Investor Day 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Intraday Herding on a Cross-Border Exchange

CORE Metadata, citation and similar papers at core.ac.uk Provided by CURVE/open Intraday Herding on a Cross-Border Exchange Andrikopoulos, P, Kallinterakis, V, Pedro Leite Ferreira, M & Verousis, T Author post-print (accepted) deposited by Coventry University’s Repository Original citation & hyperlink: Andrikopoulos, P, Kallinterakis, V, Pedro Leite Ferreira, M & Verousis, T 2017, 'Intraday Herding on a Cross-Border Exchange' International Review of Financial Analysis, vol 53, pp. 25-36 https://dx.doi.org/10.1016/j.irfa.2017.08.010 DOI 10.1016/j.irfa.2017.08.010 ISSN 1057-5219 Publisher: Elsevier NOTICE: this is the author’s version of a work that was accepted for publication in International Review of Financial Analysis. Changes resulting from the publishing process, such as peer review, editing, corrections, structural formatting, and other quality control mechanisms may not be reflected in this document. Changes may have been made to this work since it was submitted for publication. A definitive version was subsequently published in International Review of Financial Analysis, [53, (2017)] DOI: 10.1016/j.irfa.2017.08.010 © 2017, Elsevier. Licensed under the Creative Commons Attribution- NonCommercial-NoDerivatives 4.0 International http://creativecommons.org/licenses/by-nc-nd/4.0/ Copyright © and Moral Rights are retained by the author(s) and/ or other copyright owners. A copy can be downloaded for personal non-commercial research or study, without prior permission or charge. This item cannot be reproduced or quoted extensively from without first obtaining permission in writing from the copyright holder(s). The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the copyright holders. -

Singapore Exchange Limited

18 October 2016 Asia Pacific/Singapore Equity Research Diversified Financial Services Singapore Exchange Limited (SGXL.SI / SGX SP) Rating NEUTRAL Price (14 Oct 16, S$) 7.25 INITIATION Target price (S$) 7.60 Upside/downside (%) 4.8 Mkt cap (S$/US$ mn) 7,769 / 5,589 Lacks near-term catalysts Enterprise value (S$ mn) 6,887 Number of shares (mn) 1,072 ■ We initiate coverage on Singapore Exchange with a NEUTRAL rating Free float (%) 71.3 and target price of S$7.60. The key investment case for SGX is longer-term 52-wk price range (S$) 8.05-6.65 ADTO-6M (US$ mn) 10.3 growth through both equities and success in its strategy to become an Asian *Stock ratings are relative to the relevant country benchmark. regional gateway, with derivatives being the medium-term driver, in our view. ¹Target price is for 12 months. Nearer-term, its fortunes are more linked to the current level of market activity, Research Analysts which remains uninspiring, with a risk of further seasonal slowdown in 4Q. Rikin Shah 65 6212 3098 ■ Securities business remains subdued. Securities turnover and revenue hit [email protected] the decade low in FY16. The subdued turnover is mainly a result of declining velocity (peak-to-date -43%), but a dearth of IPOs and an increase in privatisation deals have further exacerbated the situation. We discuss a few structural drivers like higher free float and high frequency trading, which could improve velocity in the long term. ■ Derivatives growth secular and less volatile. Derivatives' revenue growth of 18% CAGR in the past five years has been a great stabiliser—more than offsetting a 7% fall in securities revenue. -

Filed by the NASDAQ OMX Group, Inc

Filed by The NASDAQ OMX Group, Inc. (Commission File No. 000-32651) Pursuant to Rule 425 under the Securities Act of 1933, as amended Subject Company: NYSE Euronext (Commission File No. 001-33392) NASDAQ OMX and ICE Issue Joint Statement on Superior Proposal New York, NY and Atlanta, GA (April 25, 2011) NASDAQ OMX (NDAQ) and IntercontinentalExchange (ICE) today issued a joint statement with regard to their superior proposal for NYSE Euronext: NYSE Euronext investors should be highly skeptical that after two years of exploratory merger discussions, including more than six months dedicated to finalizing the transaction, NYSE Euronext has suddenly found a reported €100 million in additional synergies. This increase appears not to be a matter of sharpening a pencil, but an unexplained shift in strategy. The discovery that initial synergies having been understated by one-third comes after receiving a superior proposal from NASDAQ OMX and ICE that achieves greater synergies. Importantly, if there are additional synergies to be found after the merger economics have been agreed, then it has to come at the expense of NYSE Euronext stockholders because there has been no increase in the price they are being offered. NYSE Euronext should describe these newly-found synergies in detail in order to support the credibility of these revised estimates, particularly in light of commitments to retain two technology platforms and two headquarters. Increasingly it appears that NYSE Euronext is more focused on protecting the transaction than its stockholders. NASDAQ OMX and ICE have described in detail our proven and focused long-term strategy from which stockholders would benefit and our companies demonstrated outperformance relative to their proposed strategy of creating a financial supermarket. -

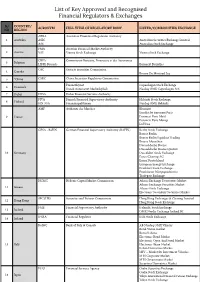

List of Key Approved and Recognised Financial Regulators & Exchanges

List of Key Approved and Recognised Financial Regulators & Exchanges S/ COUNTRY/ ACRONYM FULL TITLE OF REGULATORY BODY LISTED/COMMODITIES EXCHANGE NO REGION APRA Australian Prudential Regulation Authority 1 Australia ASIC Australian Securities Exchange Limited ASE Australian Stock Exchange FMA Austrian Financial Market Authority 2 Austria VSE Vienna Stock Exchange Vienna Stock Exchange CBFA Commission Bancaire, Financiere et des Assurances 3 Belgium LIFFE Brussels Euronext Bruxelles OSC Ontario Securities Commission 4 Canada Bourse De Montreal Inc 5 *China CSRC China Securities Regulatory Commission Finanstilsynet Copenhagen Stock Exchange 6 Denmark Dansk Autoriseret Markedsplads Nasdaq OMX Copenhagen A/S 7 Dubai DFSA Dubai Financial Services Authority FIVA Finnish Financial Supervisory Authority Helsinki Stock Exchange 8 Finland FIN-FSA Finansinspektionen Nasdaq OMX Helsinki AMF Authorite des Marches Bluenext Eurolist by Euronext Paris 9 France Euronext Paris Matif Euronext Paris Monep LCH SA GFSA - BaFIN German Financial Supervisory Authority (BAFIN) Berlin Stock Exchange Boerse Berlin Boerse Berlin Equiduct Trading Boerse Muenchen Duesseldorfer Boerse Duesseldorfer Boerse Quotrix 10 Germany Dusseldorf Stock Exchange Eurex Clearing AG Eurex Deutschland European Energy Exchange Frankfurt Stock Exchange Frankfurter Wertpapierboerse Tradegate Exchange HCMC Hellenic Capital Market Commission Athens Exchange Derivatives Market Athens Exchange Securities Market 11 Greece Athens Stock Exchange Electronic Secondary Securities Market SFC (HK) -

Intercontinental Exchange Reports Ice and Nyse May Volume

INVESTORS INTERCONTINENTAL EXCHANGE REPORTS ICE AND NYSE MAY VOLUME Released : 04 June 2014 ATLANTA--(BUSINESS WIRE)-- Intercontinental Exchange, Inc. (NYSE: ICE), the leading global network of exchanges and clearing houses, today reported exchange traded volumes for May 2014. ICE’s May average daily volume (ADV) was 5.4 million contracts, a decrease of 15% compared to May 2013. • Commodity futures and options ADV decreased 23% in May due primarily to continued low price volatility across most energy products. • Financial futures and options ADV decreased 9% in May due primarily to the low interest rate environment in Europe. This was partially offset by a 23% increase in equity derivatives ADV year to year, including a 32% increase in Liffe single stock futures. • NYSE cash equities ADV decreased 13% and Euronext cash equities ADV was flat compared to the prior May. NYSE equity options volume decreased 23% year to year. ICE Futures & Options ADV (contracts in 000s) ADV May ADV May Change ADV YTD ADV YTD Change May ’13 2014 2013 y/y May ‘14 y/y COMMODITIES Energy Brent 594 670 -11% 617 712 -13% Gasoil 214 266 -19% 220 272 -19% Other Oil (1) 248 244 2% 254 255 0% TOTAL OIL 1,055 1,179 -10% 1,092 1,239 -12% Natural Gas (2) 714 1,241 -42% 983 1,363 -28% Power (3) 131 141 -7% 130 144 -10% Emissions & Other (4) 32 30 6% 48 46 5% TOTAL ENERGY 1,932 2,591 -25% 2,252 2,792 -19% Agricultural Sugar (5) 115 113 1% 167 146 15% Other Ags & Metals (6) 156 162 -4% 192 188 2% TOTAL AGRICULTURAL & METALS 270 276 -2% 360 334 8% TOTAL COMMODITIES 2,203 2,867 -23% 2,612 3,125 -16% FINANCIALS Interest Rates Short-term Interest Rates (7) 1,729 2,213 -22% 1,761 2,312 -24% Medium & Long-term Interest Rates (8) 195 233 -16% 177 192 -8% TOTAL INTEREST RATES 1,924 2,445 -21% 1,938 2,504 -23% TOTAL EQUITY DERIVATIVES (9) 1,297 1,058 23% 1,051 1,170 -10% TOTAL FX (10) 20 43 -54% 24 38 -38% TOTAL FINANCIALS 3,241 3,547 -9% 3,012 3,712 -19% TOTAL FUTURES & OPTIONS 5,444 6,414 -15% 5,625 6,837 -18% Note: Figures may not foot due to rounding. -

Equity Markets USD 47 Tn

19 January 2012 2011 WFE Market Highlights 2011 equity volumes remained stable despite a fall in market capitalization. Derivatives, bonds, ETFs, and securitized derivatives continued to grow strongly. Total turnover value remained stable in 2011 at USD 63 tn despite a sharp decrease of the global market capitalization (-13.6% at USD 47 tn). High volatility and global uncertainty created from the sovereign debt crisis affected volumes all year through and made August 2011 the most active month in terms of trading value, a highly unusual annual peak for markets. Despite overall unfavorable conditions for primary markets in several regions, WFE members increased their total listings by 1.7% totaling 45 953 companies listed. Total number of trades decreased by 6.4% at 112 tn. This trend combined with the stability of turnover value led to a small increase in the average size of transaction which was USD 8 700 in 2011. The high volatility and lack of confidence that affected financial markets globally probably drove the needs of hedging as derivatives contracts traded grew by 8.9%. WFE members continued to diversify their products range as other products such as bonds, ETFs, and securitized derivatives all had solid growth in 2011. Equity Markets Market capitalization USD 47 tn -13.6% Domestic market capitalization declined significantly in 2011 to USD 47 401 bn roughly back to the same level of end 2009. The decline affected almost all WFE members, as there were only four exchanges ending 2011 with a higher market capitalization. The magnitude of the decline is quite similar among the three time zones: -15.9% in Asia-Pacific, -15.2% in EAME and -10.8% in the Americas. -

Annotated Presentation of Regulated Markets and National Provisions

15.7.2011 EN Official Journal of the European Union C 209/21 Annotated presentation of regulated markets and national provisions implementing relevant requirements of MiFID (Directive 2004/39/EC of the European Parliament and of the Council) (2011/C 209/13) Article 47 of the Markets in Financial Instruments Directive (Directive 2004/39/EC, OJ L 145, 30.4.2004) authorises each Member State to confer the status of ‘regulated market’ on those markets constituted on its territory and which comply with its regulations. Article 4, paragraph 1, point 14 of Directive 2004/39/EC defines a ‘regulated market’ as a multilateral system operated and/or managed by a market operator, which brings together or facilitates the bringing together of multiple third-party buying and selling interests in financial instruments — in the system and in accordance with its non-discretionary rules — in a way that results in a contract, in respect of the financial instruments admitted to trading under its rules and/or systems, and which is authorised and functions regularly and in accordance with the provisions of Title III of Directive 2004/39/EC. Article 47 of Directive 2004/39/EC requires that each Member State maintains an updated list of regulated markets authorised by it. This information should be communicated to other Member States and the European Commission. Under the same article (Article 47 of Directive 2004/39/EC), the Commission is required to publish a list of regulated markets, notified to it, on a yearly basis in the Official Journal of the European Union. The present list has been compiled pursuant to this requirement. -

Sanli Bags New Contracts in Singapore and Myanmar; Boosts Order Book to S$198.0 Million

SANLI ENVIRONMENTAL LIMITED MEDIA RELEASE For Immediate Release Sanli bags new contracts in Singapore and Myanmar; boosts order book to S$198.0 million S$7.8 million O&M contract wins from the Singapore Public Utilities Board reflects the continued confidence the public sector has in the Group’s capabilities Expansion into Myanmar is progressing well, as the Group secures EPC contracts worth approximately S$4.3 million Order book stands at S$198.0 million SINGAPORE, 2 April 2019 – Sanli Environmental Limited (“Sanli” and together with its subsidiaries, the “Group”), one of Singapore’s leading environmental engineering companies, is pleased to announce that it has recently secured new contracts (“Contracts”) in Singapore and Myanmar, worth a total of approximately S$12.1 million. With these contract wins, the Group’s order book stands at S$198.0 million. These new contracts are expected to contribute to Sanli’s revenue from the financial year ending 31 March 2020 (“FY2020”). The Operations and Maintenance (“O&M”) contracts are awarded by the Singapore Public Utilities Board (“PUB”). Spanning over a period of three years from March 2019, Sanli will be involved in the refurbishment of centrifugal pumps in the NEWater Factories and Waterworks, the overhaul of centrifugal pumps, disintegrators and related equipment and maintenance works at various PUB installations, as well as the maintenance of electrical equipment at the Johor Plants. Sanli had also secured two Engineering, Procurement and Construction (“EPC”) contracts from the Myanmar government, worth a total of 4.9 billion Myanmar Kyat (Ks) or SANLI ENVIRONMENTAL LIMITED approximately S$4.3 million. -

Evidence from the Singapore Stock Market Q

Available online at www.sciencedirect.com Journal of Banking & Finance 32 (2008) 2205–2219 www.elsevier.com/locate/jbf How does the call market method affect price efficiency? Evidence from the Singapore Stock Market q Rosita P. Chang a, S. Ghon Rhee a,b, Gregory R. Stone c, Ning Tang d,* a Shidler College of Business, University of Hawaii, 2404 Maile Way, Honolulu, HI 96822-2282, USA b Sung Kyun Kwan University Business School, Seoul, South Korea c College of Business Administration, University of Nevada, Reno, Mail Stop 028, Reno, NV 89557, USA d School of Business and Economics, Wilfrid Laurier University, Waterloo, ON, Canada N2L 3C5 Received 23 November 2006; accepted 27 December 2007 Available online 12 January 2008 Abstract On August 21, 2000, the Singapore Exchange (SGX) adopted the call market method to open and close the market while the remain- der of the day’s trading continued to rely on the continuous auction method. The call method significantly improved the price discovery process and market quality. A positive spillover effect is observed from the opening and closing calls. Day-end price manipulation also declined after the introduction of the call market method. However, the beneficial impact from the call market method is asymmetric, benefiting liquid stocks more than illiquid stocks. Ó 2008 Elsevier B.V. All rights reserved. JEL classification: G14; G15; G18 Keywords: Market mechanism; Call method; Price efficiency; Trading noise; Return reversals; Price manipulation; Singapore Exchange 1. Introduction tion which interacts with the existing quote-driven trading mechanism and subsequently introduced an opening call Schwartz (2000) correctly predicted that with advances auction later that same year. -

Capital Flows and Exchange Rate Volatility: Singapore's Experience

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Capital Controls and Capital Flows in Emerging Economies: Policies, Practices and Consequences Volume Author/Editor: Sebastian Edwards, editor Volume Publisher: University of Chicago Press Volume ISBN: 0-226-18497-8 Volume URL: http://www.nber.org/books/edwa06-1 Conference Date: December 16-18, 2004 Publication Date: May 2007 Title: Capital Flows and Exchange Rate Volatility: Singapore’s Experience Author: Basant K. Kapur URL: http://www.nber.org/chapters/c0161 12 Capital Flows and Exchange Rate Volatility Singapore’s Experience Basant K. Kapur 12.1 Introduction Singapore’s experience with international capital flows over the past two decades or so has been a rather—although not completely—benign one, owing to strong fundamentals and generally well-conceived macroeco- nomic policies. At the same time, useful lessons can be learned regarding issues such as exchange rate policy, the policy of noninternationalization of the Singapore dollar, and unavoidable fallout effects of capital flow volatil- ity even in generally sound environments and how these may best be dealt with. A feature of Singapore’s economy that sets it apart from various other countries discussed in this volume is its well-developed banking system and equities market, and the fact that it is on a (modified) currency board (CB) system. Its bond market is, however, less developed, although in recent years measures have been taken to foster its growth, as discussed below. It may be useful, therefore, to begin by comparing Singapore’s experience with that of another state with a well-developed financial system, namely Hong Kong: the latter, in addition, operates what may be termed a “pure” CB system. -

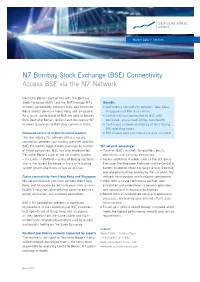

N7 Bombay Stock Exchange (BSE) Connectivity Access BSE Via the N7 Network

Market Data + Services N7 Bombay Stock Exchange (BSE) Connectivity Access BSE via the N7 Network Deutsche Börse’s partnership with the Bombay Stock Exchange (BSE) sees the BSE leverage N7’s Benefi ts network connectivity between India and Deutsche Low latency connectivity between Hong Kong, Börse access points in Hong Kong and Singapore. Singapore and BSE data centres As a result, participants of BSE are able to benefit Carrier-resilient connection to BSE with from Deutsche Börse’s resilient and low latency N7 dedicated, guaranteed 2Mbps bandwidth network to connect to BSE data centres in India. Continuous network monitoring of lines during BSE operating hours Improved access to Indian fi nancial markets BSE market feed and interactive data available The low latency N7 network offers a secure connection between your trading premises and the BSE, the world’s biggest stock exchange by number N7 network advantages of listed companies. BSE has also implemented Trade on BSE’s markets for equities, equity Deutsche Börse’s state-of-the-art trading system derivatives and currency derivatives. – the Eurex T7 Platform – across all trading segments Access additional markets such as the SIX Swiss and is the fastest Exchange in India with trading Exchange, the Singapore Exchange and the Central & system processing times as low as 200 µs. Eastern European Stock Exchange Group (CEESEG) over one physical line, leveraging the use of existing Faster connectivity from Hong Kong and Singapore network infrastructure and hardware components Market participants can now connect their Hong Work with a single contractual partner, well Kong and Singapore-based trade execution systems established and experienced in network operations to BSE’s fully regulated offering covering equities, and specialised in financial technology equity derivatives and currency derivatives. -

Bonds Denominated in USD to List for the First Time on NYSE Euronext Lisbon Market BPI Quotes 12 Million on 12Th of March

CONTACT | Media: CONTACT | Investor Relations: +31.20.550.4488 (Amsterdam), +32.2.509.1392 (Brussels) +1.212.656.5700 (New York) +351.217.900.029 (Lisbon), +44.20.7379.2789 (London) +33.1.49.27.58.60 (Paris) +1.212.656.2411 (New York), +33.1.49.27.11.33 (Paris) Bonds denominated in USD to list for the first time on NYSE Euronext Lisbon market BPI quotes 12 million on 12th of March March 11, 2010 – NYSE Euronext (NYX) is pleased to welcome Banco Português de Investimento as the first listed issuer of non-euro currency on Euronext Lisbon. Banco Português de Investimento, a company with a market capitalization of € 1.750 billion, will list two bond issues denominated in USD on the Lisbon market of NYSE Euronext on 12th March 2010: • an issue of USD 6 million of Index Linked Interested Notes “BPI AMERICAN OUTPERFORMANCE 2010-2013” and • an issue of USD 6 million of Index Linked Interest Notes “BPI JPYUSD 350% 2010- 2013”. Both bonds will be issued under the BPI’s Euro Medium Term Note Programme. The listing of these two new products will see the start of a service to trade non-Euro currency via NYSE Euronext in Lisbon. The non-Euro settlement service will be provided by Interbolsa using the non-Euro payment system operated by Caixa Geral de Depósitos. Trading member firms will need to have a clearing member firm (CMF) and a settlement agent (SA) with a settlement account at Interbolsa for the securities side and an account with Caixa Geral de Depósitos for the cash side of the settlement process.