Exports Drive Italian Tanners a Statistical Overview of the Tanning Industry’S Current Status, from the Point of View of Europe’S Largest Leather Maker

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Impacts in Real Estate of Landscape Values: Evidence from Tuscany (Italy)

sustainability Article The Impacts in Real Estate of Landscape Values: Evidence from Tuscany (Italy) Francesco Riccioli 1,* , Roberto Fratini 2 and Fabio Boncinelli 2 1 Department of Veterinary Science—Rural Economics Section, University of Pisa, 56124 Pisa, Italy 2 Department of Agriculture, Food, Environment and Forestry, University of Florence, 50144 Firenze, Italy; roberto.fratini@unifi.it (R.F.); fabio.boncinelli@unifi.it (F.B.) * Correspondence: [email protected] Abstract: Using spatial econometric techniques and local spatial statistics, this study explores the relationships between the real estate values in Tuscany with the individual perception of satisfaction by landscape types. The analysis includes the usual territorial variables such as proximity to urban centres and roads. The landscape values are measured through a sample of respondents who expressed their aesthetic-visual perceptions of different types of land use. Results from a multivariate local Geary highlight that house prices are not spatial independent and that between the variables included in the analysis there is mainly a positive correlation. Specifically, the findings demonstrate a significant spatial dependence in real estate prices. The aesthetic values influence the real estate price throughout more a spatial indirect effect rather than the direct effect. Practically, house prices in specific areas are more influenced by aspects such as proximity to essential services. The results seem to show to live close to highly aesthetic environments not in these environments. The results relating to the distance from the main roads, however, seem counterintuitive. This result probably depends on the evidence that these areas suffer from greater traffic jam or pollution or they are preferred for alternative uses such as for locating industrial plants or big shopping centres rather than residential Citation: Riccioli, F.; Fratini, R.; use. -

How to Reach Podere Ripi from PISA Airport Estimated Time 60 Minutes from Florence Estimated Time 60 Minutes

How to reach Podere Ripi Podere Ripi is in the locality of ULIGNANO, a fraction of Volterra, in the Province of Pisa. Not to be confused with the town of Ulignano to the north of San Gimignano, in the Province of Siena. From PISA Airport estimated time 60 minutes Take the highway called SGC FI-PI-LI following the blue signs towards FIRENZE Continue towards FIRENZE until you pass through the first tunnel Immediately after the tunnel take the exit for PONTEDERA (do not take the previous exit name Pontedera- Ponsacco also indicating Volterra). Follow the direction VOLTERRA on the SR 439, keep following directions for VOLTERRA on the SR439. When you reach the hotel and restaurant MOLINO D'ERA with a petrol IP station on your left. Turn to the left and then take your first right straight after a small bridge, follow signs towards COLLE VAL D'ELSA Keep driving on the SR 439 dir, after about 10 mins turn left to COZZANO SENSANO ULIGNANO. Ignore the first juntion to COZZANO and take the second indicating ULIGNANO Continue on this road that starts out as a paved road and then becomes a dirt road as it winds up the hill. You will pass the signs for Villa Scopicci and Villa di Ulignano/ Borgo della Speranza Keep going until you pass Agriturismo Caffagiolo. If you look left at this point you will see Podere Ripi from a distance. As the road curves to the right, TURN LEFT and down through a gate into our private driveway. Follow the long single track driveway until the end and park by the cypress trees. -

Pisa Town Council

PISA TOWN COUNCIL Building standards and urban redevelopment Town planning division INTERNATIONAL TOWN PLANNING COMPETITION ONE PHASE, WITH PRE-SELECTION “Urban redevelopment of the university hospital of Santa Chiara, facing Piazza dei Miracoli” 1. SUBJECT OF THE COMPETITION Pisa Town Council, hereinafter referred to as "the Caller", announces an international town planning competition through a restricted, anonymous single-phase procedure with pre-selection, for a Redevelopment plan, pursuant to Regional Act no. 1 of 3 January 2005, art. 73, at a level of detail as set forth in art. 5.5 of this Call, the subject of which is the development of a consistent plan for the urban redevelopment and the urban, landscaping and architectural enhancement of the area which comprises all the hospital buildings of Santa Chiara, including the university wards along Via Savi, through a systematic, consistent group of works to be carried out on such sites. The site of Santa Chiara (over 10 ha) is located in the heart of downtown Pisa and borders on the Cathedral Square (Piazza del Duomo), which is a UNESCO World Heritage site. The group of buildings, which dates back to 1257 and has been used since then as a hospital and university centre, will be dismantled and redeveloped; its functions will be relocated to a special area in the new city. The redevelopment plan shall be compatible with the applicable laws for the compilation of UNESCO heritage management plans. The urban redevelopment project is authorised under the Rule Sheet no. 27 of the Planning regulations of Pisa Town Council, approved with resolution C.C. -

Student Guide

THE BIOROBOTICS INSTITUTE SCUOLA SUPERIORE SANT’ANNA STUDENT GUIDE 2 THE BIOROBOTICS INSTITUTE - Student Guide Welcome to THE BIOROBOTICS INSTITUTE of SCUOLA SUPERIORE Scuola Superiore Sant'Anna was established in 1967 as the Scuola Superiore di Studi Universitari e di Perfezionamento after merging the Scuola per le Scienze Applicate A. Pacinotti (founded in 1951) and the Collegio Medico -Giuridico. In 1987 the Scuola Superiore Sant'Anna acquired complete independence both from the Scuola Normale and the University of Pisa. Scuola Superiore Sant'Anna is both a university in its own right, offering Masters and PhD courses, while for under gradu- ates it works as the Honors College of the University of Pisa. Po- tential under graduates undergo a rigorous public examination, and only the very best are creamed off to combine their Pisa Uni- versity studies with the extra options available at Scuola Superi- ore Sant'Anna, these students are called Honors College Stu- dents. Honors College Students live at the Scuola and study totally free of charge but have to get top marks in all their exams and show 3 THE BIOROBOTICS INSTITUTE - Student Guide In 2002 the ARTS and the CRIM Labs moved from Pisa to the Polo Sant'Anna Valdera (PSV), where the BioRobotics Institute is located today. The PSV was established by the Scuola Superiore Sant'Anna as a research park, in the industrial city of Pontedera, 25km from Pisa. The BioRobotics Institute is the result of a merge between ARTS Lab, CRIM Lab and EZ Lab; it is located at the Polo Sant'Anna Val- dera, which also houses an office of the Italian Institute of Tech- nology (MicroBioRobotics Center) and some joint research labs with leading universities in Japan and Korea. -

Tannery in Tuscany

TANNERY IN TUSCANY How the sector operates Within the Tuscan fashion system, the tannery and leather industry, concentrated in the typical industrial district of Santa Croce‐San Miniato, holds a highly relevant role in terms of turnover and employees. Although it constitutes a single production chain, the separation between raw material processing – vegetable tanning on the Arno’s left bank and chrome tanning on the right bank – and production of leather accessories – which also involves third‐party manufacturing – suggested the constitution of two focus groups. At national level, compared to the two still‐existing tanning industries of Arzignano and Solofra, the Tuscan district holds the highest market share and a substantial export quota, while tannery has basically disappeared elsewhere in Europe. The processing of hides and leather requires a complex multi‐phase process, which has been supported by territorial concentration and adjustment mechanisms occurred over time. The high price of raw hides and the increasing competition from Asia and Latin American (where environmental costs are evaded), together with the transformation of the fashion system, had a destabilizing effect, but the district has developed new entrepreneurial strategies at both individual and collective level. The distribution partnership with international labels have induced a speeding‐up of production, a quantity reduction and a very high product diversification. The variety of manufacturing operations and the larger portfolio of new product proposals require -

Lessons Learnt from Landslide Disasters in Europe

NEDIES PROJECT Lessons Learnt from Landslide Disasters in Europe Edited by Javier Hervás 2003 EUR 20558 EN ii NEDIES Series of EUR Publications Alessandro G. Colombo (Editor), 2000. NEDIES Project - Lessons Learnt from Avalanche Disasters, Report EUR 19666 EN , 14 pp. Alessandro G. Colombo (Editor) 2000. NEDIES Project - Lessons Learnt from Recent Train Accidents, Report EUR 19667 EN, 28 pp. Alessandro G. Colombo (Editor), 2001. NEDIES Project - Lessons Learnt from Tunnel Accidents, Report EUR 19815 EN, 48 pp. Alessandro G. Colombo and Ana Lisa Vetere Arellano (Editors), 2001. NEDIES Project - Lessons Learnt from Storm Disasters, Report EUR 19941 EN., 45 pp. Chara Theofili and Ana Lisa Vetere Arellano (Editors), 2001. NEDIES Project - Lessons Learnt from Earthquake Disasters that Occurred in Greece, Report EUR 19946 EN, 25 pp. Alessandro G. Colombo and Ana Lisa Vetere Arellano (Editors), 2002. NEDIES Project - Lessons Learnt from Flood Disasters, Report EUR 20261 EN, 91 pp. Alessandro G. Colombo, Javier Hervás and Ana Lisa Vetere Arellano, 2002. NEDIES Project – Guidelines on Flash Flood Prevention and Mitigation, Report EUR 20386 EN, 64 pp. Ana Lisa Vetere Arellano, 2002. NEDIES Project – Lessons Learnt from Maritime Disasters, Report EUR 20409 EN, 30 pp. Alessandro G. Colombo and Ana Lisa Vetere Arellano (Editors). Proceedings NEDIES Workshop - Learning our Lessons: Dissemination of Information on Lessons Learnt from Disasters (in press). Ana Lisa Vetere Arellano (Editor). Lessons Learnt from Forest Fire Disasters (in press). Javier Hervás (Editor). Recommendations to deal with Snow Avalanches in Europe (in press). iii LEGAL NOTICE Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use which might be made of the following information. -

Which Future for Small Towns? Interaction of Socio-Economic Factors and Real Estate Market in Irpinia

Which future for small towns? Interaction of socio-economic factors and real estate market in Irpinia Fabiana Forte*, Luigi Maffei**, keywords:small towns, Irpinia district, Pierfrancesco De Paola*** socioeconomic dynamics, real estate Abstract In the Italian territory most of small towns, which of research at the Department of Architecture and In- represent about 70% of the municipalities, are char- dustrial Design of University of Campania. In this acterized by “socio-economic marginality” and, perspective, the article, starting from the strategies, among the several reasons, the negative demo- tools and incentives currently available for the safe- graphic dynamics is one of the main causes. This guard and valorization of these territories, highlights phenomenon is particularly evident in the Irpinia dis- the socio-economic dynamics in some small munic- trict, approximately coincident with the province of ipalities of Irpinia, with particular reference to the ef- Avellino, in Campania Region, for a long time subject fects on the real estate market. 1. SMALL TOWNS IN IRPINIA: THE STALL OF empty, with several effects on the real estate market too. NATIONAL STRATEGY But small towns, because poor or depopulated, are also about 600 Italian municipalities with more 5.000 inhabi- “Small towns” constitute a relevant part of the Italian ter- tants (Lupatelli, 2016). Most of them are indeed character- ritory, representing about 70% of the municipalities, with ized by “socio-economic marginality” and, among the sev- a surface covering 55% of the national territory. According eral reasons, there is the negative trend of the population to Legambiente (2016) on a total of 5.497 small towns under 5.000 inhabitants, 2.430 are those who suffer a strong eco- that led to the depletion of human capital, especially nomic and demographic discomfort. -

Una Rete Castellare: Il Sistema Fortificato Irpino a Network of Castles: the Irpinian Fortified System

Defensive Architecture of the Mediterranean / Vol XII / Navarro Palazón, García-Pulido (eds.) © 2020: UGR ǀ UPV ǀ PAG DOI: https://dx.doi.org/10.4995/FORTMED2020.2020.11348 Una rete castellare: il sistema fortificato irpino A network of castles: the Irpinian fortified system Giovanni Coppola Università di Napoli “Suor Orsola Benincasa”, Naples, Italy, [email protected] Abstract In Irpinia, to grasp the extent to which the multiform and varied castellated density still has today, it is necessary to look at its hilly and mountainous landscapes or read the toponyms of its villages: from the recent study carried out in the Province of Avellino, there is a list of 78 castles still visible in elevation, a very high figure if you consider that the entire provincial territory is composed of 118 municipalities, for a percentage of almost 70%. The period of study in which this research is based on Irpinia’s fortification (castles, walls, towers and defensive walls) is part of the period in which the various foreign dynasties conquered the Regnum Si- ciliae giving rise to a military architecture which goes from the Longobard domination (568-774) to the advent of the Normans (1130-1194) and the Swabians (1194-1268), to retrace the phases of the coming first of the Angevins (1268-1435) and then of the Aragons (1442-1503). Keywords: castle, fortification, military architecture, medieval architecture, South Italy, Irpinia. L’armatura del sistema difensivo medievale irpino L’Irpinia è una multiforme e variegata “terra di niello, 2012). Durante gli anni successivi alla castelli” che ha risentito enormemente dei desti- caduta dell’Impero romano, il cosiddetto feno- ni dei tanti conquistatori e delle visioni politiche meno dell’incastellamento, dopo che lentamente che ne hanno disegnato i confini e guidato le i centri antichi di fondovalle si spopolavano, ini- sorti. -

The Monastery of Montevergine Its Foundation and Early Development

The Monastery of Montevergine Its Foundation and Early Development (1118-1210) Isabella Laura Bolognese Submitted in accordance with the requirements for the degree of Doctor of Philosophy The University of Leeds School of History September 2013 ~ i ~ The candidate confirms that the work submitted is her own and that appropriate credit has been given where reference has been made to the work of others. This copy has been supplied on the understanding that it is copyright material and that no quotation from the thesis may be published without proper acknowledgement. The right of Isabella Laura Bolognese to be identified as Author of this work has been asserted by her in accordance with the Copyright, Designs and Patents Act 1988. © 2013 The University of Leeds and Isabella Laura Bolognese ~ ii ~ ACKNOWLEDGMENTS What follows has been made possible by the support and guidance of a great many scholars, colleagues, family, and friends. I must first of all thank my supervisor, Prof. Graham Loud, who has been an endless source of knowledge, suggestions, criticism, and encouragement, of both the gentle and harsher kind when necessary, throughout the preparation and writing of my PhD, and especially for sharing with me a great deal of his own unpublished material on Cava and translations of primary sources. I must thank also the staff and colleagues at the Institute for Medieval Studies and the School of History, particularly those who read, commented, or made suggestions for my thesis: Dr Emilia Jamroziak and Dr William Flynn have both made important contributions to the writing and editing of this work. -

1 Abstract the Archaeological Map of The

Ancient Topography of the Mid Calore Valley: the City of Aeclanum and its Territory Immacolata Ditaranto Laboratory of Ancient Topography, Archaeology and Photogrammetry (LabTAF), University of Salento, Lecce, Italy email: [email protected] Abstract Keywords: Ancient Topography; Aerial Archaeol- ogy; Archaeological Map; Photogrammetry; Field The study area is located in the mid Calore valley, Survey. between the Calore and the Ufita Rivers. From prehistoric times, the territory has constituted an important crossroad among Campania, Apulia and The Archaeological Map of the City: Lucania, ensuring a connection between the Tyrre- Methodology and Results nian and Adriatic coast. The importance of the area grew with the construction of the via Appia, in the Most frequently the lack of suitable cartography third century BC. Along its route, as documented for archaeological research on the ground deter- by itinerary sources, in the early first century BC mines the need to create cartographic bases from the municipium of Aeclanum (Passo di Mirabella – scratch. All the more true and necessary when Mirabella Eclano, AV) was founded. A significant the research is related to ancient cities where the part of the research project regards this city: amount of remains on the surface is usually such archaeological field surveys were carried out in to require a base-map characterised by a good the urban area and along the city walls, still par- detail in scale and themes. The new aerophoto- tially preserved, with the aim to clarify its route. grammetric map of Aeclanum (Passo di Mirabella, The new collected data were georeferenced in an Mirabella Eclano, AV) was created, in the first aerophotogrammetric map, together with the data place, to fill in for the lack of updated cartogra- deriving from 1960s archaeological excavations phy. -

Curriculum Vitae Et Studiorum

Curriculum Vitae et Studiorum Marco Guerrazzi Date of birth: April 6th, 1974 Place of birth: Pontedera (Pisa), Italy Citizenship: Italian Office address Department of Economics – DIEC via F. Vivaldi, n. 5 16126 Genoa (GE) – Italy Phone +39-010-2095702 Fax +39-010-2095269 E-mail: [email protected] Research interests: Macroeconomics, Labour Economics, Economic Dynamics, Administrative Data. Current position December 2019 – present. Professor of Economic Policy (SECS P02). Department of Economics – DIEC, University of Genoa (Italy). Previous appointments August 2012 – Assistant Professor in Economics (SECS P01), Department of Economics – DIEC, University of November 2019 Genoa (Italy). May 2011 – July 2012 Research Fellow, Department of Economics and Management, Faculty of Political Sciences, University of Pisa (Italy). Title of the Research: Efficiency of Markets, Economic Development, Innovation (translated). November 2011 – Research Fellow, ISTAT, Department of Statistics Production and Technical-Scientific Coordinating December 2012 Committee, Rome (Italy). Title of the Research: INDACO-CVTS. CURRICULUM VITAE ET STUDIORUM – MARCO GUERRAZZI May – November 2010 Research Fellow, Department of Economics, Faculty of Political Sciences, University of Pisa (Italy). Title of the Research: Real and nominal rigidities and the functioning of the economic system (translated). January – July 2007 London School of Economics (London, UK) and the Open University (Milton Keynes, Walton Hall, UK). Visiting Research Fellow. March 2007 – February Research Fellow, Department of Economics, Faculty of Political Sciences, University of Pisa (Italy). 2010 Title of the Research: Real and nominal rigidities and the functioning of the economic system (translated). September 2005 – Research Fellow, Department of Economics, Faculty of Economics, University of Pisa (Italy). February 2007 Title of the Research: Labour force incentive in the presence of real and nominal rigidities. -

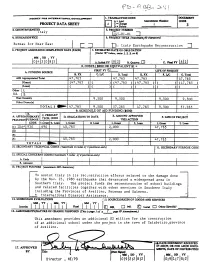

I "IIII I Ih KT'idi1__1~ 110~ [Fm 16

AGENCY FOR INTERNATIONAL DEVELOPMENT I. TRANSACTION CODE DOCUMENT A = Add Amendmet Number CODE PROJECT DATA SHEET CIAChance 3 __ D - Ddetc 2.COUNTRYErT aY S.PROJECT NUMBER OitalyY~t aLY5-81-01 --] 4. BUREAUIOFFICE 5. PROJECr TMrLZ (maMWXm,40 chatem) Bureau for Near East . Italy Earthquake Reconstruction -I 6. PROJECT ASSISTANCE COMPLETION DATE (PACD) 17. ESTIMATED DATE OF OBLIGATION (Under"B:"bdow, ewer, 2.3, or 4) MM IDD IYY1 I 1014131018151 jA IntialFY 18121 B.QuarteriC] c.l.F L4?Jy.U 8. COSTS ($000 OR EQUIVALENT $1 = A. FUNDING SOURCE FIRST FY 8 2. .LIFE OF PROJECT L FX C. L/C D. Total LFX P.C. G. Tota AD Appropriated Total 47,765 47,765 47,765 47,765 (Giant) (47,765 ) ( ) (47,765 ) (47,765 ) ( ) (47,765 (Loan) ( ) ( ) ( ) ( ) ( )( ( U.S. 2 Host Country 9,500 9 500 99500 9,500 Other Donor(s) TOTAL S 0 47,765 9,500 57,265 47,765 9,500 57,265 B._ C._PRIMARY _ 9. SCHEDULE OF AID FUNDING ($000) 1 A. APPRO PRMR C. PRIMARY E MUTAPOE PRIATION RPOSE TECH. CODE D. OBLIGATIONS TO DATE E AMOUNT APPROVED F. LIFE OF PROJECT PURPOSEI _________ THIS ACTION _____ _____ CODE 1.Grant 12. Loan 1. Grant 2. Loan 1. Grant 2. Loan 1. Grant 2. Loan (1)IDA* 930 690 45,765 2,000 47,765 (2) (3) -4) 45,765 2,000 47,765 TOTALS _____ 10. SECONDARY TECHNICAL CODES (maximum codes of 3position: each) 11. SECONDARY PURPOSE CODE S. 11T 12. SPECIAL CONCERNS CODES (maximum 7 codes of 4 positions each) A.I I I I I I B.