberlin Group. Objective The airline industry is at constant change § The objective of this Some structural challenges increasingly define the business master thesis is to environment for Lufthansa with large implications on the corporate evaluate the share price of Lufthansa Group within agenda. Since the liberalization of the EU flight market, competition its current market position significantly increased. The entry of Low Cost Carriers as well as and to give an outlook on ongoing consolidation in the sector puts high pressure on ticket industry changes prices, while costs are driven by fuel expenses as well as following the insolvency employees’ salaries and wages. of airberlin. Insolvency of airberlin strengthens Lufthansa’s market position Lufthansa at a Glance Through the insolvency of airberlin, Lufthansa’s market share on § Founded in 1926, intra-German flights increased from 69% to 87%, making it the Lufthansa Group is based dominant player in this country. It also helped Lufthansa to report a in Germany and is record high net income in 2017 and made the share price increase currently the largest by almost 150% during that year. -

Deutsche Lufthansa Aktiengesellschaft in Respect of Non-Equity Securities Within the Meaning of Art

Base Prospectus 17 November 2020 This document constitutes the base prospectus of Deutsche Lufthansa Aktiengesellschaft in respect of non-equity securities within the meaning of Art. 2 (c) of Regulation (EU) 2017/1129 of the European Parliament and of the Council of June 14, 2017 (the “Prospectus Regulation”) for the purposes of Article 8(1) of the Prospectus Regulation (the “Base Prospectus”). Deutsche Lufthansa Aktiengesellschaft (Cologne, Federal Republic of Germany) as Issuer EUR 4,000,000,000 Debt Issuance Programme (the “Programme”) In relation to notes issued under this Programme, application has been made to the Commission de Surveillance du Secteur Financier (the “CSSF”) of the Grand Duchy of Luxembourg (“Luxembourg”) in its capacity as competent authority under the Luxembourg act relating to prospectuses for securities dated 16 July 2019 (Loi du 16 juillet 2019 relative aux prospectus pour valeurs mobilières et portant mise en oeuvre du règlement (UE) 2017/1129, the “Luxembourg Law”) for approval of this Base Prospectus. The CSSF only approves this Base Prospectus as meeting the standards of completeness, comprehensibility and consistency imposed by the Prospectus Regulation. Such approval should not be considered as an endorsement of the economic or financial opportunity of the operation or the quality and solvency of the Issuer or of the quality of the Notes that are the subject of this Base Prospectus. Investors should make their own assessment as to the suitability of investing in the Notes. By approving this Base Prospectus, the CSSF does not assume any responsibility as to the economic and financial soundness of any issue of Notes under the Programme and the quality or solvency of the Issuer. -

Titel Zur Ansicht RZ.Indd

Issue 2013 Balance Key data on sustainability within the Lufthansa Group www.lufthansagroup.com/responsibility You will fi nd further information on sustainability within the Lufthansa Group at: www.lufthansagroup.com/responsibility Order your copy of our Annual Report 2012 at: www.lufthansagroup.com/investor-relations 1 Source: Lufthansa Annual Report 2012 2 For the reporting year 2012 the following companies are included: Lufthansa (including Lufthansa CityLine, Air Dolomiti, Eurowings, Contact Air, Augsburg Airways), Lufthansa Cargo, Germanwings, SWISS (including Edelweiss Air) and Austrian Airlines. Excluding the services of third parties as the company can infl u- ence neither performance nor the equipment operated (see also table “Share of third parties” on page 70). 3 Types of fl ights taken into account: all scheduled and charter fl ights. 4 See also table “Fuel consumption” on page 70. 5 Companies referred to as in 2, but including the services of third parties, as these contribute to the Group’s results. Types of fl ights as in 3, but including ferry fl ights, as these represent costs. 6 Balance: segments (operational perspective); Annual Report: distance (customer perspective); one distance can include several segments, e.g. in the event of stops en route. 7 Balance: on the basis of all passengers aboard; Annual Report: on the basis of all revenue passengers. At a glance Business performance data1 2012 2011 Change Revenue million € 30,135 28,734 + 4.9 % of which traffic revenue million € 24,793 23,779 + 4.3 % Operating result million -

LSG Group Labor Dispute Escalating in Key US Market

1 October 2019 Michael Hachey Deputy Director, Research (703) 344-4778 UNITEHERE! [email protected] LSG Group labor dispute escalating in key US market Summary As Deutsche Lufthansa AG (DLAKF) is negotiating a partial or complete sale of LSG group, labor troubles in its airline catering business segment are mounting in the key US market. • LSG Sky Chefs and North American labor union UNITE HERE are far apart on economic issues in ongoing contract negotiations covering all US employees • Tightness in the US labor market and political pressure could drive wages and benefits costs higher • US employees of LSG Sky Chefs voted to authorize strikes and petitioned for release from federal mediation which, if granted, would enable them to strike • North America is LSG Sky Chefs’ largest market, accounting for 53% of external catering revenue in first half-year of 2019 Labor and Management are Far Apart in Ongoing US Labor Negotiations The Master National Agreement with North American labor union UNITE HERE, which covers all of LSG Sky Chefs’ 11,162 employees in the US, is currently amendable. UNITE HERE proposed a $15/hour minimum wage floor, higher annual raises for all employees, and increased spending on health benefits, which Sky Chefs rejected. Currently, hourly wages range from $8.40 - $28.50 with 57% of employees earning less than $15. Workers pay expensive premiums for health insurance, at a cost of over $500/month for family coverage. As of 2018, only 34% of LSG Sky Chefs’ US employees had any employer-provided health insurance coverage and only 9% had coverage for a family member or child. -

Retail Inmotion Expands Agreement with Sunexpress Germany

Retail inMotion expands agreement with SunExpress Germany By Rick Lundstrom on December, 19 2017 | Partnerships, Collaborations & Acquisitions Retail inMotion, the onboard retail specialist of the LSG Group, has extended its existing contract with SunExpress Germany, one of the largest scheduled and charter airline carriers between Europe and Turkey. The new contract is valid for three years and covers full onboard retail management for the airline. Retail inMotion is responsible for designing and managing the airline’s onboard retail program, including category management and the implementation of Vector, their proprietary onboard retail software. The SunExpress onboard retail program consists of around 30 food and beverage items and nearly 70 boutique and duty free articles, which are offered to passengers on board. “The LSG Group is proud to continue the partnership with SunExpress Germany for three more years. We will not only provide our industry leading Retail inMotion technology and take care of the last mile, but Retail inMotion will also further manage the onboard retail program of SunExpress. This is a great sign of trust in our capabilities”, said Lars Redeligx, Chief Commercial Officer Europe at LSG Group. During the airline’s winter schedule, Retail inMotion manages the service of approximately 150 flights per week, which increases to nearly 330 flights per week during the summer schedule. “We are very happy that we could extend our partnership with Retail inMotion as we very much appreciate the flexibility, support and operational reliability of the team,” added Jens Bischof, Managing Director SunExpress. 1 Copyright DutyFree Magazine. All rights reserved. Retail inMotion has been partnering with SunExpress since the airline introduced its onboard retail program in 2014. -

LSG GROUP 2014 ENVIRONMENTAL REPORT PART 1 Company Information

THINKING GREEN LSG GROUP 2014 ENVIRONMENTAL REPORT PART 1 Company Information THE LSG GROUP is the world’s largest provider of in-flight services – COMPANY catering, onboard retail, in-flight equipment and logistics, consulting and lounge services. INFORMATION The company’s extensive culinary excellence and logistics know-how has enabled it to move successfully into adjacent markets, such as train services and retail. LSG Sky Chefs delivers 578 million meals a year, mainly for over 300 airlines at 214 airports in 51 countries. For more information, please visit our website at www.lsgskychefs.com. 2 THINKING GREEN – LSG Group Environmental Report 2014 | 3 PART 2 Environmental Management System ENVIRONMENTAL A SYSTEMATIC APPROACH FOR CONTINUOUS IMPROVEMENT Over the past 20 years, LSG Sky Chefs has developed what is today MANAGEMENT considered the in-flight service industry’s most structured and expansive approach to Environmental Care. SYSTEM This approach permeates everything we do to ensure wide-scale environmental awareness and continuous improvement throughout our worldwide organization, and is designed to meet customers‘ and shareholders‘ environmental expectations. 4 THINKING GREEN – LSG Group Environmental Report 2014 | 5 PART 2 Environmental Management System SYSTEMATIC APPROACH THE LSG GROUP’S APPROACH TO ENVIRONMENTAL RESPONSIBILITY Our whole Environmental Management System is based on the 1 2 Plan-Do-Check-Act principles of ISO 14001. PLAN DO At LSG Group, the Plan-Do-Check-Act cycle lasts three years, after which it is evaluated and adjusted to meet any changing requirements. 4 3 ACT CHECK 6 THINKING GREEN – LSG Group Environmental Report 2014 | 7 PART 2 Environmental Management System OUR POLICY IS THE BASIS OF OUR ENVIRONMENTAL ACTIVITIES ENVIRONMENTAL and contains the mission, guidelines and key elements of our Environmental Management System.